Here’s to the new feds, just like the old feds:

If you closed your eyes, you could almost imagine Stephen Harper is still prime minister.

Progressive voters who hoped Justin Trudeau would abruptly shift the federal government to the left once he became Prime Minister must be in despair as the new regime announces one conservative-friendly policy after another – further proof that when it comes to the really big decisions, the imperative of protecting jobs and the economy trumps human rights, the environment and other concerns in these difficult days.

For the umpteenth time, the Liberals campaigned from the left and now are governing from the centre-right. Only those born yesterday will be surprised by this.

…

The Liberals have taken a few token progressive steps: appointing women to half the posts in cabinet, restoring the long-form census, cancelling an ugly and intrusive monument to the victims of communism – that sort of on-the-margins thing. But on the big stuff, everyone is a Conservative, especially the Liberals.

It is my theory that on big, highly visible policy issues, you are actually more likely to get the right thing done if you have a government that – in theory – opposes the policy. For instance, consider the nineties when Chretien and Martin hacked away the deficit and got federal finances on an even keel. They did the right thing; many of their supporters criticized them harshly for this, but I suggest that a Conservative government at that time would not have been anywhere near so decisive.

If the Conservatives had done it, it would have reinforced every stereotype in the book; they would have cemented a reputation as the heartless party of Big Business only and would still be feeling that pain … in much the same way as the Ontario Progressive Conservatives are still losing votes because of Mike Harris’ ‘Common Sense Revolution’.

But when the Liberals do it … people first think that what the government is doing is awful … then they remember that it goes against party stereotypes to some degree … and then they decide that the situation must be really serious and the actions really necessary if the party is going against the grain. The Liberals have more political room to impose austerity; the Conservatives have more political room to run deficits totalling $127-billion.

And in the last campaign, the NDP couldn’t promise deficit-financed infrastructure spending; that would have reinforced their stereotype. The Liberals could.

So anyway, it was a cruddy day for equities:

The Standard & Poor’s 500 Index capped its worst-ever four-day start to a year, while gold rallied with the yen as turmoil in China spread around the world and billionaire George Soros warned that a larger crisis may be brewing.

The U.S. equities benchmark ended the first four days of 2016 lower by 4.9 percent, while the Dow Jones Industrial Average has erased more than 900 points so far this year. A measure of global shares wrapped up a four-day slide of 5.2 percent, its worst start in records back to 1998. Selling in global equities began in China after the central bank weakened the yuan an eighth day. Crude settled at a 12-year low, and copper dipped below $2 for the first time since 2009. The yen reached a four-month high.

…

The Standard & Poor’s 500 Index slid 2.4 percent at 4:15 p.m in New York. The index is down 4.9 percent this year, its worst start in data going back to 1928. The MSCI All-Country World Index fell for a fourth day, bringing its slide this year to 5.2 percent.

And pundits are dividing blame between Chinese retail investors …:

The globe-spanning stampede is vast and complicated, as hedge-fund managers, currency specialists and oil traders from Bangkok to Frankfurt weigh everything from rising U.S. interest rates to overflowing crude-oil storage tanks and a rising belief that China’s economic slowdown is more severe than once thought, and getting worse.

But at the head of the stampede is a cavalcade of largely unsophisticated Chinese investors who live in a country that has made gambling illegal but turned its stock markets into the world’s largest casino. This is not a small group, numbering nearly three times the population of Canada, but they are among the most active retail traders on Earth – and they’re playing roulette at a table where everyone is whispering that it’s time to bet on red.

… and ham-fisted Chinese regulators:

After watching a stock-market collapse wipe out $5 trillion of wealth in less than three months last year, Chinese authorities hatched a plan to stem the pain: circuit breakers that would be triggered by daily declines of 5 percent.

