The recent rally in junk bonds is having some interesting knock-on effects:

The biggest high-yield rally ever is punishing the lowest- rated companies that may no longer be able to afford avoiding bankruptcy by exchanging or buying back debt at the lowest prices on record. The “cruel irony” of rising prices means the neediest businesses will have a harder time finding financing, Morgan Stanley analysts led by Jocelyn Chu in New York said in a May 15 report. That may lead to more defaults than anticipated.

Freescale Semiconductor Inc., part-owned by 62-year-old Schwarzman’s Blackstone Group LP, wiped away $1.9 billion of debt in March by giving investors an average of 32 cents on the dollar in loans. Since the bond exchange was announced March 4, the securities have tripled to as high as 54.1 cents on the dollar, curtailing the chipmaker’s ability to cut the rest of its $7.5 billion debt load.

C-EBS is hosting a public hearing on liquidity buffers, in an attempt to finalize a framework for EU national bank supervision. There is a a wide range of industry practices:

– Within the industry, most banks either formally define a liquidity buffer or alternatively it is a concept implicit in their liquidity management policy.

– One institution formally defines its liquidity buffer as highly liquid unencumbered assets set at a level to get through the initial stages of a liquidity shock. It also defines a maximum amount of collateral that may be needed for intraday payment system purposes and deducts this from the stock of unencumbered assets. Buffers are formed for each of the currencies in which it is active. A survival period of 90 days is defined and liquidity shock scenarios developed to calibrate the size of the buffer.

– Another bank defines the buffer as a liquidity gap based on a runoff scenario (all maturing assets and liabilities not renewed during a 4 week period) that can be covered from high quality funding sources.

– Another bank defines the buffer over 30 days but does not use stress tests to measure the required size of buffer. Instead, expert judgement from the ALCO sets the buffer level. The quality of the assets in the buffer also impacts the level of buffer held.

– Another bank does not formally define a buffer. Instead it manages its overall counterbalancing capacity. As part of this, it uses projected flows to estimate a level of unencumbered assets that will cover the liquidity gap such that no change to the bank’s business model is required. This output is an input to the overall policy on managing its counterbalancing capacity.

The Globe and Mail has a story on Property & Casualty insurers:

The Office of the Superintendent of Financial Institutions (OSFI), which regulates about 200 companies in the sector, is worried about capital levels in the industry.

“It’s a period of great uncertainty right now,” said Bruce Thompson, a director in the supervision sector of OSFI’s Toronto office. “Our expectation is that 2009 is going to be a difficult year for the industry.”

…

Its total capital level dropped last year for the first time since 2003. The key measure of a property and casualty insurer’s financial cushion is called the Minimum Capital Test. The sector-wide ratio fell to 238 per cent at the end of 2008, from 252 per cent at the end of 2007. (Regulators require it to remain above a floor of 150 per cent, but Mr. Thompson pointed out that “companies know darn well that 150 is a territory you don’t go.”)

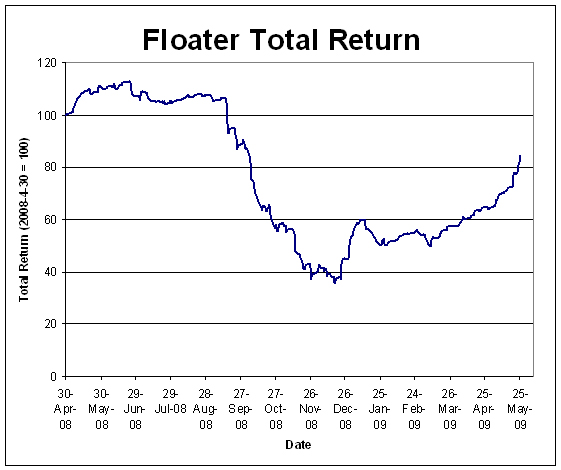

A basically flat day for preferreds amidst continued heavy volume.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1717 % | 1,303.5 |

