Assiduous Reader B let me know that the Financial Post breathlessly informs us that FixedResets went down in January.

The Greek tragedy is headed for a showdown:

Euro region finance ministers failed to reach an agreement on how to keep bailout funds flowing to Greece and will resume talks next week.

“We covered a lot of ground but didn’t actually reach a joint conclusion on how to take the next steps,” Eurogroup Chairman Jeroen Dijsselbloem said at a press conference in Brussels. “There has to be a political agreement on the way forward.”

Earlier, four euro region officials said that ministers were moving toward an agreement on a bailout extension. A Greek official then said that no agreement had been made and the government won’t accept an extension of the existing bailout program.

Canadian Western Bank, proud issuer of CWB.PR.B, has sold its insurance subsidiary to Intact Financial, proud issuer of IFC.PR.A and IFC.PR.C:

Canadian Western Bank Group (TSX: CWB) today announced a refinement to its long-term growth strategy with a definitive agreement to sell its property and casualty insurance subsidiary, Canadian Direct Insurance (CDI), to Intact Financial Corporation (Intact) for $197 million in cash. The purchase price is approximately 2.5 times the net book value of CDI as at October 31, 2014. The transaction is subject to customary closing conditions, including regulatory approvals. The closing date is expected in mid-2015.

“This transaction is the result of a purposeful strategic assessment that we started over a year ago,” said Chris Fowler, CWB’s president and chief executive officer. “Our strategic direction is to increase the depth and breadth of client relationships through a focus on our core business banking platform with complementary financial services in personal banking, equipment finance and leasing, alternative mortgages, wealth management and trust services. These core areas provide the best opportunities to drive meaningful future growth and build long-term value for CWB shareholders, while the insurance business is much less strategically aligned. We believe this opportunity to monetize and redeploy the significant value created by CDI into our identified core areas will generate superior returns for CWB shareholders moving forward.”

“Upon closing, we estimate the capital generated from the expected gain on sale from this transaction will increase CWB’s common equity Tier 1 ratio by approximately 60 basis points. The gain will also drive considerable outperformance relative to our published 2015 key profitability targets and growth in earnings per common share. However, the resulting elevated capital level is expected to constrain our 2015 return on common shareholders’ equity from continuing operations. As stated, it is our intention to redeploy this capital in due course for strategic and accretive opportunities that are consistent with our risk appetite. This capital level will position us to move quickly on investment opportunities as they materialize. Our primary areas of interest for potential strategic acquisitions are centred on opportunities in equipment finance and leasing, and wealth management.”

DBRS regards the transaction as credit-neutral for CWB.

There was a pullback for the Canadian preferred share market today, with PerpetualDiscounts down 19bp, FixedResets losing 22bp and DeemedRetractibles off 7bp. There is yet another lengthy Performance Highlights table, dominated by losing FixedResets. Volume was average.

PerpetualDiscounts now yield 4.96%, equivalent to 6.45% interest at the standard equivalency factor of 1.3x. Long corporates now yield about 3.75%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 270bp, a narrowing from the 280bp reported February 4.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

