SEC Commissioner Daniel M. Gallagher has updated his Crazy Quilt Chart of Regulation:

Click for Full Version

SEC Chair Mary Jo White touts efforts to open up the market to smaller IPOs … but instead of simplifying the rules, they’re trying to create a web of exceptions:

Indeed, more than 20 states have enacted some form of intrastate crowdfunding legislation or rules, and a number of others are considering similar initiatives. As states are seeking to expand the avenues in which issuers may conduct intrastate offerings, we have focused on the fact that some of our laws and rules were put into place years ago prior to widespread use of the internet and may present challenges to the states’ efforts.

For example, Securities Act Rule 147, which you will be discussing today, created a safe harbor that issuers often rely on for intrastate offerings. Rule 147 was adopted in 1974, and how an issuer might conduct an intrastate offering using the internet was not contemplated at that time. The staff in the Division of Corporation Finance is currently considering ways to improve the rule, by looking at, among other things, the conditions included in the rule for an offering to be considered intrastate. Securities Act Rule 504, an exemption that could be used to facilitate regional crowdfunding offerings for up to $1 million that are registered in one or more states, is another rule that may benefit from modernization and the staff is considering ways to do that. We look forward to having your input on these topics and to hearing your thoughts on whether there are aspects of these or other rules that could be usefully updated or changed.

The global bond rout is becoming a headline standard:

The global bond rout gathered pace, with Japanese notes slipping a fourth day after Mario Draghi forecast faster euro-area inflation and continued market volatility. Australia’s dollar dropped as most Asian shares rose and oil held losses.

Yields on 10-year Japanese government bonds climbed 3 basis points to 0.49 percent by 11:51 a.m. in Tokyo, the highest level since November, while Australian yields increased for a third day. The Aussie declined 0.8 percent after data showed the nation’s exports slid in April. A measure of Chinese shares in Hong Kong and Japanese stocks advanced while U.S. index futures fell 0.1 percent. U.S. oil held below $60 a barrel before Friday’s OPEC meeting.

This year’s gains in global bonds evaporated as the European Central Bank chief inflamed a selloff in German bunds, saying price growth in the region would pick up further. Greece’s premier claimed to be near agreement with creditors, adding there was no need to worry about an International Monetary Fund payment due Friday.

Meanwhile – and related to the discussion on liquidity, below – there are dark mutterings about taper tantrum redux:

Prices on U.S. investment-grade bonds have fallen 1.1 percent in the first two days of June, a pace so fast it’s reminiscent of the notes’ 5 percent selloff in two months in 2013 when speculation emerged that the Federal Reserve was poised to scale back its bond buying. Bank of America Corp. strategists see the pain deepening from here.

The reason? Investors who like these bonds tend to prize safety and reliable returns above all. They plowed into corporate bonds, often instead of more-creditworthy notes such as U.S. Treasuries, for higher yields as the Fed purchased debt and held interest rates at record lows to ignite growth.

These buyers, in particular, don’t like to see losses on their monthly mutual-fund statements. When the prospects for their debt look shaky, they’ve often responded by yanking their money. And that’s what they’ll likely do now, according to Bank of America analysts.

“We expect high-grade fund flows to turn generally negative in line with the initial experience during the Taper Tantrum,” Hans Mikkelsen, a strategist in New York, wrote in a June 2 report. “Corporate bond prices are declining at a pace eerily similar to what we saw” during that selloff of 2013.

That year, U.S. bond funds reported record withdrawals as investors girded for a period of steadily rising debt yields — or, in other words, losses. Investors pulled more than $70 billion from bond mutual funds in 2013, according to TrimTabs Investment Research.

Matt Levine is one of my favourite columnists, if for no other reason than disproving the idea that PrefBlog hates everybody. He’s written a great column on bond market liquidity:

People are worried about bond market liquidity, is the point I’m trying to make here.

Should they be? I don’t know. I don’t even entirely know what the question means; it is really an assortment of interrelated questions. (What even is the “bond market”? Corporates? Treasuries? Loan ETFs?) Still I figured I would make a series of disconnected observations here, since this stuff keeps coming up.

