On April 30, S&P published its 2014 Annual Global Corporate Default Study And Rating Transitions:

In a year marked by considerable geopolitical turmoil, the ending of the Federal Reserve’s monthly asset purchases, and the steep decline in the price of oil, corporate borrowers fared very well by historical standards. In the full year, 60 global corporate issuers defaulted, considerably lower than the 81 last year and the lowest total since 2011 (see table 1). These 60 defaulted issuers accounted for a total of $91.6 billion in debt, down from $97.3 billion in 2013.

Overall, credit quality and rating stability remained high in 2014 (see table 6). The ratio of downgrades to upgrades increased marginally relative to 2013, but the rate of upgrades still outpaced that of downgrades. Overall, the percentage of rating actions decreased, and the magnitude of individual rating changes remained muted. This pushed the average number of notches recorded among downgrades to 1.36 from 1.38 in 2013. Meanwhile, the average number of notches for upgrades remained nearly unchanged, at 1.16 versus 1.15 in 2013 (see chart 13). (Watch the related CreditMatters TV segment titled, “Standard & Poor’s Global Corporate Default And Rating Transitions Study,” dated April 30, 2015.)

Overview

- •The number of global defaults in 2014 declined to 60 from 81 in 2013. This helped push the global speculative-grade default rate down to 1.42% from 2.28% at the end of 2013. Similar to 2013, this decline is a result of both a smaller number of defaults and an increase in the number of speculative-grade issuers in 2014–up to 3,163 from 2,804 a year earlier.

- •The one-year global Gini ratio rose to 93 in 2014, which is the second highest in 34 years. This is largely attributable to the roughly 91% of the rated defaulters in 2014 beginning the year with ratings of ‘B-‘ or lower.

- •The overall rate of rating actions decreased in 2014. The downgrade rate decreased to 8.4% from 9.4% in 2013, while the upgrade rate declined to 9.3% from 11.4%. Ratings stability increased, with the rate of unchanged ratings hitting a 10-year high of 74.5%.

- •Consistent with past years, the U.S. continues to account for the majority of defaults globally in 2014, at 55%. However, this is the lowest percentage in the past 34 years. Following the U.S., emerging markets accounted for just over 25% of the remaining defaulters.

They have also published a bit more commentary:

U.S. corporate credit performed exceptionally well in 2014 as the number of rated companies defaulting declined to its lowest number since 2007. While the Federal Reserve completed its round of tapering, winding down its monthly large-scale asset purchases, interest rates for highly rated credits fell from already low levels. Corporate bond issuance surpassed $1 trillion for a third consecutive year, and investment-grade and Treasury bond yields fell. As the speculative-grade market faced rising volatility during the year brought about by falling oil prices and rising geopolitical strains, the speculative-grade default rate fell to below 2%, less than one half of its long-term average. Slow but steady economic growth continued to support business conditions, and the upgrade to downgrade ratio improved as more U.S. companies were upgraded than downgraded in 2014. The number of U.S. corporate defaulters fell to 33 from 45 in 2013. The defaulting companies were either unrated or were rated ‘B-‘ and lower as of the beginning of 2014, consistent with our findings that Standard & Poor’s Ratings Services’ U.S. corporate credit ratings continue to serve as effective indicators of relative credit risk. (Watch the related CreditMatters TV segment titled, “Standard & Poor’s U.S. Corporate Default And Rating Transitions Study,” dated May 11, 2015.)

Overview

- •In 2014, 33 U.S. companies with $82 billion in outstanding debt defaulted; by comparison, 45 U.S. corporates defaulted with $64.9 billion of outstanding debt in 2013.

- •The U.S. speculative-grade (‘BB+’ and lower) corporate default rate fell to 1.59% as of year-end 2014 from 2.16% as of year-end 2013. Of the companies that defaulted in 2014, the highest rated was ‘B-‘.

- •Companies in the lowest rating categories had the highest default rates: 25% of the companies rated ‘CCC’/’C’ at the beginning of the year had defaulted by the end of the year.

- •The one-year Gini ratio for Standard & Poor’s 2014 ratings’ performance climbed to a new high of 96.1%. This is the highest one-year Gini recorded for U.S. corporates in our data going back to 1981.

- •Overall, ratings were more stable in 2014 than in 2013: Nearly 76% of ratings were unchanged in 2014, up from 72% the prior year.

