Here’s a story that brings together two themes frequently highlighted on PrefBlog – the difficulty of pricing corporate bonds and the incompetence of traders as investors:

Canada’s C$112 billion ($84 billion) Public Sector Pension Investment Board sued Saba in New York state court on Friday, saying the firm “artificially manipulated” the value of its investment by marking down a significant portion of the fund’s portfolio after the retirement plan asked for all its money back, only to boost the value of the assets the following month.

The lawsuit is another setback to Weinstein, 42, the former co-chief of Deutsche Bank AG’s credit business, who posted three straight years of losses before making 5.2 percent this year through August. Assets at New York-based Saba, which Weinstein started in 2009, have slumped more than two-thirds from a peak of $5.5 billion three years ago and some senior partners have left the firm.

…

The pension board, represented by law firm Skadden, Arps, Slate, Meagher & Flom LLP, said it asked Saba for its money back at the end of the first quarter after the fund couldn’t explain why it had suffered losses, and rejected a request to return its capital in three installments to keep other investors from finding out.

At the time, Saba held McClatchy Co. bonds that were hard to sell, according to the suit. The pension fund claimed that Saba changed the way it priced the debt before it returned the money. Normally, the hedge fund would use independent pricing services or brokers who regularly traded the bonds and had valued them at 50 cents to 60 cents on the dollar.

Instead, the retirement plan said Saba used a different process, which “purportedly produced materially depressed bids,” pricing the bonds at 31 cents as of March 31. Within a month, Saba returned to its usual pricing methodology and the bonds were marked in the 50s, the pension plan said.

Increasing the Fed Funds rate won’t be easy for the Fed:

In the past, the central bank kept the fed funds rate at or near the target chosen by policy makers by injecting or draining bank reserves from the system via the New York Fed’s trading desk. The amounts of cash involved were small and the Fed was pretty good at hitting its desired rate. Not anymore.

Three rounds of so-called quantitative easing from 2008 to 2014, in which the Fed bought bonds to support the economy, has swamped banks with cash — deposited with them by investors who sold bonds to the Fed. That added $2.6 trillion of reserves in excess of requirements to banks’ accounts held at the Fed. It also boosted the size of the Fed’s own balance sheet to $4.5 trillion, a five-fold increase from pre-crisis levels.

With so much cash and little need for banks to borrow in the fed funds market, the Fed has lost the ability to lift the funds rate in the way that it did before the crisis. It has also decided for now against selling the bonds back to investors, which would shrink its own balance sheet and extinguish the excess reserves.

…

Their main innovation, an overnight reverse repurchase agreement facility, is a powerful solution, but heavy usage may cause problems for banks trying to comply with new regulations installed in the wake of the financial crisis, said Zoltan Pozsar, director of U.S. economics at Credit Suisse Securities USA LLC in New York.

The facility promises to drain reserves from the banks by encouraging investors to withdraw the deposits created when they sold bonds to the Fed, and place the cash in money-market mutual funds.

Through overnight reverse repos, the Fed can borrow the cash from money funds at a specified rate and post securities as collateral, unwinding the trades the next day. In effect, the Fed will be borrowing back the money it created to buy the bonds while cutting out the middlemen in the banking system.

The problem: Banks aren’t sure exactly how much of their deposits they will cede to money-market funds once the Fed starts raising rates, or whose money or how fast. All of those things are important to understand for banks trying to stay in compliance with the liquidity coverage ratio, a major new pillar of global post-crisis banking regulation.

…

The liquidity rule requires banks to hold more cash and other “high-quality liquid assets” like Treasuries and government-backed mortgage bonds against their deposit base to protect themselves from runs. Because they can hold less cash against retail deposits than investor deposits, they will probably raise retail-deposit rates aggressively to hang on to these customers, according to [director of U.S. economics at Credit Suisse Securities USA LLC in New York Zoltan] Pozsar, who previously studied the plumbing of the post-crisis financial system in positions at the New York Fed and U.S. Treasury.

“They are going to fight for retail deposits like you’ve never seen them fight for retail deposits before,” Pozsar said. “That is going to be basically the defining feature of this hiking cycle.”

The upshot: Credit will become more expensive faster than in previous tightening cycles as banks pass higher deposit costs on to borrowers in an effort to maintain profitability.

In another article:

In a recent note, Credit Suisse analysts Zoltan Pozsar and James Sweeney highlight the potential impact on bank deposits and the potential for turbulence as the Fed approaches its “historic liftoff from the zero lower bound.” At issue are the non-operating accounts held by big institutional investors, which the analysts estimate equate to about 60 percent of the $1.1 trillion in deposits held by U.S. financial institutions.

For banks with lots of HQLA reserves and high-quality assets, the prospect of a bunch of hot money departing for the greener pastures of money market funds may not prove very worrisome. In fact, as deposits depart, such banks may find their balance sheets benefiting from a surplus of capital with which they can do all sorts of amusing things, such as buy back their stock and debt or (gasp!) raise deposit rates.

But for banks that haven’t loaded up on stickier funding or higher-quality assets to offset their non-operating deposits, well, things have the potential to become more interesting. As Pozsar and Sweeney put it: “A rising tide – rising interest rates – may not lift all boats as is typically the case during hiking cycles.”

…

Banks whose non-operating deposits eclipse their reserves do have a few levers they can pull to try to stem outflows, including paying depositors higher rates or lending out securities from their HQLA portfolios. But the point here should be clear. Two grand experiments, one conducted in the technical backwaters of monetary policy and the other operating in the realm of new banking rules, are about to collide.

So how to get new deposits? Here’s one way:

Since the 1950s, the U.K. has been issuing “premium bonds” that come with a chance to win a million-pound jackpot. An experiment at a South African bank 10 years ago boosted customers’ savings by 38 percent.

Now, D2D Fund, a nonprofit group focused on developing savings tools for low-income groups, has been pushing the idea in the U.S. It helped start “prize-linked savings” accounts at credit unions, which could take advantage of a loophole in federal law that allowed the contests. It also lobbied legislators to undo federal and state laws that banned cash giveaways by banks. President Barack Obama signed the American Savings Promotion Act on Dec. 18. A change in Virginia law took effect in July.

Brian Plum, Blue Ridge Bank’s 35-year-old president, was ready and waiting. He’d read about the concept last year and was eager to try it. He saw it as a way to help customers save more while also attracting new customers and new deposits to the $260-million asset bank.

Each month, the bank has a drawing with one $200 winner and four $50 winners. At the end of the year, it will give away a jackpot of $5,000. Customers get one drawing entry for every $25 increase in their account balance. To encourage savings, the bank allows only one withdrawal from a jackpot savings account per month, or else depositors pay a $5 withdrawal fee.

Another idea might be free toasters!

Bank of Montreal has released a report titled BMO Global Asset Management 2015 ETF Outlook, which is remarkable for its Panglossian insouciance regarding EFT liquidity:

Exchange traded funds have recently been in the news with questions about their liquidity. They have been called out as victims of their own success, growing rapidly and possibly outsizing less-liquid asset classes. The Volcker Rule, which restricts U.S. banks (and foreign banks operating in the United States) from engaging in certain types of speculative trading, may have caused fixed-income dealer trading inventory to drop. For asset classes like high yield bonds, this may mean less support from traditional sources like banks in the event of a liquidity crisis, leaving investors to wonder how an ETF will perform.

