The USD has been hammered to the point where it is at parity with CAD. Fortunately for Americans, however, there is some evidence that import prices remain constant in USD terms:

“Foreign exporters have simply been more willing to vary their margins when selling into the U.S. market. Moreover, this difference in pricing behavior seems, if anything, to have become more pronounced in recent years,” the study says.

Unfortunately:

There is an important caveat to the study’s implications for the dollar’s recent fall. It notes that local-currency profit margins for foreign companies selling to the U.S. peaked in 2002 and have since declined, showing the dollar’s fall is taking a toll on profit margins. “It remains an open issue as to whether profit margins on exports to the United States are now ‘too narrow’ or margins were unusually high several years ago,” they say. Left unsaid: if indeed margins are “too low” now, then exporters may be reaching the limit of their ability to keep prices in the U.S. stable, and the dollar’s drop may be more inflationary in coming years than it has been to date.

The USA will not return to fiscal sanity until forced – the way Canada was forced to get religion in the ’90’s and that wasn’t a whole lot of fun for a lot of people. We’ll see.

US ABCP outstanding declined again this week, as reported by Bloomberg:

The U.S. commercial paper market shrank for a sixth week, extending the biggest slump in at least seven years and signaling Federal Reserve interest rate cuts haven’t yet drawn investors back to short-term debt.

I suggest that confidence is an awfully hard thing to regain, once lost. There are a lot of firms dancing close to the edge; a lot of financing is still being done at high rates, with all terms of USD ABCP yielding more than 5% – about half a point more than financial paper. And those, remember are average rates. While the cuts will have put a lot of companies back into positive carry territory, they will be much more risk averse than they were; at the margins, structures will be delevered and terms will be extended into bonds.

My guess is that we’ll see continued delevering at least until Christmas, as the market adjusts to whatever the new paradigm is. But who knows? Pays yer money and take yer chances.

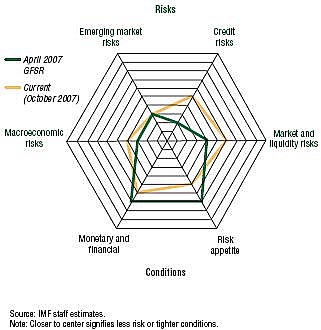

Charles Wyplosz makes an argument at Voxeu in defense of the wholesale liquidity injection, accepting as a necessary evil the fact that ‘bad banks’ will benefit from this injection as much as bad banks. While agreeing with his conclusions, I disagree with his arguments, which are very interventionist –

Once the dust settles, the time of punishment will come. Inquiries should be conducted and those who violated the law must be brought to account.

Let’s start with first principles – Wyplosz states that the root of the problem to be addressed is:

What each financial institution does not know, and should not know, is what is on the books of the other financial institutions with which it trades daily. The old result, which goes under the colourful name of lemon’s markets, is that, suspecting the worst, no financial institution wants to lend to the others. The consequence is that liquidity is plentiful inside most financial institutions, but not available on the interbank market

I take the view that the problem is not so much one of the financial institutions not trusting one another – although that clearly is a factor – as one whereby the banks do not know which of their contingent lines will be drawn on in the near future. Countrywide Credit rather famously drew down USD 11.5-billion in one shot in August; this will not have been an isolated occurance. The banks will, I suspect, be happily engaged in the practice of grossing up their balance sheets by lending to their own customers right now, at penalty rates. This will be consistent with the work of Gatev & Strahan which I quoted on September 14. The banks, wishing to keep their powder dry, will not make term loans to one another (a term loan meaning, in this, ‘longer than overnight’) because their customers might want the lines tomorrow.

In such a case, liquidity injection is the desired policy since as long as there is liquidity then well-capitalized banks will be able to make term loans while at the same time retaining the extra capacity required to meet their commitments. My concern – which I am sure will be explicitly addressed by regulators over the next year – is whether such contingent claims from customers and off-balance sheet entities (e.g., bank controlled ABCP issuers) are adequately reflected in risk-weighted assets.

As far as punishment for excessive risk-taking is concerned … the market is meting that out quite efficiently, as Northern Rock’s shareholders can testify. Coventree’s employees are in a position to confirm this. The ‘real banks’ have bailed out the ‘non-banks’ to a greater or lesser extent, which is their function, at a greater or lesser cost to the non-bank’s shareholders, which is their punishment.

BoE Governor King testified to a parliamentary committee that:

U.K. banking laws prevented the central bank from a covert rescue of Northern Rock Plc, which it would have preferred.

“The bank would have preferred to have acted covertly as lender as last resort, to have lent to Northern Rock without publishing it,” King told a parliamentary committee in London today. “As a result of the market abuses directive (of 2005) we were unable to carry that out.”