SEC Chair Mary Jo White gave a speech lauding the opportunities that market complexity gives for regulatory employment, and the fine job the SEC is doing, titled Optimizing Our Equity Market Structure. These were Opening Remarks at the Inaugural Meeting of the Equity Market Structure Advisory Committee:

It is fitting that today we are starting our market structure discussion with an assessment of Rule 611 of Regulation NMS — the order protection rule. The selection of this rule for the inaugural meeting is reflective of how important it is to examine the fundamentals of our current market and regulatory structure, to explore their impact and assess their continued utility. This is not done just for an interesting discussion — although I am sure it will be that. Rather, we are about the serious business of optimizing the structure of our equity markets through a careful, data-driven assessment where no issue is off limits or any assumption unquestioned. And Rule 611 is most certainly a rule that features prominently in the discussion of market structure, with different views of its various impacts, including critiques that it has: (1) contributed to excessive fragmentation; (2) led to increased off-exchange trading; (3) harmed institutional investors; and (4) failed to achieve the objective of enhancing displayed liquidity. The Division of Trading and Markets has prepared and posted on our website a memorandum that is intended to help explore the extent to which these claims may or may not be accurate. Addressing Rule 611 will no doubt serve to highlight the other forces that have shaped our market structure, whether they be regulatory, competitive, or technological.

Rule 611 is part of Regulation NMS:

Regulation NMS includes new substantive rules that are designed to modernize and strengthen the regulatory structure of the U.S. equity markets. First, the “Order Protection Rule” requires trading centers to establish, maintain, and enforce written policies and procedures reasonably designed to prevent the execution of trades at prices inferior to protected quotations displayed by other trading centers, subject to an applicable exception. To be protected, a quotation must be immediately and automatically accessible. Second, the “Access Rule” requires fair and non-discriminatory access to quotations, establishes a limit on access fees to harmonize the pricing of quotations across different trading centers, and requires each national securities exchange and national securities association to adopt, maintain, and enforce written rules that prohibit their members from engaging in a pattern or practice of displaying quotations that lock or cross automated quotations. Third, the “Sub-Penny Rule” prohibits market participants from accepting, ranking, or displaying orders, quotations, or indications of interest in a pricing increment smaller than a penny, except for orders, quotations, or indications of interest that are priced at less than $1.00 per share. Finally, the Commission is adopting amendments to the “Market Data Rules” that update the requirements for consolidating, distributing, and displaying market information, as well as amendments to the joint industry plans for disseminating market information that modify the formulas for allocating plan revenues (“Allocation Amendment”) and broaden participation in plan governance (“Governance Amendment”).

After all the garbage coming from the regulators, it’s nice to see that someone gets it:

An ex-Jefferies & Co. trader convicted last year of lying to buyers and sellers of mortgage-backed bonds may have done nothing worse in one judge’s view than what a homeowner does when selling a house.

There’s a “certain amount of license and puffery” that goes on in the bond market, especially with “big boys” “who are capable of very sophisticated analysis,” U.S. Circuit Judge Barrington D. Parker said Wednesday during the appeal of Jesse Litvak’s conviction. “This kind of thing goes on all the time.”

Litvak, 40, was found guilty by a federal jury in New Haven, Connecticut, in March 2014, becoming the first person convicted of fraud tied to the Troubled Asset Relief Program set up by the U.S. amid the 2008 financial crisis. On appeal, Litvak says the case would make crimes out of statements in everyday negotiations such as car sales and that his lies weren’t material to the bond transactions.

Parker, one of three judges hearing the case in the U.S. Court of Appeals in New York, may agree. He asked Assistant U.S. Attorney Jonathan Francis if a real estate broker would be making a material misrepresentation by falsely telling a home buyer that a seller wouldn’t accept a lower offer.

Francis said the rules are different in the securities industry and that a higher standard is needed to discourage deceit and ensure that markets are fair and that investors won’t be ripped off.

Mr. Francis’ position is, of course, bullshit. The reason there is more regulation in the securities industry than in real-estate is because there are more layers of middlemen in securities transactions and these middlemen are giant corporations who pay regulatory fees as a part of doing business and pass them on to clients without itemization. If clients knew how much regulation was costing them, directly and indirectly, there would be a lot less regulation.