…

We believe all this attention is missing the point. Exchange traded funds are an access vehicle for an asset class – they provide additional benefits of liquidity, tradability, and diversification. This is particularly so for over-the-counter asset classes like bonds.

Investors looking for income, high returns, or portfolio benefits may decide high-yield bonds are appropriate. By trading an established ETF, the natural liquidity between buyers and sellers on the exchange may make the trade more efficient. If one investor is looking to buy and another is looking to sell, they can meet in the middle instead of each buying directly into the investment vehicle. Rather than sourcing bonds or buying into a fund with a daily opening, ETF investors can profit from intraday liquidity on the exchange and full transparency of trading costs through the market bid and ask prices. Importantly, ETFs are also backed by market makers who provide additional liquidity by holding and creating shares of the ETF. One-sided flows may affect the underlying asset classes in direct trading, but as market makers hedge their investment risk through the underlying holdings, the diversification across issues and issuers in ETFs reduces their impact.

As a test case of a market in crisis, we can look back to the high yield market in 2007. The liquidity crisis essentially froze trading in the underlying bonds. Meanwhile, as measured by SPDR Barclays High Yield Bond ETF (ticker JNK), ETFs continued to trade, acting as a price discovery vehicle for the asset class.

The ETF did trade at a significant discount of up to 8.7%, and later at a premium of up to 9.9%, which means the market price moved away from the net asset value (NAV). However, since the NAV was not reflecting actual bond trades, the ETF reflected the true value in the marketplace. Importantly, while trading spreads may have widened as a reflection of market uncertainty, investors that needed to buy or sell high yield bonds were able to do so via the ETF, rather than through the underlying portfolio.

The WSJ points out:

The downside: ETF investors can end up with a lower return than they expected if, for instance, they buy at a sizable premium to NAV but end up selling at a smaller one. This year, through June 30, JNK returned 6.1% based on its NAV but 5.8% based on its price, according to Morningstar. The gap is wider, 6.1% vs. 5.1%, for HYG.

… and as I noted on September 4:

So I’ll take solace in the growing recognition that circuit-breakers do not work as intended. Sadly, the response to ‘rules not working’ appears to be ‘more rules’:

When stocks were halted on Aug. 24, the result caused mayhem for many large ETFs because they became unmoored from their underlying share prices. The result was exaggerated swings in ETF prices, in excess of 40 per cent in some cases.

And, more seriously, Barclay’s musings reported on September 10, with the highlight:

The relationship between ETFs, funds and crisis liquidity has been a hot issue. Barclays weighs in with some musings on ‘first-mover’ advantage:

Illiquidity in corporate bonds would in theory spell bad news for bond funds that promise investors the ability to immediately get out of their positions. The concern here is that once investors get a whiff of an impending mass selloff in bonds, they could potentially rush for the exits to try to get ahead of it.

With liquidity already low, that could put massive pressure on debt prices. Those who manage to squeeze through the keyhole first get rewarded for their speed but end up exacerbating this downward spiral. The slowest investors, meanwhile, get left with a portfolio of bonds that’s potentially much reduced in price.

By how much, you ask? Barclays estimates about 2 percent for funds that hold junk-rated corporate debt (boldface ours):

…

It is disgraceful that BMO’s trained seals have not addressed these serious concerns forthrightly. But hey, this is Canada and the banks have a federally approved hegemony over the entire financial system, so suck it up.

Meanwhile, Silver Bullion Trust has released yet another vituperative letter to unitholders (emphasis from original):

As you may know, Sprott recently announced a fourth extension of their inadequate, hostile offer to acquire your Units. They have made no improvement to the terms of their offer, which is now set to expire on October 9, 2015. The reason for this latest extension is clear: despite bombarding Unitholders with a drawn out smear campaign against Silver Bullion Trust (“SBT”), its Trustees and its administrator, and despite paying brokers to convince their clients to tender, the vast majority of Unitholders have so far rejected Sprott’s offer. Sprott’s offer cannot succeed unless 662/3% of the Units are actually tendered, which has not been achieved.

Over the next few weeks, Sprott will undoubtedly continue to harass you and spread misinformation. Don’t be fooled, the facts haven’t changed: retaining your SBT Units remains a clearly superior alternative to Sprott’s inadequate offer, which is solely driven by their desperate desire to increase their assets under management and reverse the precipitous decline in their fee revenue, which has dropped by almost 40%1 since 2012.

There’s a new discussion paper out from the Bank of Canada, by Oleksiy Kryvtsov, Miguel Molico and Ben Tomlin titled On the Nexus of Monetary Policy and Financial Stability: Recent Developments and Research:

Because financial and macroeconomic conditions are tightly interconnected, financial stability considerations are an important element of any monetary policy framework. Yet, the circumstances under which it would be appropriate for the Bank to use monetary policy to lean against financial risks need to be more fully specified (Côté 2014). The extent to which financial stability concerns should be taken into account by monetary policy will be a priority topic of research at the Bank for the renewal of the inflation-control target agreement in 2016. This paper reviews four considerations of interest, taking stock of key domestic and international developments and knowledge gained over the past few years: (i) Canada and other countries have made significant progress in the implementation of micro- and macroprudential regulatory reforms, and limited existing research finds that most of these policies were effective in reducing the potential need for leaning by monetary policy; (ii) the effectiveness of the monetary policy transmission mechanism depends on the state of the financial system, implying that financial system conditions need to be taken into account by monetary policy; (iii) although exceptionally low interest rates and other forms of monetary stimulus are sometimes needed to support growth and achieve inflation-target mandates, they may lead to excessive risk-taking activities and therefore contribute to the buildup of financial imbalances; and (iv) coordination of monetary and macroprudential policies for dealing with imbalances may, in some circumstances, be beneficial. The paper concludes by identifying future areas of research to further clarify the role of monetary policy in addressing financial stability risks.

I haven’t had time to review this paper thoroughly yet, but a quick read gives me the impression it’s intended to provide a scrap of respectability for mission creep and central planning by our Wise Masters in Ottawa. Assiduous Readers will remember that “macroprudential” is the Central Planners’ jargon for credit rationing, as discussed in the post Ultra-low or negative interest rates: what they mean for financial stability and growth.

It was a pretty awful day for equities:

Evidence of industrial weakness in China renewed anxiety about a global slowdown, sending Freeport-McMoRan Inc. tumbling 9.1 percent as copper dropped to the lowest in a month. Energy shares lost 3.6 percent as oil prices slid. The Nasdaq Biotechnology Index sank 6 percent following its worst week since 2011. Amazon.com Inc. and Facebook Inc. fell more than 3.8 percent as investors sold some of the year’s better performers. Alcoa Inc. rose 5.7 percent after saying it will split into two companies.

The Standard & Poor’s 500 Index fell 2.6 percent to 1,881.77 at 4 p.m. in New York, down for a fifth consecutive session to the lowest since Aug. 25. The Dow Jones Industrial Average lost 312.78 points, or 1.9 percent, to 16,001.89. The Nasdaq Composite Index dropped 3 percent, while the Russell 2000 Index slumped 2.9 percent to an 11-month low. About 8.4 billion shares traded hands on U.S. exchanges Monday, 15 percent above the three-month average.