The new system went into effect Jan. 4. It lasted all of four days. After two harrowing sessions — on Monday and Thursday — that tripped the breaker repeatedly and convulsed global markets, officials suspended the rule, saying it was only exacerbating declines. While that acknowledgment addresses critics’ concerns, the flip-flop at the same time only adds to the sentiment among global investors that authorities are improvising — and improvising poorly — as they try to stabilize markets and shore up the economy.

…

On the currency front, policy makers have pledged to keep the yuan stable, drawing down a record $108 billion from foreign reserves last month to prop it up. At the same time, the People’s Bank of China set its reference rate at unexpectedly weak levels this week, raising speculation that it’s more tolerant of depreciation to spur exports.“The more alarming thing is that they weakened the currency after saying they wouldn’t,” said Patrick Chovanec, New York-based chief strategist at Silvercrest Asset Management Group. “So that raises all these issues of mixed signals, confusion. It is very unclear what the policy is, whether they know what the policy is, whether they know how to implement the policy.”

…

Chinese regulators moved to control the damage earlier Thursday, imposing a new limit on the amount of stock that major corporate shareholders can sell. That followed intervention by government funds to prop up shares on Tuesday, according to people familiar with the matter.

The Chinese circuit-breakers have attracted high-level criticism:

“They’re just on the wrong track,” said Nicholas Brady, 85, the former U.S. Treasury secretary who ran a committee that recommended the curbs on equity trading after the 1987 crash. “They need a set of circuit breakers that appropriately reflects their market.”

Brady spoke Thursday after Chinese regulators suspended their newly introduced program that ends stock trading for the entire day after a 7 percent plunge. The halt was set off twice in its first week of operation, bolstering speculation China set its threshold too low.

…

“I don’t think this is an exact science,” said Sang Lee, an analyst at financial-markets researcher Aite Group. With circuit breakers, “If you set these too low, instead of easing volatility it may increase volatility.”That echoes the view of Brady, who was chairman of Wall Street powerhouse Dillon Read & Co. when President Ronald Reagan asked him to figure out what happened during the 1987 crash and propose solutions.

Meanwhile, Adam Haigh on Bloomberg reminds us there’s still lots of arbitrary rules to restrict Chinese markets:

A 10 percent daily limit on single stock moves and a rule preventing investors from buying and selling the same shares in a day remain in force. Volume in what was once the world’s most active index futures market is minimal after authorities curtailed trading amid a summer rout, making it more difficult to implement hedging strategies. Officials unveiled curbs Thursday on share sales by major stockholders just a day before an existing ban was due to expire. And the activity of foreign investors is limited by quotas, given either to asset managers or to users of the Hong Kong-Shanghai exchange link.

…

There’s also the prospect that regulators and executives will dust off last year’s playbook as they seek to stem losses. At the height of the summer rout, about half of China’s listed companies were halted, while officials investigated trading strategies, made it harder for investors to borrow money to buy equities and vowed to “purify” the market.

Meanwhile, Poloz has a new script from his new masters:

Bank of Canada governor Stephen Poloz is encouraging the Liberal government to act on promised infrastructure spending, acknowledging there are limits to what monetary policy can do to boost Canada’s sluggish economy.

Officials with Canada’s central bank are currently working with the Finance Department on economic models aimed at measuring the likely impact of promised government spending on infrastructure, as well as tax cuts that took effect this year.

…

Speaking to reporters in Ottawa, Mr. Poloz said the cheaper dollar alone is not enough to counter the shock from the commodities price slump. And he said the economy would benefit from some government fiscal policy.“Infrastructure is an ingredient to economic growth. It’s sort of the enabler of economic growth,” he said.

Speaking of the Canadian dollar, I ran across the publication A History of the Canadian Dollar by James Powell and published by the Bank of Canada today. It’s ten years old now … it might need a new chapter! I’m too young to remember the hey-day of:

Click for Big

… so I’ll have to find solace in boring the whippersnappers with tales of:

Click for Big

There’s a chance that PrefBlog won’t have John Nagel to kick around any more:

John Nagel, a fixture in the preferred share market for more than three decades, has retired from his post at Desjardins Securities.

