Today’s big news was the expansion of the Term Securities Lending Facility:

The Federal Reserve announced today an expansion of its securities lending program. Under this new Term Securities Lending Facility (TSLF), the Federal Reserve will lend up to $200 billion of Treasury securities to primary dealers secured for a term of 28 days (rather than overnight, as in the existing program) by a pledge of other securities, including federal agency debt, federal agency residential-mortgage-backed securities (MBS), and non-agency AAA/Aaa-rated private-label residential MBS. The TSLF is intended to promote liquidity in the financing markets for Treasury and other collateral and thus to foster the functioning of financial markets more generally. As is the case with the current securities lending program, securities will be made available through an auction process. Auctions will be held on a weekly basis, beginning on March 27, 2008. The Federal Reserve will consult with primary dealers on technical design features of the TSLF.

The kerfuffle over Bear Stearns yesterday shows that the market is prepared to believe anything, as long as it’s bad. Yes, times are tough. But they actually managed to scrape out a profit last year (Nov. 30 year end) and have $18-billion cash on the balance sheet thanks to a vigorous term issuance programme in which they haven’t been afraid to pay up for five year money. They’re not going to disappear overnight. Though mind you, as Naked Capitalism points out, they’re very highly levered:

With this in mind, why were Bear and Lehman so highly geared? Lehman is levered 40 to 1, Bear is geared 34:1 (by contrast, Carlyie is levered 32:1). Trading firms should know better.

In deteriorating debt markets, the last thing you want to be carrying is a big balance sheet. Perhaps the banks in question assumed that the Fed’s interest rate cuts would produce enough gains in value (due to lower prevailing rates) to make deleveraging less urgent.

But now Bear and Lehman (and no doubt their peers as well) are delevearging out of necessity, as mark-to-market losses force them to write down assets, leading to hits to equity, and then putting them at gearing levels that are untenable. So shrink they must.

And, mind you, if I was thinking about buying their stock, I wouldn’t be counting on a return to pre-2007 earnings anytime soon. Neither would Punk Ziegel.

“The key problem is not the write-offs and losses that the company must take in the just-ended first fiscal quarter. The key issue is building a new business model,” Bove said. “Bear Stearns must adjust and it is probably going to be forced to find a merger partner,” he added.

Find a partner? Maybe they have!

Joseph Lewis, the second-largest shareholder in Bear Stearns Cos., may add to his holdings after the stock fell on speculation the company lacks sufficient access to capital, a person close to him said.

Times are tough, did I say above? Econbrowser‘s James Hamilton won’t quarrel if you say a recession has begun and his partner Menzie Chinn takes a certain amount of Democrat glee in the prospects for a two recession Bush presidency:

So, I’ll echo Jim’s assessment: too soon to be sure, but chances are pretty darn good that we that we’re into the second recession of the G.W. Bush presidency.

It seems to me the next question of interest is whether the recession is likely to be short or long. I keep on seeing predictions of a short V-shaped recession [3], [4], [5]. Most macro forecasts do predict a resurgence in 2008H2 (just as CEA Chair Lazear alluded to in his last press conference). For instance, today’s Deutsche Bank forecast is for (-0.5%) and (-0.3%) in Q1 and Q2, respectively, with growth spiking in Q3 at 2.6% before settling at 0.9% in Q4. Still, with oil and ag commodity prices stubbornly high, the extent of the financial system turmoil uncertain, and the less-than optimally constructed fiscal stimulus limited to only one percent of GDP, I’m don’t think the 2008H2 acceleration will be a sustained one.

Well … I’m not an economist and I have a high degree of skepticism towards any macro-forecast anyway … but if I had to bet a nickel I’d bet on a long grinding recession that squeezes every last bit of leverage out of the system. The credit markets are thoroughly disfunctional, borrowers are extending term to stay alive (Bear Stearns, CIT, …) rather than to expand and these funds are staying on the balance sheet as cash at a negative carry (Bear Stearns, CIT, …). I don’t know what will happen tomorrow, but I can say it looks pretty ugly out there today!

As usual, Accrued Interest has some sensible remarks regarding what will bring an end to the credit market:

What would bring an end to this bear market? Simple. Bear markets end when the market runs out of sellers.

I would prefer to phrase it … ‘Bear markets end when prices stop going down’, but this is a mere quibble.