And even worse for commodities:

Investors are reacting to diminished demand from China and an end to the cheap-money era provided by the Federal Reserve. A Bloomberg index of commodity futures has fallen 50 percent since a 2011 high, and eight of the 10 worst performers in the Standard & Poor’s 500 Index this year are commodities-related businesses.

Now it all seems to be coming apart at once. Alcoa Inc., the biggest U.S. aluminum producer, said it would break itself into two companies amid a glut stemming from booming production. Royal Dutch Shell Plc announced it would abandon its drilling campaign in U.S. Arctic waters after spending $7 billion. And the carnage culminated Monday with Glencore Plc, the commodities powerhouse that came to symbolize the era with its initial public offering in 2011 and bold acquisition of a rival in 2013, falling by as much as 31 percent in London trading.

And portfolio managers who live by the sword, die by the sword:

Ruane Cunniff & Goldfarb, managers of the $7.8 billion Sequoia Fund, suffered a paper loss of about $1.2 billion after shares of Valeant Pharmaceuticals plunged.

The drug maker fell as much as 20 percent after Democrats in the U.S. House asked to subpoena the company for documents relating to drug price increases, the latest move by politicians seeking to curb prices on acquired drugs.

Ruane Cunniff, Valeant’s largest owner, held 33.9 million shares of the drug company as of June 30, according to data compiled by Bloomberg. Valeant fell $35.79, or 18 percent, in New York trading at 2:23 pm, which translates to a loss for the money manager of $1.21 billion. The calculation assumes the money manager has not added or sold shares.

…

Valeant represented 29 percent of the fund’s holdings as of June 30, according to data compiled by Bloomberg. The fund outperformed 99 percent of rivals this year and 97 percent over the past five years.

Valeant shares, including reinvested dividends, have climbed almost seven-fold over the past five years.

And Fed officials are still jawboning the market:

The Federal Reserve will probably raise interest rates later this year and tighten policy gradually thereafter, New York Fed President William C. Dudley said, echoing the sentiment of Chair Janet Yellen that an uncertain global outlook won’t postpone liftoff into 2016.

“The economy is doing pretty well,” Dudley said Monday at an event hosted by the Wall Street Journal in New York. “My expectation is that we probably will raise interest rates later this year.” Dudley said he expected growth in the second half will be a little bit weaker than in the first half, when the U.S. grew around 2.25 percent on an annualized basis.

San Francisco Fed President John Williams, speaking later on Monday, made a similar argument. Their remarks line up with Yellen, who said Sept. 24 she felt it likely the Fed would increase rates this year for the first time in almost a decade.

Meanwhile, Canadian preferred share investors were having lunch with their brokers:

It was an incredibly awful day for the Canadian preferred share market, with PerpetualDiscounts down 103bp, FixedResets losing an amazing 245bp and DeemedRetractibles off a mere 86bp. Let’s not even talk about the Performance Highlights table, it’s ridiculous. Volume was high.

PerpetualDiscounts now yield 5.76%, equivalent to 7.49% interest at the standard equivalency factor of 1.3x. Long corporates continue to yield about 4.2%, so the pre-tax interest-equivalent spread is now about 330bp. Let’s put that figure into perspective, shall we? I show only a five week period in the past fifteen years of Seniority Spreads exceeding this figure – from 2008-11-26 to 2018-12-24, inclusive. Spreads approached this figure in May, 2010, but did not breach the 330bp level.

We’ve also got FixedResets yield 4.77% … call it GOC-5 +400bp, give or take. This is ludicrous! In my listing of investment-grade FixedResets in the September PrefLetter, there was nothing with an Issue Reset Spread of as much as that; the highest spread was HSE.PR.E with a spread of +357. This has since been surpassed by the BAM new issue 5.00%+417M500, but still!

The market isn’t doing this on credit problems, or even concerns about credit problems, which would at least make some sense. I don’t know what’s driving this crash any more, although I can mutter nostrums such as ‘fear’ and ‘negative sentiment’ with the best of them. I have to think that this is an amazing buying opportunity … but as a buddy of mine used to like to say ‘One more buying opportunity … and I’ll be broke!’

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

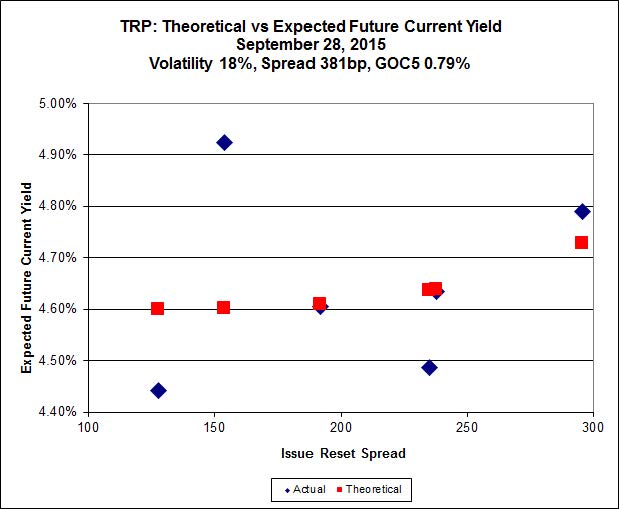

Here’s TRP:

Click for Big

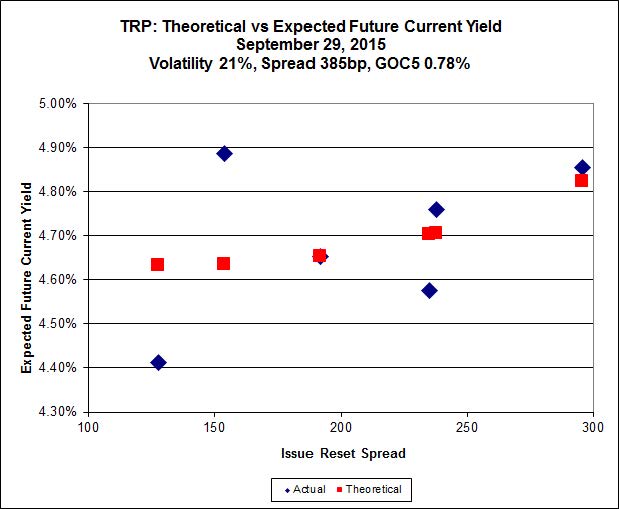

Click for BigImplied Volatility jumped again today.

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 17.50 to be $0.57 rich, while TRP.PR.C, resetting 2016-1-30 at +164, is $0.83 cheap at its bid price of 11.83.