But it’s not clear at this stage, whether Nagel who spent the past 13 plus years at Desjardins, has retired from the investment industry.

In a note to clients, Nagel – who first traded preferred shares while at Gardiner Watson in the mid-1980s – noted the firm had achieved a “great deal” since he arrived in June 2002. For instance the firm “established and earned a significant improvement in its syndication positions,” as well as hiring and training assistants and analysts “many of whom have continued on successfully in the financial services field.” In addition, Nagel’s team, that produced market commentary and market, improved the firm’s preferred trading and sales activities.

…

With Nagel’s retirement, the preferred share department will report to Mark Lucey, a managing director and head of equities and capital markets. Previously it reported to fixed income. Julian Pope, David Paul and Alex Somjen will now man the firm’s pref share group.

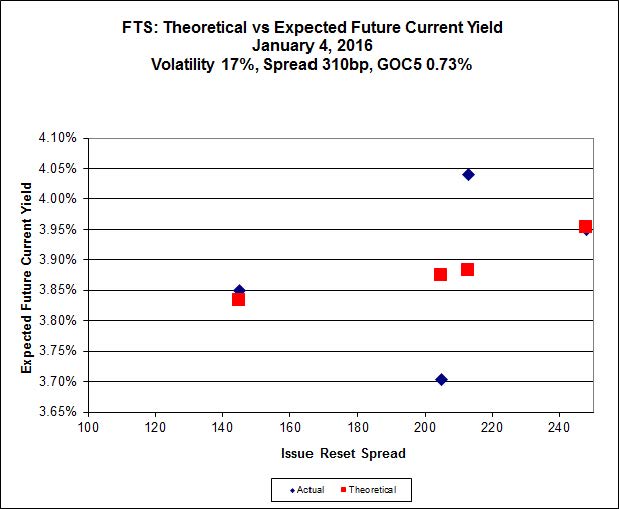

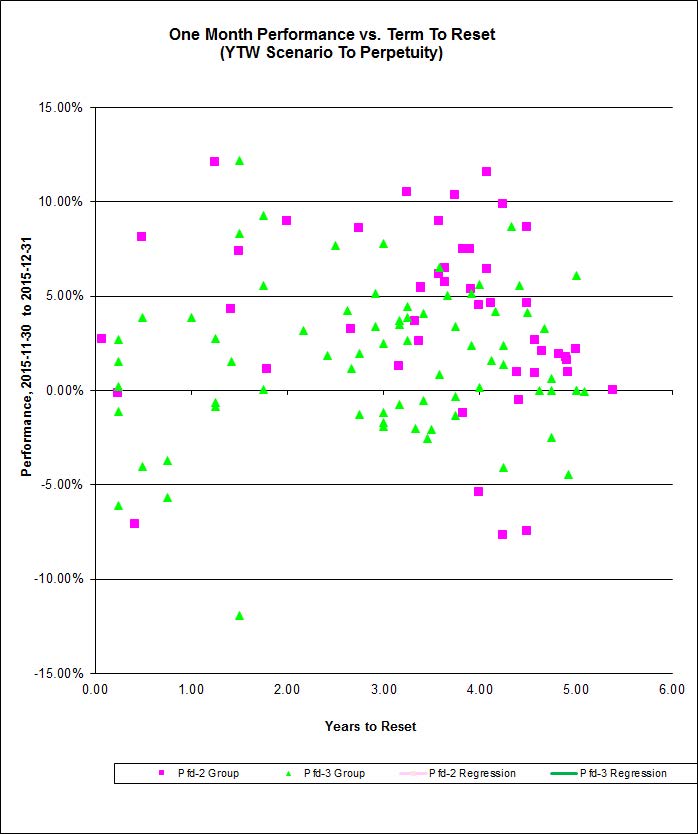

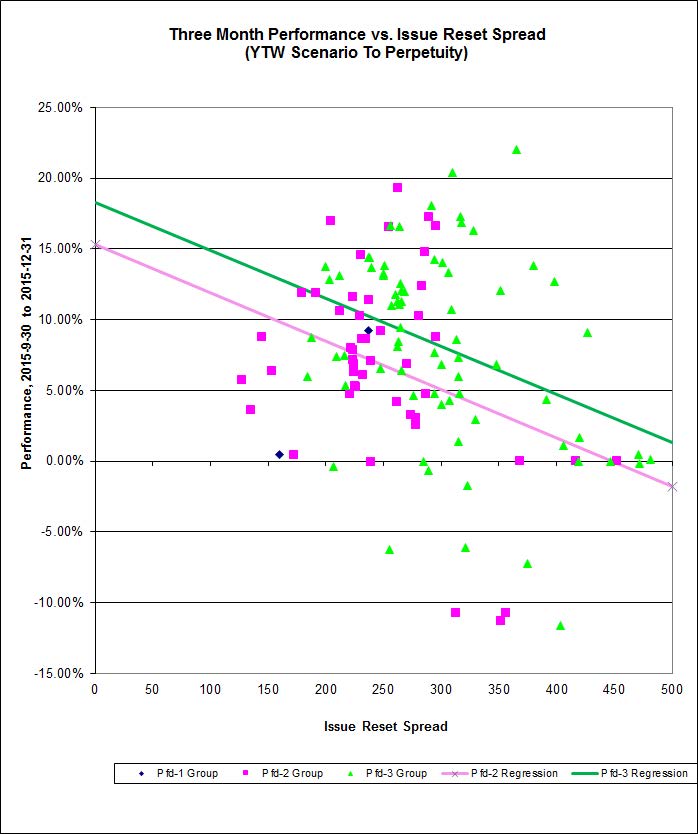

Meanwhile, in the Canadian preferred share market:

Click for Big

It was an appalling day for the Canadian preferred share market, with PerpetualDiscounts down 101bp, FixedResets losing 136bp and DeemedRetractibles off 63bp. The Performance Highlights table is about as long as one might expect. Volume was well below average.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 4.85 % | 5.88 % | 27,752 | 16.80 | 1 | -1.7544 % | 1,605.2 |