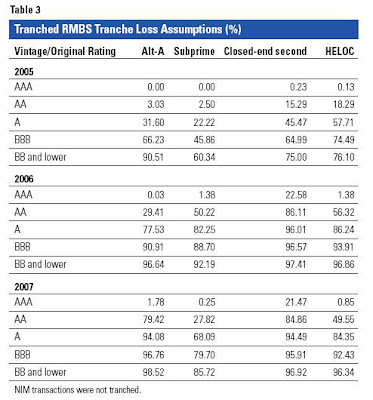

Naked Capitalism has an interesting piece on the Credit Rating Agencies’ alleged reluctance to cut the ratings on AAA sub-prime paper:

The Bloomberg story confirms our cynicism about the S&P’s and Moody’s. It reports that the rating agencies have held back from downgrading AAA subprime related securities.

Why is this important? In most deals, roughly 80% is of the value of the transaction was in the AAA tranches. These are far and away the most important in terms of economic value. But, not surprisingly, many of the buyers of this paper did so because they had portfolio constraints or capital requirements that made top-rated instruments particularly desirable. Thus in many cases, downgrades of this paper would have a pronounced impact, leading in many cases to sales, depressing prices.

…The ratings methods balance estimated losses against so-called credit support, a measure of how likely it is that owners of each piece of the bond will incur losses. For AAA rated debt, credit support needs to be five times the expected losses, according to Sylvain Raynes, author of The Analysis of Structured Securities, a college textbook.

All but six of the 80 AAA ABX bonds failed an S&P test for investment-grade status, which requires credit support to be twice the percentage of troubled collateral. The guideline was one of four tests used by S&P, and a failure to meet the standard wouldn’t have automatically resulted in a downgrade. The other companies used similar metrics to grade bonds, Raynes said. Investment grade refers to all bonds rated above BBB- by S&P and Baa3 by Moody’s….

On a $118 million Washington Mutual bond issued in 2007, WMHE 2007-HE2 2A4, 5.6 percent of its loans are in foreclosure and its safety margin, or the debt available to absorb losses, is less than the combined total of its loans at risk. Both S&P and Moody’s rate it AAA.

Fitch rates that bond B, five levels below investment grade and 15 levels less than its rivals….

The full Bloomberg story explains the Fitch discrepency a little better:

“We have built in 20 percent more home price declines from the end of ’07,” said Glenn Costello, managing director for residential mortgage-backed securities at Fitch. “When you build in that much home price decline, I feel good when I pick up the paper and I see that home prices are only down another 3 percent. My ratings are still good.”

Fitch is a good shop. I like Fitch.

In yet another sign of the cavalier sloppiness that was epidemic at the height of the bubble, there are indications that CDO deal documents are not clear:

These bad decisions, in turn, have resulted in the collapse of many investment vehicles: more than 100 collateralised debt obligations (CDOs) and structured investment vehicles (SIVs) have already entered the murky post-event of default (EOD) state. This number will grow in the coming weeks.

Unfortunately, the legal documents that govern these transactions are so poorly written – full of ambiguities, inconsistencies, “circular references” and worse, contradictions – that many investors, trustees and respective legal advisors do not know how to interpret them.

The lawyers will feast!

Speaking of lawyers and their feasting, I was asked recently about BCE’s bonds following their triumph over the bondholders. It was one of Markit’s “CDS Deteriorators” on March 10, with 5-Year CDS yields increasing 73bp to 646bp. According to Markit’s CDS commentary for March 10:

BCE’s spreads widened on expectations that the company’s LBO will go ahead. A Quebec Court threw out a bondholder lawsuit that alleged the takeover of the Canadian telecoms company by an investment consortium was unlawful.

Volume returned to the preferred market today and was actually relatively heavy – the first time that’s happened in a while! I don’t know quite what to make of the price and volume activity in the PWF/GWO issues … there’s no news that I can see – it may just be a single manager re-jigging his portfolio. Or random chance!

| Note that these indices are experimental; the absolute and relative daily values are expected to change in the final version. In this version, index values are based at 1,000.0 on 2006-6-30 | |||||||

| Index | Mean Current Yield (at bid) | Mean YTW | Mean Average Trading Value | Mean Mod Dur (YTW) | Issues | Day’s Perf. | Index Value |

