Securities market participants will be gratified to learn that the tradition of administrative efficiency in Canadian securities regulation will be continued by the national securities regulator:

Canada’s new securities regulator is facing another delay on the bumpy road to its launch in 2015.

The group of participating provinces announced Friday that the regulations to outline the operating details of the new Cooperative Capital Markets Regulator will now be delayed until early spring and will not be out by Dec. 19, as previously anticipated.

Greek markets are beginning to resemble Canadian ones:

Greek stocks suffered their steepest daily fall in more than a quarter century on Tuesday and its bond yields jumped after Prime Minister Antonis Samaras brought forward a presidential election in a gamble over his, and the country’s future.

If Mr. Samaras fails to secure victory in parliament for his presidential candidate, snap national elections will be called that the leftist Syriza party – a fierce opponent of Greece’s bailout deal with the European Union and IMF – is likely to win.

…

The Athens general stock index tumbled 12.8 pe rcent, its biggest loss in a day since 1987. An index of Greece’s listed banks fell 14.7 per cent, with Attica Bank down 27.5 per cent.The decision sent 10-year Greek government bond yields up 74 basis points to 8.09 per cent.

Canadian preferred share investors are currently looking for indicators to guide them through current market turmoil:

The Canadian preferred share market took another good whacking today, with PerpetualDiscounts losing 41bp, FixedResets down 39bp and DeemedRetractibles off 20bp. The performance highlights table contains its usual lengthy list of FixedReset losers, but it is of interest to note that a large number of the credit-uncertain Enbridge issues were included. Volume was above average.