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts gaining 24bp, FixedResets off 3bp and DeemedRetractibles down 7bp. The performance highlights table shows volatility remains a big factor, with Enbridge issues prominent on the bad side. Volume was on the low side of average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

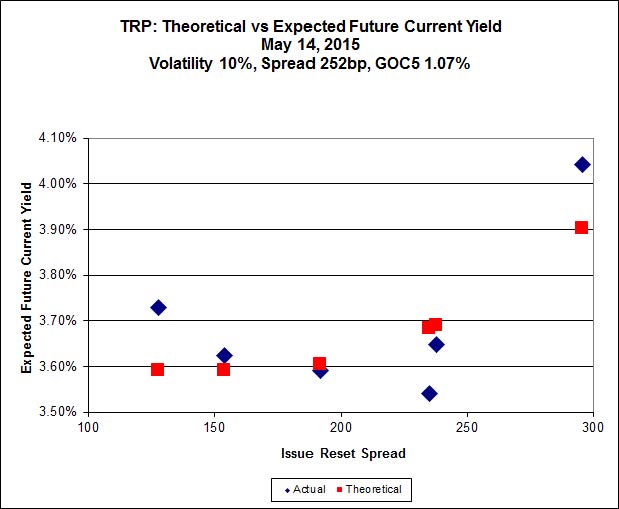

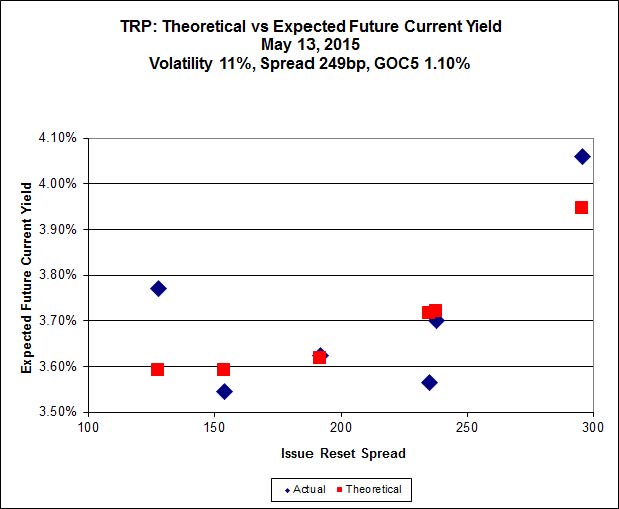

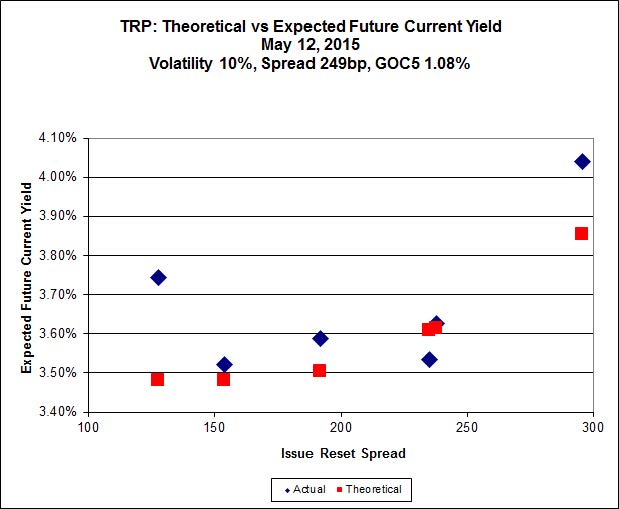

Here’s TRP:

Click for Big

Click for BigTRP.PR.E, which resets 2019-10-30 at +235, is bid at 24.20 to be $0.99 rich, while TRP.PR.B, resetting 2015-6-30 at +128, is $0.79 cheap at its bid price of 15.78.

