There is more muttering about a September Fed hike:

Traders have never been more convinced of a September rate hike by the Federal Reserve.

The chances of an interest-rate increase next month reached 52 percent Wednesday, up from just 38 percent just two days earlier. What’s fueled the change of heart? Hawkish comments from Fed Bank of Atlanta President Dennis Lockhart on Tuesday, and a surprisingly strong report on U.S. service-sector growth Wednesday morning.

…

Yields on Treasury one-month bills rose Wednesday to the highest since November, while those on two-year notes touched the highest since 2011. Longer maturities slumped as well. Benchmark 10-year yields added five basis points to 2.27 percent.

But historical rules may not apply in this peculiar world:

Treasury two-year yields of just 0.73 percent are low historically, yet they’re looking better and better compared with the alternatives.

The U.S. yield is almost 1 percentage point more than its German counterpart, which is negative 0.25 percent. The premium reached the most this week since 2007. Against Canada, the spread was as much as 33 basis points on Aug. 4, also the most in eight years.

…

While the Fed is getting ready to raise rates, the European Central Bank is buying government bonds to support the economy by putting downward pressure on borrowing costs. The Bank of Canada cut interest rates twice this year.

Yesterday I reported on SEC Commissioner Daniel M. Gallagher’s harsh words reporting Dodd-Frank. Today there’s some more Dodd-Frank idiocy:

The Securities and Exchange Commission today adopted a final rule that requires a public company to disclose the ratio of the compensation of its chief executive officer (CEO) to the median compensation of its employees. The new rule, mandated by the Dodd-Frank Wall Street Reform and Consumer Protection Act, provides companies with flexibility in calculating this pay ratio, and helps inform shareholders when voting on “say on pay.”

This social engineering was endorsed by Commissioner Kara M. Stein, Commissioner Luis A. Aguilar and Chair Mary Jo White, who noted:

To say that the views on the pay ratio disclosure requirement are divided is an obvious understatement. Since it was mandated by Congress, the pay ratio rule has been controversial, spurring a contentious and, at times, heated dialogue. The Commission has received more than 287,400 comment letters, including over 1,500 unique letters, with some asserting the importance of the rule to shareholders as they consider the issue of appropriate CEO compensation and investment decisions, and others asserting that the rule has no benefits and will needlessly cause issuers to incur significant costs.

These differences in views were evident at the time the Commission voted to propose the pay ratio rule. That the Commission was even considering the rule proposal was, for example, criticized as contrary to our mission. We may hear similar thoughts today.

So the three Democrats supported the measure, but the two Republicans opposed it; our friend Commissioner Daniel M. Gallagher stated:

The release does an impressive job of creating out of whole cloth a rationale for this rule: that it could help inform investors in their oversight of executive compensation, including say-on-pay votes.[1] But, to steal a line from Justice Scalia, this is pure applesauce.[2] The purpose of this rule is not to inform a reasonable investor’s voting or investment decision.[3] The AFL-CIO, which lobbied for the rule’s inclusion in Dodd-Frank, has explained for us its true purpose: “Disclosing this pay ratio will shame companies into lowering C.E.O. pay.”[4] And, “They will be embarrassed, and that’s the whole point.”[5] But addressing perceived income inequality is not the province of the securities laws or the Commission. And yet here we are, on the cusp of adopting a nakedly political rule that hijacks the SEC’s disclosure regime to once again effect social change desired by ideologues and special interest groups.

* * *

As an initial matter, we did not have to take up this rule today. Section 953(b) of Dodd-Frank does not have a statutory deadline. There are other, more pressing matters for the Commission, including policymaking with respect to matters actually involving the SEC’s core mission. On the occasion of Dodd-Frank’s fifth anniversary, many have spoken about the law as a fait accompli. But that is far from the truth at the SEC.[6] For example, we have not completed our implementation of Title VII,[7] and we are way past the statutory deadline for adopting mandated rules on stock lending transparency. This rulemaking may well be the most useless of all our Dodd-Frank mandates — that really says something — and it warranted the “caboose” treatment.

and Commissioner Michael S. Piwowar said:

Today’s rulemaking implements a provision of the highly partisan Dodd-Frank Act[2] that pandered to politically-connected special interest groups and, independent of the Act, could not stand on its own merits.[3] I am incredibly disappointed the Commission is stepping into that fray.

Section 953(b) of Dodd-Frank simply has nothing to do with protecting investors, ensuring fair, orderly, and efficient markets, or facilitating capital formation. The proposing release is candid about the fact that “neither the statute nor the related legislative history directly states the objectives or intended benefits of the provision or of a specific market failure, if any, that is intended to be remedied.”[4]

…

The timing of this vote is quite peculiar given the recent moves by Congress to repeal the pay-ratio provision. Last week, six more co-sponsors signed on to a bill introduced in the House by Representative Bill Huizenga of Michigan to repeal Section 953(b), bringing the total number of co-sponsors to 23 members.[32] Less than a month ago, Senator Mike Rounds of South Dakota introduced a pay-ratio repeal bill in the Senate, which added a co-sponsor two days ago.[33] It does not seem coincidental that our open meeting was scheduled for the week after the House of Representatives adjourned for August recess and one day before the Senate is expected to do the same.[34]

But it ain’t over ’til it’s over … and that might be a while:

Even so, Republicans and business groups still oppose the requirement and said the SEC ignored some of their recommendations to improve it. Groups such as the U.S. Chamber of Commerce or the Business Roundtable are expected to sue the agency over the rule.

“We will continue to review the rule and explore our options for how best to clean up the mess it has created,” the chamber’s David Hirschmann said in a statement Wednesday.

The whole thing is as crazy as it would be to get the securities regulators to encourage greater representation by women on boards and in positions of senior management … oh, wait … we’ve done that … it was a request of the Ontario government. Well, at least it reassures us that everything is perfect in InvestmentLand!

Wonder of wonders, it was a good day for the Canadian preferred share market, something I haven’t had much opportunity to say in he past three months! PerpetualDiscounts gained 29bp, FixedResets won 62bp and DeemedRetractibles were up 32bp. The Performance Highlights table is lengthy and very heavily tilted towards winners. Volume was below average.

PerpetualDiscounts now yield 5.43%, equivalent to 7.06% interest at the standard equivalency factor of 1.3x. Long corporates now yield about 4.0%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 305bp, a significant increase from the 295bp reported July 29.