| FixedFloater | 6.82 % | 6.05 % | 32,894 | 16.14 | 1 | 0.0000 % | 2,859.5 |

| Floater | 4.29 % | 4.53 % | 81,017 | 16.40 | 4 | -2.4801 % | 1,780.7 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.3178 % | 2,735.5 |

| SplitShare | 4.83 % | 5.76 % | 74,846 | 1.82 | 6 | -0.3178 % | 3,201.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.3178 % | 2,497.6 |

| Perpetual-Premium | 5.87 % | 3.79 % | 84,250 | 0.09 | 6 | -0.5644 % | 2,515.6 |

| Perpetual-Discount | 5.71 % | 5.75 % | 94,652 | 14.31 | 34 | -1.0117 % | 2,528.5 |

| FixedReset | 5.29 % | 4.64 % | 243,586 | 14.80 | 81 | -1.3646 % | 1,951.6 |

| Deemed-Retractible | 5.26 % | 5.23 % | 121,283 | 5.28 | 34 | -0.6262 % | 2,559.5 |

| FloatingReset | 2.89 % | 4.49 % | 62,948 | 5.62 | 13 | -0.5922 % | 2,085.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| VNR.PR.A | FixedReset | -7.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 17.62 Evaluated at bid price : 17.62 Bid-YTW : 5.13 % |

| PWF.PR.T | FixedReset | -5.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 21.02 Evaluated at bid price : 21.02 Bid-YTW : 3.87 % |

| HSE.PR.A | FixedReset | -4.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 11.31 Evaluated at bid price : 11.31 Bid-YTW : 5.44 % |

| SLF.PR.H | FixedReset | -4.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.40 Bid-YTW : 8.53 % |