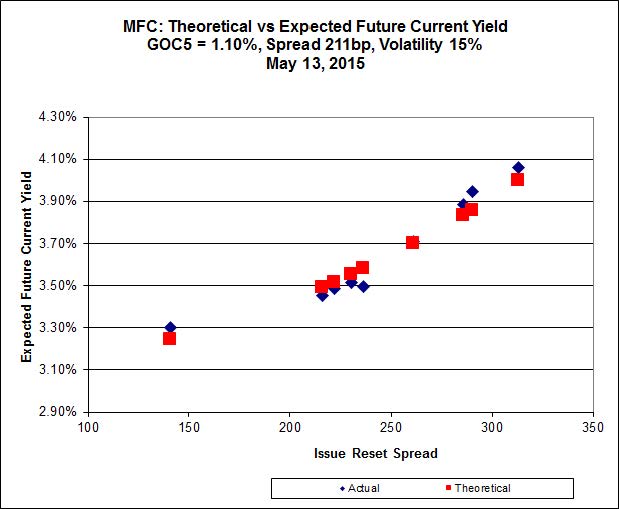

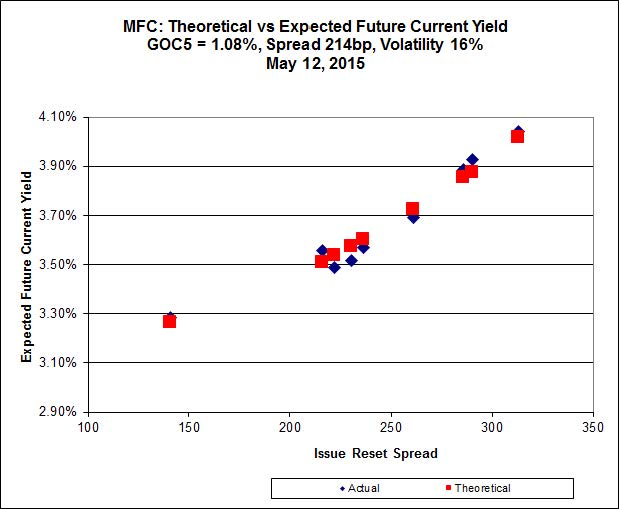

Click for Big

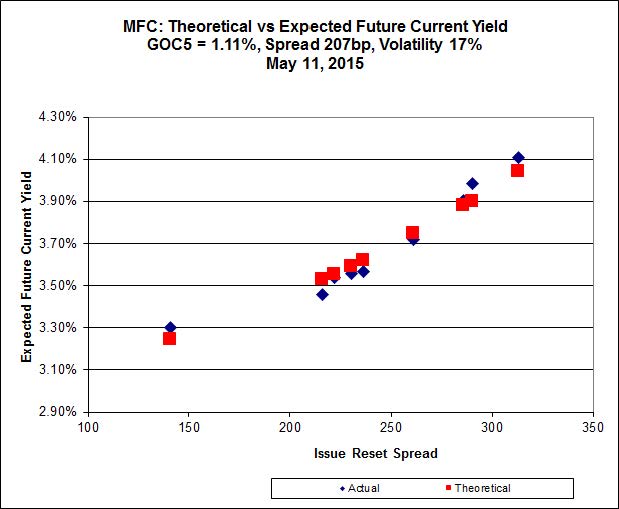

Click for BigAnother excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.M, resetting at +236 on 2019-12-19, bid at 24.75 to be $0.60 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 25.33 to be $0.61 cheap.