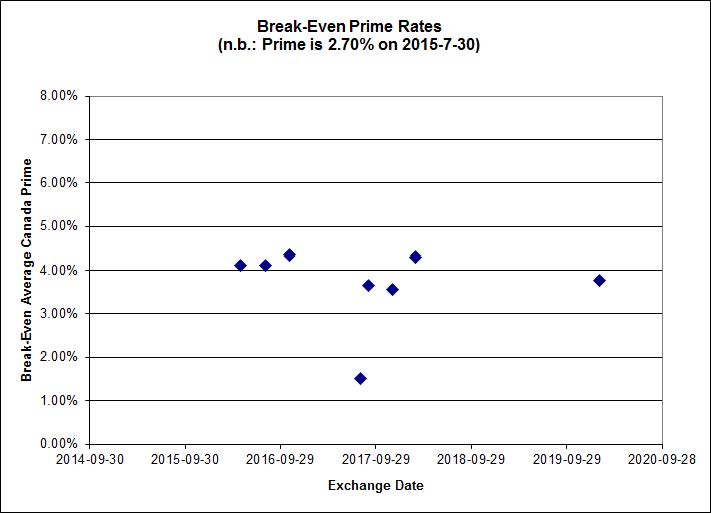

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

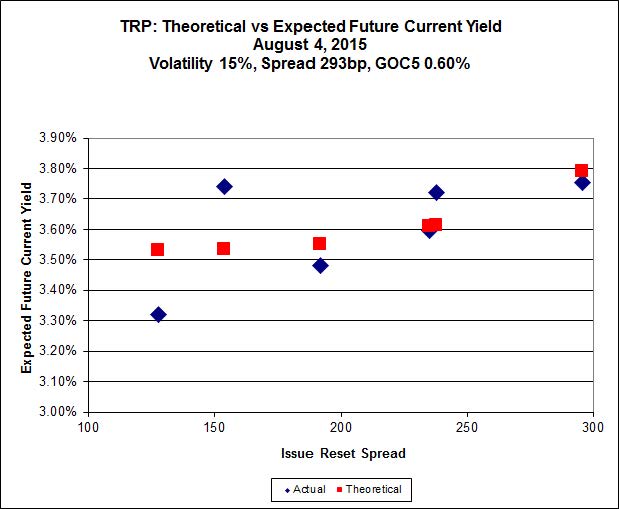

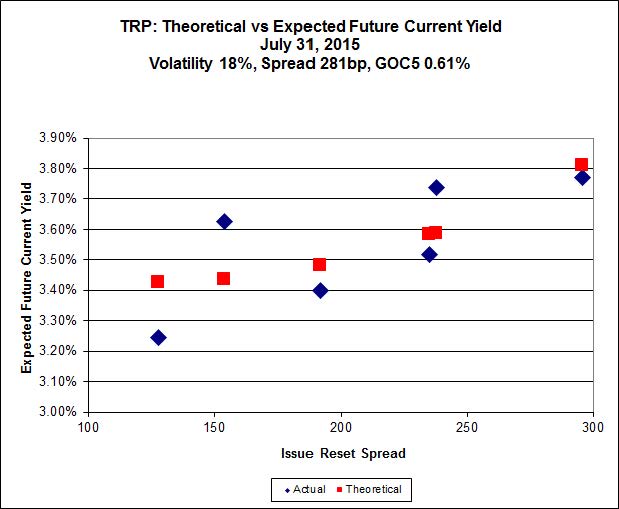

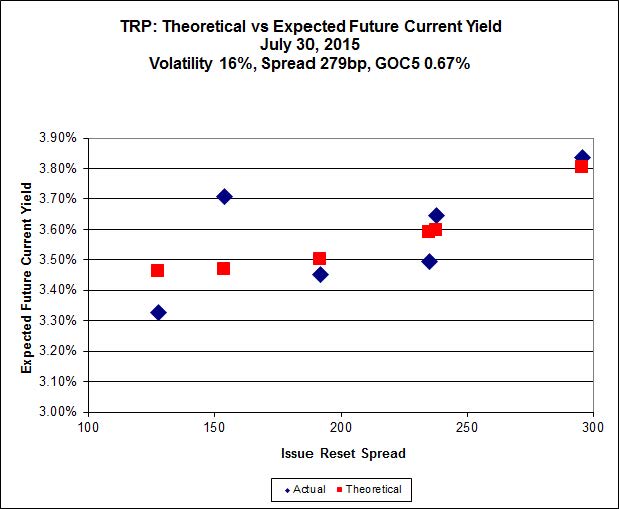

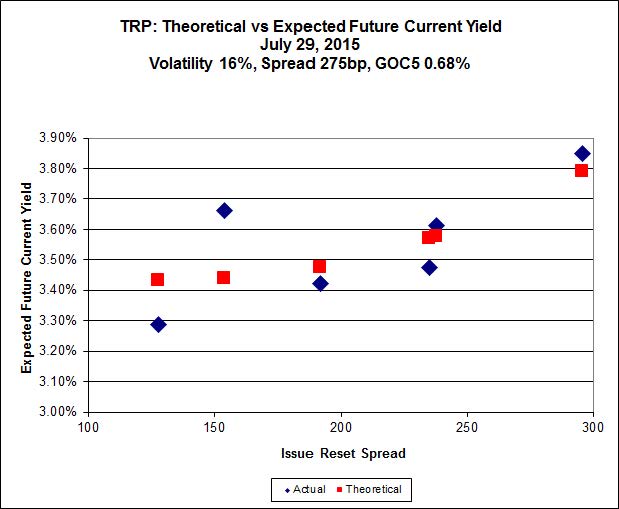

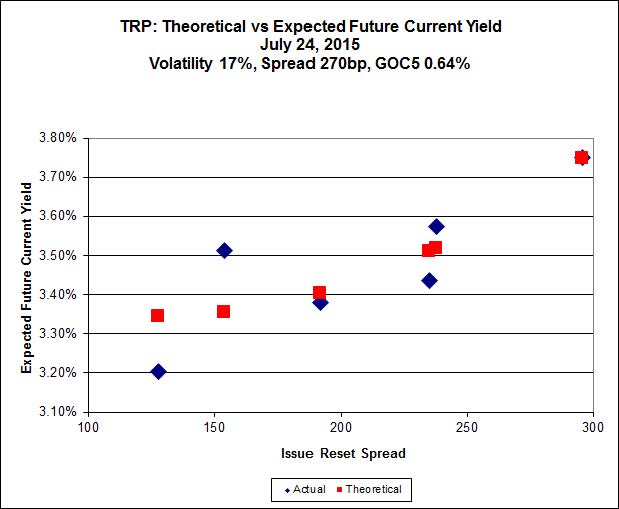

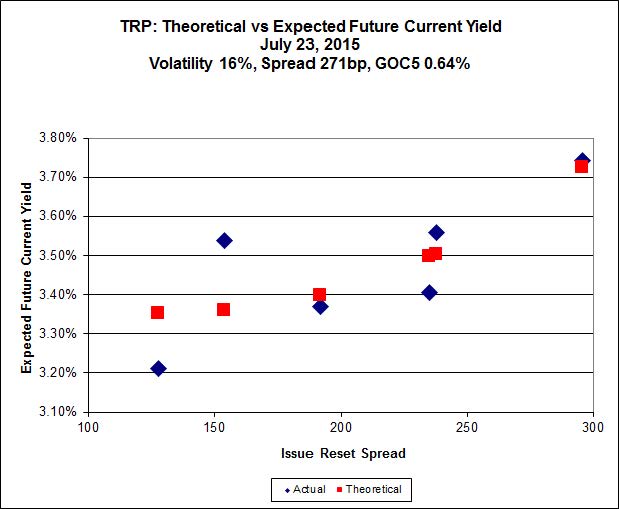

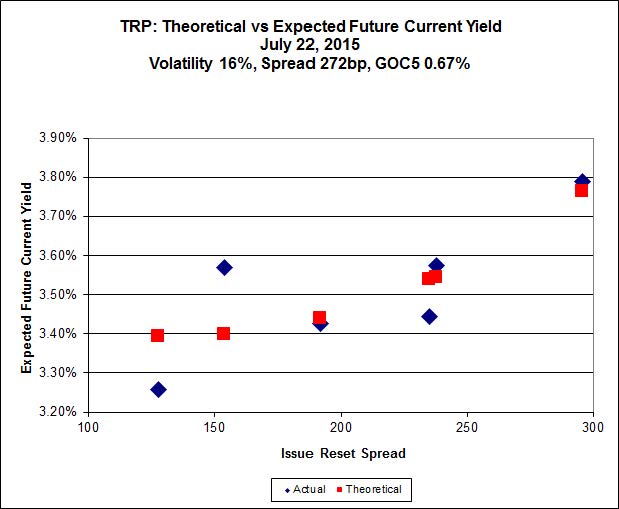

Here’s TRP:

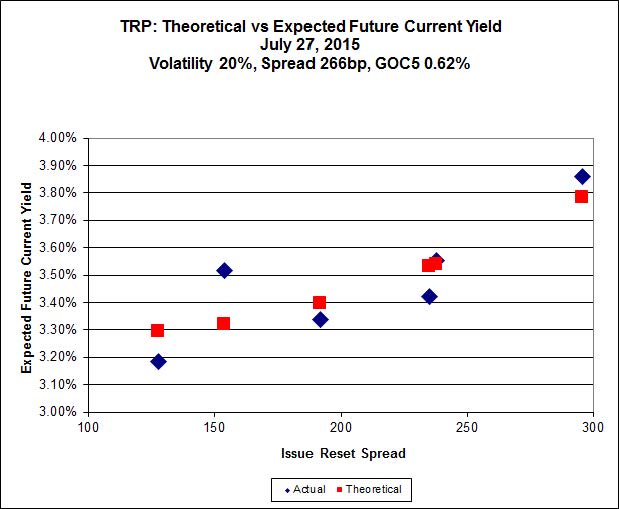

Click for Big

TRP.PR.B, which resets 2020-6-30 at +128, is bid at 14.06 to be $0.46 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.81 cheap at its bid price of 14.36.