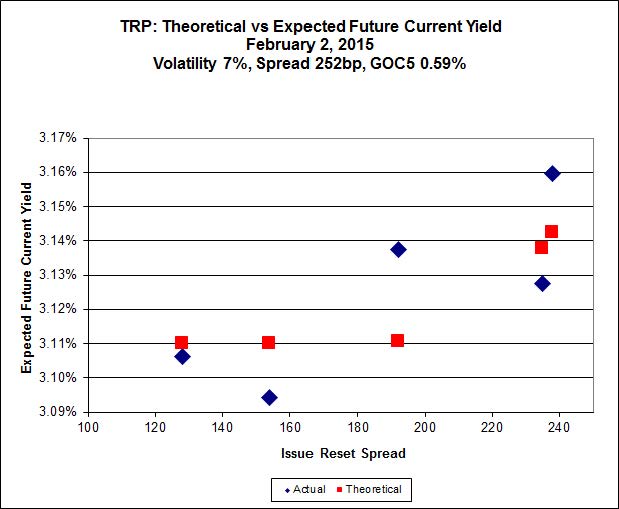

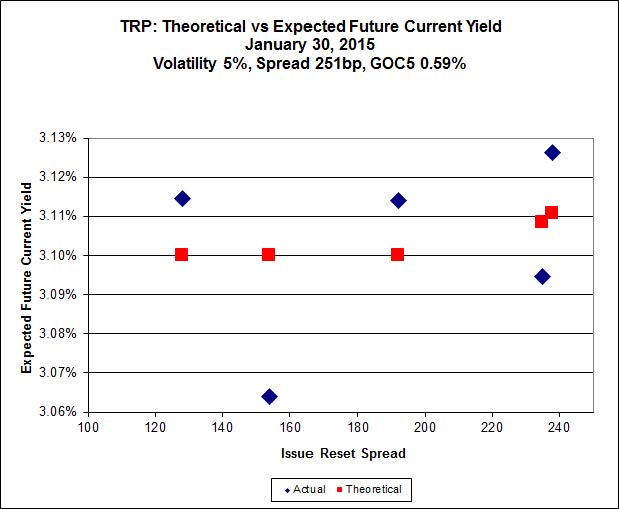

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 24.90 to be $1.20 rich, while TRP.PR.A, resetting 2019-12-31 at +192, is bid at 19.75 to be $0.66 cheap.

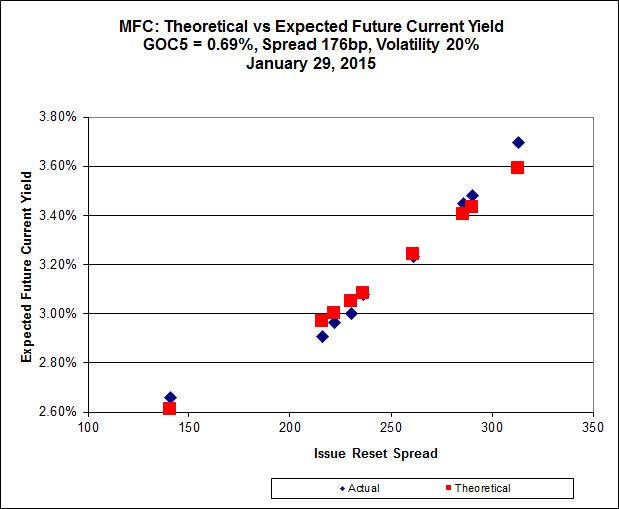

Click for Big

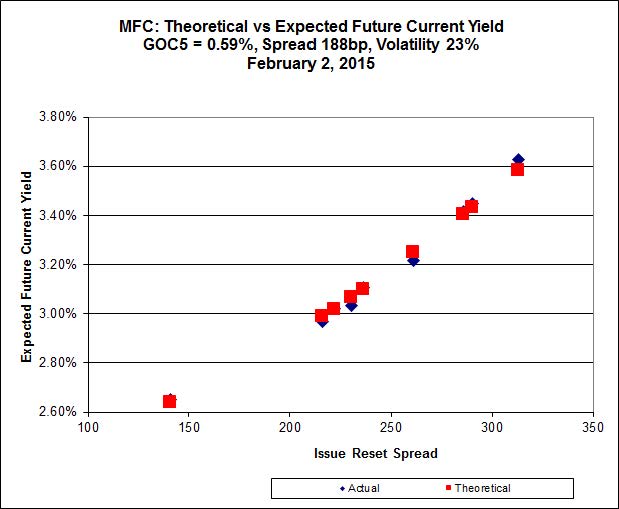

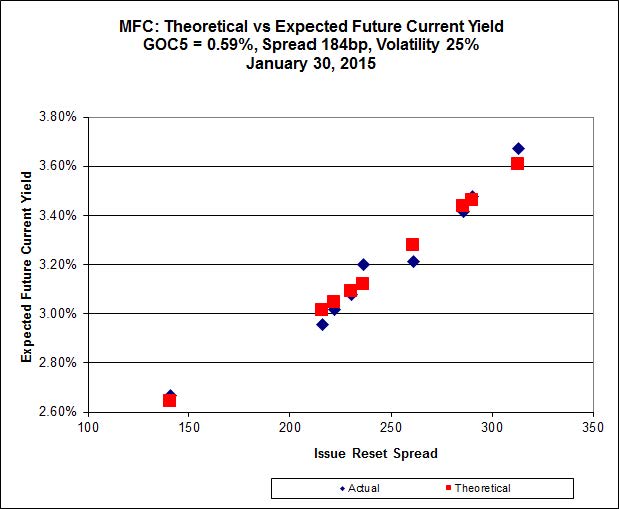

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.N, resetting at +230 on 2020-3-19, bid at 24.80 to be $0.34 rich, while MFC.PR.H, resetting at +313 on 2017-3-19 is bid at 25.91 to be $0.50 cheap.