…

The risk, it seems to me, can’t be located in the dealers (i.e. the banks). Volcker, capital requirements, etc., drive up the cost of immediacy, but they don’t increase the risk of a crash, because bond dealers were never in the business of buying all the bonds all the way down. If there’s a bond crash, the banks won’t be buying bonds, but they would never have been buying bonds in a crash. That was never their job.

…

People are also really worried about liquidity in the Treasury market, in ways that seem to me to be mostly unrelated to the worries about the corporate market. One obvious thing here is: Treasuries look much more like stocks than corporates do. Treasuries trade a lot on electronic exchanges, and banks are relatively unimportant in intermediating Treasury trades. “For Treasuries, the share of transactions by primary dealers has dwindled by more than half to 4 percent since the end of 2008,” with electronic traders like Citadel expanding their role as dealers, and the complaints about the Treasury market sound a lot like the complaints in the equity markets about human market makers being replaced by algorithmic traders.

…

The worries about the Treasury market seem to be largely microstructural; Pimco uses words like “flash crashes” and “air pockets,” not “crises” or “crashes.” The latest Treasury-market news is from ICAP, which “is studying the possibility of temporarily halting Treasurys trading following large price moves,” a classic idea imported from the equity markets. The idea is that sometimes algorithms lose their cool, and rather than letting markets chase the algorithms all the way down, you turn off the whole market for five minutes until human investors can get to their desks and realize that Treasuries are going for bargain prices. People hate flash crashes, and obviously they cause some people to lose money, but they have always struck me as sort of non-systemic, a technical glitch rather than a major fear. A sharp permanent drop in asset prices is scary. A sharp temporary drop in asset prices is kind of funny, honestly.

His first point, distinguishing the role of dealers in terms of liquidity provision vs. crash prevention, echoes the point I made yesterday when I mocked Nouriel Roubini.

Bloomberg published another illustration of the shift in holdings:

Click For Big

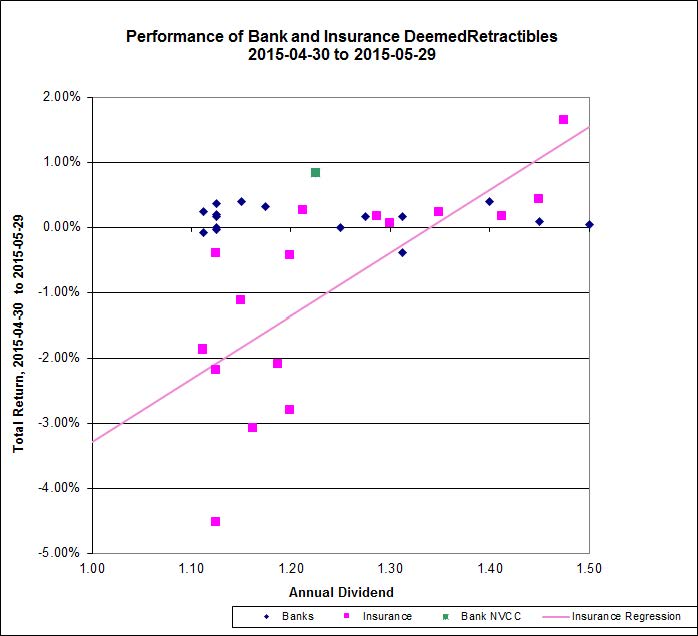

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts up 7bp, FixedResets off 24bp and DeemedRetractibles gaining 4bp. The Performance Highlights table is dominated by losing FixedResets. Volume was slightly below average.

PerpetualDiscounts now yield 5.07%, equivalent to 6.59% interest at the standard equivalency factor of 1.3x. Long corporates now yield about 4.05%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 255bp, a meaningful narrowing from the 265bp reported May 27.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