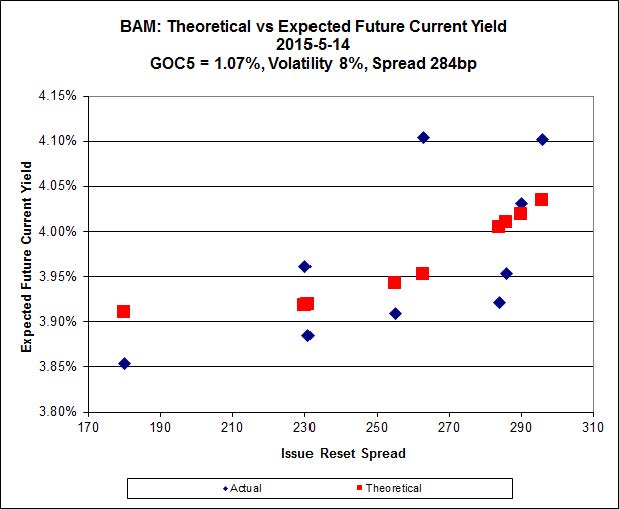

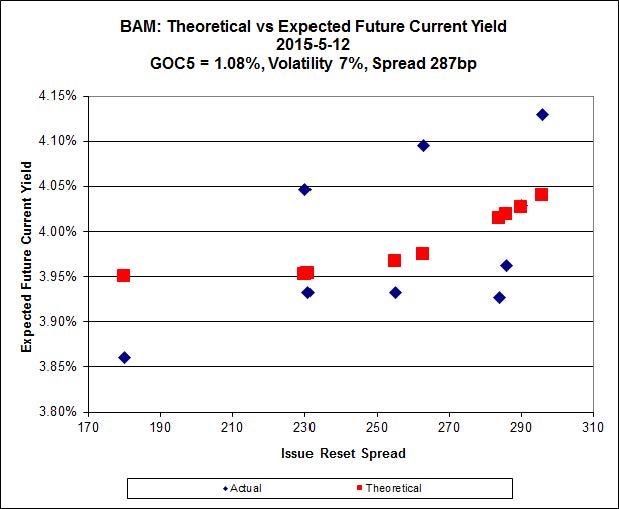

Click for Big

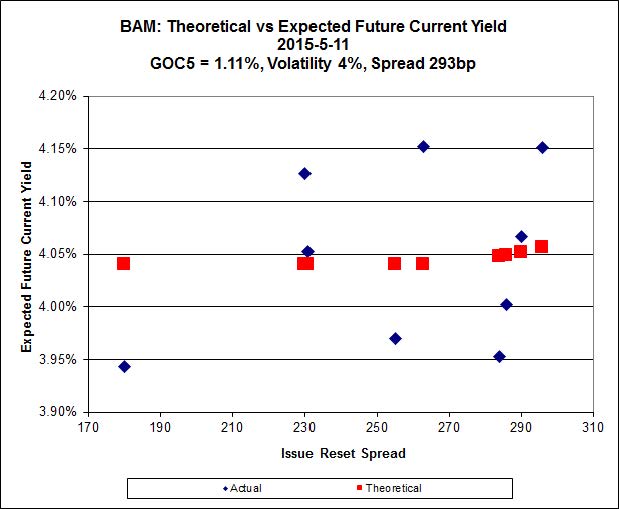

Click for BigThe cheapest issue relative to its peers is BAM.PF.B, resetting at +263bp on 2019-3-31, bid at 22.52 to be $0.83 cheap. BAM.PF.G, resetting at +284bp 2020-6-30 is bid at 24.97 and appears to be $0.56 rich.