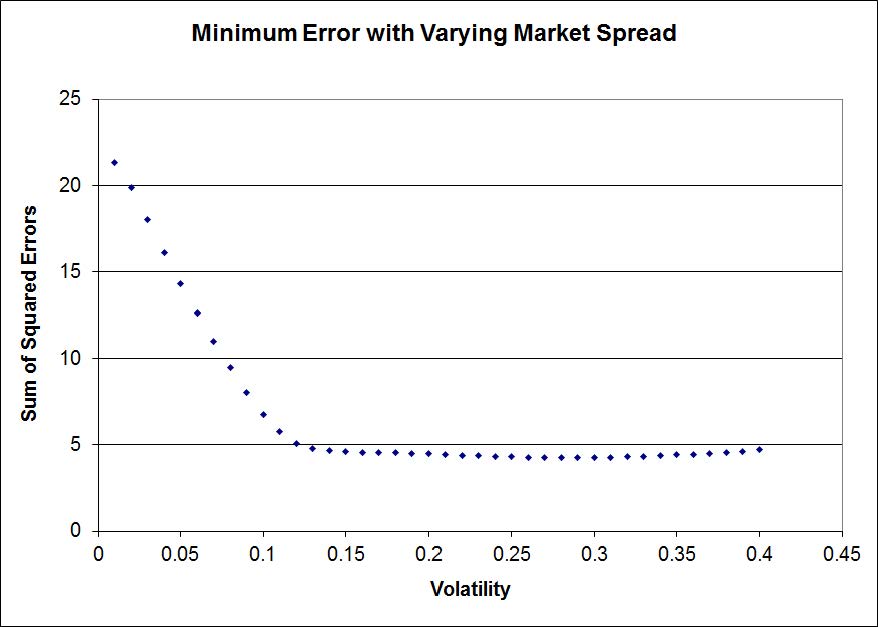

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

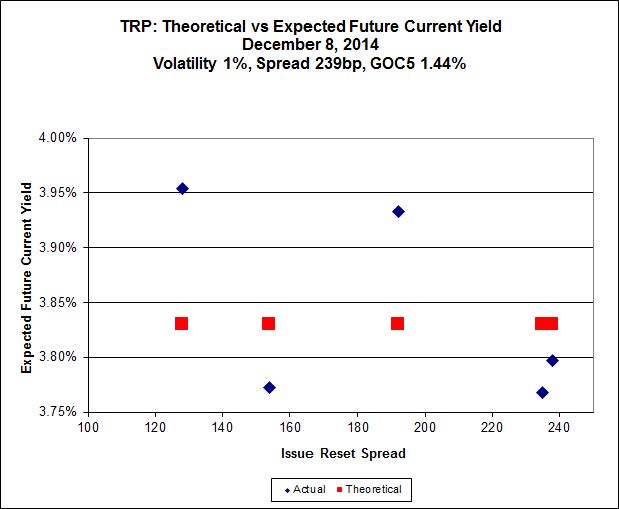

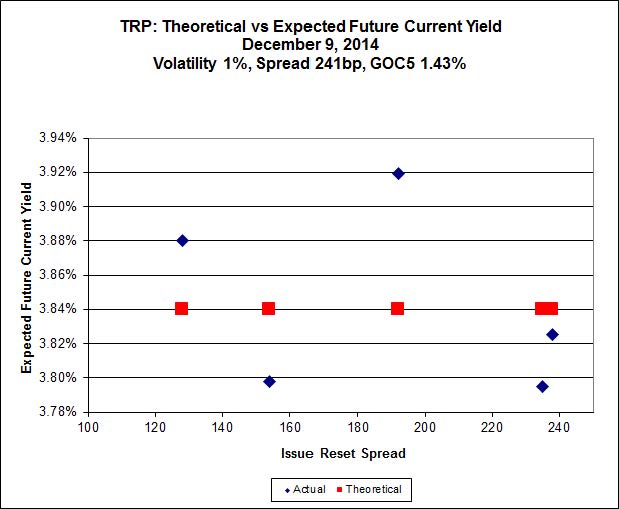

Here’s TRP:

Click for Big

So according to this, TRP.PR.A, bid at 21.37, is $0.44 cheap, but it has already reset. TRP.PR.B, bid at 17.46, is $0.18 cheap, but it resets 2015-6-30. TRP.PR.C, bid at 19.55, is $0.21 expensive, but it resets 2016-1-30. The TRP issues seem to be steadily rationalizing.

The MFC series is just weird.

Click for Big

Clearly MFC.PR.F, resetting at +141 on 2016-06-19, is out of step with the others and is screwing up the calculation. To the extent that one can trust both Implied Volatility Theory AND the market’s reasonably more-or-less consistent application of it, MFC.PR.F should be bid significantly higher than its current 20.00 and the calculated Implied Volatility should be higher than the distorted value of 28%. The fit is pretty poor – all one can really tell is that the Spread is more than about 80bp and the Implied Volatility is more than about 13%.

Click for Big

Click for Big

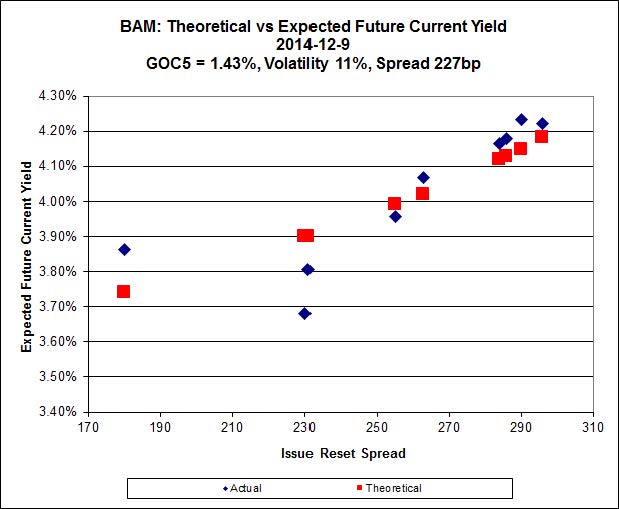

The BAM series is now also a little out of whack:

Click for Big

BAM.PR.X, with a +180bp spread, bid at 20.91, looks $0.68 cheap and doesn’t reset until 2017-6-30 – but Implied Volatility continues to drop rapidly (a reduction in Implied Volatility flattens the curve and causes low-spread issues to underperform). BAM.PR.R, with a +230bp spread, bid at 25.34, looks $1.43 rich and resets 2016-6-30. So go figure that one out, wise guy.