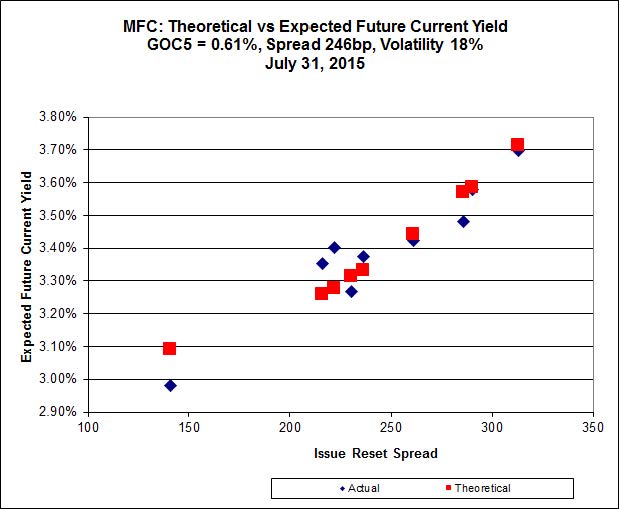

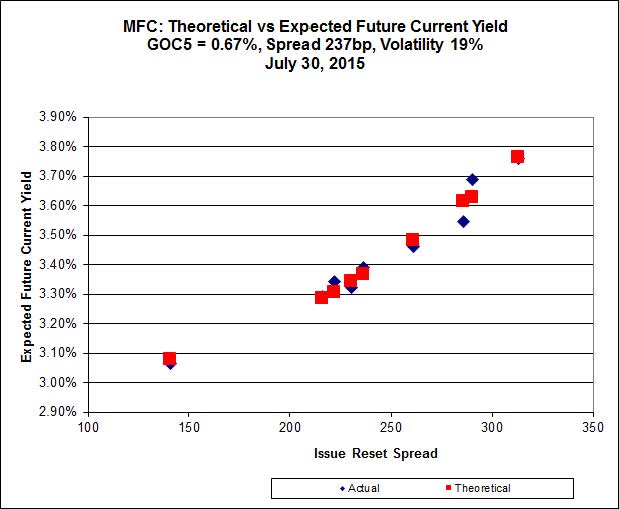

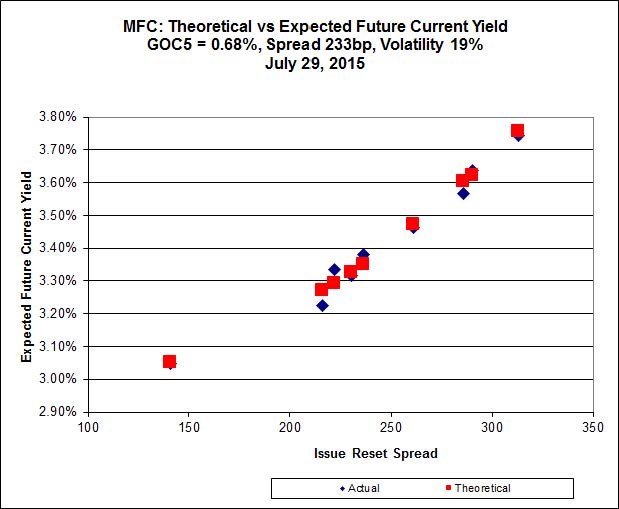

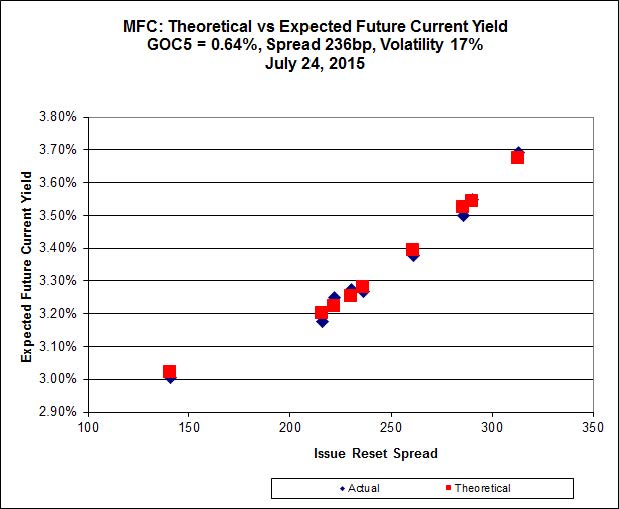

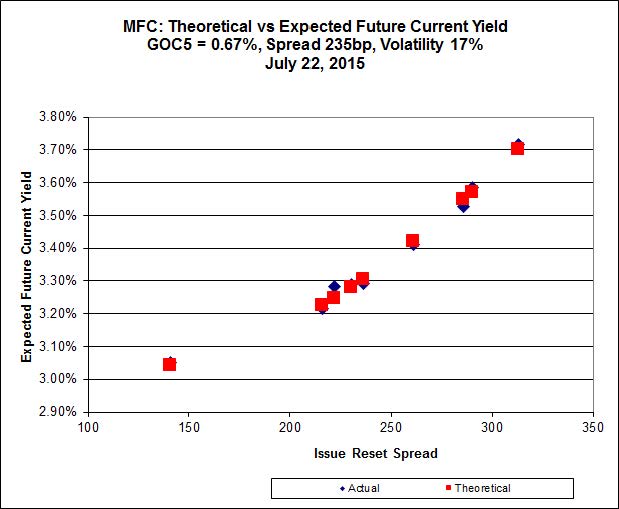

Click for Big

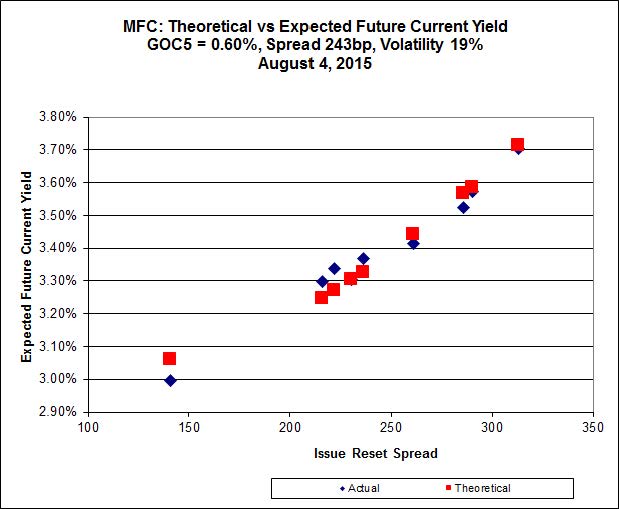

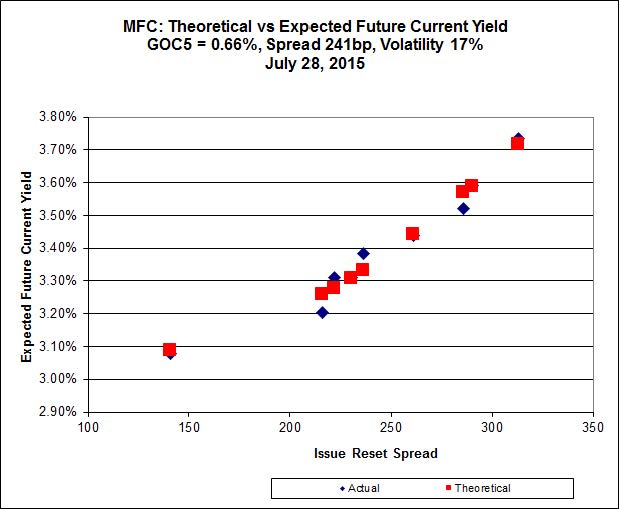

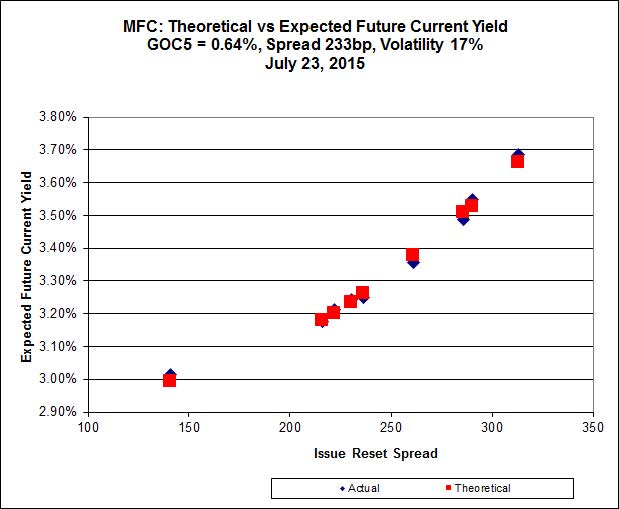

Another good fit today!