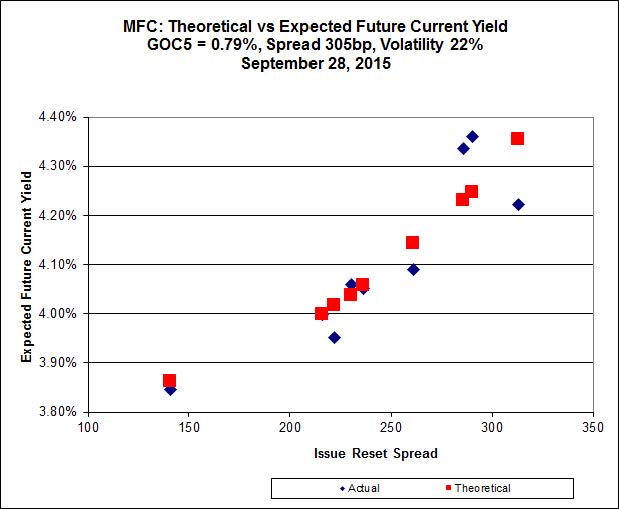

Click for Big

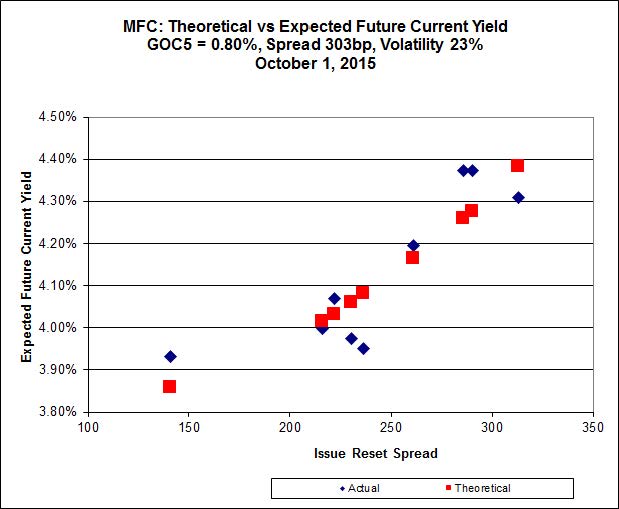

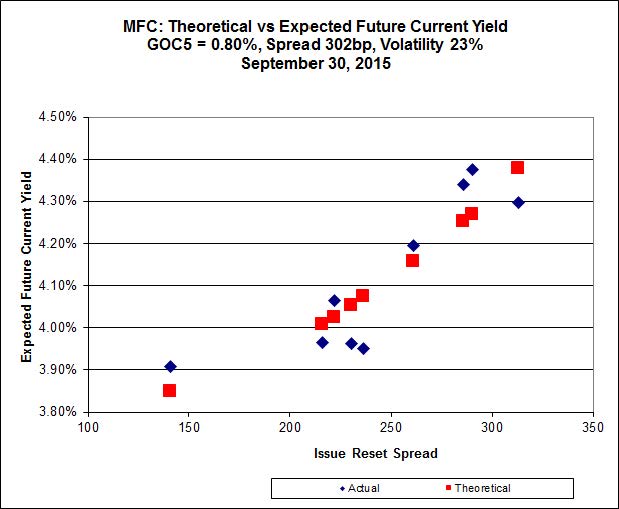

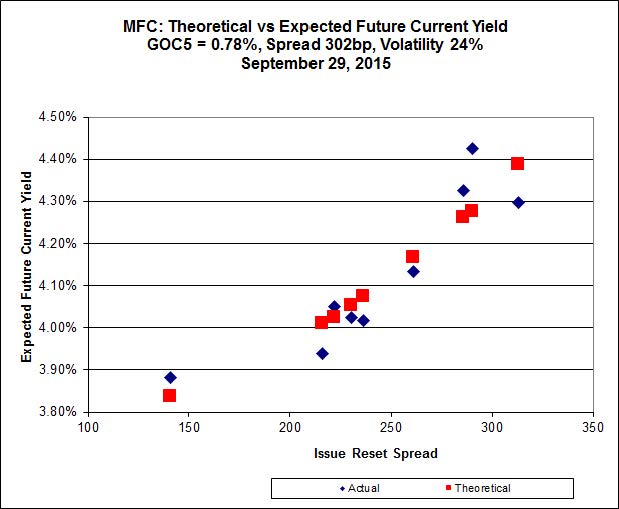

Click for BigAnother good fit today for MFC, with Implied Volatility jumping.

Most expensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 23.21 to be 0.71 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 21.16 to be 0.57 cheap.