| Ratchet | 5.46% | 5.47% | 33,714 | 14.69 | 2 | +0.6357% | 1,095.5 |

| Fixed-Floater | 4.75% | 5.54% | 65,192 | 14.81 | 8 | +0.3328% | 1,046.7 |

| Floater | 4.73% | 4.81% | 85,992 | 15.75 | 2 | -0.2826% | 865.8 |

| Op. Retract | 4.84% | 3.11% | 75,909 | 2.93 | 15 | -0.1809% | 1,042.9 |

| Split-Share | 5.32% | 5.67% | 97,130 | 4.04 | 14 | +0.3192% | 1,033.5 |

| Interest Bearing | 6.17% | 6.52% | 68,570 | 4.23 | 3 | +0.6168% | 1,086.7 |

| Perpetual-Premium | 5.76% | 5.45% | 282,678 | 7.74 | 17 | +0.0534% | 1,023.3 |

| Perpetual-Discount | 5.46% | 5.52% | 261,975 | 14.61 | 51 | -0.0211% | 942.6 |

| Major Price Changes | |||

| Issue | Index | Change | Notes |

| GWO.PR.E | OpRet | -3.6399% | Now with a pre-tax bid-YTW of 4.97% based on a bid of 24.62 and a softMaturity 2014-3-30 at 25.00. |

| GWO.PR.H | PerpetualDiscount | -2.1885% | Now with a pre-tax bid-YTW of 5.55% based on a bid of 21.90 and a limitMaturity. |

| CM.PR.H | PerpetualDiscount | -1.1765% | Now with a pre-tax bid-YTW of 5.80% based on a bid of 21.00 and a limitMaturity. |

| PWF.PR.K | PerpetualDiscount | -1.0480% | Now with a pre-tax bid-YTW of 5.53% based on a bid of 22.66 and a limitMaturity. |

| WFS.PR.A | SplitShare | +1.0152% | Asset coverage of just under 1.7:1 as of March 6, according to Mulvihill. Now with a pre-tax bid-YTW of 5.80% based on a bid of 9.95 and a hardMaturity 2011-6-30 at 10.00. |

| BCE.PR.R | FixFloat | +1.0417% | |

| BCE.PR.B | FixFloat | +1.0417% | |

| BNS.PR.M | PerpetualDiscount | +1.0427% | Now with a pre-tax bid-YTW of 5.35% based on a bid of 21.32 and a limitMaturity. |

| FBS.PR.B | SplitShare | +1.1579% | Asset coverage of just under 1.6:1 as of March 6, according to TD Securities. Now with a pre-tax bid-YTW of 5.94% based on a bid of 9.61 and a hardMaturity 2011-12-15 at 10.00. |

| MFC.PR.A | OpRet | +1.2785% | Now with a pre-tax bid-YTW of 3.89% based on a bid of 25.35 and a softMaturity 2015-12-18 at 25.00. |

| BSD.PR.A | InterestBearing | +1.5991% | Asset coverage of 1.6+:1 as of March 7, according to Brookfield Funds. Now with a pre-tax bid-YTW of 6.90% (mostly as interest) based on a bid of 9.53 and a hardMaturity 2015-3-31 at 10.00. |

| W.PR.H | PerpetualDiscount | +1.6352% | Now with a pre-tax bid-YTW of 5.70% based on a bid of 24.24 and a limitMaturity. |

| BNA.PR.C | SplitShare | +2.2947% | Asset coverage of 3.3+:1 as of January 31, according to the company. Now with a pre-tax bid-YTW of 7.03% based on a bid of 20.06 and a hardMaturity 2019-1-10 at 25.00. Compare with BNA.PR.A (5.67% to call 2008-10-31) and BNA.PR.B (7.71% to hardMaturity 2016-3-25). |

| Volume Highlights | |||

| Issue | Index | Volume | Notes |

| PWF.PR.J | OpRet | 100,272 | Desjardins crossed 100,000 at 26.10. Now with a pre-tax bid-YTW of 3.79% based on a bid of 26.08 and a call 2010-5-30 at 25.00. |

| PWF.PR.D | OpRet | 94,410 | Nesbitt crossed 60,000 at 26.49. Now with a pre-tax bid-YTW of –7.46% based on a bid of 26.41 and a call 2008-4-10 at 26.00. Will yield 4.02% if it makes it to the softMaturity 2012-10-30 at 25.00. |

| PWF.PR.K | PerpetualDiscount | 29,300 | Nesbitt crossed 25,000 at 22.70. Now with a pre-tax bid-YTW of 5.53% based on a bid of 22.66 and a limitMaturity. |

| RY.PR.G | PerpetualDiscount | 28,030 | Now with a pre-tax bid-YTW of 5.37% based on a bid of 21.16 and a limitMaturity. |

| TD.PR.O | PerpetualDiscount | 24,831 | Now with a pre-tax bid-YTW 5.23% based on a bid of 23.45 and a limitMaturity. |

There were thirty-three other index-included $25-pv-equivalent issues trading over 10,000 shares today.