Thanks, Rebel Traders (via WSJ)!

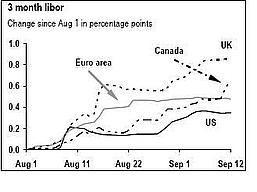

Inflation numbers came out today, with the core rate in the US easing to 2.1% yoy, which some have taken as a validation of the Fed’s rate cut. The core rate in Canada is 2.1% yoy, but there are storm clouds on the horizon:

Signs inflation may pick up include a Sept. 14 Statistics Canada report showing unit labor costs, the cost of paying workers to produce an extra unit of a good, jumped 4.8 percent in the second quarter from a year earlier, the fastest since 1991. Also, average hourly wages rose the fastest in six years in August with the jobless rate at a 33-year low of 6 percent.

There are hopes that the PCE index will also come down – we will see!

Another interesting trend is the increased linkage between energy and foodstuff prices. We’ve heard about the Italian pasta strike and Mexican tortilla protests. We may well see Canadian Jos. Louis riots if the trend continues.

The authorities in general are loosening standards! Do they know something we don’t or what? The Bank of England has reversed its position on loosing loan standards, while the portfolio limits on the US Government Sponsored mortgage lenders are being relaxed. I suspect that James Hamilton will not be pleased. In addition to raising the portfolio limits, there is also pressure to increase the permitted size of each mortgage: Bernanke is not pleased:

“Both the size and composition of the portfolios should be tied to reforms that both reduce the systemic risks posed by the portfolios and also clarify the public purpose,” Bernanke said.

But – look at the situation: record foreclosures:

U.S. home prices fell by a record 3.2 percent in the second quarter, according to the S&P/Case-Shiller Index. Lawrence Yun, chief economist for the Chicago-based National Association of Realtors, has warned that year-over-year prices will fall for the first time since the Great Depression of the 1930s.

And the Congressional Budget Office has adopted a somewhat gloomy tone:

The recent market turmoil and a weakening of consumer confidence could “pose serious economic risks,” and as a result have “heightened” the chance of a recession, Congressional Budget Office Director Peter Orszag says in testimony before the Joint Economic Committee this morning.

The Brookings institution has published a commentary on current economic and regulatory issues – the author concludes, inter alia, that although the Fed wasn’t perfect in the 2004-06 period, they weren’t all that wrong, either. He also agrees with most of Levitt’s credit rating agency recommendations.

On September 10 I noted a report of the destabilizing effect of mark-to-market accounting; Moody’s has produced an interesting commentary:

The world would be a much safer place if all securities were held by “real money” buy-and-hold investors who did not have to mark to market, and who therefore did not have to make forced sales into panicked markets. Unfortunately, literally trillions of dollars of securities are now held by leveraged mark-to-market institutions relying on other people’s money to finance sometimes opaque, complex and risky investments.

CNR had a new bond issue today for USD 550-million that showed a few signs of the times: the purpose of the issue is to repay commercial paper and reduce the size of the accounts receivable securitization programme; and there is a poison put, whereby the bonds are puttable to the company at $101 upon a credit downgrade. While as a bond-guy I like the poison-put feature (and will pay more for the issue than its comparables because of it), as an amateur-economist guy and equity-guy, I’m not so sure. This will have the effect of forcing the bond market’s mark-to-market woes onto the operating company, which will have to find financing (or sweeten the terms of the deal and negotiate their way out of it) at the worst possible time. Hmm …

Other issuers today were Lehman and GE as well as Suncor. Money abounds for solid credits; the market is operating as it should in this, the most perfect of all possible worlds.

Another hedge fund has stopped redemptions, in what seems like a rather complex story in which the portfolio manager quit:

Homm said yesterday he quit after directors declined to follow his lead by turning down bonuses and contributing shares to support the funds during market turmoil. Absolute Capital said today it approved the bonuses Homm recommended.

Homm didn’t answer calls to his mobile phone, and Chief Executive Officer Jonathan Treacher didn’t immediately return calls to his office and mobile phone. In an interview yesterday, Treacher said he was “surprised” by Homm’s departure. “We never discussed him resigning,” he said.

The BCE saga, last reviewed about five weeks ago has taken another twist: the bondholders are going to court:

They want the deal declared a “reorganization” under the terms of the 1976 and 1996 trust indentures, which would require bondholder approval.

BCE bondholders argue the takeover is unfair will see them take “significant losses” since the debentures have lost “hundreds of millions of dollars” in market value since talks of the company going private began earlier this year.

As well, the debt for the leveraged buyout and related interest costs have caused one rating agency to downgrade the debentures from investment grade to junk status, the bonderholders argue.

It’s interesting that a rating agency downgrade should be considered worthy of mention – I thought we weren’t paying attention to them any more. PrefBlog’s crack investigative reporting team has discovered the fact that the issuer, BCE, is paying the credit ratings agencies! Video at 11.

Brad Setser has reviewed the larger implications of the liquidity crunch:

My wild guess is that some kind of new financial innovation will be necessary to end the (financial) droid wars …

Either that or there may be a lot of CDOs containing some housing exposure may be sitting around on various firms balance sheets for a very long time.