This is interesting. Those with long memories will remember the Panic of 1825 and commentary by Larry Neal that:

The first mention of the crisis occurs on December 8, 1825, when “The Governor [Cornelius Buller] acquainted the Court that he had with the concurrence of the Deputy Governor [John Baker Richards] and several of the Committee of Treasury afforded assistance to the banking house of Sir Peter Pole, etc.” This episode is described in vivid detail by the sister of Henry Thornton Jr., the active partner of Pole, Thornton & Co. at the time. On the previous Saturday, the governor and deputy governor counted out £400,000 in bills personally to Henry Thornton, Jr., at the Bank without any clerks present. All this was done to keep it secret so that other large London banks would not press their claims as well. A responsible lender of last resort would have publicized the cash infusion to reassure the public in general. Instead, the run on Pole & Thornton continued unabated, causing the company to fail by the end of the week. Then the deluge of demands for advances by other banks overwhelmed the Bank’s Drawing Office.

The propriety of the BoE’s actions will surely be debated for decades. If the two views can be reconciled at all, one mechanism is through introduction of the idea that the public no longer trusts public institutions – at least, not to the extent that they did in 1825, when a man’s word was his bond. There have been far too many instances in recent history when those in authority have stated ‘We will not devalue, we will not devalue, we will not devalue, we have just devalued, we will not devalue again, we will not devalue again …’

And they do this, of course, without blushing.

Another way to reconcile the two theses is through introducing the idea of discretion; it may well be that Governor King agrees with the publicity desired by Neal in general, but not in this particular instance, for very well-founded reasons. And it may be that Neal will agree with him. It has always amazed me to see how much money is being paid to people – judges, regulators, high-school principals, whatever – while at the same time their discretion is circumscribed to ludicrous extremes with often ludicrous results. Perhaps Northern Rock was one of these time … perhaps not. The facts will emerge at some time long after public interest has evaporated, and become the topic of discussion in specialized journals.

In sub-prime news, it appears that credit anticipation plays by Goldman Sachs and Bear Stearns were right and wrong, respectively. And … a CDO has blown up, a victim of mark-to-market:

TCW Asset Management, the money manager owned by France’s second-biggest bank, is selling $3.2 billion of mortgage securities backing collateralized debt obligations after the value of the bonds fell.

…

Fitch Ratings last week said another five Westways Funding CDOs might have to sell assets under the CDOs’ rules.

…

A $200 million CDO in the Enhanced Mortgage-Backed Securities series of market-value CDOs managed by MassMutual Financial Group’s Babson Capital Management LLC has finished liquidating after failing a similar test, Fitch said yesterday.

Isn’t forced liquidation fun? Boy, the guys who have all their analytical ducks in a row and have some capital available must be making a killing. Unfortunately, these buyers include the US GSE’s, who are able to finance themselves due only to the implicit guarantee of the US Government – the market would never allow them to survive as independent companies with their current capital structure. There is some pressure to reduce this source of false economic signals. Tom Graff has prepared a numerical example of why you need players in the system who are prepared to increase leverage when nobody else will – currently this role is being played largely by the banks and the US GSEs.

US Equities had a bad day, attributed to fears that the Fed Cut – and more like it? – will cause inflation; the excuse for Canadian equities was the fear of expropriation … er … I mean, a fairer royalty sharing scheme in the oil patch. CNR was in the news again …

Canadian National Railway Co. (CNR CN) declined C$1.19, or 2.1 percent, to C$56.65. The country’s largest railroad agreed to sell its Central Station complex in Montreal to Homburg Invest Inc. (HII/B CN) for C$355 million ($350 million). Canadian National will lease back its headquarters and passenger rail facilities from Homburg as part of the agreement, the Montreal-based carrier said in a statement. Homburg shares fell 15 cents, or 2.7 percent, to C$5.50.

Yesterday I mentioned CNR’s new bond issue … they seem to be raising a substantial amount of cash. An answer may – may! – be these notes in their financials:

Revolving credit facility

As at June 30, 2007, the Company had letters of credit drawn on its U.S.$1 billion revolving credit facility of $303 million ($308 million as at December 31, 2006) and had U.S.$442 million (Cdn$471 million) of borrowings under its commercial paper program (nil as at December 31, 2006) at an average interest rate of 5.29%.

Accounts receivable securitization

The Company has a five-year agreement, expiring in May 2011, to sell an undivided co-ownership interest of up to a maximum of $600 million in a revolving pool of freight receivables to an unrelated trust.

At June 30, 2007, the Company had sold receivables that resulted in proceeds of $575 million under this program ($393 million at December 31, 2006). The retained interest in the receivables was approximately 10% of this amount and is recorded in Other current assets. At June 30, 2007, the servicing asset and liability were not significant.

