Today’s whining over liquidity focusses on investor homogeneity and the victory of deep pockets:

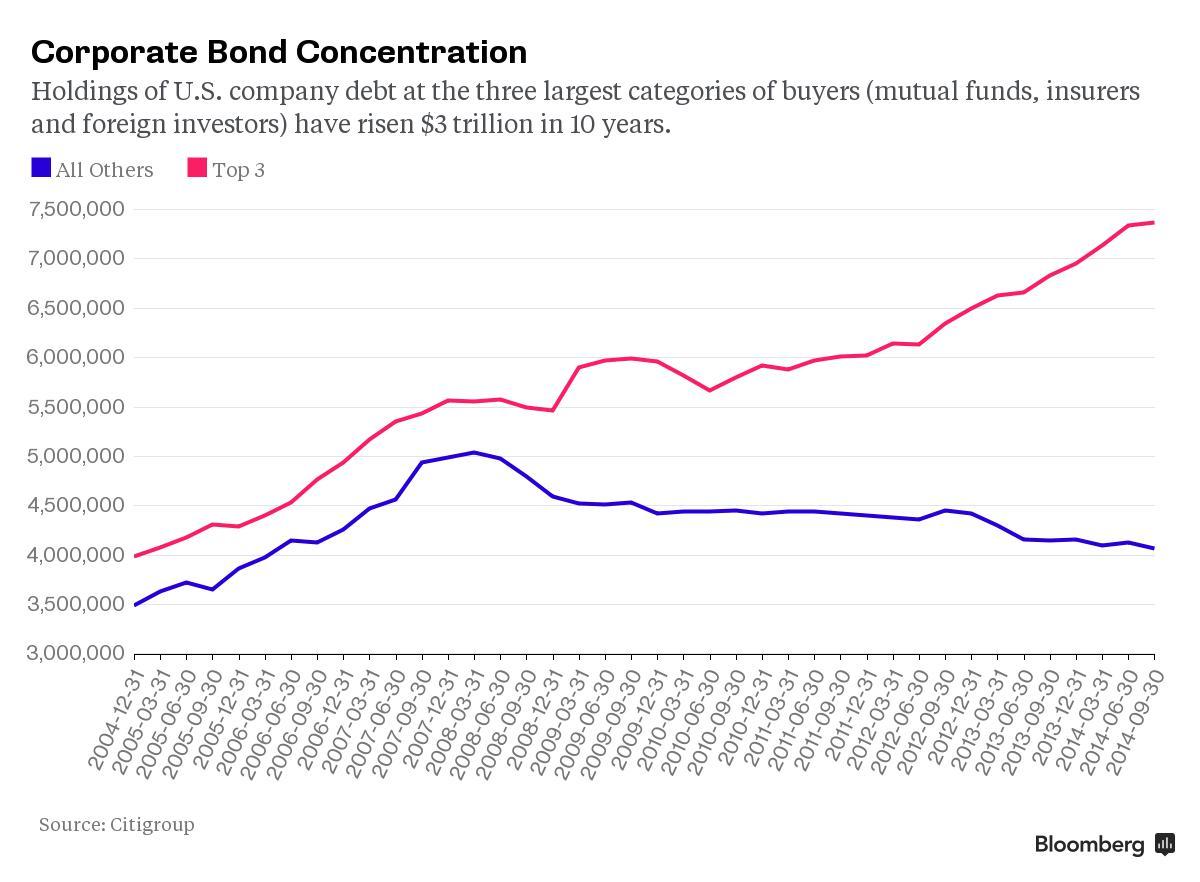

The size of the U.S. corporate-bond market has ballooned by $3.7 trillion during the past decade, yet almost all of that growth is concentrated in the hands of three types of buyers: mutual funds, foreign investors and insurance companies, according to Citigroup. That combination could lead to more selling than the market can absorb when the Federal Reserve raises interest rates for the first time since 2006, [Citigroup Inc. strategist Stephen] Antczak said.