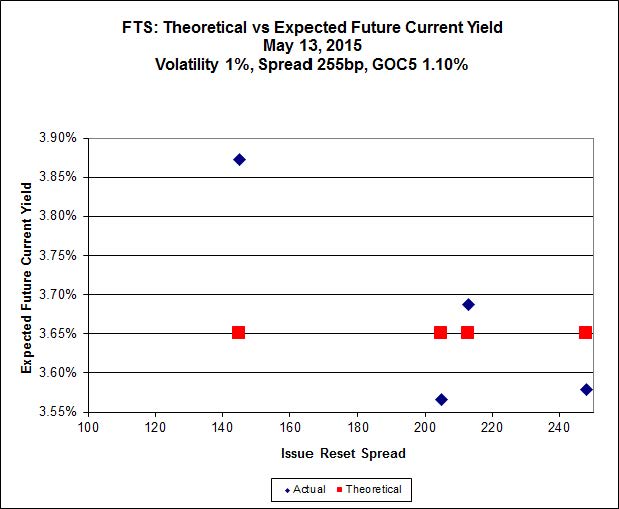

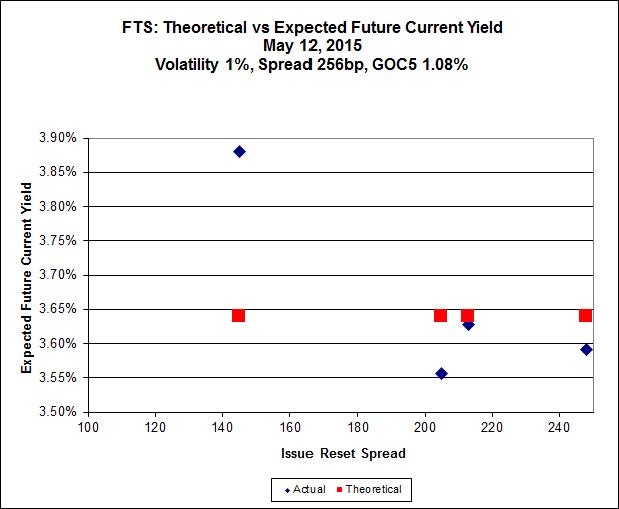

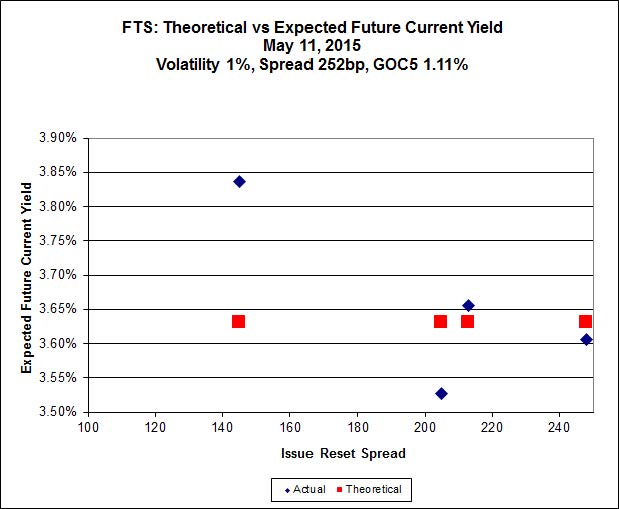

Click for Big

Click for BigFTS.PR.H, with a spread of +145bp, and bid at 16.46, looks $1.01 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 22.08 and is $0.50 rich.