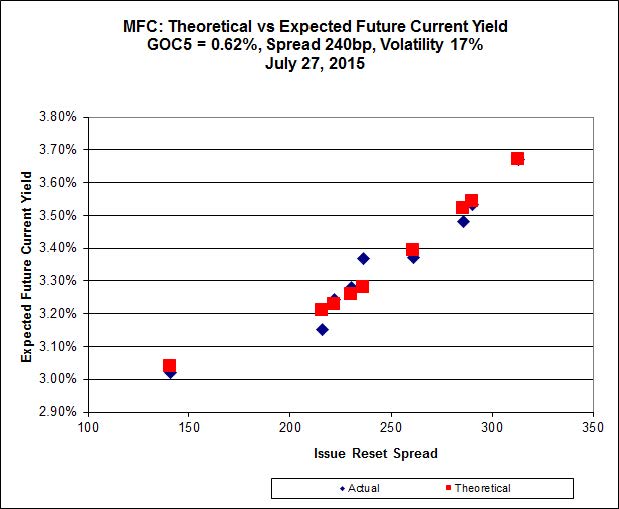

Most expensive is MFC.PR.I, resetting at +286bp on 2017-9-19, bid at 24.85 to be 0.59 rich, while MFC.PR.K, resetting at +222bp on 2018-9-19, is bid at 21.20 to be $0.42 cheap.