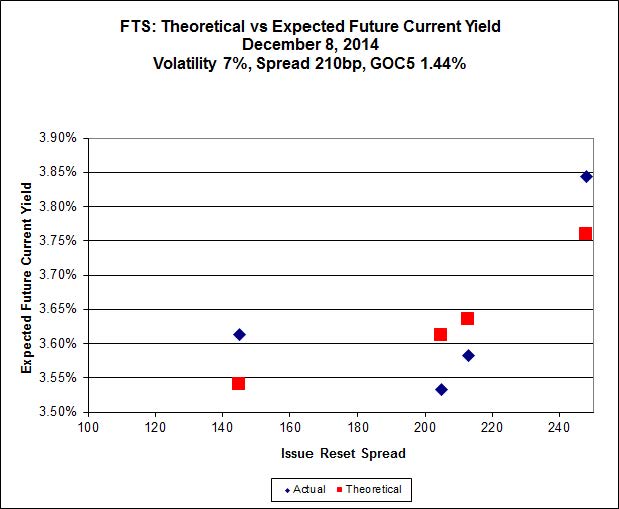

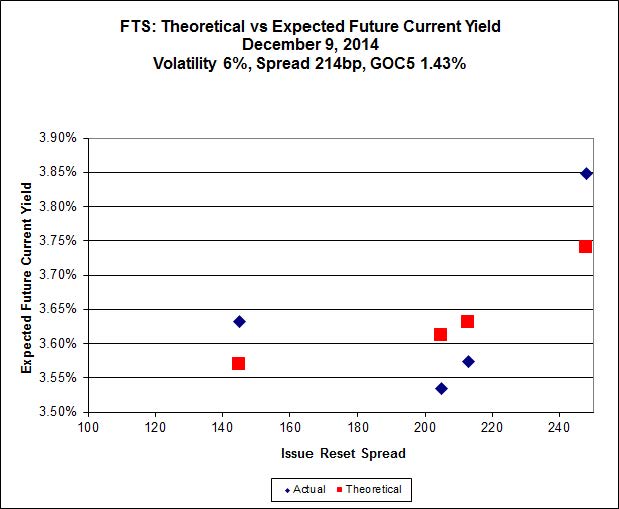

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 19.82, looks $0.35 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp, and bid at 24.62, looks $0.53 expensive and resets 2019-3-1

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2129 % | 2,523.2 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2129 % | 3,994.7 |

| Floater | 2.99 % | 3.11 % | 62,134 | 19.38 | 4 | -0.2129 % | 2,682.3 |

| OpRet | 4.41 % | -6.18 % | 28,767 | 0.08 | 2 | -0.2345 % | 2,752.0 |

| SplitShare | 4.29 % | 4.01 % | 39,096 | 3.73 | 5 | 0.0202 % | 3,178.5 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2345 % | 2,516.4 |

| Perpetual-Premium | 5.44 % | -1.52 % | 72,150 | 0.09 | 20 | 0.0196 % | 2,476.9 |

| Perpetual-Discount | 5.19 % | 5.12 % | 112,430 | 15.22 | 15 | -0.4110 % | 2,639.6 |

| FixedReset | 4.27 % | 3.74 % | 199,857 | 16.40 | 75 | -0.3933 % | 2,520.7 |

| Deemed-Retractible | 5.00 % | 1.77 % | 102,744 | 0.21 | 40 | -0.2029 % | 2,598.2 |

| FloatingReset | 2.54 % | 1.89 % | 60,996 | 3.47 | 5 | 0.0000 % | 2,550.6 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| MFC.PR.L | FixedReset | -3.99 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.06 Bid-YTW : 4.22 % |

| MFC.PR.F | FixedReset | -3.61 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.00 Bid-YTW : 5.72 % |

| ENB.PR.H | FixedReset | -3.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-09 Maturity Price : 20.68 Evaluated at bid price : 20.68 Bid-YTW : 4.45 % |

| ENB.PF.C | FixedReset | -2.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-09 Maturity Price : 22.73 Evaluated at bid price : 23.93 Bid-YTW : 4.31 % |

| ENB.PR.Y | FixedReset | -2.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-09 Maturity Price : 21.65 Evaluated at bid price : 22.00 Bid-YTW : 4.40 % |

| ENB.PF.G | FixedReset | -2.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-09 Maturity Price : 22.68 Evaluated at bid price : 23.86 Bid-YTW : 4.36 % |

| ENB.PF.A | FixedReset | -1.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-09 Maturity Price : 22.73 Evaluated at bid price : 23.90 Bid-YTW : 4.33 % |

| ENB.PF.E | FixedReset | -1.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-09 Maturity Price : 22.71 Evaluated at bid price : 23.90 Bid-YTW : 4.33 % |

| ENB.PR.F | FixedReset | -1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-09 Maturity Price : 22.53 Evaluated at bid price : 23.25 Bid-YTW : 4.24 % |

| ENB.PR.P | FixedReset | -1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-09 Maturity Price : 22.21 Evaluated at bid price : 22.80 Bid-YTW : 4.33 % |

| MFC.PR.B | Deemed-Retractible | -1.37 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.00 Bid-YTW : 5.72 % |

