Interesting article in the WSJ regarding the changing life insurance business:

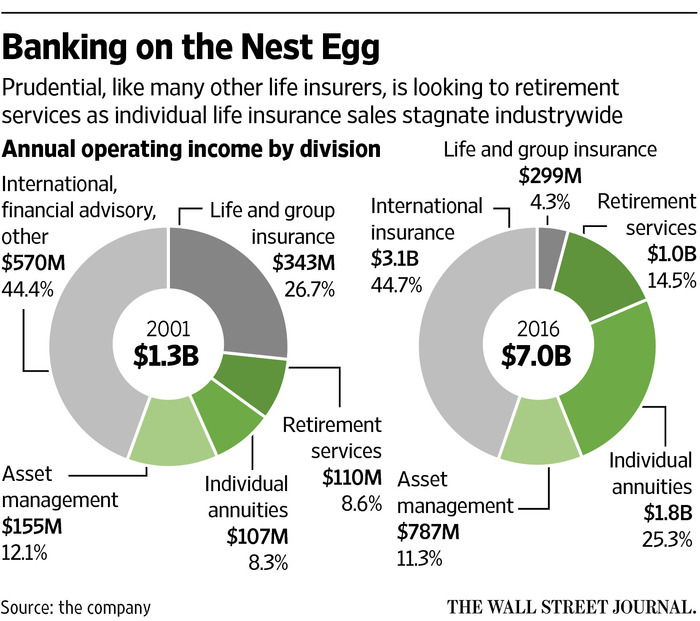

Prudential Financial Inc. is about to become the largest life insurance company in America by assets. But U.S. life insurance sales aren’t the biggest source of its profits.

Today, many Americans say they fear outliving their savings more than the premature death of a major breadwinner. And industry sales of individual life-insurance policies are down sharply since the mid-1980s. As a result, Prudential has transformed itself into an investing giant focused heavily on retirement-related products and services.

…

Up next, PGIM is making its first foray into ETFs, according to people familiar with the matter. The firm aims to start with two types of ETFs: actively managed fixed-income products, and so-called smart beta equity ETFs, which track the performance of non-market-capitalization-weighted indexes, these people said.

…

The industry shift away from life insurance is in part the result of the proliferation of mutual funds in the 1980s, which opened the door to stock-market investing by middle-income households through tax-advantaged savings plans. Before then “whole life insurance,” combining a death benefit with a tax-advantaged savings account, was a common way to save.

Basic term-life policies picked up some of the slack as savings plans proliferated. But many agents quit the business because commissions were relatively small, further depressing sales.

Click for Big

Click for BigAnd there are housing woes even outside Canada:

In places such as New York and San Francisco, which offer the greatest array of high-paying jobs, rents and home prices have shot up beyond the reach of many young workers. The squeeze has even affected the Bay Area’s amply compensated technology workers, whose salaries often aren’t enough to offset the rapidly rising rents and housing costs.

Technology workers who own a home in Seattle, by contrast, can expect to have about $2,000 more of disposable income left over each month after paying housing costs and taxes than those who live in San Francisco, according to a new analysis by Zillow and LinkedIn Corp. released Thursday.

Seattle tech workers who own their homes keep an average of 59% of their incomes after housing and tax costs, while Bay Area tech workers pocket just 37%, according to the study. In Austin, workers hold on to 54% of their incomes if they rent and 62% if they own.

But Ontario is mulling the destruction of the condominium business, given the success of rent control in destroying the apartment market:

Ontario is developing “substantive rent control reform,” the housing minister said Thursday, as the provincial NDP push for tenants in newer units to have the same protections as all other renters.

Currently, annual rent increase caps only apply to residential buildings or units constructed before November 1991. This year the rent for those tenants could be increased by up to 1.5 per cent without the landlord applying to the Landlord and Tenant Board.

…

Ontario Housing Minister Chris Ballard said it’s “unacceptable” that many Ontarians are seeing dramatically increasing housing costs.

“My staff are already developing a plan to address unfair rises in rental costs by delivering substantive rent control reform in Ontario as part of an ongoing review of the Residential Tenancies Act,” Ballard said in a statement.

“In the days ahead, we’ll share more details about a transformative plan that will allow Ontarians, no matter their budget or community, to realize their dream of having an affordable place to call home.”