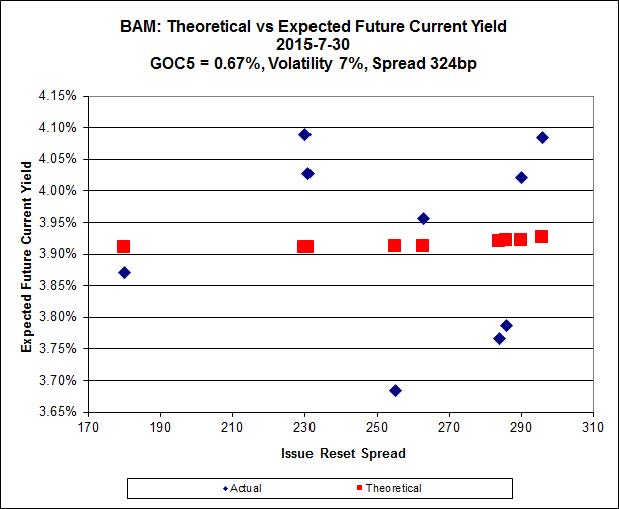

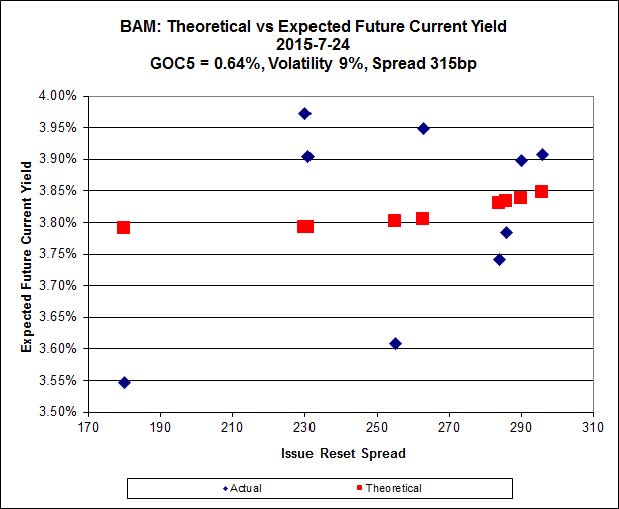

Click for Big

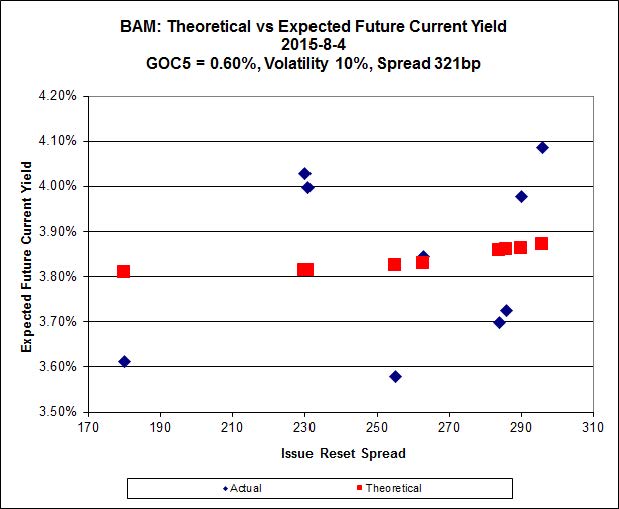

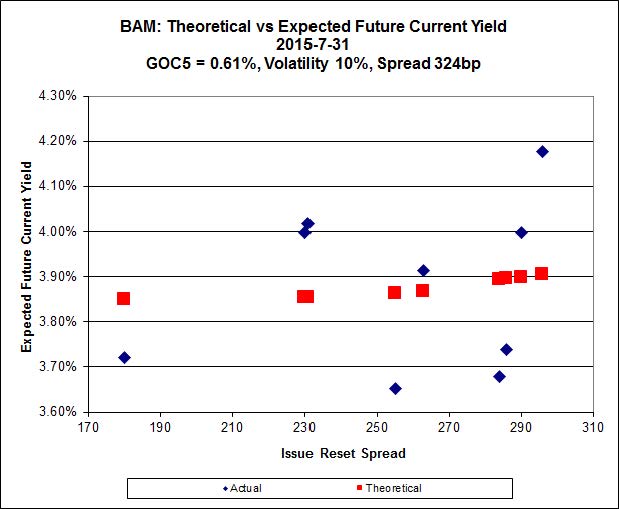

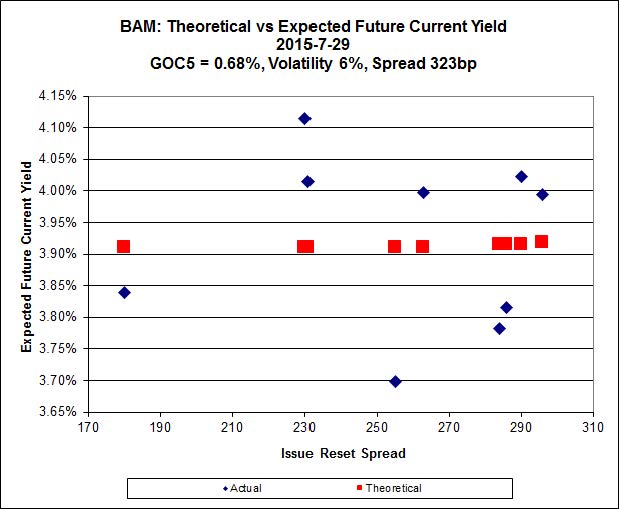

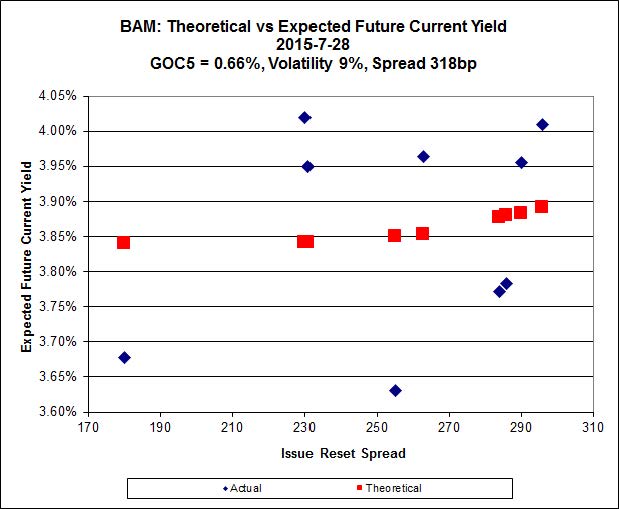

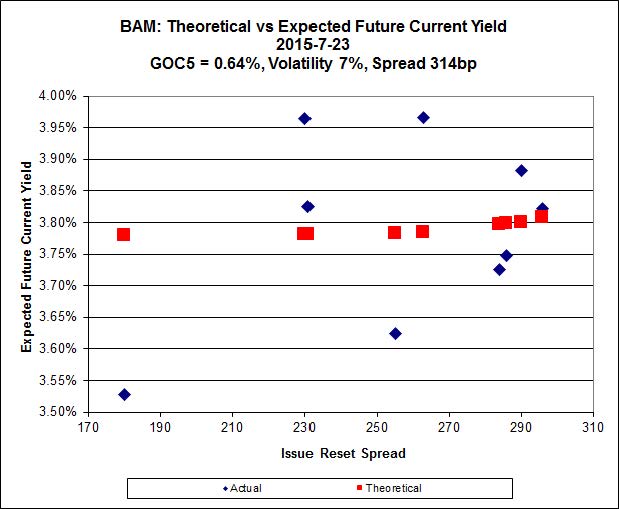

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.Z, resetting at +296bp on 2017-12-31, bid at 21.83 to be $1.04 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 23.40 and appears to be $1.17 rich.