| CU.PR.C | FixedReset | -1.36 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-06-01 Maturity Price : 25.00 Evaluated at bid price : 25.30 Bid-YTW : 3.55 % |

| BAM.PR.R | FixedReset | -1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-09 Maturity Price : 23.83 Evaluated at bid price : 25.34 Bid-YTW : 3.79 % |

| CU.PR.D | Perpetual-Discount | -1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-09 Maturity Price : 23.61 Evaluated at bid price : 24.00 Bid-YTW : 5.12 % |

| GWO.PR.I | Deemed-Retractible | -1.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.69 Bid-YTW : 5.71 % |

| BAM.PR.X | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-09 Maturity Price : 20.91 Evaluated at bid price : 20.91 Bid-YTW : 4.18 % |

| TRP.PR.C | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-09 Maturity Price : 19.55 Evaluated at bid price : 19.55 Bid-YTW : 3.97 % |

| SLF.PR.B | Deemed-Retractible | -1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.92 Bid-YTW : 5.35 % |

| ENB.PR.J | FixedReset | -1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-09 Maturity Price : 22.71 Evaluated at bid price : 23.74 Bid-YTW : 4.28 % |

| ENB.PR.N | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-09 Maturity Price : 22.67 Evaluated at bid price : 23.60 Bid-YTW : 4.28 % |

| CU.PR.E | Perpetual-Discount | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-09 Maturity Price : 23.61 Evaluated at bid price : 24.00 Bid-YTW : 5.12 % |

| SLF.PR.D | Deemed-Retractible | -1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.60 Bid-YTW : 5.71 % |

| CGI.PR.D | SplitShare | 1.09 % | YTW SCENARIO Maturity Type : Soft Maturity Maturity Date : 2023-06-14 Maturity Price : 25.00 Evaluated at bid price : 25.09 Bid-YTW : 3.71 % |

| MFC.PR.M | FixedReset | 1.37 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2019-12-19 Maturity Price : 25.00 Evaluated at bid price : 25.15 Bid-YTW : 3.76 % |

| TRP.PR.B | FixedReset | 1.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-09 Maturity Price : 17.46 Evaluated at bid price : 17.46 Bid-YTW : 3.95 % |

| SLF.PR.G | FixedReset | 3.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.75 Bid-YTW : 5.66 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| HSE.PR.C | FixedReset | 619,946 | New issue settled today. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-09 Maturity Price : 23.16 Evaluated at bid price : 25.01 Bid-YTW : 4.46 % |

| BMO.PR.P | FixedReset | 133,054 | YTW SCENARIO Maturity Type : Call Maturity Date : 2015-02-25 Maturity Price : 25.00 Evaluated at bid price : 25.32 Bid-YTW : 0.37 % |

| IAG.PR.E | Deemed-Retractible | 125,050 | YTW SCENARIO Maturity Type : Call Maturity Date : 2015-01-30 Maturity Price : 26.00 Evaluated at bid price : 25.97 Bid-YTW : 4.17 % |

| TRP.PR.A | FixedReset | 113,648 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-09 Maturity Price : 21.37 Evaluated at bid price : 21.37 Bid-YTW : 3.95 % |

| ENB.PR.D | FixedReset | 83,910 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-09 Maturity Price : 22.41 Evaluated at bid price : 23.00 Bid-YTW : 4.17 % |

| TD.PF.B | FixedReset | 77,745 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-09 Maturity Price : 23.21 Evaluated at bid price : 25.07 Bid-YTW : 3.63 % |

| There were 39 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.L | FixedReset | Quote: 24.06 – 25.06 Spot Rate : 1.0000 Average : 0.5532 YTW SCENARIO |

| PVS.PR.C | SplitShare | Quote: 25.61 – 26.83 Spot Rate : 1.2200 Average : 0.8660 YTW SCENARIO |

| ELF.PR.H | Perpetual-Premium | Quote: 25.35 – 26.00 Spot Rate : 0.6500 Average : 0.4410 YTW SCENARIO |

| GWO.PR.N | FixedReset | Quote: 19.36 – 19.99 Spot Rate : 0.6300 Average : 0.4257 YTW SCENARIO |

| TRP.PR.C | FixedReset | Quote: 19.55 – 20.14 Spot Rate : 0.5900 Average : 0.4054 YTW SCENARIO |

| TRP.PR.D | FixedReset | Quote: 24.90 – 25.34 Spot Rate : 0.4400 Average : 0.2816 YTW SCENARIO |