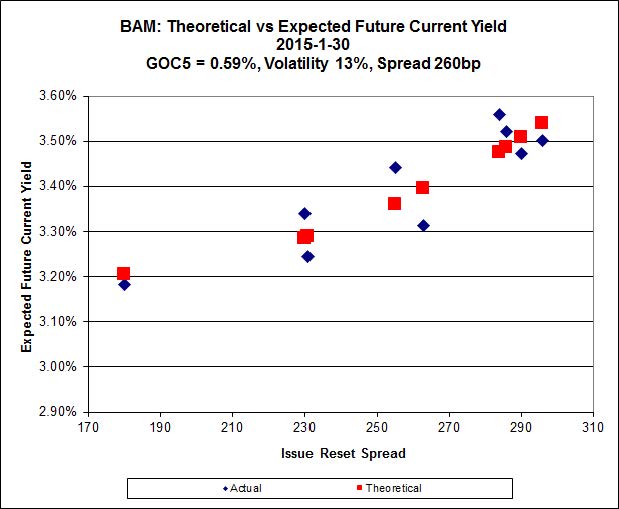

Click for Big

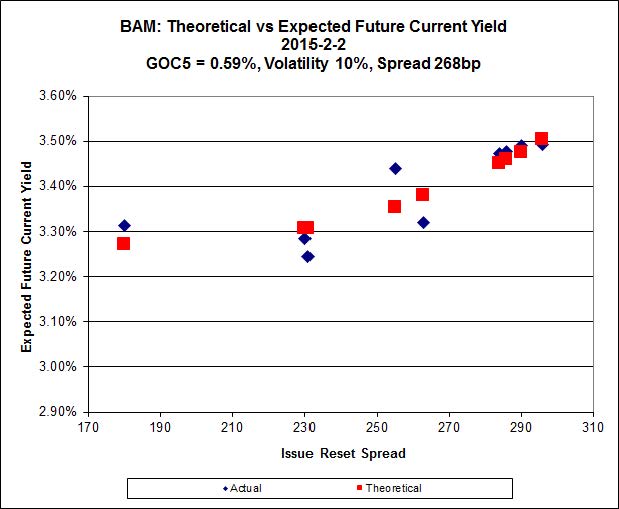

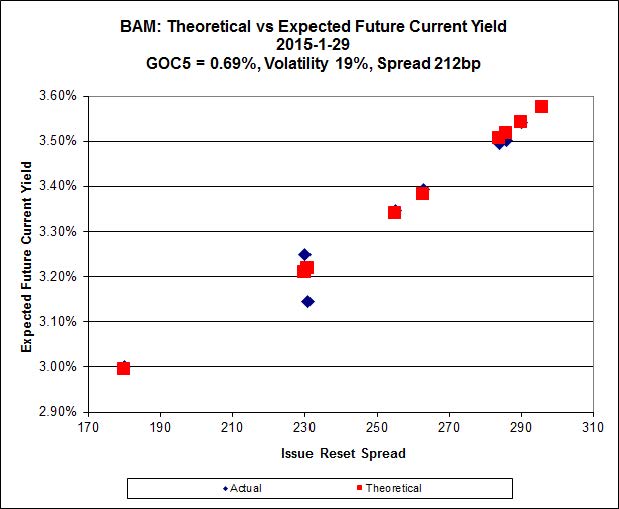

The cheapest issue relative to its peers is BAM.PR.X, resetting at +180bp on 2017-6-30, bid at 18.06 to be $0.53 cheap. BAM.PF.E, resetting at +255bp 2020-3-31 is bid at 24.95 and appears to be $1.07 rich.