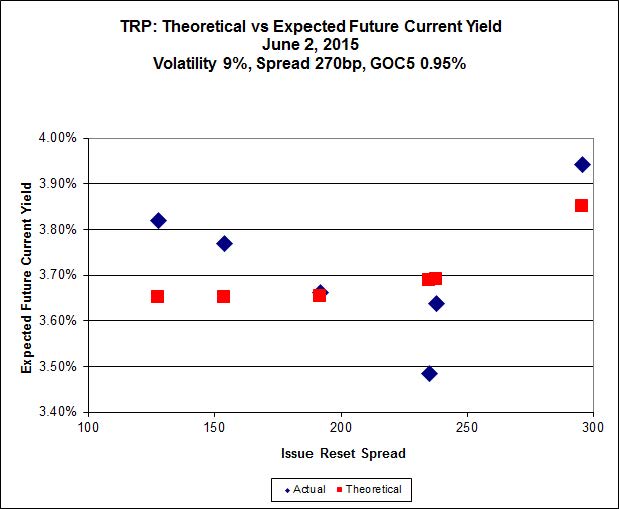

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 23.50 to be $1.23 rich, while TRP.PR.B, which will reset June 30 at 2.152% (GOC5 + 128bp), is $0.64 cheap at its bid price of 14.57.