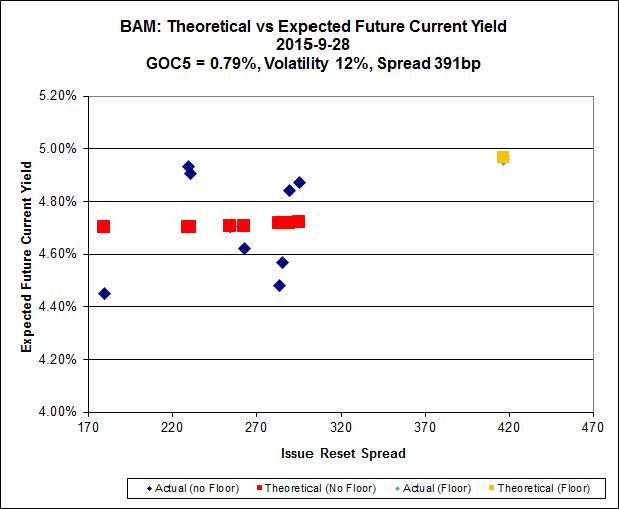

Click for Big

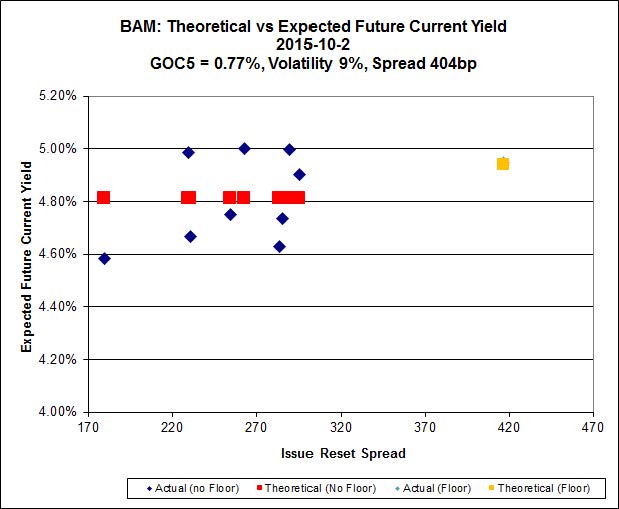

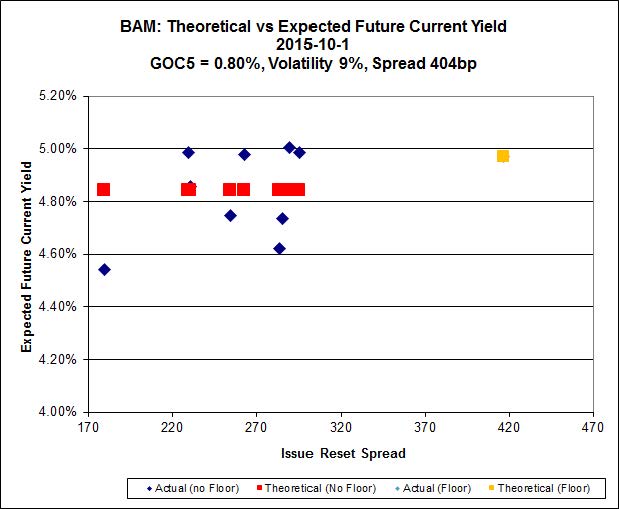

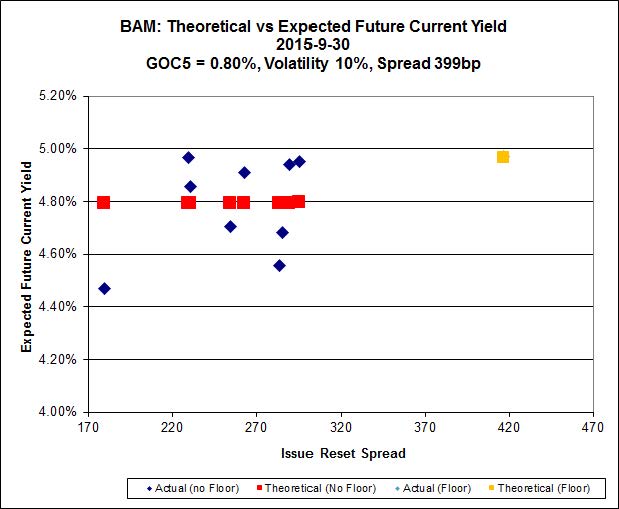

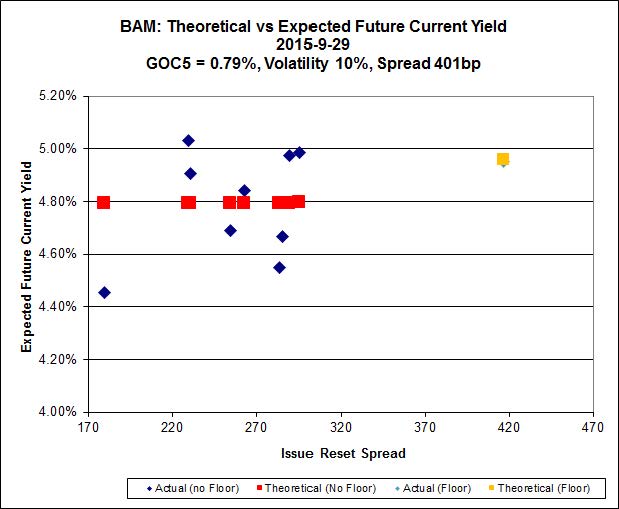

Click for BigThe fit on the BAM issues continues to be horrible. Note that the pending new issue has been added with a price of 25.00; the valuation effects of the rate floor have been ignored.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 15.70 to be $0.77 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 20.25 and appears to be $1.00 rich.

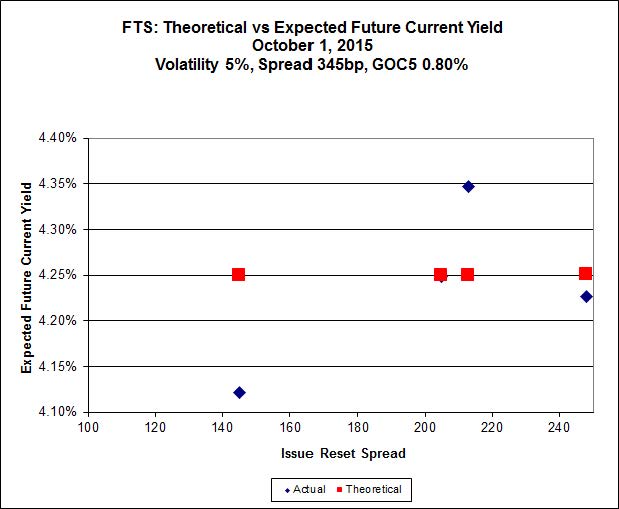

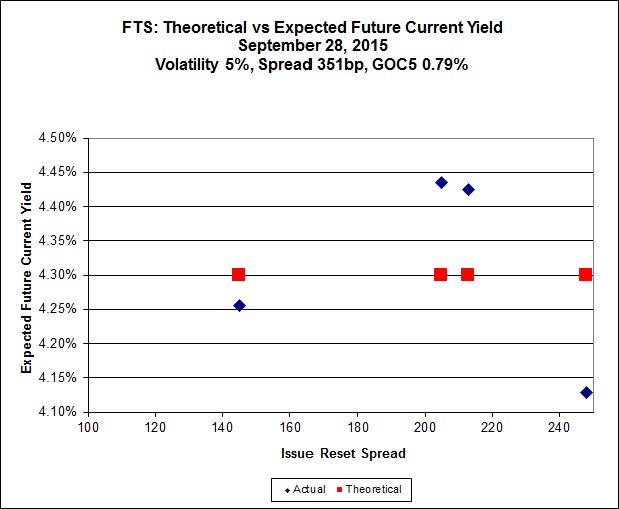

Click for Big

Click for BigFTS.PR.M, with a spread of +248bp, and bid at 19.80, looks $0.79 expensive and resets 2019-12-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 16.01 and is $0.50 cheap.