| CCS.PR.C | Deemed-Retractible | -4.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.02 Bid-YTW : 6.84 % |

| BAM.PR.T | FixedReset | -3.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 16.21 Evaluated at bid price : 16.21 Bid-YTW : 4.83 % |

| BAM.PF.E | FixedReset | -3.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 18.70 Evaluated at bid price : 18.70 Bid-YTW : 4.74 % |

| BAM.PR.B | Floater | -3.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 10.50 Evaluated at bid price : 10.50 Bid-YTW : 4.53 % |

| BMO.PR.Q | FixedReset | -3.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.50 Bid-YTW : 6.64 % |

| MFC.PR.F | FixedReset | -3.43 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.78 Bid-YTW : 9.87 % |

| SLF.PR.J | FloatingReset | -3.31 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.15 Bid-YTW : 9.96 % |

| BAM.PR.X | FixedReset | -3.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 14.32 Evaluated at bid price : 14.32 Bid-YTW : 4.69 % |

| NA.PR.W | FixedReset | -3.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 17.40 Evaluated at bid price : 17.40 Bid-YTW : 4.54 % |

| FTS.PR.K | FixedReset | -3.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 17.79 Evaluated at bid price : 17.79 Bid-YTW : 4.21 % |

| BMO.PR.Y | FixedReset | -3.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 19.76 Evaluated at bid price : 19.76 Bid-YTW : 4.50 % |

| BAM.PR.C | Floater | -2.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 10.43 Evaluated at bid price : 10.43 Bid-YTW : 4.56 % |

| RY.PR.M | FixedReset | -2.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 19.23 Evaluated at bid price : 19.23 Bid-YTW : 4.48 % |

| BAM.PR.K | Floater | -2.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 10.50 Evaluated at bid price : 10.50 Bid-YTW : 4.53 % |

| BAM.PF.B | FixedReset | -2.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 18.66 Evaluated at bid price : 18.66 Bid-YTW : 4.71 % |

| MFC.PR.L | FixedReset | -2.53 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.12 Bid-YTW : 7.65 % |

| W.PR.J | Perpetual-Discount | -2.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 22.88 Evaluated at bid price : 23.15 Bid-YTW : 6.07 % |

| CM.PR.Q | FixedReset | -2.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 19.35 Evaluated at bid price : 19.35 Bid-YTW : 4.56 % |

| MFC.PR.K | FixedReset | -2.52 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.82 Bid-YTW : 7.77 % |

| BNS.PR.Z | FixedReset | -2.46 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.02 Bid-YTW : 7.00 % |

| FTS.PR.H | FixedReset | -2.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 13.81 Evaluated at bid price : 13.81 Bid-YTW : 4.09 % |

| RY.PR.J | FixedReset | -2.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 19.41 Evaluated at bid price : 19.41 Bid-YTW : 4.55 % |

| POW.PR.D | Perpetual-Discount | -2.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 21.66 Evaluated at bid price : 21.91 Bid-YTW : 5.72 % |

| POW.PR.G | Perpetual-Discount | -2.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 23.53 Evaluated at bid price : 24.00 Bid-YTW : 5.84 % |

| BAM.PF.G | FixedReset | -2.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 20.35 Evaluated at bid price : 20.35 Bid-YTW : 4.67 % |

| MFC.PR.I | FixedReset | -2.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.50 Bid-YTW : 6.46 % |

| MFC.PR.H | FixedReset | -2.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.35 Bid-YTW : 6.14 % |

| NA.PR.S | FixedReset | -1.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 17.95 Evaluated at bid price : 17.95 Bid-YTW : 4.57 % |

| BAM.PF.A | FixedReset | -1.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 20.00 Evaluated at bid price : 20.00 Bid-YTW : 4.71 % |

| TRP.PR.D | FixedReset | -1.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 17.55 Evaluated at bid price : 17.55 Bid-YTW : 4.64 % |