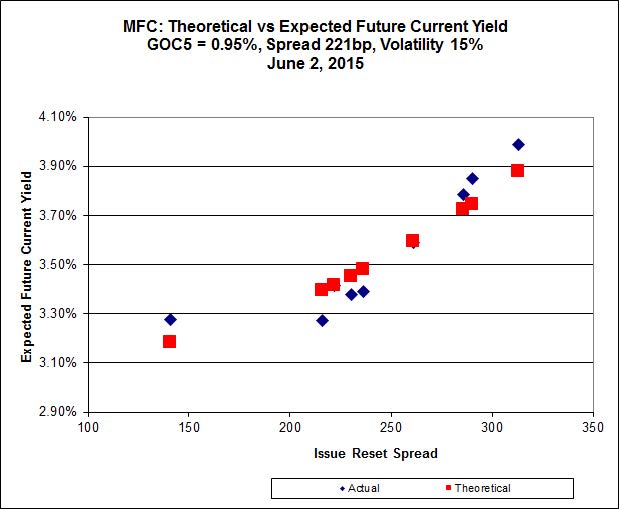

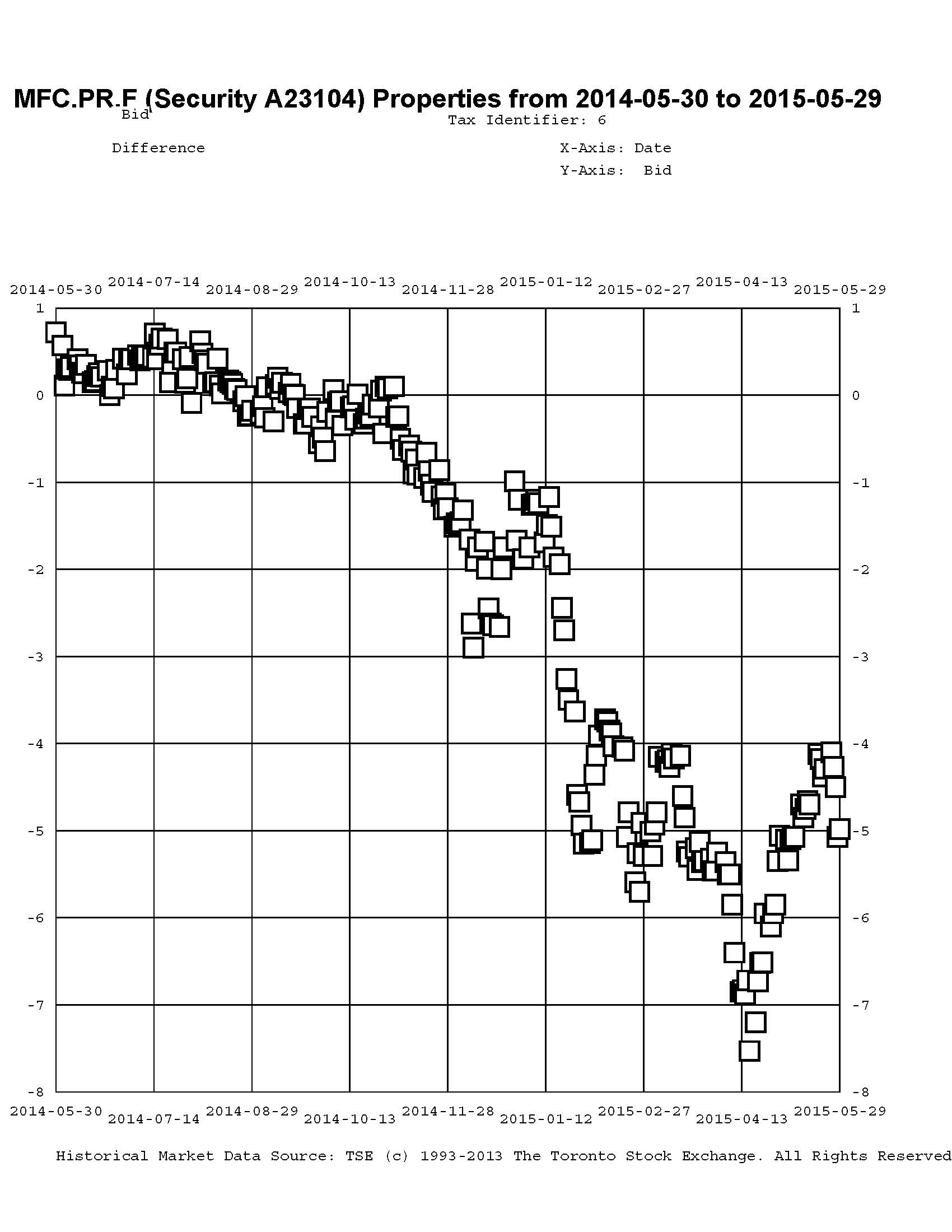

Click for Big

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule). It is clear that the lowest spread issue, MFC.PR.F, is well off the relationship defined by the other issues, but this doesn’t resolve the conundrum – it just makes it more conundrous.

Most expensive is MFC.PR.L, resetting at +216 on 2019-6-19, bid at 23.75 to be $0.88 rich, while MFC.PR.H, resetting at +313bp on 2017-3-19, is bid at 25.42 to be $0.85 cheap.