Click for Big

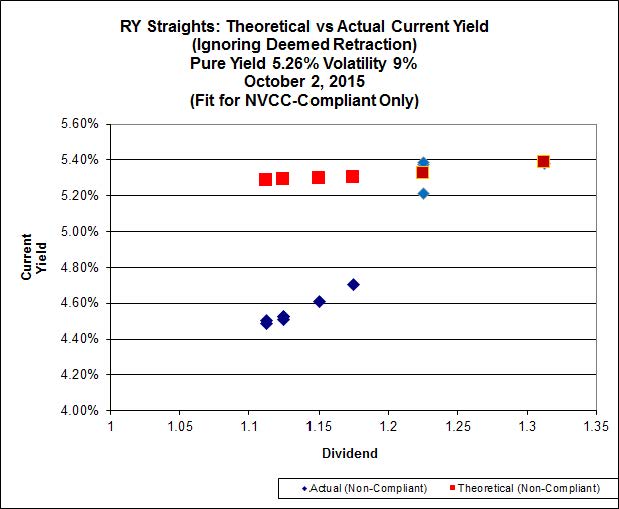

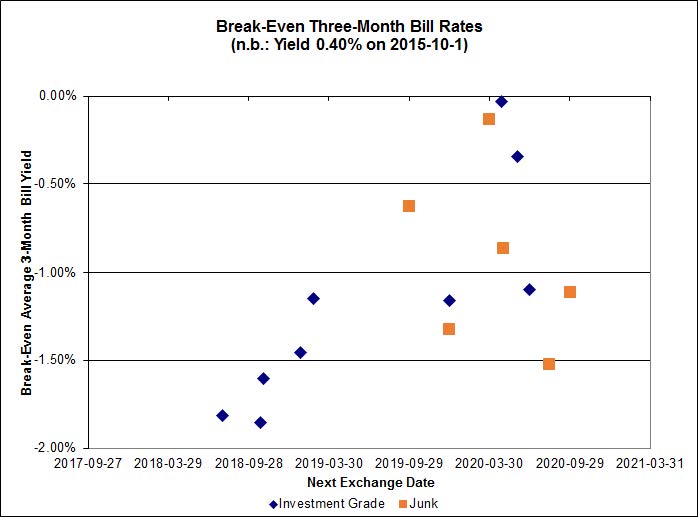

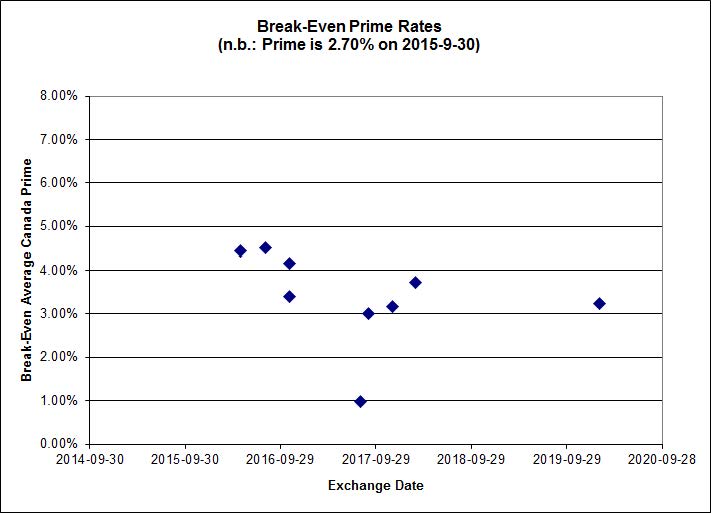

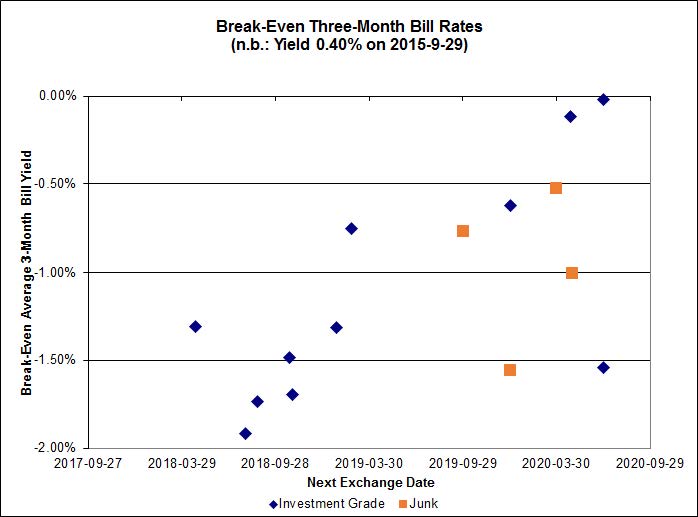

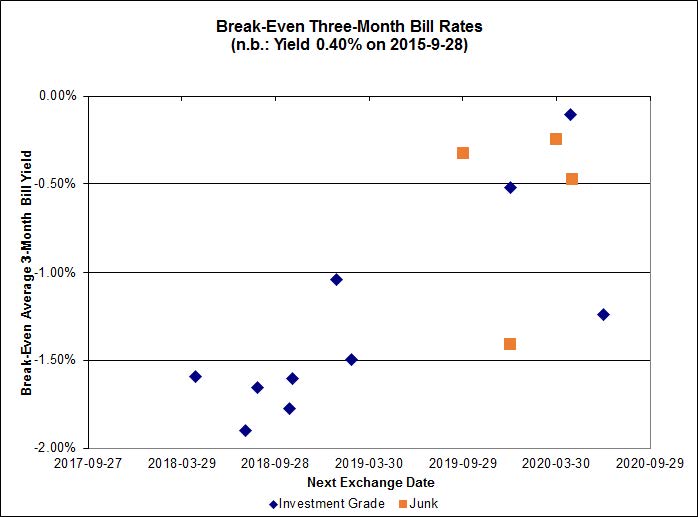

Click for BigInvestment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.04%, with two outliers above 0.00%. The distribution’s bimodality has returned, with bank NVCC non-compliant pairs averaging -1.58% and other issues averaging -0.29%. There are two junk outliers above 0.00%.

Click for Big

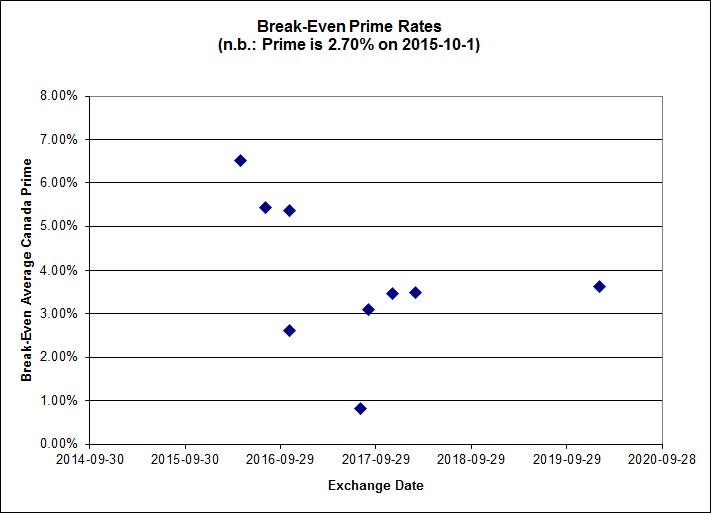

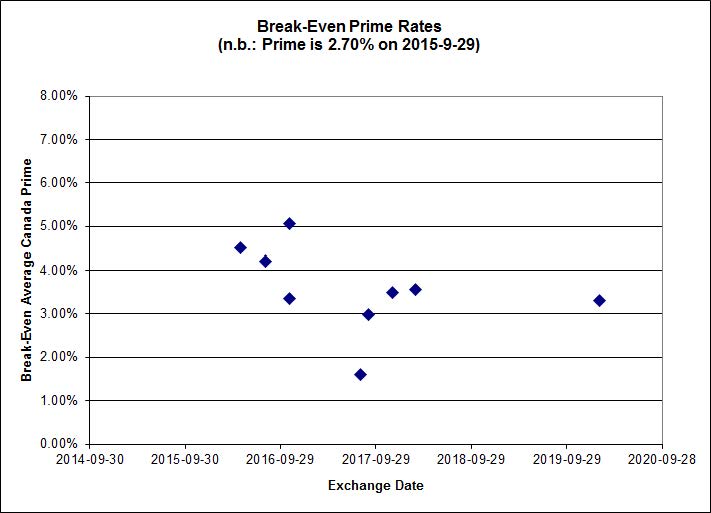

Click for BigShall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

Other Canadian preferred share investors were examining their statements:

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.3485 % |

1,659.6 |

| FixedFloater |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.3485 % |

2,901.8 |

| Floater |

4.48 % |

4.47 % |

61,062 |

16.48 |

3 |

0.3485 % |

1,764.3 |

| OpRet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.2130 % |

2,761.0 |

| SplitShare |

4.50 % |

4.92 % |

65,822 |

3.03 |

4 |

-0.2130 % |

3,235.7 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.2130 % |

2,524.7 |

| Perpetual-Premium |

5.81 % |

5.82 % |

60,640 |

14.07 |

8 |

-0.9740 % |

2,465.1 |

| Perpetual-Discount |

5.69 % |

5.76 % |

72,206 |

14.22 |

30 |

-1.0303 % |

2,493.6 |

| FixedReset |

5.15 % |

4.77 % |

173,723 |

15.27 |

75 |

-2.4533 % |

1,974.2 |

| Deemed-Retractible |

5.28 % |

5.13 % |

95,269 |

5.46 |

33 |

-0.8641 % |

2,517.7 |

| FloatingReset |

2.63 % |

4.46 % |

61,997 |

5.84 |

9 |

-1.2200 % |

2,067.0 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| TD.PF.D |

FixedReset |

-5.70 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 20.50

Evaluated at bid price : 20.50

Bid-YTW : 4.43 % |

| MFC.PR.L |

FixedReset |

-5.48 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.45

Bid-YTW : 7.35 % |

| TD.PF.E |

FixedReset |

-5.43 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 21.45

Evaluated at bid price : 21.75

Bid-YTW : 4.25 % |

| RY.PR.M |

FixedReset |

-5.32 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 19.74

Evaluated at bid price : 19.74

Bid-YTW : 4.42 % |

| MFC.PR.I |

FixedReset |

-5.31 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.05

Bid-YTW : 6.11 % |

| MFC.PR.G |

FixedReset |

-4.86 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.16

Bid-YTW : 6.00 % |

| CM.PR.Q |

FixedReset |

-4.83 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 20.51

Evaluated at bid price : 20.51

Bid-YTW : 4.36 % |

| RY.PR.J |

FixedReset |

-4.71 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 20.04

Evaluated at bid price : 20.04

Bid-YTW : 4.47 % |

| TD.PF.A |

FixedReset |

-4.62 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 18.60

Evaluated at bid price : 18.60

Bid-YTW : 4.39 % |

| BMO.PR.W |

FixedReset |

-4.61 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 18.22

Evaluated at bid price : 18.22

Bid-YTW : 4.41 % |

| TD.PF.B |

FixedReset |

-4.32 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 18.60

Evaluated at bid price : 18.60

Bid-YTW : 4.37 % |

| MFC.PR.J |

FixedReset |

-4.28 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.78

Bid-YTW : 6.00 % |

| TRP.PR.E |

FixedReset |

-4.28 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 17.50

Evaluated at bid price : 17.50

Bid-YTW : 4.82 % |

| RY.PR.H |

FixedReset |

-4.17 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 18.62

Evaluated at bid price : 18.62

Bid-YTW : 4.37 % |

| RY.PR.N |

Perpetual-Discount |

-4.06 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 22.37

Evaluated at bid price : 22.66

Bid-YTW : 5.54 % |

| BAM.PF.E |

FixedReset |

-4.05 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 17.75

Evaluated at bid price : 17.75

Bid-YTW : 5.12 % |

| CM.PR.O |

FixedReset |

-4.04 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 18.75

Evaluated at bid price : 18.75

Bid-YTW : 4.36 % |

| TRP.PR.D |

FixedReset |

-3.88 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 17.10

Evaluated at bid price : 17.10

Bid-YTW : 4.86 % |

| NA.PR.W |

FixedReset |

-3.84 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 18.27

Evaluated at bid price : 18.27

Bid-YTW : 4.48 % |

| CM.PR.P |

FixedReset |

-3.70 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 17.97

Evaluated at bid price : 17.97

Bid-YTW : 4.44 % |

| IFC.PR.C |

FixedReset |

-3.64 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.55

Bid-YTW : 7.44 % |

| NA.PR.S |

FixedReset |

-3.57 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 18.90

Evaluated at bid price : 18.90

Bid-YTW : 4.50 % |

| RY.PR.Z |

FixedReset |

-3.56 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 18.71

Evaluated at bid price : 18.71

Bid-YTW : 4.30 % |

| SLF.PR.H |

FixedReset |

-3.54 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.17

Bid-YTW : 7.89 % |

| TRP.PR.F |

FloatingReset |

-3.46 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 13.10

Evaluated at bid price : 13.10

Bid-YTW : 4.43 % |

| RY.PR.O |

Perpetual-Discount |

-3.45 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 22.28

Evaluated at bid price : 22.65

Bid-YTW : 5.49 % |

| BMO.PR.S |

FixedReset |

-3.40 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 19.01

Evaluated at bid price : 19.01

Bid-YTW : 4.36 % |

| MFC.PR.N |

FixedReset |

-3.40 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.03

Bid-YTW : 7.05 % |

| BNS.PR.D |

FloatingReset |

-3.38 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.60

Bid-YTW : 6.38 % |

| FTS.PR.H |

FixedReset |

-3.31 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 13.16

Evaluated at bid price : 13.16

Bid-YTW : 4.41 % |

| BMO.PR.Y |

FixedReset |

-3.30 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 20.82

Evaluated at bid price : 20.82

Bid-YTW : 4.39 % |

| FTS.PR.G |

FixedReset |

-3.23 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 16.50

Evaluated at bid price : 16.50

Bid-YTW : 4.69 % |

| PWF.PR.F |

Perpetual-Discount |

-3.21 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 22.34

Evaluated at bid price : 22.61

Bid-YTW : 5.90 % |

| MFC.PR.M |

FixedReset |

-3.19 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.44

Bid-YTW : 6.83 % |

| TD.PF.C |

FixedReset |

-3.13 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 18.26

Evaluated at bid price : 18.26

Bid-YTW : 4.45 % |

| BAM.PF.G |

FixedReset |

-3.11 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 20.25

Evaluated at bid price : 20.25

Bid-YTW : 4.77 % |

| FTS.PR.K |

FixedReset |

-2.97 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 16.01

Evaluated at bid price : 16.01

Bid-YTW : 4.82 % |

| GWO.PR.L |

Deemed-Retractible |

-2.83 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.05

Bid-YTW : 6.23 % |

| BAM.PF.F |

FixedReset |

-2.82 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 19.97

Evaluated at bid price : 19.97

Bid-YTW : 4.82 % |

| GWO.PR.I |

Deemed-Retractible |

-2.79 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.59

Bid-YTW : 7.16 % |

| MFC.PR.K |

FixedReset |

-2.76 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.04

Bid-YTW : 6.83 % |

| GWO.PR.R |

Deemed-Retractible |

-2.75 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.25

Bid-YTW : 7.06 % |

| MFC.PR.F |

FixedReset |

-2.72 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 14.30

Bid-YTW : 9.38 % |

| TRP.PR.B |

FixedReset |

-2.59 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 11.65

Evaluated at bid price : 11.65

Bid-YTW : 4.49 % |

| IAG.PR.G |

FixedReset |

-2.59 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.70

Bid-YTW : 6.25 % |

| BAM.PF.B |

FixedReset |

-2.58 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 18.51

Evaluated at bid price : 18.51

Bid-YTW : 4.85 % |

| TRP.PR.A |

FixedReset |

-2.52 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 14.71

Evaluated at bid price : 14.71

Bid-YTW : 4.85 % |

| PWF.PR.R |

Perpetual-Premium |

-2.51 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 23.64

Evaluated at bid price : 24.10

Bid-YTW : 5.79 % |

| VNR.PR.A |

FixedReset |

-2.49 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 18.40

Evaluated at bid price : 18.40

Bid-YTW : 5.11 % |

| GWO.PR.H |

Deemed-Retractible |

-2.42 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.37

Bid-YTW : 7.03 % |

| TRP.PR.G |

FixedReset |

-2.39 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 19.57

Evaluated at bid price : 19.57

Bid-YTW : 4.85 % |

| BMO.PR.Z |

Perpetual-Discount |