Click for Big

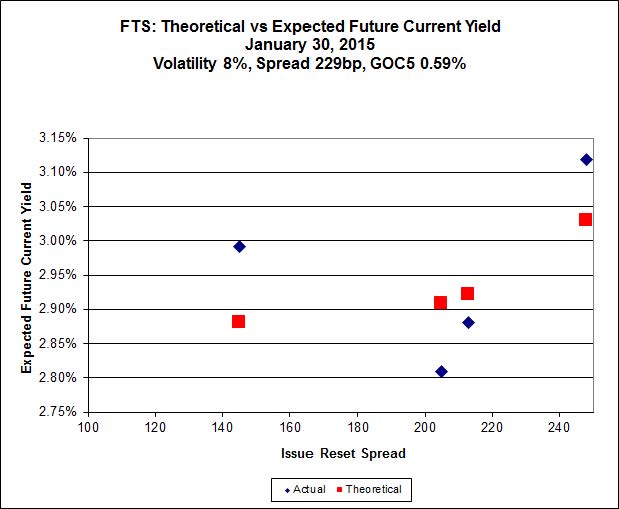

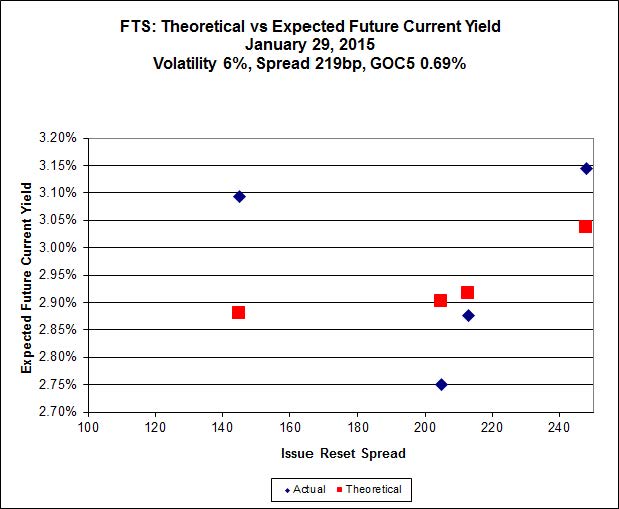

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 17.00, looks $0.97 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 23.97 and is $1.16 rich.