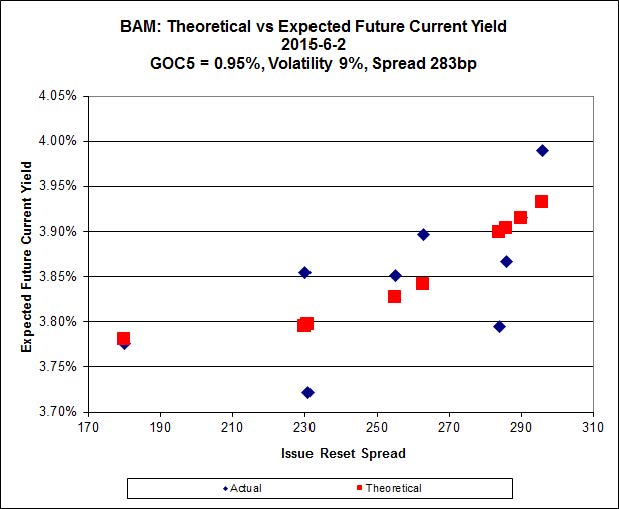

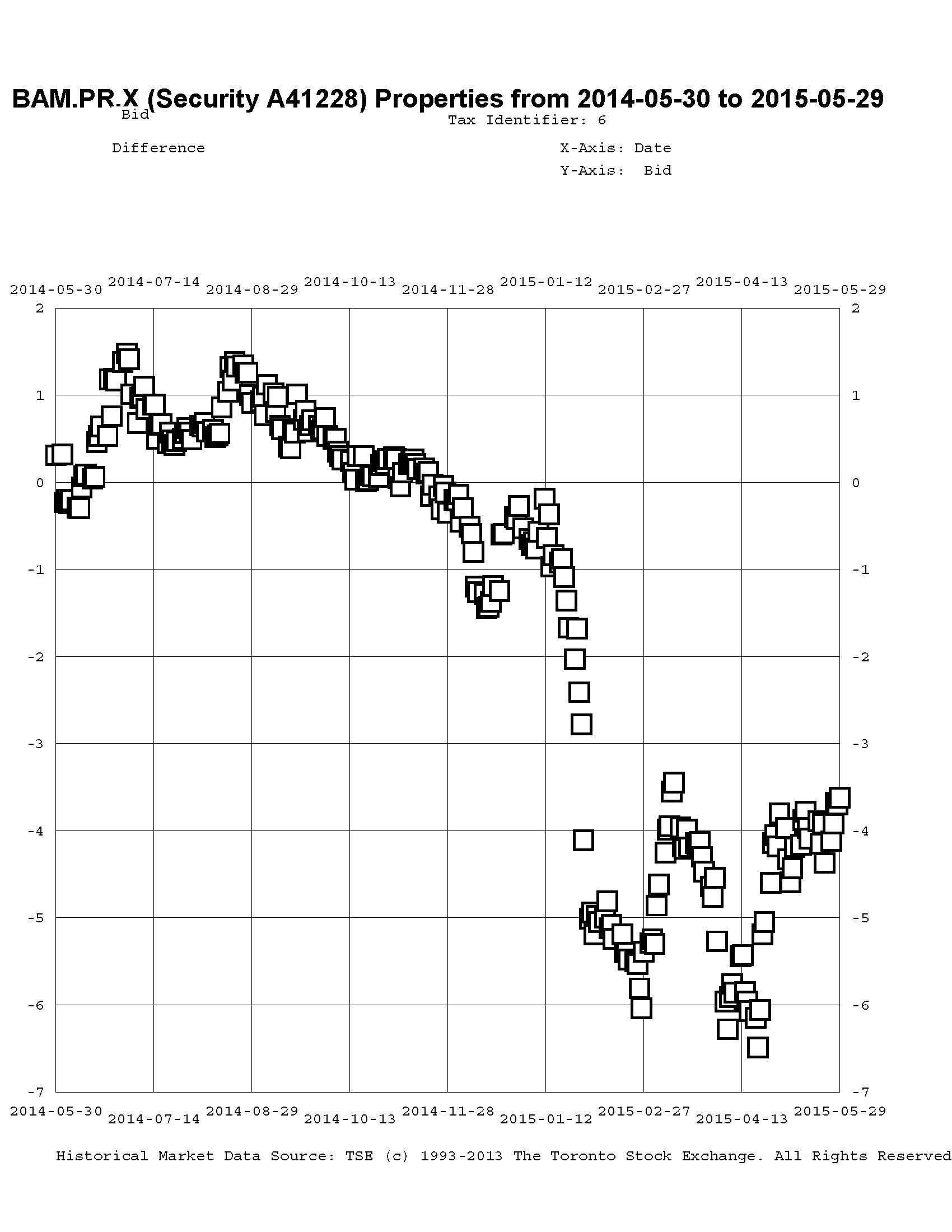

Click for Big

The cheapest issue relative to its peers is BAM.PR.Z, resetting at +296bp on 2017-12-31, bid at 24.50 to be $0.40 cheap. BAM.PF.G, resetting at +284bp 2020-6-30 is bid at 24.91 and appears to be $0.59 rich.