“All the money is going to the same place, and when something adversely impacts one, chances are the same factor adversely impacts everyone else, and there’s nobody there to take the other side,” Antczak said in a telephone interview. “We used to have 23 types of investors in the market. Now we have three. In my mind, that’s the key driver.”

The three investor groups hold almost two-thirds of total corporate debt, Citigroup data show. Mutual funds, which are forced to sell when investors redeem cash, grew the fastest, more than doubling their share to 22 percent in 10 years. Overseas investors now hold almost a quarter of the market. Wells Fargo & Co. analysts warned last month that those buyers may be prompted to exit if the dollar weakened at the same time bond yields rose.

Hedge funds, government pension funds and securities brokers are among 20 other groups that hold 37 percent.

…

“A couple of investors have been acting like brokers, thinking about being a source of liquidity to the Street,” Antczak said. “They are big and able to hold less-liquid positions because they don’t have to mark it against the market and can hold until maturity.”That’s what New York Life Insurance Co.’s investment arm, which oversees $215 billion of policyholder money, did during the so-called taper tantrum of 2013. The Fed’s move to end its unprecedented stimulus measures that year triggered a selloff that wiped out 5 percent from U.S. speculative-grade corporate bonds in less than two months.

The declines were “exaggerated because the need for liquidity was in excess of what the dealer community could provide,” Tom Girard, head of fixed-income investments at NYL Investors, said in a telephone interview. The firm stepped in to buy both investment-grade and speculative-grade securities, he said.

“New York Life acquired significant amounts of bonds at very attractive spreads and yield levels because we were able to provide liquidity,” he said. “If we get another situation similar to that taper tantrum, then from my perspective it starts to shift from a challenge to an opportunity.”

Click for Big

And there is chatter that junk bond investors are getting nervous:

After providing a haven from the global bond-market selloff, speculative-grade securities have now joined the rout, tumbling almost 1 percent since the end of May. Investors are starting to flee, yanking $1.5 billion from the two biggest high-yield bond exchange-traded funds over the past week, according to data compiled by Bloomberg.

…

High-yield debt markets have “shown a degree of resiliency here to the shift in the inflation outlook,” Jeffrey Rosenberg, a managing director at BlackRock Inc.’s, said in a Bloomberg radio interview Tuesday. “That resilience could be challenged if we follow up this bout of higher rates with a shift in” expectations for when the Federal Reserve will lift rates.Case in point: BlackRock’s $14.3 billion high-yield bond ETF plunged 1.6 percent in the six days through Monday as $940.5 million exited the fund, Bloomberg data show. State Street Corp.’s $10.7 billion junk-debt ETF dropped 1.7 percent, with $571.7 million of withdrawals.

Leveraged-loan investors aren’t too happy either:

Leveraged loans dropped to their lowest level in four months amid a pullback by buyers stung by borrowers such as Dollar Tree Inc. and Goodyear Tire & Rubber Co., who have taken advantage of a paucity of new deals by seeking to lower payments on existing debt. Barclays Plc last week cut its 2015 forecast for U.S. leveraged-loan issuance to as little as $250 billion as regulatory scrutiny slows the pace of buyout financings.

Investors who buy leveraged loans are caught in a bind. A push by regulators to curb risky underwriting practices has left them with fewer deals to chase, while the interest they earn on the loans they hold falls. Sentiment has also been weighed down by a global bond rout that has sent Treasury yields to levels not seen since October.

“Buyers are pulling back from paying a premium due to the fear they will be hurt by a refinancing in very short order,” said Jason Rosiak, head of portfolio management at Newport Beach, California-based Pacific Asset Management. “That weighs on the overall market.”

Loans prices dropped to 95.9 cents on the dollar on Wednesday, after falling each of the past three weeks in the longest such stretch since the fourth quarter, according to the Standard & Poor’s/LSTA U.S. Leveraged Loan 100 Index. The debt lost 0.36 percent this month, after gaining just 0.05 percent in May, the smallest monthly return of the year.

But at least there’s less debt with negative yield:

Everyone knew it defied logic to pay for the privilege of lending trillions of dollars to European governments.