Click for Big

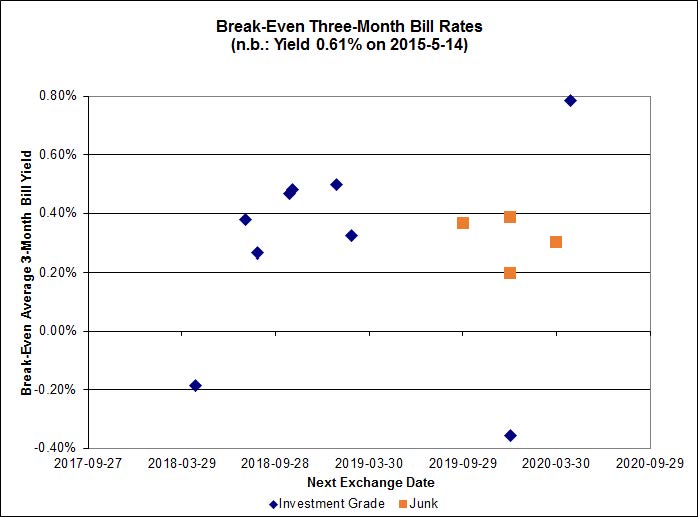

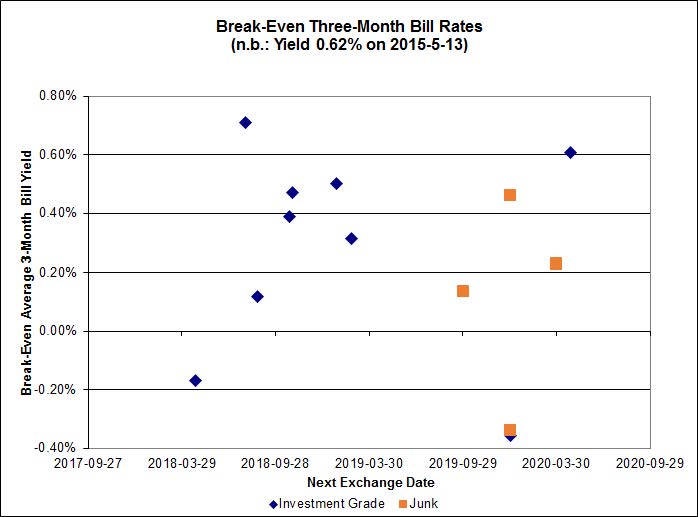

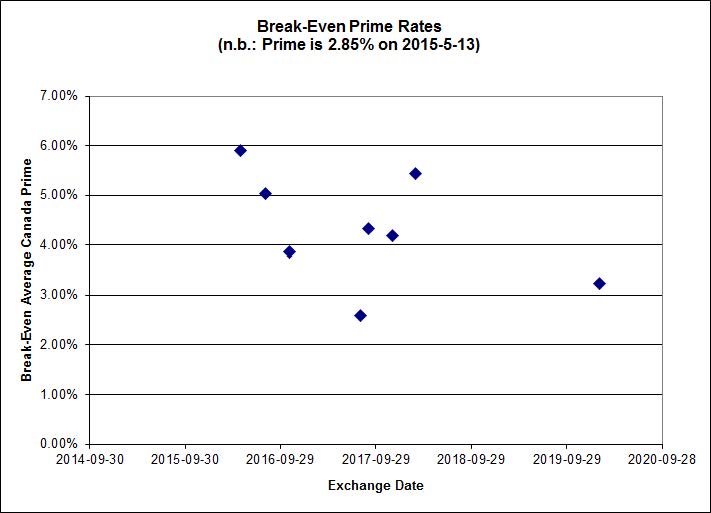

Click for BigInvestment-grade pairs predict an average over the next five-odd years of about 0.30%, including the TRP.PR.A / TRP.PR.F at -0.36%. On the junk side, the FFH.PR.E / FFH.PR.F pair is at -1.06%, while BRF.PR.A / BRF.PR.B is at -1.36%.