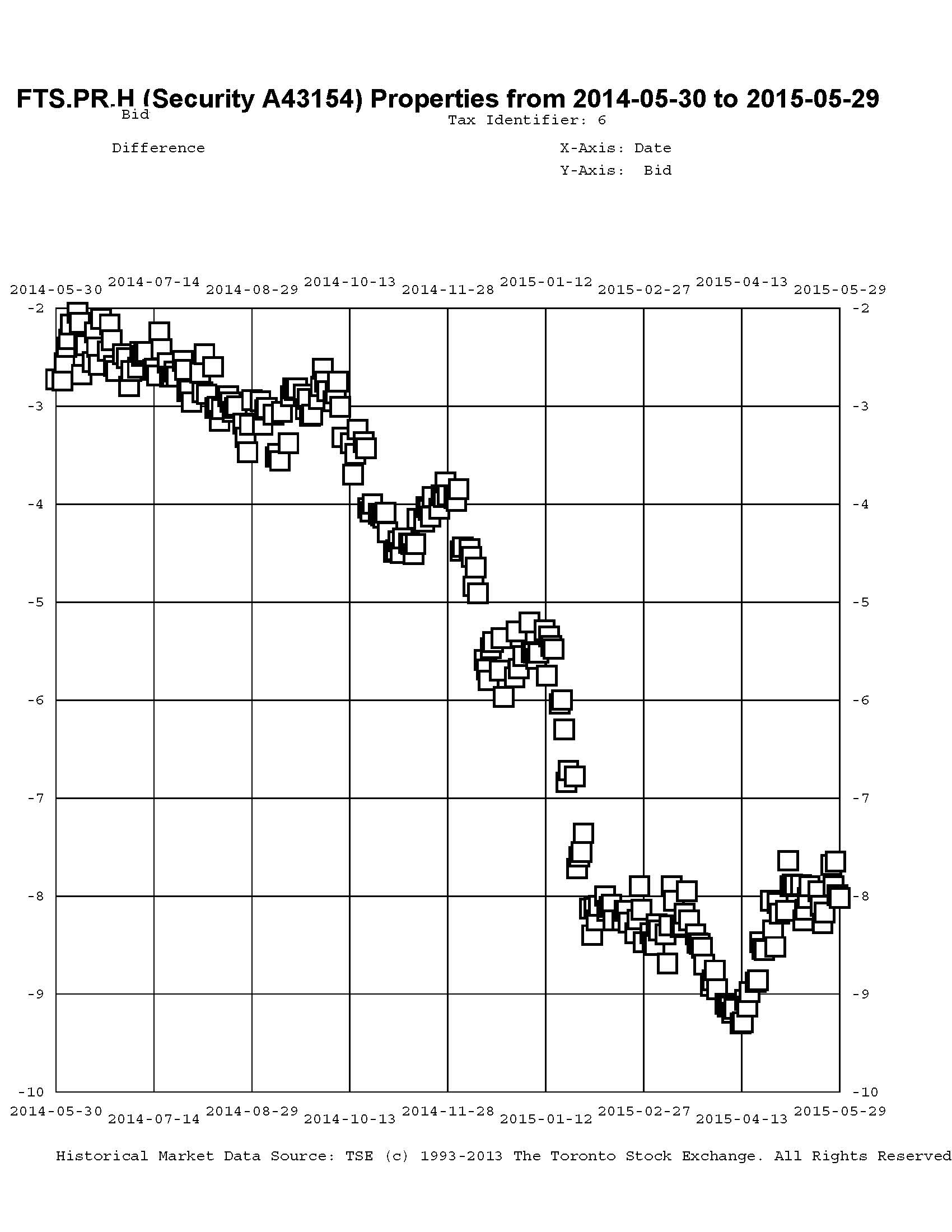

Click for Big

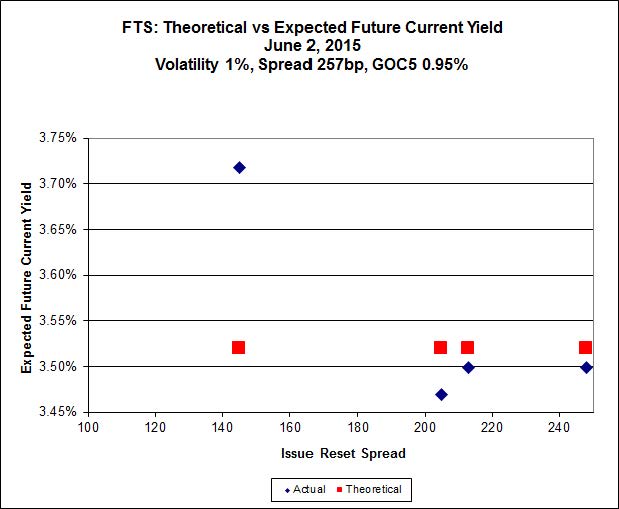

FTS.PR.H, with a spread of +145bp, and bid at 16.10, looks $0.89 cheap and resets 2020-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 21.62 and is $0.45 rich.