But two months ago, that didn’t stop investors from doing exactly that, causing the pool of European bonds with negative yields to soar to almost 3 trillion euros ($3.4 trillion) as of mid-April, Bank of America Corp. data show.

That trade is now dying quickly. The amount of such securities in the market has shrunk nearly in half, to 1.6 trillion euros as of June 9.

The Lapdog’s boss has told him to step up the war on banks:

Bank of England Governor Mark Carney ordered the finance industry to observe new rules on market conduct and threatened an even tougher regime if traders and bankers fail to comply.

His comments came as the BOE published the Fair and Effective Markets Review in London Wednesday, which recommends a new code of practice and longer jail terms for infractions. He said individuals must be “held to account” and firms must also take greater responsibility.

“This is a major opportunity for the industry to establish common standards of market practice,” Carney said. “If firms and their staff fail to take this opportunity, more restrictive regulation is inevitable.”

…

The markets review was announced by Chancellor of the Exchequer George Osborne at the same event a year ago. In his comments, Carney said revelations of misconduct have appeared with a “depressing frequency.” Bankers’ “ethical drift” has led to higher borrowing costs and falling confidence, while the $150 billion in fines levied on global banks has reduced their lending capacity by $3 trillion.

I love the bit where the banks are being blamed for the effects of their payment of $150-billion in fines. Very Jesuitical.

Naturally, Osborne has a valuable ally in his campaign for eternal re-election:

The Justice Department has begun an examination of trading in the U.S. Treasury market, following the outlines of its successful cases against Wall Street’s illegal practices in foreign currencies and other businesses, said three people familiar with the inquiry.

The government is also continuing to look into possible collusion in gold and silver markets and in trading around certain oil benchmarks, the people said.

Though the latest inquiry into Treasury trading is in its earliest stages, investigators are said to be probing whether information is being shared improperly by financial institutions. Some of the world’s biggest banks and their subsidiaries pleaded guilty after traders were shown to be using chat rooms, which functioned as cartels, to coordinate positions on foreign-exchange markets. These practices violated federal antitrust laws. Some of the same banks were among those that settled fraud and antitrust investigations into manipulating key interest rates.

…

It remains unclear where in the Treasury markets prosecutors aim to find wrongdoing, or if any specific allegations against Wall Street banks prompted the inquiries.

The best part of that story is that individual traders will be blamed for liquidity problems:

The Treasury Market Practices Group, an advisory committee backed by the New York Fed, finalized additions to its best practices guidelines Wednesday. For example, on a list of trading practices to avoid, it now includes “those that give a false impression of market price, depth or liquidity.”

It also added an updated recommendation “that market participants who employ trading strategies that involve high-trading volume or quoting activity should be mindful of whether a sudden change in these strategies could adversely affect market liquidity and should seek to avoid changes likely to cause such disruption,” the TMPG wrote in a statement.

And the regulators are very concerned about ‘banging the close’:

It was a simple process, according to the CFTC: Barclays traders told their brokers to buy or sell as many interest-rate swaps as needed just before 11 a.m. New York time to push the benchmark in the desired direction.

…

Here’s how a broker described the process to a trader in 2007, according to the CFTC: “If you want to affect it at 11, you tell me which way you want to affect it we’ll, we’ll attempt to affect it that way.”Another time that year, a Barclays trader told his broker to buy as much as $400 million worth of swaps to move the benchmark, according to the complaint.

…

For example, on June 25, 2007, the Barclays options desk in New York had a $635 million swaption contract that was coming due, according to the CFTC. “Barclays traders on multiple desks coordinated to employ three methods of manipulation in an attempt to maximize the amount paid to Barclays in the swaption cash settlement,” the CFTC said in the complaint.At 10:50 a.m. that day, the trader told his broker, “Don’t let ’em go down. For the eleven o’clock fix I need to lift 5s up,” he said, referring to the five-year swap spread trade. This is the trader who told the broker he could buy as much as $400 million in notional value of the swaps to move the benchmark.

…

That’s also known as banging the close — or, as a Barclays trader put it on March 7, 2007: “What happens at 11 is the bloody thing moves like half a basis point up and down because everybody’s trying to bang the screen.”