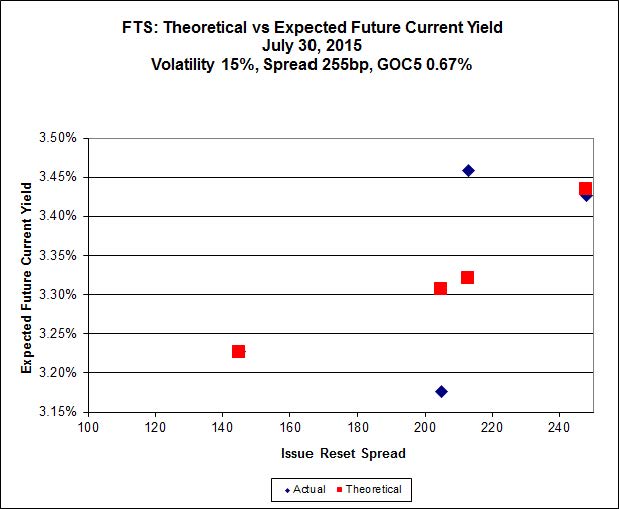

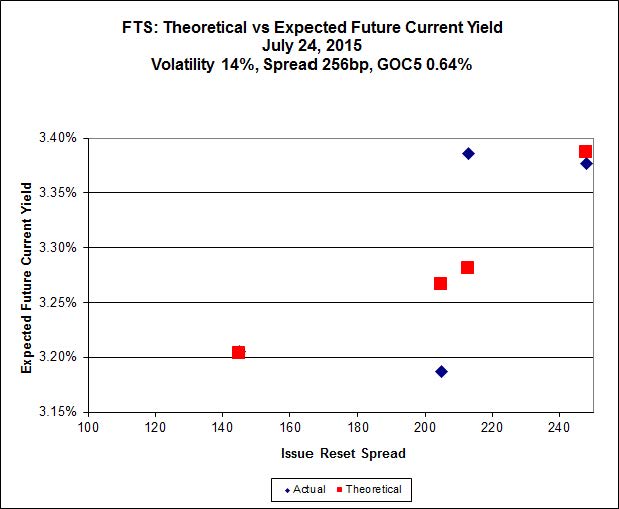

Click for Big

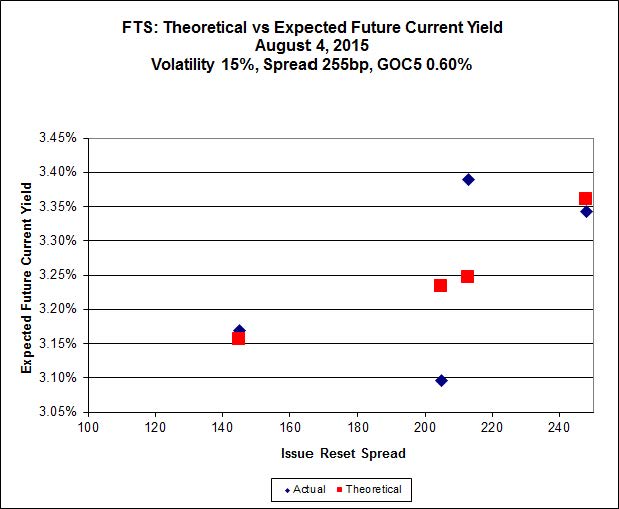

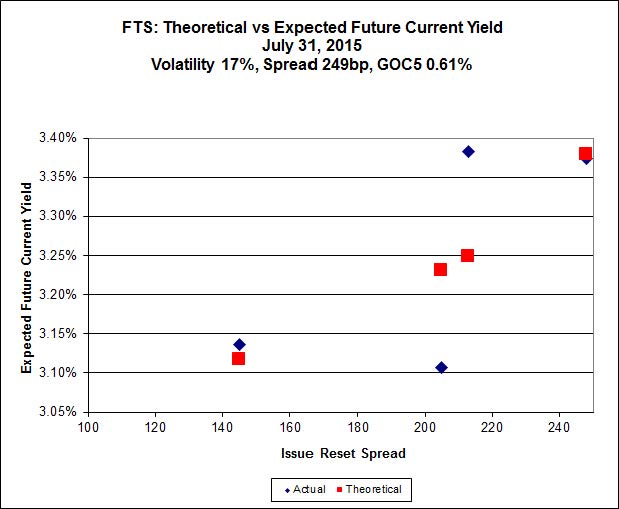

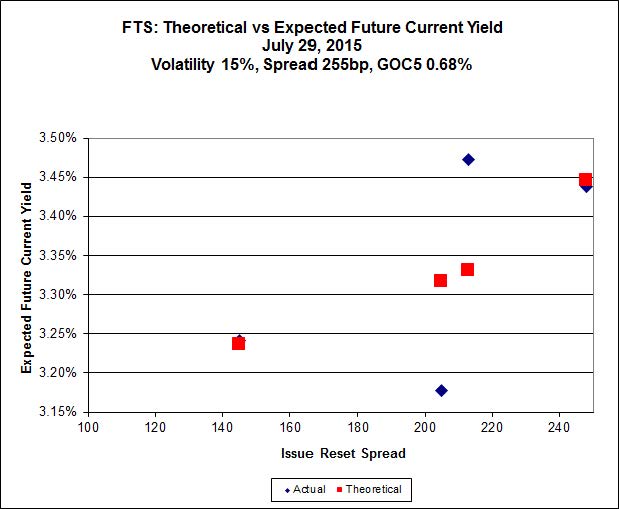

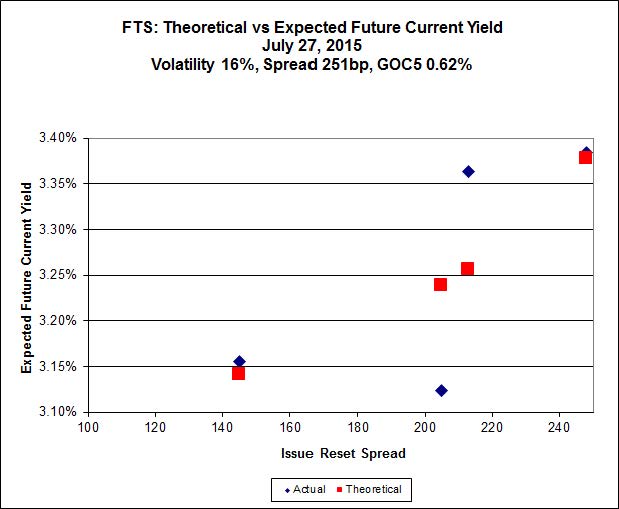

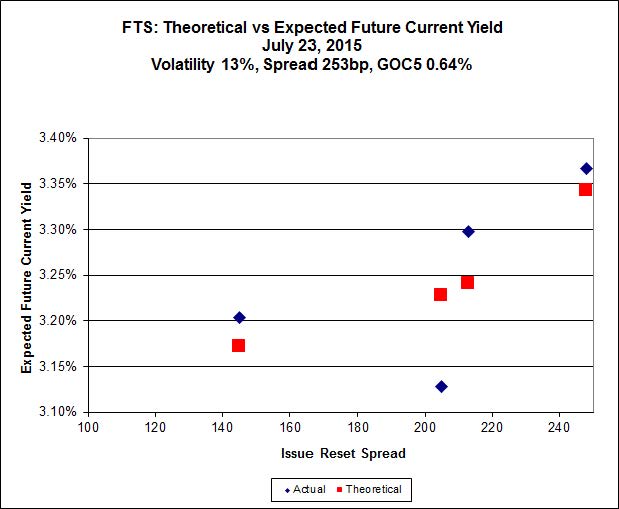

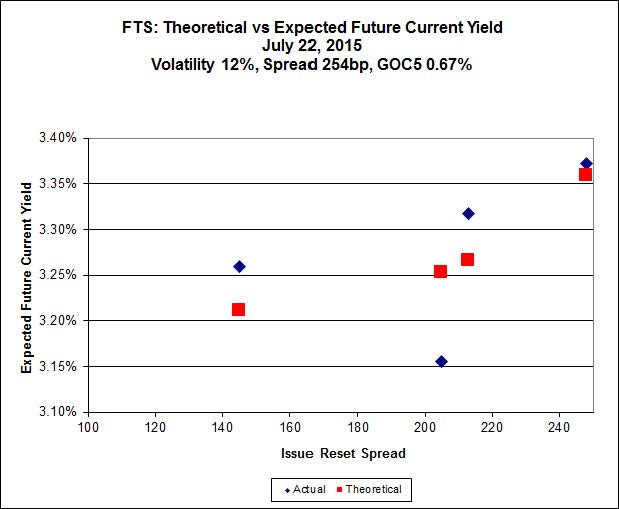

FTS.PR.K, with a spread of +205bp, and bid at 21.18, looks $0.70 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 19.96 and is $1.03 cheap.