-2.31 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 22.48

Evaluated at bid price : 22.80

Bid-YTW : 5.56 % |

| GWO.PR.G |

Deemed-Retractible |

-2.30 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.52

Bid-YTW : 6.68 % |

| POW.PR.B |

Perpetual-Discount |

-2.26 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 22.69

Evaluated at bid price : 22.93

Bid-YTW : 5.84 % |

| MFC.PR.B |

Deemed-Retractible |

-2.25 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.82

Bid-YTW : 7.20 % |

| MFC.PR.C |

Deemed-Retractible |

-2.15 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.01

Bid-YTW : 7.58 % |

| RY.PR.F |

Deemed-Retractible |

-2.12 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.51

Bid-YTW : 4.92 % |

| HSE.PR.G |

FixedReset |

-2.00 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 21.68

Evaluated at bid price : 22.05

Bid-YTW : 4.97 % |

| BMO.PR.T |

FixedReset |

-1.99 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 18.72

Evaluated at bid price : 18.72

Bid-YTW : 4.32 % |

| FTS.PR.M |

FixedReset |

-1.98 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 19.80

Evaluated at bid price : 19.80

Bid-YTW : 4.39 % |

| BNS.PR.Y |

FixedReset |

-1.95 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.56

Bid-YTW : 6.06 % |

| BMO.PR.Q |

FixedReset |

-1.94 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.25

Bid-YTW : 5.94 % |

| TD.PF.F |

Perpetual-Discount |

-1.91 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 22.74

Evaluated at bid price : 23.10

Bid-YTW : 5.38 % |

| BNS.PR.Z |

FixedReset |

-1.88 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.85

Bid-YTW : 6.41 % |

| POW.PR.D |

Perpetual-Discount |

-1.85 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 21.48

Evaluated at bid price : 21.74

Bid-YTW : 5.76 % |

| SLF.PR.G |

FixedReset |

-1.84 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 14.92

Bid-YTW : 8.64 % |

| CU.PR.G |

Perpetual-Discount |

-1.83 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 19.80

Evaluated at bid price : 19.80

Bid-YTW : 5.75 % |

| BAM.PF.A |

FixedReset |

-1.80 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 19.05

Evaluated at bid price : 19.05

Bid-YTW : 5.04 % |

| W.PR.J |

Perpetual-Discount |

-1.79 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 23.32

Evaluated at bid price : 23.60

Bid-YTW : 6.05 % |

| SLF.PR.E |

Deemed-Retractible |

-1.71 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.15

Bid-YTW : 7.46 % |

| TD.PR.T |

FloatingReset |

-1.68 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.63

Bid-YTW : 4.46 % |

| POW.PR.A |

Perpetual-Premium |

-1.67 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 23.95

Evaluated at bid price : 24.20

Bid-YTW : 5.79 % |

| HSE.PR.C |

FixedReset |

-1.55 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 20.33

Evaluated at bid price : 20.33

Bid-YTW : 5.02 % |

| IGM.PR.B |

Perpetual-Premium |

-1.52 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 24.55

Evaluated at bid price : 24.84

Bid-YTW : 5.93 % |

| TD.PR.Y |

FixedReset |

-1.50 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.23

Bid-YTW : 3.68 % |

| CU.PR.E |

Perpetual-Discount |

-1.43 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 21.34

Evaluated at bid price : 21.34

Bid-YTW : 5.81 % |

| SLF.PR.A |

Deemed-Retractible |

-1.41 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.02

Bid-YTW : 7.15 % |

| MFC.PR.H |

FixedReset |

-1.40 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.21

Bid-YTW : 5.04 % |

| PWF.PR.P |

FixedReset |

-1.36 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 14.52

Evaluated at bid price : 14.52

Bid-YTW : 4.22 % |

| PWF.PR.K |

Perpetual-Discount |

-1.36 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 21.57

Evaluated at bid price : 21.83

Bid-YTW : 5.76 % |

| SLF.PR.I |

FixedReset |

-1.34 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.90

Bid-YTW : 6.63 % |

| BMO.PR.M |

FixedReset |

-1.32 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.89

Bid-YTW : 3.75 % |

| GWO.PR.S |

Deemed-Retractible |

-1.30 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.80

Bid-YTW : 6.56 % |

| RY.PR.W |

Perpetual-Discount |

-1.23 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 23.12

Evaluated at bid price : 23.38

Bid-YTW : 5.29 % |

| W.PR.H |

Perpetual-Discount |

-1.18 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 23.22

Evaluated at bid price : 23.52

Bid-YTW : 5.96 % |

| CU.PR.F |

Perpetual-Discount |

-1.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 20.00

Evaluated at bid price : 20.00

Bid-YTW : 5.69 % |

| BNS.PR.A |

FloatingReset |

-1.10 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.45

Bid-YTW : 4.30 % |

| BNS.PR.B |

FloatingReset |

-1.10 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.56

Bid-YTW : 4.63 % |

| TD.PR.S |

FixedReset |

-1.07 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.00

Bid-YTW : 3.67 % |

| CU.PR.C |

FixedReset |

-1.07 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 19.40

Evaluated at bid price : 19.40

Bid-YTW : 4.23 % |

| CU.PR.D |

Perpetual-Discount |

-1.06 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 21.45

Evaluated at bid price : 21.45

Bid-YTW : 5.78 % |

| HSE.PR.A |

FixedReset |

-1.04 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 13.36

Evaluated at bid price : 13.36

Bid-YTW : 4.85 % |

| IFC.PR.A |

FixedReset |

1.04 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 15.50

Bid-YTW : 9.26 % |

| PWF.PR.L |

Perpetual-Discount |

3.23 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 22.44

Evaluated at bid price : 22.70

Bid-YTW : 5.70 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| NA.PR.M |

Deemed-Retractible |

320,275 |

Called for redemption.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2015-10-28

Maturity Price : 25.50

Evaluated at bid price : 25.81

Bid-YTW : -0.29 % |

| BNS.PR.M |

Deemed-Retractible |

112,933 |

RBC crossed 100,000 at 25.16.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 25.00

Bid-YTW : 4.66 % |

| CU.PR.I |

FixedReset |

74,489 |

TD crossed 30,000 at 25.15.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 23.19

Evaluated at bid price : 25.12

Bid-YTW : 4.38 % |

| MFC.PR.J |

FixedReset |

44,170 |

Scotia crossed 36,600 at 21.70.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.78

Bid-YTW : 6.00 % |

| SLF.PR.I |

FixedReset |

24,950 |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.90

Bid-YTW : 6.63 % |

| TD.PF.C |

FixedReset |

24,300 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 18.26

Evaluated at bid price : 18.26

Bid-YTW : 4.45 % |

| There were 44 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| RY.PR.M |

FixedReset |

Quote: 19.74 – 20.79

Spot Rate : 1.0500

Average : 0.7348

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 19.74

Evaluated at bid price : 19.74

Bid-YTW : 4.42 % |

| CM.PR.O |

FixedReset |

Quote: 18.75 – 19.49

Spot Rate : 0.7400

Average : 0.4815

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 18.75

Evaluated at bid price : 18.75

Bid-YTW : 4.36 % |

| MFC.PR.I |

FixedReset |

Quote: 21.05 – 21.79

Spot Rate : 0.7400

Average : 0.4926

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.05

Bid-YTW : 6.11 % |

| PWF.PR.F |

Perpetual-Discount |

Quote: 22.61 – 23.45

Spot Rate : 0.8400

Average : 0.5973

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 22.34

Evaluated at bid price : 22.61

Bid-YTW : 5.90 % |

| RY.PR.O |

Perpetual-Discount |

Quote: 22.65 – 23.28

Spot Rate : 0.6300

Average : 0.3890

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-28

Maturity Price : 22.28

Evaluated at bid price : 22.65

Bid-YTW : 5.49 % |

| RY.PR.F |

Deemed-Retractible |

Quote: 24.51 – 25.09

Spot Rate : 0.5800

Average : 0.3629

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.51

Bid-YTW : 4.92 % |