Click for Big

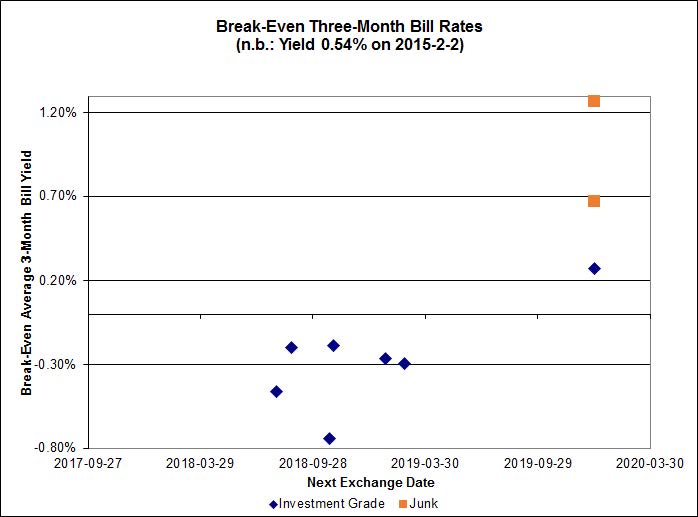

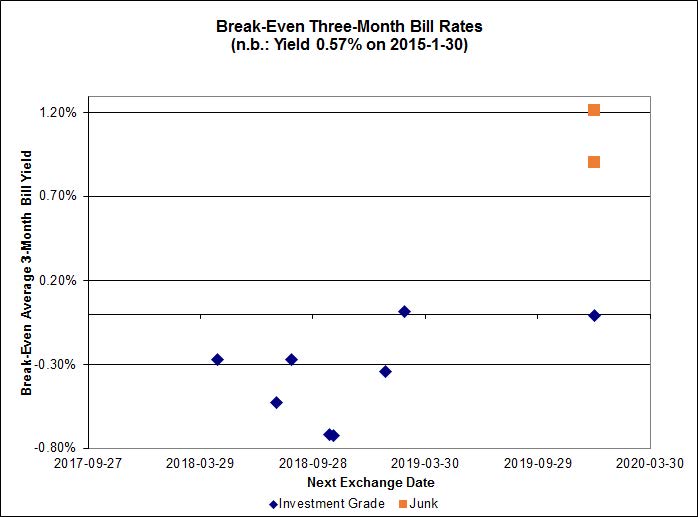

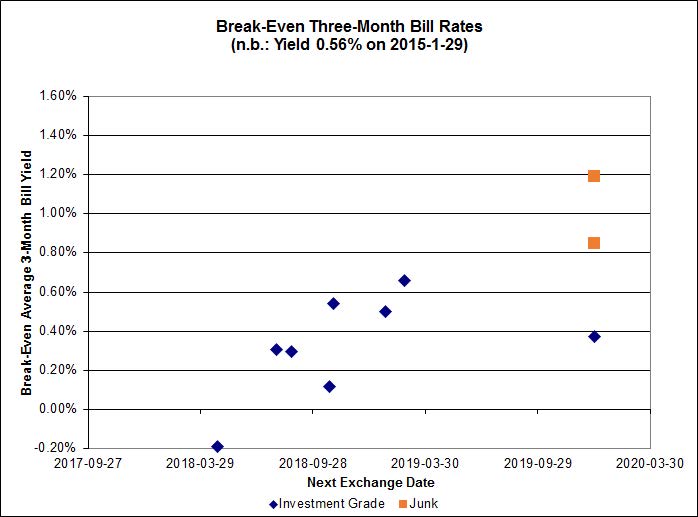

All the break-even rates are scattered around negative 10bp – the market has started believing the deflation story again!

On the other hand, the market’s distaste for product linked to Money Market rates does not extend to prime, as shown by the FixedFloater/RatchetRate pairs:

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.5278 % | 2,202.5 |

| FixedFloater | 4.35 % | 3.51 % | 19,937 | 18.39 | 1 | -0.0458 % | 4,059.6 |

| Floater | 3.27 % | 3.46 % | 62,249 | 18.57 | 4 | 0.5278 % | 2,341.5 |

| OpRet | 4.04 % | 1.52 % | 98,709 | 0.35 | 1 | 0.0000 % | 2,757.5 |

| SplitShare | 4.27 % | 3.66 % | 30,302 | 3.55 | 5 | 0.0791 % | 3,201.4 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 2,521.4 |

| Perpetual-Premium | 5.33 % | -4.20 % | 58,161 | 0.08 | 24 | -0.0434 % | 2,515.0 |

| Perpetual-Discount | 4.95 % | 4.96 % | 125,184 | 15.25 | 10 | -0.1875 % | 2,788.7 |

| FixedReset | 4.38 % | 3.37 % | 200,866 | 17.11 | 79 | -0.2225 % | 2,445.6 |

| Deemed-Retractible | 4.90 % | 0.34 % | 107,959 | 0.12 | 39 | -0.0725 % | 2,650.4 |

| FloatingReset | 2.49 % | 2.96 % | 84,101 | 6.41 | 7 | -0.3094 % | 2,305.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| HSE.PR.A | FixedReset | -2.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-11 Maturity Price : 17.25 Evaluated at bid price : 17.25 Bid-YTW : 3.78 % |

| SLF.PR.G | FixedReset | -2.76 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.68 Bid-YTW : 5.63 % |

| ENB.PR.B | FixedReset | -2.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-11 Maturity Price : 19.91 Evaluated at bid price : 19.91 Bid-YTW : 4.07 % |

| BAM.PR.T | FixedReset | -2.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-11 Maturity Price : 22.28 Evaluated at bid price : 22.60 Bid-YTW : 3.56 % |

| ENB.PR.D | FixedReset | -2.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-11 Maturity Price : 19.95 Evaluated at bid price : 19.95 Bid-YTW : 4.08 % |

| BAM.PR.X | FixedReset | -2.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-11 Maturity Price : 18.06 Evaluated at bid price : 18.06 Bid-YTW : 3.91 % |

| BMO.PR.Q | FixedReset | -1.51 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.90 Bid-YTW : 3.71 % |

| PWF.PR.P | FixedReset | -1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-11 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 3.25 % |

| FTS.PR.F | Perpetual-Discount | -1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-11 Maturity Price : 24.79 Evaluated at bid price : 25.08 Bid-YTW : 4.96 % |