My guess? Hedge funds will arise that are more than happy to take care of the problem at a discount to market. I don’t think the banks will mind – the big losses will have been taken by by the original owners that were forced to sell. Not a big deal, really.

Cleveland Fed researchers have reviewed the slope of the yield curve again and its implications for recession probabilities, but note:

First, probabilities are themselves subject to error, as is the case with all statistical estimates. Second, other researchers have postulated that the underlying determinants of the yield spread today are materially different from the determinants that generated yield spreads during prior decades. Differences could arise from changes in international capital flows and inflation expectations, for example.

I suggest that any such readings taken now will reflect plain and simple panic. Let’s wait until panic has subsided and uncertainty has returned to normal levels before drawing any conclusions from the slope of the government yield curve.

US Equities continued their huge rally, but Canadian equities fell:

Canadian stocks fell, led by Suncor Energy Inc., on concern that a proposed oil and gas royalty increase may cut energy companies’ profits.

The province of Alberta should raise royalty rates to reap the benefits of rising prices, a report from a government-appointed task force said yesterday after markets closed.

The phrase “markets closed” should be read “markets closed Tuesday“, by the way.

Treasuries fell with steepening due to inflation fears. Canadas followed.

Something of an odd Pref market today, with the PerpetualPremiums down and the PerpetualDiscounts up … given the action in the bond market, with the long end having an awful day, the opposite might have been expected. Assigning reasons to day-to-day fluctuations in any market, let alone the pref market, is something of an exercise in frustration, so we’ll just let that slide, shall we? Volume picked up a little today, a good sign.

| Note that these indices are experimental; the absolute and relative daily values are expected to change in the final version. In this version, index values are based at 1,000.0 on 2006-6-30 | |||||||

| Index | Mean Current Yield (at bid) | Mean YTW | Mean Average Trading Value | Mean Mod Dur (YTW) | Issues | Day’s Perf. | Index Value |

| Ratchet | 4.82% | 4.77% | 1,300,892 | 15.73 | 1 | +0.0000% | 1,044.5 |

| Fixed-Floater | 4.84% | 4.75% | 99,969 | 15.83 | 8 | +0.3184% | 1,035.5 |

| Floater | 4.47% | 1.82% | 84,202 | 10.79 | 3 | +0.1232% | 1,050.1 |

| Op. Retract | 4.83% | 3.86% | 76,114 | 3.86 | 15 | -0.0376% | 1,029.8 |

| Split-Share | 5.14% | 4.88% | 95,623 | 3.86 | 13 | -0.2242% | 1,045.4 |

| Interest Bearing | 6.30% | 6.75% | 65,855 | 4.26 | 3 | -0.3362% | 1,036.2 |

| Perpetual-Premium | 5.48% | 5.09% | 90,310 | 5.28 | 24 | -0.1201% | 1,031.5 |

| Perpetual-Discount | 5.04% | 5.09% | 245,066 | 15.72 | 38 | +0.1156% | 986.2 |

| Major Price Changes | |||

| Issue | Index | Change | Notes |

| BSD.PR.A | InterestBearing | -1.6358% | Asset coverage of just under 1.8:1 as of September 14, according to the company. Now with a pre-tax bid-YTW of 7.82% (mostly interest) based on a bid of 9.02 and a hardMaturity 2015-3-31 at 10.00. |

| BNA.PR.C | SplitShare | -1.5618% | Asset coverage of 3.83:1 as of July 31, according to the company. Now with a pre-tax bid-YTW of 5.83% based on a bid of 22.06 and a hardMaturity 2019-1-10 at 25.00. |

| PWF.PR.L | PerpetualDiscount | +1.0331% | Now with a pre-tax bid-YTW of 5.28% based on a bid of 24.45 and a limitMaturity. |

| BCE.PR.G | FixFloat | +1.4015% | |

| Volume Highlights | |||

| Issue | Index | Volume | Notes |

| FFN.PR.A | SplitShare | 110,900 | A split share, top of the list! Scotia crossed 96,300 at 10.39. Asset coverage of 2.53:1 as of September 14, according to the company. Now with a pre-tax bid-YTW of 4.69% based on a bid of 10.38 and a hardMaturity 2014-12-01 at 10.00. |

| BCE.PR.G | FixFloat | 39,700 | TD crossed 17,400 at 24.65. |

| BMO.PR.H | PerpetualPremium | 24,200 | Desjardins crossed 23,400 at 25.90. Now with a pre-tax bid-YTW of 4.67% based on a bid of 25.87 and a call 2013-3-27 at 25.00. |

| BAM.PR.N | PerpetualDiscount | 17,650 | Closed at 20.20-25, 2×16. The virtually identical BAM.PR.M closed at 20.45-56, 5×1. BAM.PR.N now has a pre-tax bid-YTW of 5.91% based on a bid of 20.20 and a limitMaturity. |

| NA.PR.L | PerpetualDiscount | 17,533 | Now with a pre-tax bid-YTW of 5.30% based on a bid of 23.11 and a limitMaturity. |

There were eleven other $25-equivalent index-included issues trading over 10,000 shares today.