Click for Big

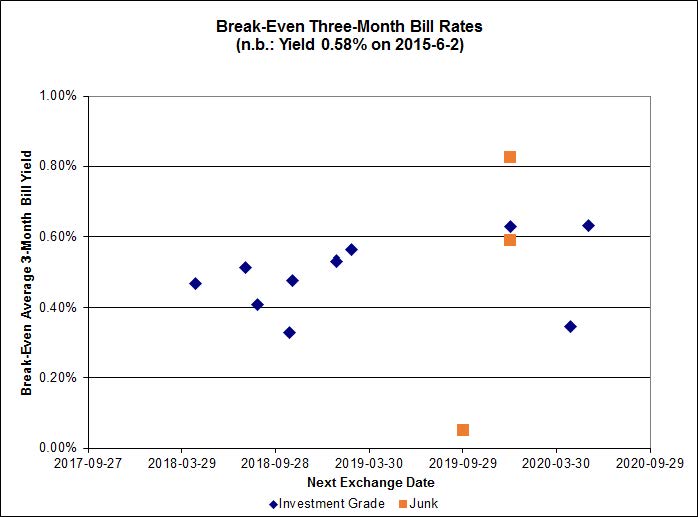

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of about 0.65%, including TRP.PR.A / TRP.PR.F at 1.12% and FTS.PR.H / FTS.PR.I at 1.43%. On the junk side, four pairs are outside the range of the graph: FFH.PR.E / FFH.PR.F at -1.01%; AIM.PR.A / AIM.PR.B at -1.38%; BRF.PR.A / BRF.PR.B at -1.26%; and DC.PR.B / DC.PR.D at -1.75%.

Click for Big

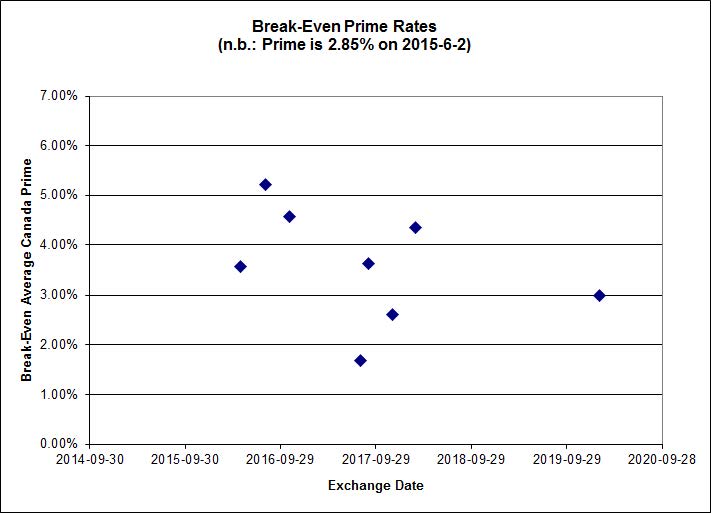

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.9476 % | 2,185.6 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.9476 % | 3,821.5 |

| Floater | 3.51 % | 3.55 % | 61,508 | 18.34 | 3 | 0.9476 % | 2,323.5 |

| OpRet | 4.44 % | -13.94 % | 27,689 | 0.09 | 2 | 0.0000 % | 2,782.9 |

| SplitShare | 4.57 % | 4.36 % | 72,102 | 3.32 | 3 | 0.6847 % | 3,264.5 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 2,544.7 |

| Perpetual-Premium | 5.45 % | 4.72 % | 64,310 | 1.50 | 19 | 0.0538 % | 2,518.5 |

| Perpetual-Discount | 5.07 % | 5.07 % | 116,220 | 15.37 | 14 | 0.0694 % | 2,773.0 |

| FixedReset | 4.46 % | 3.75 % | 257,019 | 16.63 | 86 | -0.2377 % | 2,379.3 |

| Deemed-Retractible | 4.98 % | 3.30 % | 110,465 | 0.71 | 34 | 0.0404 % | 2,634.5 |

| FloatingReset | 2.48 % | 2.89 % | 54,135 | 6.15 | 9 | 0.4976 % | 2,343.9 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| CIU.PR.C | FixedReset | -3.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-03 Maturity Price : 15.75 Evaluated at bid price : 15.75 Bid-YTW : 3.72 % |

| TD.PF.B | FixedReset | -2.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-03 Maturity Price : 22.52 Evaluated at bid price : 23.35 Bid-YTW : 3.51 % |

| FTS.PR.M | FixedReset | -2.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-03 Maturity Price : 22.81 Evaluated at bid price : 24.00 Bid-YTW : 3.61 % |

| GWO.PR.N | FixedReset | -1.72 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.10 Bid-YTW : 6.84 % |

| TD.PF.C | FixedReset | -1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-03 Maturity Price : 22.37 Evaluated at bid price : 23.14 Bid-YTW : 3.54 % |