| ENB.PR.H | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-11 Maturity Price : 18.90 Evaluated at bid price : 18.90 Bid-YTW : 4.06 % |

| ENB.PR.F | FixedReset | -1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-11 Maturity Price : 20.75 Evaluated at bid price : 20.75 Bid-YTW : 4.07 % |

| TRP.PR.A | FixedReset | -1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-11 Maturity Price : 19.75 Evaluated at bid price : 19.75 Bid-YTW : 3.59 % |

| BAM.PR.R | FixedReset | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-11 Maturity Price : 21.41 Evaluated at bid price : 21.73 Bid-YTW : 3.70 % |

| GWO.PR.N | FixedReset | -1.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.35 Bid-YTW : 5.18 % |

| TRP.PR.B | FixedReset | -1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-11 Maturity Price : 15.02 Evaluated at bid price : 15.02 Bid-YTW : 3.45 % |

| ENB.PR.J | FixedReset | -1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-11 Maturity Price : 21.80 Evaluated at bid price : 22.16 Bid-YTW : 3.96 % |

| TD.PR.Z | FloatingReset | -1.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.70 Bid-YTW : 2.97 % |

| BNS.PR.Y | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.15 Bid-YTW : 3.69 % |

| BNS.PR.Z | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.14 Bid-YTW : 3.56 % |

| NA.PR.S | FixedReset | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-11 Maturity Price : 23.27 Evaluated at bid price : 25.15 Bid-YTW : 3.17 % |

| MFC.PR.L | FixedReset | 1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.00 Bid-YTW : 3.94 % |

| MFC.PR.K | FixedReset | 1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.19 Bid-YTW : 3.76 % |

| TRP.PR.E | FixedReset | 1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-11 Maturity Price : 23.15 Evaluated at bid price : 24.90 Bid-YTW : 3.23 % |

| FTS.PR.K | FixedReset | 1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-11 Maturity Price : 22.84 Evaluated at bid price : 23.97 Bid-YTW : 3.10 % |

| HSE.PR.C | FixedReset | 1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-11 Maturity Price : 23.25 Evaluated at bid price : 25.25 Bid-YTW : 3.90 % |

| IFC.PR.A | FixedReset | 1.89 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.49 Bid-YTW : 5.48 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| ENB.PR.Y | FixedReset | 60,241 | Desjardins crossed blocks of 29,200 and 10,000, both at 20.87. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-11 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 3.96 % |

| RY.PR.J | FixedReset | 52,350 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-11 Maturity Price : 23.20 Evaluated at bid price : 25.18 Bid-YTW : 3.35 % |

| BNS.PR.L | Deemed-Retractible | 51,820 | TD crossed 50,000 at 25.49. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-04-28 Maturity Price : 25.25 Evaluated at bid price : 25.49 Bid-YTW : 0.47 % |

| RY.PR.I | FixedReset | 45,700 | TD crossed 35,000 at 25.35. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.35 Bid-YTW : 2.94 % |

| SLF.PR.G | FixedReset | 28,241 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.68 Bid-YTW : 5.63 % |

| BAM.PR.K | Floater | 24,350 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-11 Maturity Price : 14.15 Evaluated at bid price : 14.15 Bid-YTW : 3.56 % |

| There were 30 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BNS.PR.B | FloatingReset | Quote: 23.74 – 24.20 Spot Rate : 0.4600 Average : 0.2872 YTW SCENARIO |

| BAM.PR.T | FixedReset | Quote: 22.60 – 23.10 Spot Rate : 0.5000 Average : 0.3295 YTW SCENARIO |

| BAM.PR.X | FixedReset | Quote: 18.06 – 18.50 Spot Rate : 0.4400 Average : 0.2705 YTW SCENARIO |

| PWF.PR.P | FixedReset | Quote: 18.75 – 19.34 Spot Rate : 0.5900 Average : 0.4487 YTW SCENARIO |

| TD.PR.Z | FloatingReset | Quote: 23.70 – 24.16 Spot Rate : 0.4600 Average : 0.3277 YTW SCENARIO |

| FTS.PR.F | Perpetual-Discount | Quote: 25.08 – 25.49 Spot Rate : 0.4100 Average : 0.2780 YTW SCENARIO |