Delevering time! Term Extension Time! Note that I spent a grand total of about 45 seconds looking at their financials … I bring this up as something interesting to be investigated further. If anybody has any (links to) interesting commentary, let me know!

Treasuries had a horrible day, with the ten-year falling in price over a buck, with steepening. Would you like your Fed Cut with a side of inflation? I’m unable to find a good link to Canadian bonds – not surprising, given the pathetic state of Canadian media, and even good old Reuters let me down today – but trust me, Canadas did horribly too. Just not as horribly as Treasuries.

Volume returned to the preferred share market today, with some nice chunky crosses getting done. The various floating rate indices were dragged down by BCE issues, presumably a reaction to yesterday’s news that the bondholders are going to fight the Teachers’ deal in court.

| Note that these indices are experimental; the absolute and relative daily values are expected to change in the final version. In this version, index values are based at 1,000.0 on 2006-6-30 |

| Index |

Mean Current Yield (at bid) |

Mean YTW |

Mean Average Trading Value |

Mean Mod Dur (YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

4.80% |

4.76% |

1,248,908 |

15.75 |

1 |

-0.0816% |

1,043.7 |

| Fixed-Floater |

4.85% |

4.77% |

98,445 |

15.80 |

8 |

-0.3903% |

1,031.2 |

| Floater |

4.49% |

1.83% |

85,557 |

10.73 |

3 |

-0.4069% |

1,045.8 |

| Op. Retract |

4.83% |

3.99% |

75,771 |

3.99 |

15 |

-0.0766% |

1,029.0 |

| Split-Share |

5.15% |

4.87% |

97,729 |

3.84 |

13 |

-0.1948% |

1,043.3 |

| Interest Bearing |

6.30% |

6.76% |

65,451 |

4.26 |

3 |

+0.0012% |

1,036.2 |

| Perpetual-Premium |

5.48% |

5.06% |

90,996 |

5.27 |

24 |

-0.0755% |

1,030.7 |

| Perpetual-Discount |

5.05% |

5.09% |

245,888 |

14.97 |

38 |

-0.0003% |

986.2 |

| Major Price Changes |

| Issue |

Index |

Change |

Notes |

| BNA.PR.C |

SplitShare |

-2.4932% |

Asset coverage of just over 3.8:1 as of July 31, according to the company. Now with a pre-tax bid-YTW of 6.13% based on a bid of 21.51 and a hardMaturity 2019-1-10 at 25.00. That’s an interest equivalent of almost 8.6% based on a 1.4x equivalency factor! |

| IAG.PR.A |

PerpetualDiscount |

-1.0799% |

Now with a pre-tax bid-YTW of 5.03% based on a bid of 22.90 and a limitMaturity. |

| BAM.PR.B |

FixFloat |

-1.0288% |

|

| BCE.PR.Z |

FixFloat |

-1.0221% |

|

| Volume Highlights |

| Issue |

Index |

Volume |

Notes |

| GWO.PR.E |

OpRet |

184,603 |

TD crossed 21,900 at 25.65. Now with a pre-tax bid-YTW of 3.86% based on a bid of 25.70 and a call 2011-4-30 at 25.00. |

| FBS.PR.B |

SplitShare |

366,750 |

Nesbitt bought 97,000 from Scotia at 10.05 and crossed 250,000 at the same price. Asset coverage of almost 2.9:1 as of September 13, according to TD. Now with a pre-tax bid-YTW of 3.31% based on a bid of 10.05 and a call 2008-1-14 at 10.00. |

| CU.PR.A |

PerpetualPremium |

128,434 |

Now with a pre-tax bid-YTW of 5.11% based on a bid of 25.80 and a call 2012-3-31 at 25.00. |

| PWF.PR.E |

PerpetualPremium |

106,900 |

Nesbitt crossed 104,000 at 25.45. Now with a pre-tax bid-YTW of 5.35% based on a bid of 25.40 and a call 2013-3-2 at 25.00. |

| SLF.PR.E |

PerpetualDiscount |

104,250 |

Nesbitt crossed 100,000 at 23.03. Now with a pre-tax bid-YTW of 4.92% based on a bid of 22.95 and a limitMaturity. |

| CCS.PR.C |

Scraps (would be PerpetualDiscount, but there are credit concerns) |

102,250 |

Scotia crossed 100,000 at 22.10. Now with a pre-tax bid-YTW of 5.69% based on a bid of 22.05 and a limitMaturity. |

| GWO.PR.F |

PerpetualPremium |

101,086 |

Nesbitt crossed 100,000 at 26.95. Now with a pre-tax bid-YTW of 2.39% based on a bid of 26.90 and a call 2008-10-30 at 26.00. |

There were twenty-one other $25-equivalent index-included issues trading over 10,000 shares today.