| VNR.PR.A | FixedReset | -1.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-03 Maturity Price : 22.95 Evaluated at bid price : 23.74 Bid-YTW : 3.99 % |

| TRP.PR.A | FixedReset | -1.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-03 Maturity Price : 19.30 Evaluated at bid price : 19.30 Bid-YTW : 3.80 % |

| GWO.PR.P | Deemed-Retractible | -1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.45 Bid-YTW : 5.14 % |

| TD.PF.A | FixedReset | -1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-03 Maturity Price : 22.60 Evaluated at bid price : 23.53 Bid-YTW : 3.48 % |

| ENB.PR.B | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-03 Maturity Price : 18.56 Evaluated at bid price : 18.56 Bid-YTW : 4.58 % |

| HSE.PR.A | FixedReset | 1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-03 Maturity Price : 16.64 Evaluated at bid price : 16.64 Bid-YTW : 4.09 % |

| BAM.PR.N | Perpetual-Discount | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-03 Maturity Price : 22.13 Evaluated at bid price : 22.54 Bid-YTW : 5.34 % |

| PVS.PR.D | SplitShare | 1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2021-10-08 Maturity Price : 25.00 Evaluated at bid price : 24.60 Bid-YTW : 4.81 % |

| BAM.PF.D | Perpetual-Discount | 2.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-03 Maturity Price : 23.12 Evaluated at bid price : 23.44 Bid-YTW : 5.30 % |

| BAM.PR.K | Floater | 2.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-03 Maturity Price : 14.20 Evaluated at bid price : 14.20 Bid-YTW : 3.55 % |

| FTS.PR.I | FloatingReset | 5.10 % | There was real trading today, with 4,636 shares changing hands, as opposed to yesterday’s quote, which was just a reasonable guess. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-03 Maturity Price : 16.50 Evaluated at bid price : 16.50 Bid-YTW : 3.09 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| ENB.PR.B | FixedReset | 227,636 | Scotia crossed 205,700 at 18.50. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-03 Maturity Price : 18.56 Evaluated at bid price : 18.56 Bid-YTW : 4.58 % |

| CM.PR.Q | FixedReset | 87,491 | RBC crossed two blocks of 40,000 each, both at 24.91. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-03 Maturity Price : 23.08 Evaluated at bid price : 24.80 Bid-YTW : 3.64 % |

| BMO.PR.Q | FixedReset | 62,859 | TD Crossed blocks of 22,600 and 30,000, both at 23.50. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.50 Bid-YTW : 3.44 % |

| BNS.PR.M | Deemed-Retractible | 55,025 | Nesbitt crossed 15,000 at 25.45; TD crossed 31,300 at the same price. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-07-27 Maturity Price : 25.25 Evaluated at bid price : 25.45 Bid-YTW : 1.89 % |

| TRP.PR.B | FixedReset | 50,563 | Desjardins crossed 35,000 at 14.60. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-03 Maturity Price : 14.57 Evaluated at bid price : 14.57 Bid-YTW : 3.77 % |

| ENB.PR.Y | FixedReset | 46,616 | Scotia crossed 40,000 at 18.55. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-03 Maturity Price : 18.53 Evaluated at bid price : 18.53 Bid-YTW : 4.68 % |

| There were 28 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| FTS.PR.M | FixedReset | Quote: 24.00 – 24.74 Spot Rate : 0.7400 Average : 0.4625 YTW SCENARIO |

| CIU.PR.C | FixedReset | Quote: 15.75 – 16.40 Spot Rate : 0.6500 Average : 0.4967 YTW SCENARIO |

| ENB.PR.B | FixedReset | Quote: 18.56 – 18.99 Spot Rate : 0.4300 Average : 0.2971 YTW SCENARIO |

| RY.PR.M | FixedReset | Quote: 24.37 – 24.74 Spot Rate : 0.3700 Average : 0.2544 YTW SCENARIO |

| MFC.PR.K | FixedReset | Quote: 23.32 – 23.74 Spot Rate : 0.4200 Average : 0.3070 YTW SCENARIO |

| RY.PR.K | FloatingReset | Quote: 24.31 – 24.61 Spot Rate : 0.3000 Average : 0.2041 YTW SCENARIO |