The obvious solution to the problem – if there is indeed a problem, which is by no means clear – is to lengthen the period of time over which the fix is calculated … if indeed a fix is really required at all. Another excellent option is to ensure that expiring contracts can be exchanged for physicals, rather than automatic cash settlement. But this isn’t about logic; this is all about asshole regulators and politicians making names for themselves.

You don’t believe me? Then I must assume you also don’t believe in proportionality:

Jamie Forese, head of the Citigroup Inc. unit that houses trading and investment banking, said fines the firm paid for rigging foreign-exchange markets dwarfed the amount generated by the illegal conduct.

Revenue from the trades amounted to about $1 million, while Citigroup paid out $2.5 billion in fines and penalties, Forese estimated Wednesday at an investor conference in New York.

However, one guy has been brave enough to bite back:

JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon took aim at U.S. Senator Elizabeth Warren, a critic of large banks, as he expressed broad concerns about leadership in Washington.

“I don’t know if she fully understands the global banking system,” Dimon, speaking Wednesday at an event in Chicago, said of the Massachusetts Democrat. Still, he said he agrees with some of her concerns about risks.

It looks like Lagarde isn’t the only one who wants to be a Fed governor:

The World Bank joined the IMF in urging the Federal Reserve to hold off raising rates until next year, citing an uneven U.S. recovery and the risks to emerging markets of tightening policy any sooner.

“My concern is that the signals coming out of the U.S. economy have been mixed,” World Bank Chief Economist Kaushik Basu told reporters Wednesday in Washington on a conference call to discuss the bank’s semiannual global economic forecasts.

A premature move by the Fed could cause the dollar to strengthen, which may slow the U.S. economy and sideswipe emerging and developing countries, he said.

The Washington-based development bank lowered its forecast for U.S. growth this year to 2.7 percent, from 3.2 percent in January. The bank also expects the U.S. to expand at a 2.8 percent pace next year, down from 3 percent in January.

And many sets of entrails are being examined:

Economists surveyed June 5-9 put the probability of a September increase in the benchmark federal funds rate at 50 percent, according to the median estimate. The odds were nine percent for October, 20 percent for December and 10 percent for some time in 2016.

Some investors making bets on interest-rate futures have a more hawkish view. The market-implied probability of liftoff by September is somewhere between 93 percent and 100 percent, according to Stan Jonas, who has been trading fed funds futures since he helped create them in 1988.

The Federal Open Market Committee gathers on June 16-17, and Chair Janet Yellen will hold a press conference after the meeting. Fed officials will also publish updated quarterly economic and interest-rate forecasts.

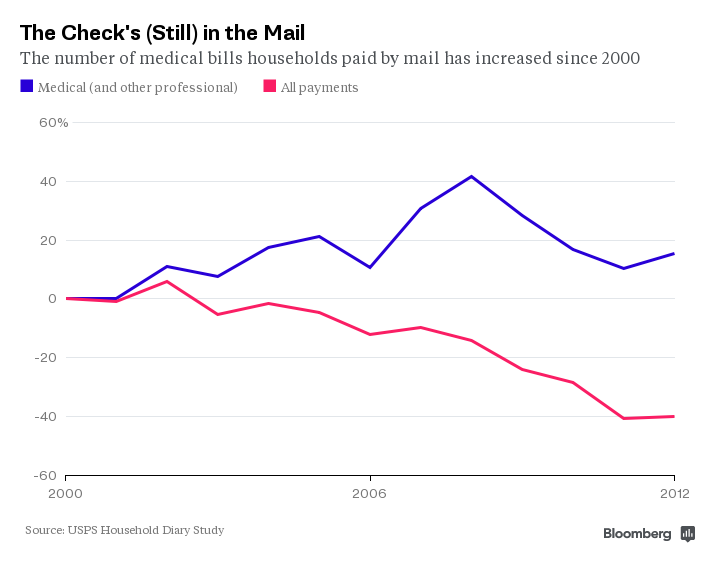

And, as some comic relief, Bloomberg presents a good story on medical billing:

Dealing with medical bills, like waiting for the cable guy or buying a used car, has become a cliché of consumer exasperation. Everything from electricity and phone bills to tax returns and parking tickets migrated to electronic payments years ago, but America’s $2.9 trillion health-care economy remains stubbornly stuck in the 1990s. The number of medical bills paid by paper check through the U.S. mail has even increased while payments for all other services have decreased dramatically. Medical payments are the only category to register an increase in paperwork since the start of the 21st century: [Chart]

It’s not just consumers who are paying by mail. Just 15 percent of commercial insurers make payments to medical providers electronically, according to a report last month from PricewaterhouseCoopers Health Research Institute. The largest insurers are usually the best at going digital, but Cigna, with 14.5 million customers, sends only 39 percent of payments electronically. That’s because many doctors aren’t signed up to receive electronic transfers, according to spokesman Joe Mondy. Aetna and UnitedHealth Group, in contrast, both say around 80 percent of payments are paperless.

Hospitals, medical offices, and insurance companies need an army of workers to push all that paper1increase click area, which is also frequently shuffled through middlemen like billing agencies2increase click area and clearinghouses3increase click area. One claims clearinghouse, Emdeon, which handles paper billing for many of its health plan clients, spent $87 million4increase click area on postage alone in the first three months of 2015—nearly a quarter of its total revenue—according to financial filings. All this bureaucracy pushed the cost of administering private insurance to $173 billion5increase click area in 2013, according to federal data.

Click for Big

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts gaining 1bp, FixedResets off 15bp and DeemedRetractibles up 6bp. The Performance Highlights table is of average length – given recent standards – and features ENB FixedReset losers and BAM FixedReset winners. Volume was on the high side of average.

PerpetualDiscounts now yield 5.09%, equivalent to 6.62% interest at the standard equivalency factor of 1.3x. Long corporates now yield about 4.1%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 250bp, a slight (and perhaps spurious) narrowing from the 255bp reported June 3.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

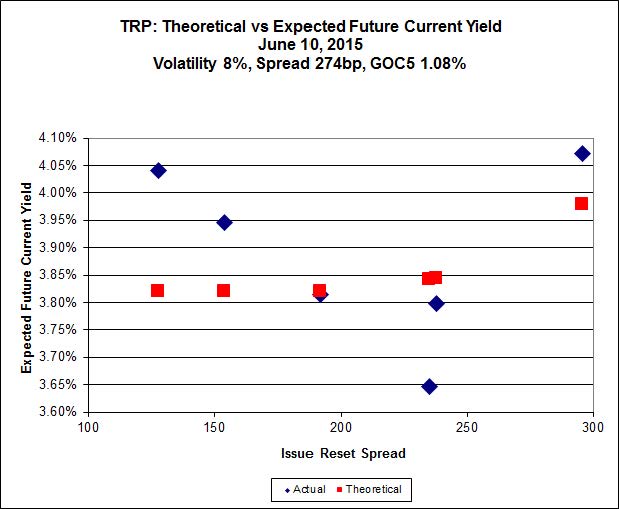

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 23.52 to be $1.19 rich, while TRP.PR.B, which will reset June 30 at 2.152% (+128), is $0.85 cheap at its bid price of 14.60

Click for Big

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule). It is clear that the lowest spread issue, MFC.PR.F, is well off the relationship defined by the other issues, but this doesn’t resolve the conundrum – it just makes it more conundrous.

Most expensive is MFC.PR.L, resetting at +216bp on 2019-6-19, bid at 23.27 to be $0.63 rich, while MFC.PR.H, resetting at +313bp on 2017-3-19, is bid at 25.46 to be $0.54 cheap.