| BAM.PR.R | FixedReset | -1.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 15.35 Evaluated at bid price : 15.35 Bid-YTW : 5.00 % |

| PWF.PR.R | Perpetual-Discount | -1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 23.17 Evaluated at bid price : 23.60 Bid-YTW : 5.82 % |

| MFC.PR.G | FixedReset | -1.86 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.10 Bid-YTW : 6.68 % |

| TRP.PR.F | FloatingReset | -1.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 13.25 Evaluated at bid price : 13.25 Bid-YTW : 4.54 % |

| SLF.PR.G | FixedReset | -1.78 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.36 Bid-YTW : 9.29 % |

| GWO.PR.N | FixedReset | -1.77 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.31 Bid-YTW : 10.16 % |

| MFC.PR.J | FixedReset | -1.77 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.45 Bid-YTW : 6.91 % |

| BAM.PR.E | Ratchet | -1.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 25.00 Evaluated at bid price : 14.00 Bid-YTW : 5.88 % |

| MFC.PR.C | Deemed-Retractible | -1.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.25 Bid-YTW : 7.50 % |

| PWF.PR.K | Perpetual-Discount | -1.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 21.49 Evaluated at bid price : 21.49 Bid-YTW : 5.77 % |

| PWF.PR.H | Perpetual-Premium | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 24.22 Evaluated at bid price : 24.51 Bid-YTW : 5.87 % |

| W.PR.H | Perpetual-Discount | -1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 22.71 Evaluated at bid price : 23.00 Bid-YTW : 6.00 % |

| BNS.PR.N | Deemed-Retractible | -1.53 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-01-27 Maturity Price : 25.00 Evaluated at bid price : 25.07 Bid-YTW : 4.66 % |

| MFC.PR.B | Deemed-Retractible | -1.52 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.75 Bid-YTW : 7.33 % |

| BAM.PF.F | FixedReset | -1.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 20.25 Evaluated at bid price : 20.25 Bid-YTW : 4.67 % |

| SLF.PR.I | FixedReset | -1.50 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.01 Bid-YTW : 7.22 % |

| TD.PF.E | FixedReset | -1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 20.45 Evaluated at bid price : 20.45 Bid-YTW : 4.42 % |

| BMO.PR.Z | Perpetual-Discount | -1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 22.84 Evaluated at bid price : 23.23 Bid-YTW : 5.44 % |

| PWF.PR.P | FixedReset | -1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 13.30 Evaluated at bid price : 13.30 Bid-YTW : 4.36 % |

| CM.PR.O | FixedReset | -1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 18.35 Evaluated at bid price : 18.35 Bid-YTW : 4.37 % |

| TD.PF.D | FixedReset | -1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 19.51 Evaluated at bid price : 19.51 Bid-YTW : 4.52 % |

| CU.PR.G | Perpetual-Discount | -1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 20.25 Evaluated at bid price : 20.25 Bid-YTW : 5.63 % |

| FTS.PR.G | FixedReset | -1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 17.06 Evaluated at bid price : 17.06 Bid-YTW : 4.43 % |

| ELF.PR.F | Perpetual-Discount | -1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 22.44 Evaluated at bid price : 22.70 Bid-YTW : 5.85 % |

| TD.PR.Y | FixedReset | -1.33 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.68 Bid-YTW : 3.92 % |

| TRP.PR.H | FloatingReset | -1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 9.71 Evaluated at bid price : 9.71 Bid-YTW : 4.53 % |

| SLF.PR.E | Deemed-Retractible | -1.32 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.26 Bid-YTW : 7.47 % |

| MFC.PR.N | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.06 Bid-YTW : 7.08 % |

| FTS.PR.M | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 19.15 Evaluated at bid price : 19.15 Bid-YTW : 4.46 % |

| IFC.PR.A | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.35 Bid-YTW : 9.35 % |