Click for Big

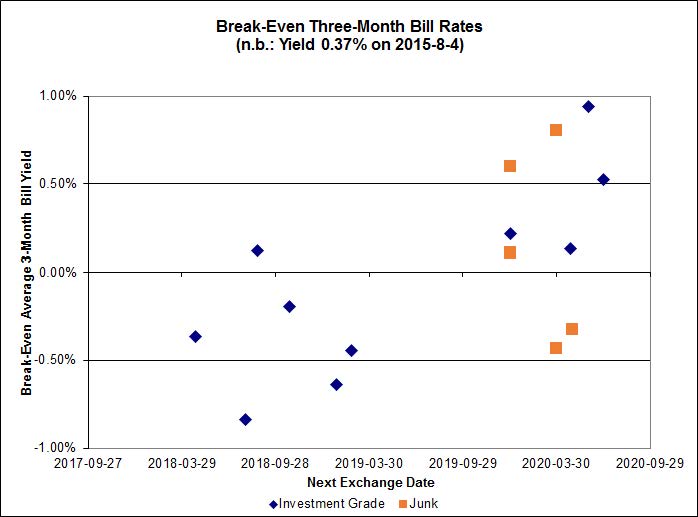

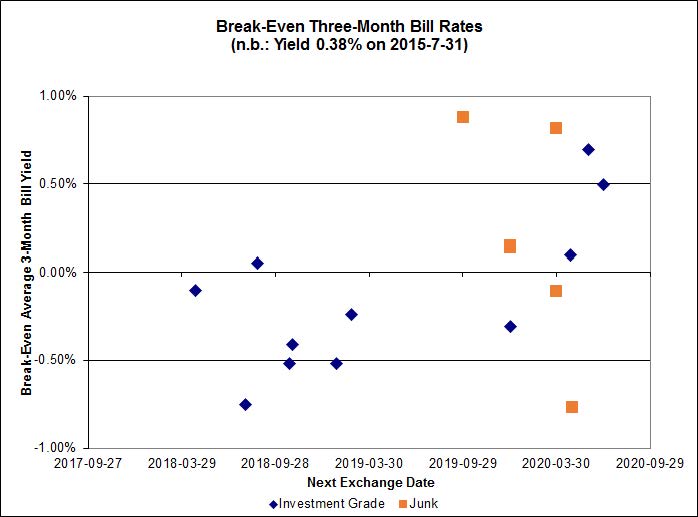

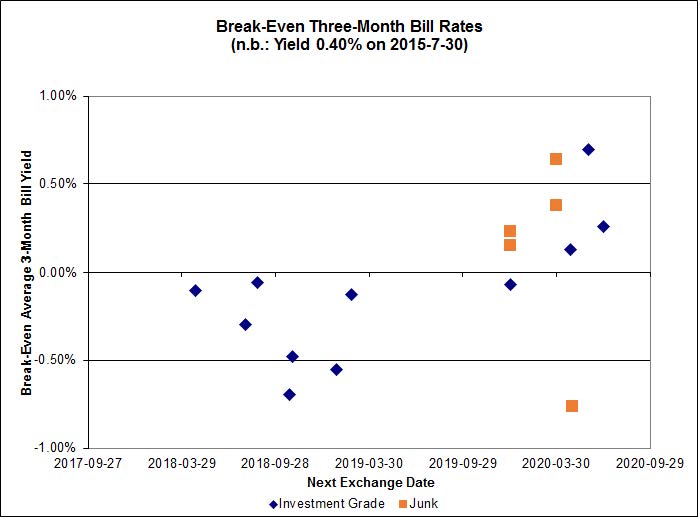

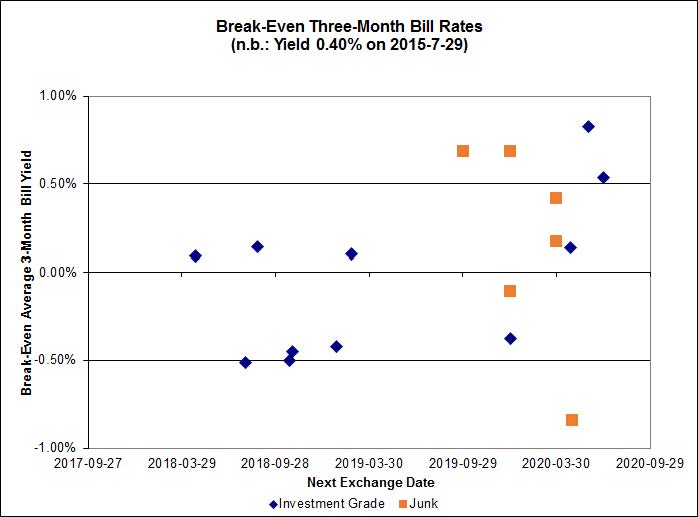

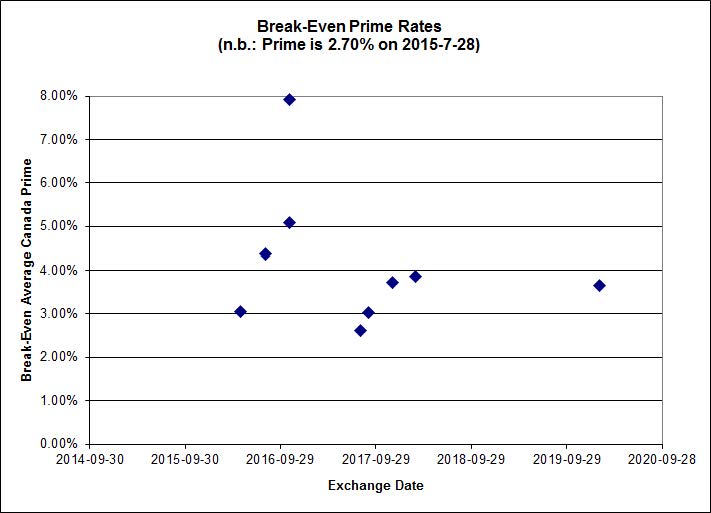

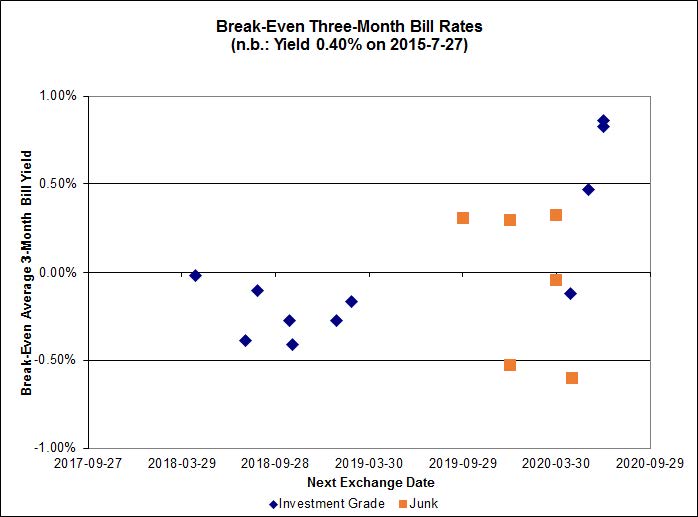

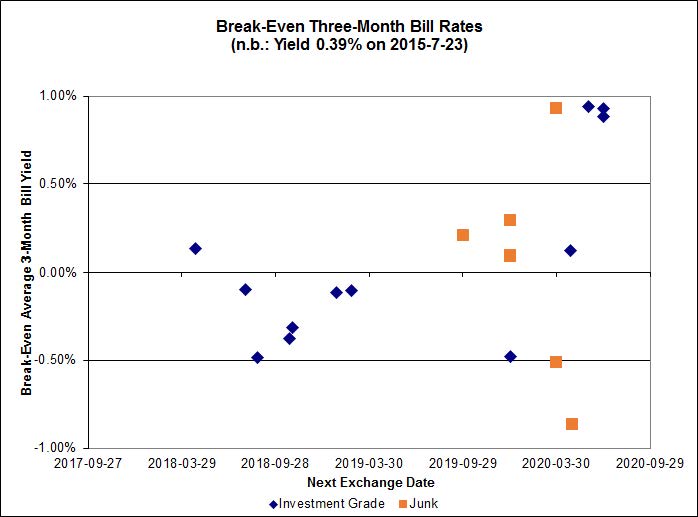

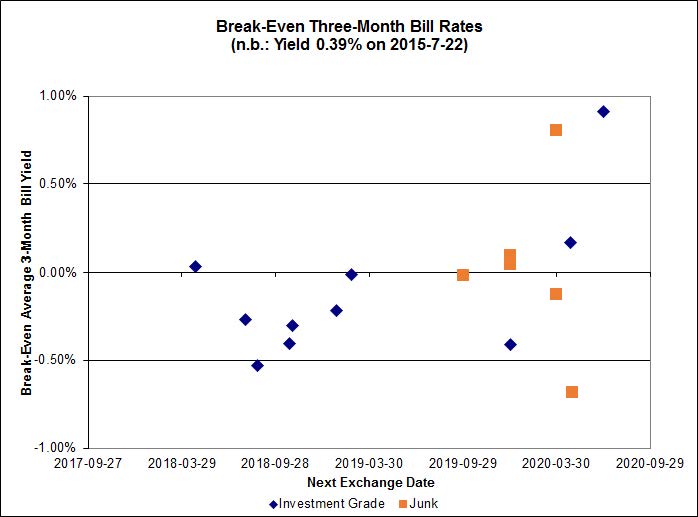

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.03%, with one outlier above 1.00%. There is one junk outlier above +1.00%.

Click for Big

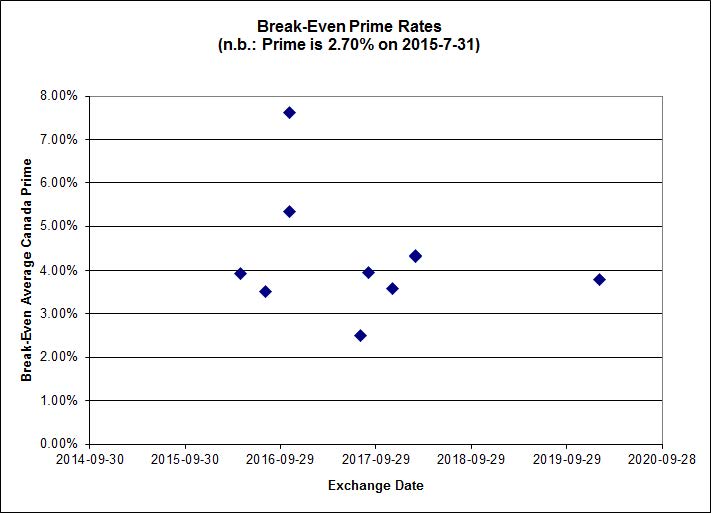

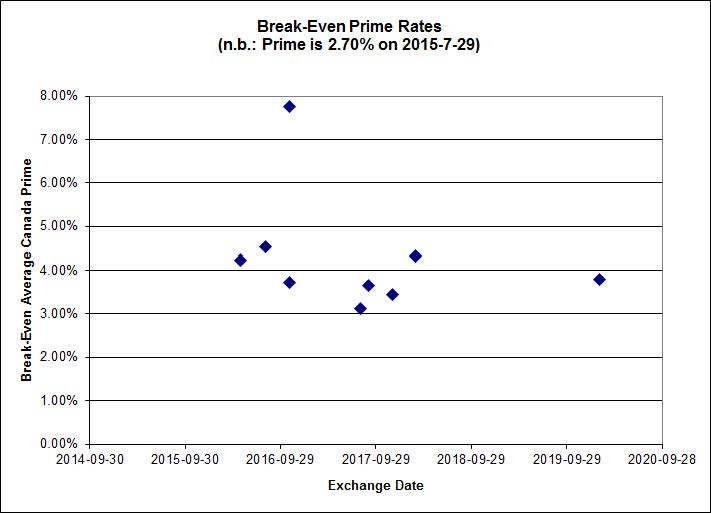

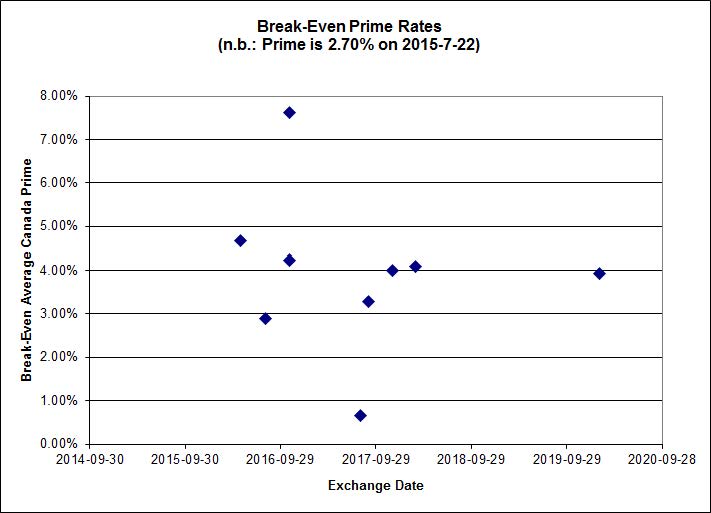

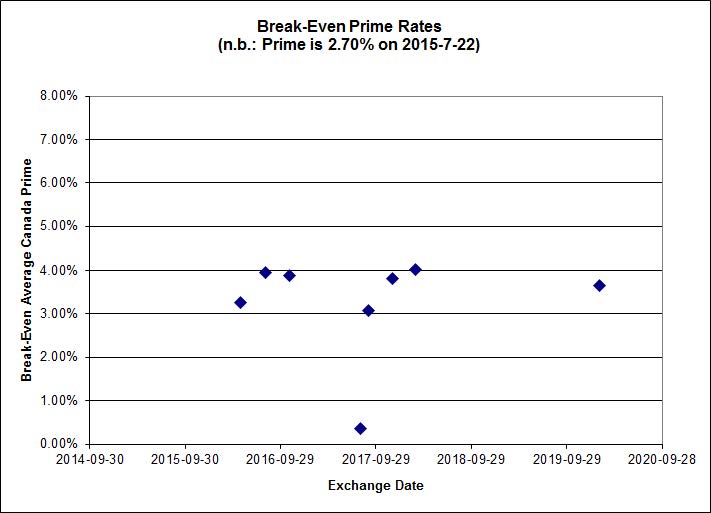

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4166 % | 1,996.4 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4166 % | 3,490.6 |