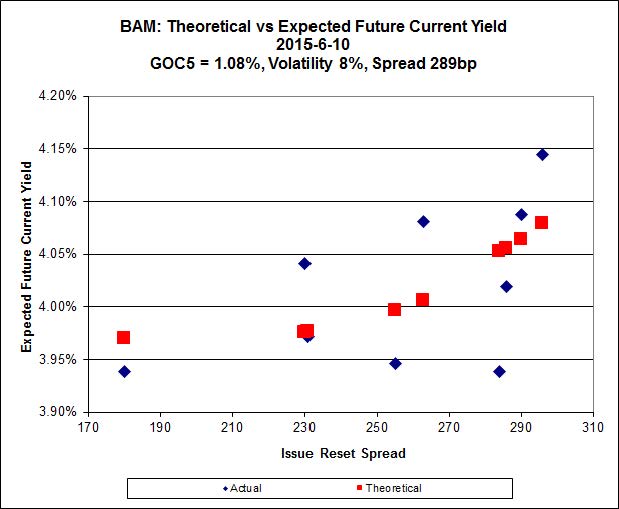

Click for Big

The cheapest issue relative to its peers is BAM.PF.B, resetting at +263bp on 2019-3-31, bid at 22.73 to be $0.42 cheap. BAM.PF.G, resetting at +284bp 2020-6-30 is bid at 24.88 and appears to be $0.70 rich.

Click for Big

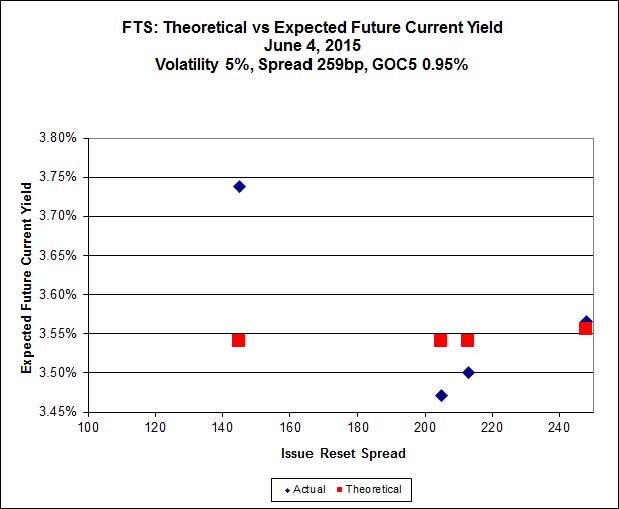

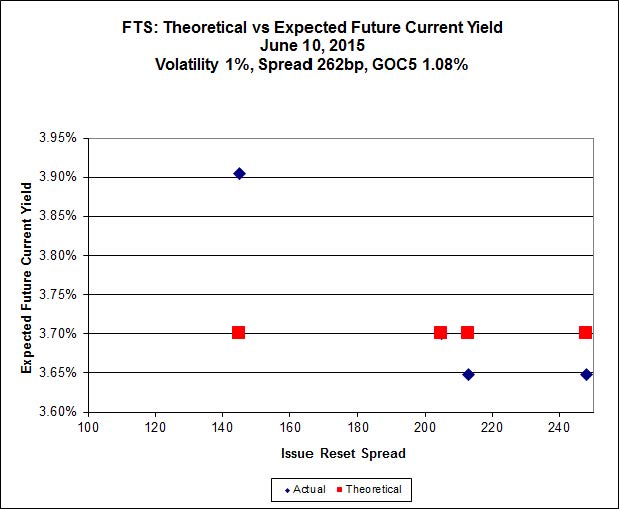

FTS.PR.H, with a spread of +145bp, and bid at 16.20, looks $0.89 cheap and resets 2020-6-1. FTS.PR.M, with a spread of +248bp and resetting 2019-12-1, is bid at 24.40 and is $0.35 rich.