| FixedFloater | 7.22 % | 5.76 % | 30,426 | 15.93 | 1 | -0.9211 % | 2,089.1 |

| Floater | 2.89 % | 3.31 % | 78,447 | 18.89 | 3 | 0.1717 % | 1,628.5 |

| OpRet | 5.01 % | 3.89 % | 144,274 | 2.56 | 14 | 0.0313 % | 2,167.7 |

| SplitShare | 5.91 % | 5.10 % | 52,663 | 4.26 | 3 | 0.2486 % | 1,845.4 |

| Interest-Bearing | 6.00 % | 7.49 % | 26,431 | 0.56 | 1 | 0.0000 % | 1,987.2 |

| Perpetual-Premium | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0241 % | 1,726.2 |

| Perpetual-Discount | 6.36 % | 6.38 % | 162,051 | 13.41 | 71 | -0.0241 % | 1,589.8 |

| FixedReset | 5.70 % | 4.91 % | 602,319 | 4.42 | 38 | 0.0425 % | 1,991.0 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.I | OpRet | -1.66 % | YTW SCENARIO Maturity Type : Soft Maturity Maturity Date : 2013-12-30 Maturity Price : 25.00 Evaluated at bid price : 23.75 Bid-YTW : 7.09 % |

| W.PR.J | Perpetual-Discount | -1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-03 Maturity Price : 21.20 Evaluated at bid price : 21.20 Bid-YTW : 6.73 % |

| PWF.PR.E | Perpetual-Discount | -1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-03 Maturity Price : 21.08 Evaluated at bid price : 21.08 Bid-YTW : 6.62 % |

| RY.PR.A | Perpetual-Discount | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-03 Maturity Price : 18.33 Evaluated at bid price : 18.33 Bid-YTW : 6.13 % |

| RY.PR.H | Perpetual-Discount | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-03 Maturity Price : 23.19 Evaluated at bid price : 23.35 Bid-YTW : 6.10 % |

| RY.PR.W | Perpetual-Discount | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-03 Maturity Price : 20.11 Evaluated at bid price : 20.11 Bid-YTW : 6.15 % |

| BAM.PR.B | Floater | 1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-03 Maturity Price : 12.00 Evaluated at bid price : 12.00 Bid-YTW : 3.31 % |

| CU.PR.B | Perpetual-Discount | 1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-03 Maturity Price : 24.50 Evaluated at bid price : 24.80 Bid-YTW : 6.08 % |

| CM.PR.R | OpRet | 1.86 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2009-07-03 Maturity Price : 25.60 Evaluated at bid price : 26.23 Bid-YTW : -18.42 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| MFC.PR.E | FixedReset | 1,144,632 | New issue settled today. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-03 Maturity Price : 25.00 Evaluated at bid price : 25.05 Bid-YTW : 5.53 % |

| CM.PR.K | FixedReset | 127,965 | RBC crossed 92,100 at 25.10. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-03 Maturity Price : 25.00 Evaluated at bid price : 25.05 Bid-YTW : 4.73 % |

| BMO.PR.O | FixedReset | 113,970 | National crossed 15,000 at 26.95; Desjardins crossed blocks of 50,000 and 25,000 shares, both at 27.00. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-06-24 Maturity Price : 25.00 Evaluated at bid price : 26.99 Bid-YTW : 5.05 % |

| CM.PR.R | OpRet | 104,700 | RBC crossed 100,000 at 25.85. YTW SCENARIO Maturity Type : Call Maturity Date : 2009-07-03 Maturity Price : 25.60 Evaluated at bid price : 26.23 Bid-YTW : -18.42 % |

| GWO.PR.X | OpRet | 59,677 | Dundee bought 56,000 from TD at 25.75. YTW SCENARIO Maturity Type : Soft Maturity Maturity Date : 2013-09-29 Maturity Price : 25.00 Evaluated at bid price : 25.56 Bid-YTW : 4.16 % |

| SLF.PR.F | FixedReset | 46,985 | YTW SCENARIO Maturity Type : Call Maturity Date : 2014-07-30 Maturity Price : 25.00 Evaluated at bid price : 25.76 Bid-YTW : 5.41 % |

| There were 41 other index-included issues trading in excess of 10,000 shares. | |||