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-1.4422 % |

2,117.8 |

| FixedFloater |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-1.4422 % |

3,886.1 |

| Floater |

3.59 % |

3.74 % |

51,931 |

17.99 |

4 |

-1.4422 % |

2,239.6 |

| OpRet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0065 % |

3,019.9 |

| SplitShare |

4.93 % |

3.91 % |

63,810 |

0.72 |

6 |

0.0065 % |

3,606.4 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0065 % |

2,813.9 |

| Perpetual-Premium |

5.35 % |

2.17 % |

69,733 |

0.09 |

20 |

-0.0234 % |

2,743.4 |

| Perpetual-Discount |

5.16 % |

5.20 % |

95,992 |

15.10 |

16 |

0.0397 % |

2,924.4 |

| FixedReset |

4.40 % |

4.15 % |

250,897 |

6.70 |

94 |

-0.0794 % |

2,347.8 |

| Deemed-Retractible |

5.04 % |

2.55 % |

141,569 |

0.19 |

31 |

0.0317 % |

2,860.2 |

| FloatingReset |

2.47 % |

3.20 % |

48,859 |

4.60 |

9 |

0.2968 % |

2,501.3 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| TRP.PR.B |

FixedReset |

-2.16 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2047-03-16

Maturity Price : 14.51

Evaluated at bid price : 14.51

Bid-YTW : 4.29 % |

| BAM.PR.B |

Floater |

-2.02 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2047-03-16

Maturity Price : 12.60

Evaluated at bid price : 12.60

Bid-YTW : 3.74 % |

| BAM.PR.K |

Floater |

-1.95 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2047-03-16

Maturity Price : 12.60

Evaluated at bid price : 12.60

Bid-YTW : 3.74 % |

| TRP.PR.C |

FixedReset |

-1.94 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2047-03-16

Maturity Price : 15.70

Evaluated at bid price : 15.70

Bid-YTW : 4.35 % |

| BAM.PR.C |

Floater |

-1.26 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2047-03-16

Maturity Price : 12.52

Evaluated at bid price : 12.52

Bid-YTW : 3.77 % |

| PWF.PR.T |

FixedReset |

-1.24 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2047-03-16

Maturity Price : 22.66

Evaluated at bid price : 23.01

Bid-YTW : 4.04 % |

| IFC.PR.A |

FixedReset |

-1.24 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.05

Bid-YTW : 7.10 % |

| SLF.PR.J |

FloatingReset |

1.21 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 15.89

Bid-YTW : 8.28 % |

| MFC.PR.R |

FixedReset |

1.41 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2022-03-19

Maturity Price : 25.00

Evaluated at bid price : 25.96

Bid-YTW : 4.01 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| BMO.PR.C |

FixedReset |

371,771 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2022-05-25

Maturity Price : 25.00

Evaluated at bid price : 25.29

Bid-YTW : 4.29 % |

| BNS.PR.H |

FixedReset |

197,496 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2022-01-26

Maturity Price : 25.00

Evaluated at bid price : 26.25

Bid-YTW : 3.88 % |

| MFC.PR.R |

FixedReset |

103,221 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2022-03-19

Maturity Price : 25.00

Evaluated at bid price : 25.96

Bid-YTW : 4.01 % |

| RY.PR.Q |

FixedReset |

90,309 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2021-05-24

Maturity Price : 25.00

Evaluated at bid price : 27.10

Bid-YTW : 3.43 % |

| BAM.PR.X |

FixedReset |

82,059 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2047-03-16

Maturity Price : 16.32

Evaluated at bid price : 16.32

Bid-YTW : 4.72 % |

| BIP.PR.D |

FixedReset |

82,040 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2022-03-31

Maturity Price : 25.00

Evaluated at bid price : 25.14

Bid-YTW : 4.85 % |

| There were 44 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| PWF.PR.O |

Perpetual-Premium |

Quote: 25.95 – 26.23

Spot Rate : 0.2800

Average : 0.1780

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2017-04-15

Maturity Price : 25.50

Evaluated at bid price : 25.95

Bid-YTW : -7.40 % |

| HSE.PR.A |

FixedReset |

Quote: 16.22 – 16.50

Spot Rate : 0.2800

Average : 0.1952

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2047-03-16

Maturity Price : 16.22

Evaluated at bid price : 16.22

Bid-YTW : 4.44 % |

| PWF.PR.T |

FixedReset |

Quote: 23.01 – 23.25

Spot Rate : 0.2400

Average : 0.1706

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2047-03-16

Maturity Price : 22.66

Evaluated at bid price : 23.01

Bid-YTW : 4.04 % |

| TRP.PR.B |

FixedReset |

Quote: 14.51 – 14.78

Spot Rate : 0.2700

Average : 0.2030

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2047-03-16

Maturity Price : 14.51

Evaluated at bid price : 14.51

Bid-YTW : 4.29 % |

| IAG.PR.G |

FixedReset |

Quote: 23.30 – 23.50

Spot Rate : 0.2000

Average : 0.1351

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.30

Bid-YTW : 5.18 % |

| IFC.PR.A |

FixedReset |

Quote: 19.05 – 19.30

Spot Rate : 0.2500

Average : 0.1867

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.05

Bid-YTW : 7.10 % |