Click for Big

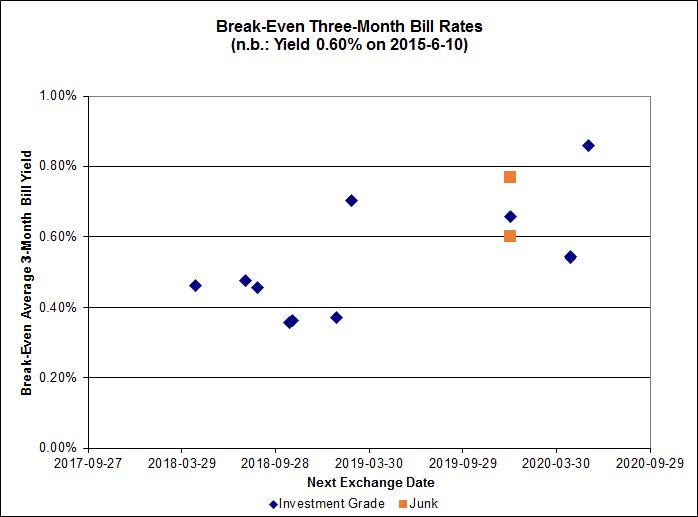

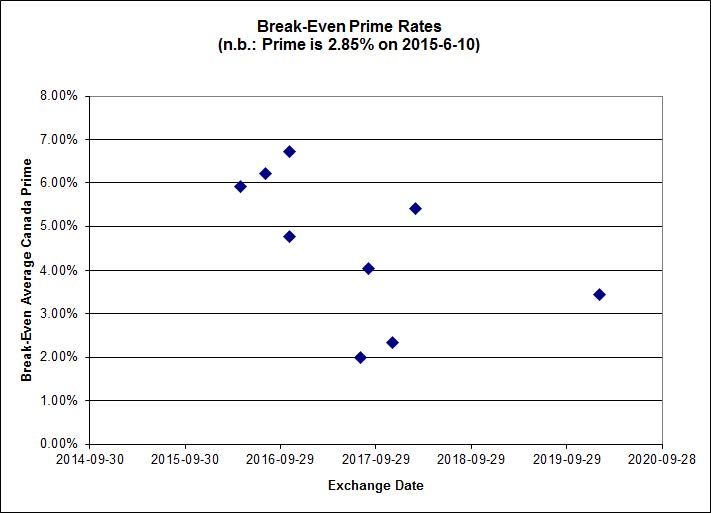

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of about 0.45%, with no ridiculous outliers. On the junk side, four out of the six pairs are outside the range of the graph: FFH.PR.E / FFH.PR.F at -1.22%; AIM.PR.A / AIM.PR.B at -0.09%; BRF.PR.A / BRF.PR.B at -0.48%; and DC.PR.B / DC.PR.D at -1.37%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0233 % | 2,197.4 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0233 % | 3,842.1 |

| Floater | 3.49 % | 3.54 % | 60,205 | 18.35 | 3 | -0.0233 % | 2,336.0 |

| OpRet | 4.44 % | -12.44 % | 28,675 | 0.08 | 2 | 0.0000 % | 2,782.9 |

| SplitShare | 4.60 % | 4.86 % | 71,862 | 3.30 | 3 | -0.1073 % | 3,241.4 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 2,544.7 |

| Perpetual-Premium | 5.46 % | 4.86 % | 62,784 | 4.94 | 19 | 0.1495 % | 2,513.3 |

| Perpetual-Discount | 5.07 % | 5.09 % | 113,344 | 15.34 | 15 | 0.0056 % | 2,762.0 |

| FixedReset | 4.47 % | 3.86 % | 248,669 | 16.46 | 87 | -0.1460 % | 2,366.4 |

| Deemed-Retractible | 5.01 % | 3.33 % | 110,958 | 0.70 | 34 | 0.0597 % | 2,620.4 |

| FloatingReset | 2.50 % | 2.89 % | 56,762 | 6.13 | 9 | 0.4783 % | 2,341.4 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| ENB.PF.A | FixedReset | -2.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-10 Maturity Price : 19.95 Evaluated at bid price : 19.95 Bid-YTW : 4.87 % |

| FTS.PR.K | FixedReset | -2.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-10 Maturity Price : 21.15 Evaluated at bid price : 21.15 Bid-YTW : 3.85 % |

| BAM.PR.K | Floater | -2.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-10 Maturity Price : 13.93 Evaluated at bid price : 13.93 Bid-YTW : 3.62 % |