Click for Big

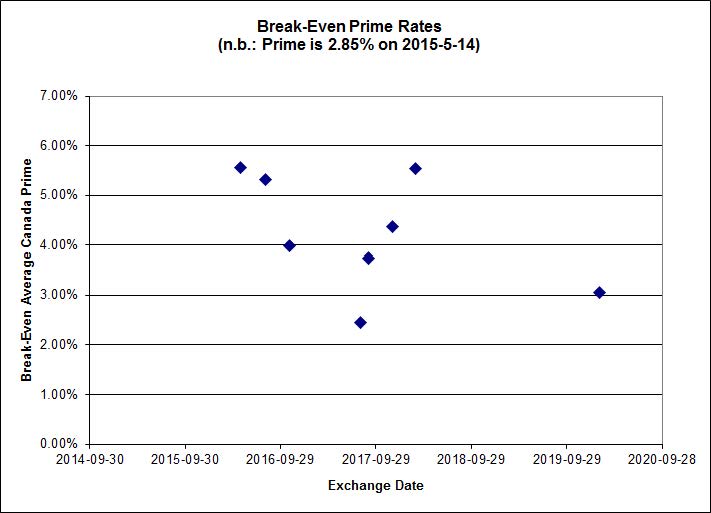

Click for BigShall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.4728 % |

2,298.2 |

| FixedFloater |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.4728 % |

4,018.3 |

| Floater |

3.16 % |

3.30 % |

54,370 |

18.96 |

4 |

-0.4728 % |

2,443.1 |

| OpRet |

4.41 % |

-4.13 % |

38,819 |

0.13 |

2 |

0.0980 % |

2,774.6 |

| SplitShare |

4.57 % |

4.81 % |

59,198 |

3.34 |

3 |

0.0802 % |

3,224.1 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0980 % |

2,537.1 |

| Perpetual-Premium |

5.46 % |

2.38 % |

63,834 |

0.08 |

18 |

0.0052 % |

2,521.3 |

| Perpetual-Discount |

5.04 % |

5.04 % |

121,767 |

15.29 |

15 |

0.2370 % |

2,788.9 |

| FixedReset |

4.39 % |

3.76 % |

272,135 |

16.42 |

86 |

-0.0255 % |

2,424.1 |

| Deemed-Retractible |

4.92 % |

3.24 % |

110,399 |

0.62 |

35 |

-0.0696 % |

2,643.6 |

| FloatingReset |

2.58 % |

2.92 % |

61,974 |

6.18 |

7 |

-0.0729 % |

2,336.4 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| ENB.PR.N |

FixedReset |

-2.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 20.35

Evaluated at bid price : 20.35

Bid-YTW : 4.59 % |

| ENB.PR.Y |

FixedReset |

-1.81 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 19.25

Evaluated at bid price : 19.25

Bid-YTW : 4.59 % |

| HSE.PR.A |

FixedReset |

-1.80 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 17.48

Evaluated at bid price : 17.48

Bid-YTW : 4.07 % |

| ENB.PR.P |

FixedReset |

-1.65 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 20.01

Evaluated at bid price : 20.01

Bid-YTW : 4.52 % |

| ENB.PR.F |

FixedReset |

-1.54 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 19.55

Evaluated at bid price : 19.55

Bid-YTW : 4.61 % |

| TRP.PR.D |

FixedReset |

-1.43 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 22.62

Evaluated at bid price : 23.51

Bid-YTW : 3.68 % |

| ENB.PR.D |

FixedReset |

-1.35 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 19.50

Evaluated at bid price : 19.50

Bid-YTW : 4.46 % |

| ENB.PR.T |

FixedReset |

-1.34 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 19.68

Evaluated at bid price : 19.68

Bid-YTW : 4.60 % |

| ENB.PR.B |

FixedReset |

-1.10 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 19.45

Evaluated at bid price : 19.45

Bid-YTW : 4.47 % |

| ELF.PR.H |

Perpetual-Premium |

-1.10 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 24.72

Evaluated at bid price : 25.20

Bid-YTW : 5.49 % |

| ELF.PR.G |

Perpetual-Discount |

-1.06 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 23.11

Evaluated at bid price : 23.40

Bid-YTW : 5.11 % |

| ENB.PR.A |

Perpetual-Premium |

1.04 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2015-06-12

Maturity Price : 25.00

Evaluated at bid price : 25.35

Bid-YTW : -14.37 % |

| RY.PR.Z |

FixedReset |

1.06 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 23.15

Evaluated at bid price : 24.72

Bid-YTW : 3.29 % |

| SLF.PR.H |

FixedReset |

1.15 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.95

Bid-YTW : 4.96 % |

| CM.PR.P |

FixedReset |

1.16 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 23.00

Evaluated at bid price : 24.50

Bid-YTW : 3.34 % |

| CU.PR.D |

Perpetual-Discount |

1.23 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2020-09-01

Maturity Price : 25.25

Evaluated at bid price : 25.50

Bid-YTW : 4.61 % |

| CIU.PR.C |

FixedReset |

1.25 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 16.20

Evaluated at bid price : 16.20

Bid-YTW : 3.76 % |

| PWF.PR.S |

Perpetual-Discount |

1.77 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 24.33

Evaluated at bid price : 24.75

Bid-YTW : 4.86 % |

| MFC.PR.M |

FixedReset |

2.74 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.75

Bid-YTW : 3.85 % |

| MFC.PR.L |

FixedReset |

3.65 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.59

Bid-YTW : 4.31 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| ENB.PR.H |

FixedReset |

121,407 |

Nesbitt crossed 100,000 at 18.60.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 18.37

Evaluated at bid price : 18.37

Bid-YTW : 4.47 % |

| MFC.PR.A |

OpRet |

89,420 |

Called for redemption June 19.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2015-06-19

Maturity Price : 25.00

Evaluated at bid price : 25.25

Bid-YTW : 0.32 % |

| BAM.PF.G |

FixedReset |

44,659 |

Desjardins crossed 40,000 at 24.85.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 23.14

Evaluated at bid price : 24.97

Bid-YTW : 3.94 % |

| SLF.PR.H |

FixedReset |

41,221 |

Nesbitt crossed 38,300 at 21.90.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.95

Bid-YTW : 4.96 % |

| ENB.PR.P |

FixedReset |

27,576 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 20.01

Evaluated at bid price : 20.01

Bid-YTW : 4.52 % |

| RY.PR.H |

FixedReset |

24,106 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 23.07

Evaluated at bid price : 24.59

Bid-YTW : 3.34 % |

| There were 29 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| MFC.PR.K |

FixedReset |

Quote: 23.82 – 24.50

Spot Rate : 0.6800

Average : 0.4164

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.82

Bid-YTW : 4.12 % |

| ELF.PR.H |

Perpetual-Premium |

Quote: 25.20 – 25.65

Spot Rate : 0.4500

Average : 0.3273

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 24.72

Evaluated at bid price : 25.20

Bid-YTW : 5.49 % |

| ENB.PR.N |

FixedReset |

Quote: 20.35 – 20.73

Spot Rate : 0.3800

Average : 0.2644

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 20.35

Evaluated at bid price : 20.35

Bid-YTW : 4.59 % |

| ENB.PR.F |

FixedReset |

Quote: 19.55 – 19.87

Spot Rate : 0.3200

Average : 0.2273

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-05-13

Maturity Price : 19.55

Evaluated at bid price : 19.55

Bid-YTW : 4.61 % |

| MFC.PR.I |

FixedReset |

Quote: 25.48 – 25.73

Spot Rate : 0.2500

Average : 0.1654

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2017-09-19

Maturity Price : 25.00

Evaluated at bid price : 25.48

Bid-YTW : 3.85 % |

| IFC.PR.A |

FixedReset |

Quote: 20.78 – 21.15

Spot Rate : 0.3700

Average : 0.2903

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.78

Bid-YTW : 5.53 % |