| MFC.PR.M | FixedReset | -1.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.43 Bid-YTW : 6.88 % |

| ELF.PR.G | Perpetual-Discount | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 5.68 % |

| CU.PR.F | Perpetual-Discount | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 20.25 Evaluated at bid price : 20.25 Bid-YTW : 5.63 % |

| CM.PR.P | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 17.88 Evaluated at bid price : 17.88 Bid-YTW : 4.38 % |

| BNS.PR.C | FloatingReset | -1.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.01 Bid-YTW : 4.52 % |

| RY.PR.H | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 18.16 Evaluated at bid price : 18.16 Bid-YTW : 4.39 % |

| RY.PR.I | FixedReset | -1.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.44 Bid-YTW : 4.39 % |

| BAM.PR.Z | FixedReset | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 19.61 Evaluated at bid price : 19.61 Bid-YTW : 4.87 % |

| CU.PR.D | Perpetual-Discount | -1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 21.45 Evaluated at bid price : 21.77 Bid-YTW : 5.69 % |

| GWO.PR.S | Deemed-Retractible | -1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.12 Bid-YTW : 5.81 % |

| CU.PR.H | Perpetual-Discount | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 23.15 Evaluated at bid price : 23.45 Bid-YTW : 5.66 % |

| POW.PR.A | Perpetual-Discount | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 23.96 Evaluated at bid price : 24.21 Bid-YTW : 5.80 % |

| PWF.PR.A | Floater | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 12.61 Evaluated at bid price : 12.61 Bid-YTW : 3.78 % |

| FTS.PR.J | Perpetual-Discount | -1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 21.45 Evaluated at bid price : 21.78 Bid-YTW : 5.51 % |

| HSE.PR.C | FixedReset | 1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 17.88 Evaluated at bid price : 17.88 Bid-YTW : 5.63 % |

| BNS.PR.D | FloatingReset | 1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.24 Bid-YTW : 6.95 % |

| HSE.PR.G | FixedReset | 1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 18.70 Evaluated at bid price : 18.70 Bid-YTW : 5.84 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.Q | FixedReset | 162,764 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2021-05-24 Maturity Price : 25.00 Evaluated at bid price : 25.64 Bid-YTW : 5.05 % |

| TRP.PR.H | FloatingReset | 110,400 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 9.71 Evaluated at bid price : 9.71 Bid-YTW : 4.53 % |

| TRP.PR.F | FloatingReset | 106,435 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-07 Maturity Price : 13.25 Evaluated at bid price : 13.25 Bid-YTW : 4.54 % |

| MFC.PR.F | FixedReset | 105,420 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.78 Bid-YTW : 9.87 % |

| BNS.PR.E | FixedReset | 102,593 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2021-04-25 Maturity Price : 25.00 Evaluated at bid price : 25.72 Bid-YTW : 4.97 % |

| SLF.PR.I | FixedReset | 74,345 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.01 Bid-YTW : 7.22 % |

| There were 21 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| VNR.PR.A | FixedReset | Quote: 17.62 – 18.91 Spot Rate : 1.2900 Average : 0.8588 YTW SCENARIO |

| CCS.PR.C | Deemed-Retractible | Quote: 22.02 – 22.75 Spot Rate : 0.7300 Average : 0.4943 YTW SCENARIO |

| POW.PR.G | Perpetual-Discount | Quote: 24.00 – 24.50 Spot Rate : 0.5000 Average : 0.3265 YTW SCENARIO |

| PWF.PR.T | FixedReset | Quote: 21.02 – 22.00 Spot Rate : 0.9800 Average : 0.8083 YTW SCENARIO |

| CU.PR.G | Perpetual-Discount | Quote: 20.25 – 20.70 Spot Rate : 0.4500 Average : 0.2944 YTW SCENARIO |

| RY.PR.O | Perpetual-Discount | Quote: 22.60 – 22.97 Spot Rate : 0.3700 Average : 0.2234 YTW SCENARIO |