| ENB.PF.G | FixedReset | -2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-10 Maturity Price : 20.16 Evaluated at bid price : 20.16 Bid-YTW : 4.87 % |

| ENB.PR.J | FixedReset | -1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-10 Maturity Price : 19.86 Evaluated at bid price : 19.86 Bid-YTW : 4.76 % |

| MFC.PR.N | FixedReset | -1.43 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.51 Bid-YTW : 4.34 % |

| ENB.PF.E | FixedReset | -1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-10 Maturity Price : 20.12 Evaluated at bid price : 20.12 Bid-YTW : 4.85 % |

| SLF.PR.G | FixedReset | -1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.11 Bid-YTW : 7.75 % |

| BMO.PR.W | FixedReset | -1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-10 Maturity Price : 22.45 Evaluated at bid price : 23.25 Bid-YTW : 3.57 % |

| TRP.PR.G | FixedReset | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-10 Maturity Price : 23.07 Evaluated at bid price : 24.81 Bid-YTW : 3.86 % |

| BAM.PR.X | FixedReset | 1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-10 Maturity Price : 18.28 Evaluated at bid price : 18.28 Bid-YTW : 4.21 % |

| BAM.PR.B | Floater | 1.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-10 Maturity Price : 14.66 Evaluated at bid price : 14.66 Bid-YTW : 3.44 % |

| BAM.PF.E | FixedReset | 1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-10 Maturity Price : 22.29 Evaluated at bid price : 23.00 Bid-YTW : 4.13 % |

| BAM.PF.G | FixedReset | 2.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-10 Maturity Price : 23.12 Evaluated at bid price : 24.88 Bid-YTW : 3.99 % |

| FTS.PR.I | FloatingReset | 3.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-10 Maturity Price : 16.00 Evaluated at bid price : 16.00 Bid-YTW : 3.22 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BNS.PR.M | Deemed-Retractible | 142,980 | Nesbitt crossed 28,800 at 25.47, then another 109,200 at 25.49. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-07-27 Maturity Price : 25.25 Evaluated at bid price : 25.45 Bid-YTW : 2.18 % |

| RY.PR.A | Deemed-Retractible | 139,529 | RBC crossed 50,000 at 25.18; Nesbitt crossed 85,000 at 25.23. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-07-10 Maturity Price : 25.00 Evaluated at bid price : 25.21 Bid-YTW : -3.21 % |

| TD.PF.C | FixedReset | 98,165 | Desjardins crossed 95,000 at 23.05. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-10 Maturity Price : 22.30 Evaluated at bid price : 23.00 Bid-YTW : 3.66 % |

| GWO.PR.Q | Deemed-Retractible | 65,906 | Nesbitt crossed 62,000 at 25.05. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.00 Bid-YTW : 5.14 % |

| RY.PR.N | Perpetual-Discount | 63,295 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-10 Maturity Price : 24.55 Evaluated at bid price : 24.94 Bid-YTW : 4.92 % |

| GWO.PR.I | Deemed-Retractible | 55,410 | Nesbitt crossed 54,600 at 22.86. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.81 Bid-YTW : 5.69 % |

| There were 38 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PR.K | Floater | Quote: 13.93 – 14.51 Spot Rate : 0.5800 Average : 0.3775 YTW SCENARIO |

| MFC.PR.M | FixedReset | Quote: 23.90 – 24.40 Spot Rate : 0.5000 Average : 0.3374 YTW SCENARIO |

| VNR.PR.A | FixedReset | Quote: 23.71 – 24.28 Spot Rate : 0.5700 Average : 0.4250 YTW SCENARIO |

| IFC.PR.C | FixedReset | Quote: 24.20 – 24.59 Spot Rate : 0.3900 Average : 0.2988 YTW SCENARIO |

| TRP.PR.C | FixedReset | Quote: 16.60 – 16.97 Spot Rate : 0.3700 Average : 0.2929 YTW SCENARIO |

| ENB.PR.B | FixedReset | Quote: 18.31 – 18.62 Spot Rate : 0.3100 Average : 0.2395 YTW SCENARIO |