| Floater | 3.68 % | 3.73 % | 55,743 | 17.97 | 3 | 0.4166 % | 2,122.3 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.7363 % | 2,754.4 |

| SplitShare | 4.62 % | 4.98 % | 60,650 | 3.15 | 3 | -0.7363 % | 3,228.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.7363 % | 2,518.6 |

| Perpetual-Premium | 5.71 % | 5.37 % | 66,049 | 2.09 | 9 | 0.1765 % | 2,489.3 |

| Perpetual-Discount | 5.40 % | 5.43 % | 83,874 | 14.66 | 28 | 0.2884 % | 2,611.8 |

| FixedReset | 4.69 % | 3.80 % | 210,220 | 15.97 | 87 | 0.6218 % | 2,241.7 |

| Deemed-Retractible | 5.12 % | 5.17 % | 104,287 | 5.48 | 34 | 0.3192 % | 2,579.6 |

| FloatingReset | 2.32 % | 3.29 % | 46,800 | 6.02 | 9 | 0.1789 % | 2,257.0 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| PVS.PR.D | SplitShare | -2.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2021-10-08 Maturity Price : 25.00 Evaluated at bid price : 24.00 Bid-YTW : 5.44 % |

| BAM.PF.B | FixedReset | -1.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 20.60 Evaluated at bid price : 20.60 Bid-YTW : 4.18 % |

| FTS.PR.K | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 21.18 Evaluated at bid price : 21.18 Bid-YTW : 3.43 % |

| HSE.PR.G | FixedReset | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 22.01 Evaluated at bid price : 22.55 Bid-YTW : 4.71 % |

| GWO.PR.S | Deemed-Retractible | 1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.05 Bid-YTW : 5.33 % |

| ELF.PR.H | Perpetual-Discount | 1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 24.13 Evaluated at bid price : 24.61 Bid-YTW : 5.62 % |

| CU.PR.D | Perpetual-Discount | 1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 22.72 Evaluated at bid price : 23.04 Bid-YTW : 5.40 % |

| ENB.PR.H | FixedReset | 1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 15.62 Evaluated at bid price : 15.62 Bid-YTW : 4.75 % |

| HSE.PR.C | FixedReset | 1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 22.16 Evaluated at bid price : 22.75 Bid-YTW : 4.28 % |

| CU.PR.C | FixedReset | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 23.42 Evaluated at bid price : 23.78 Bid-YTW : 3.23 % |

| GWO.PR.G | Deemed-Retractible | 1.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.65 Bid-YTW : 5.49 % |

| BAM.PR.T | FixedReset | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 18.41 Evaluated at bid price : 18.41 Bid-YTW : 4.18 % |

| BAM.PF.D | Perpetual-Discount | 1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 21.39 Evaluated at bid price : 21.72 Bid-YTW : 5.70 % |

| MFC.PR.I | FixedReset | 1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.85 Bid-YTW : 3.82 % |

| BAM.PR.R | FixedReset | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 18.22 Evaluated at bid price : 18.22 Bid-YTW : 4.14 % |

| TD.PR.Z | FloatingReset | 1.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.11 Bid-YTW : 3.29 % |

| BMO.PR.T | FixedReset | 1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 22.19 Evaluated at bid price : 22.75 Bid-YTW : 3.27 % |

| MFC.PR.F | FixedReset | 1.49 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.03 Bid-YTW : 6.93 % |

| ENB.PR.B | FixedReset | 1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 15.64 Evaluated at bid price : 15.64 Bid-YTW : 5.01 % |

| RY.PR.Z | FixedReset | 1.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 22.05 Evaluated at bid price : 22.50 Bid-YTW : 3.29 % |

| GWO.PR.P | Deemed-Retractible | 1.54 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.00 Bid-YTW : 5.51 % |

| NA.PR.W | FixedReset | 1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 21.57 Evaluated at bid price : 21.88 Bid-YTW : 3.47 % |

| BMO.PR.S | FixedReset | 1.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 22.29 Evaluated at bid price : 22.88 Bid-YTW : 3.34 % |

| TRP.PR.A | FixedReset | 1.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 18.40 Evaluated at bid price : 18.40 Bid-YTW : 3.66 % |

| FTS.PR.H | FixedReset | 1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 16.45 Evaluated at bid price : 16.45 Bid-YTW : 3.28 % |

| TD.PF.B | FixedReset | 1.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 22.03 Evaluated at bid price : 22.50 Bid-YTW : 3.33 % |

| ENB.PR.T | FixedReset | 1.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 17.21 Evaluated at bid price : 17.21 Bid-YTW : 4.84 % |

| TD.PF.C | FixedReset | 1.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 21.66 Evaluated at bid price : 22.00 Bid-YTW : 3.41 % |

| SLF.PR.G | FixedReset | 1.88 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.77 Bid-YTW : 7.01 % |

| IFC.PR.C | FixedReset | 2.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.30 Bid-YTW : 4.86 % |

| BMO.PR.W | FixedReset | 2.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 21.73 Evaluated at bid price : 22.09 Bid-YTW : 3.36 % |

| TRP.PR.C | FixedReset | 2.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 14.62 Evaluated at bid price : 14.62 Bid-YTW : 3.68 % |

| CU.PR.F | Perpetual-Discount | 2.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 21.30 Evaluated at bid price : 21.30 Bid-YTW : 5.38 % |

| HSE.PR.E | FixedReset | 2.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 22.39 Evaluated at bid price : 23.16 Bid-YTW : 4.57 % |

| PWF.PR.T | FixedReset | 2.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 23.04 Evaluated at bid price : 24.30 Bid-YTW : 3.14 % |

| ENB.PR.P | FixedReset | 2.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 17.25 Evaluated at bid price : 17.25 Bid-YTW : 4.80 % |

| TRP.PR.E | FixedReset | 2.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 21.11 Evaluated at bid price : 21.11 Bid-YTW : 3.80 % |

| BAM.PR.X | FixedReset | 3.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 17.15 Evaluated at bid price : 17.15 Bid-YTW : 3.80 % |

| TRP.PR.D | FixedReset | 3.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 20.77 Evaluated at bid price : 20.77 Bid-YTW : 3.80 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| SLF.PR.G | FixedReset | 164,280 | TD crossed 160,000 at 16.70. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.77 Bid-YTW : 7.01 % |

| RY.PR.J | FixedReset | 121,200 | Desjardins crossed 113,100 at 23.55. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 22.56 Evaluated at bid price : 23.51 Bid-YTW : 3.52 % |

| PWF.PR.T | FixedReset | 103,109 | RBC crossd 100,000 at 24.50. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 23.04 Evaluated at bid price : 24.30 Bid-YTW : 3.14 % |

| BMO.PR.Y | FixedReset | 78,718 | Desjardins crossed 74,300 at 24.00. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-05 Maturity Price : 22.77 Evaluated at bid price : 24.00 Bid-YTW : 3.50 % |

| HSB.PR.D | Deemed-Retractible | 67,500 | RBC crossed 49,800 at 25.00. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.93 Bid-YTW : 5.17 % |

| TD.PR.Y | FixedReset | 51,933 | RBC crossed 50,000 at 25.07. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.10 Bid-YTW : 2.88 % |

| There were 25 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| FTS.PR.F | Perpetual-Discount | Quote: 22.93 – 23.90 Spot Rate : 0.9700 Average : 0.6488 YTW SCENARIO |

| ENB.PR.J | FixedReset | Quote: 17.58 – 18.28 Spot Rate : 0.7000 Average : 0.4452 YTW SCENARIO |

| MFC.PR.N | FixedReset | Quote: 21.88 – 22.80 Spot Rate : 0.9200 Average : 0.6700 YTW SCENARIO |

| HSE.PR.G | FixedReset | Quote: 22.55 – 23.25 Spot Rate : 0.7000 Average : 0.4504 YTW SCENARIO |

| TRP.PR.B | FixedReset | Quote: 14.06 – 14.75 Spot Rate : 0.6900 Average : 0.4812 YTW SCENARIO |

| PVS.PR.D | SplitShare | Quote: 24.00 – 24.50 Spot Rate : 0.5000 Average : 0.3164 YTW SCENARIO |