There are some interesting statistics from electronic bond trading:

Traders trying to purchase investment-grade notes are failing about 46 percent of the time, close to the worst rate in more than four years as measured by activity on MarketAxess Holdings Inc.’s electronic platform. On the flip side, investors trying to sell the debt are having the easiest time on record, with an 85 percent success rate.

Bond buyers are showing an unwillingness to part with their holdings as a rally fueled by more than five years of unprecedented Federal Reserve stimulus refuses to die. Ironically, it’s harder than ever to find securities for sale even though the U.S. corporate-debt market has grown 53 percent since 2008, with companies selling $6.9 trillion of notes since then, according to data compiled by the Securities Industry and Financial Markets Association and Bloomberg.

“Right now, everyone’s a buyer,” said Edward Meigs, who manages $1.6 billion of debt assets at First Eagle Investment Management in Baltimore. “There’s a marked level of complacency.”

Traders will submit offers to buy or sell bonds on MarketAxess’s platform within a set period of time. The transaction is considered to fail when time runs out with no takers. New York-based MarketAxess is the most-active electronic venue for trading corporate bonds in the U.S.

And given the difficulty in buying bonds, guess what’s making a comeback?:

Commercial real-estate investor H/2 Capital Partners bundled a hodge podge of its holdings — from bonds tied to skyscrapers and malls to junk-rated bank loans — into about $400 million of securities. The deal, similar to the pre-crisis transactions known as collateralized debt obligations, included one portion that Moody’s Investors Service gave its highest rating of Aaa.

The investment firm is seizing on a revival of the types of transactions that fueled the property boom in 2006 and 2007, showing the lengths to which investors are going to bolster skimpy yields across credit markets. Such offerings are giving commercial-property investors a wider range of options to fund acquisitions, according to Richard Hill, a debt analyst at Morgan Stanley.

The war on markets continues:

U.S. Attorney General Eric Holder promised Congress a thorough investigation into whether high-frequency trading violates laws against insider trading.

Holder said he is responding to concerns being raised about whether the practice creates an uneven playing field for investors.

“The department is committed to ensuring the integrity of our financial markets, and we are determined to follow this investigation wherever the facts and the law may lead,” Holder said in testimony today at a hearing of the House Appropriations subcommittee that oversees the Justice Department.

With respect to my remarks about High Frequency Trading on April 3, Assiduous Reader PL writes in and says:

OK, I see your point. James you are like PT Barnum. But for you there is a sucker born every millisecond.

This is not strictly true. My objection to rules about spoofing and layering and all the other little tactical games that speculators play is twofold:

- They seek to protect speculators from the consequences of their own actions, and

- They are completely arbitrary

With respect to the first point – anybody who buys a stock at 20.55 simply because there’s a big bid at 20.50 is taking his chances. He is speculating and he knows he’s speculating. As a matter of public policy, there is no reason to worry over-much about the consequences that might befall speculators; speculators are of interest solely because they provide liquidity to real money players.

That big bid at 20.50 is valuable to real-money players seeking to sell – putting in a spoof order is a dangerous game and can easily blow up in the face of Mr. Clever if somebody else has a well timed pounce algorithm or otherwise hits that bid. Mr. Clever – whose actual goal is to sell a few shares at 20.55 – is now behind the eight-ball and has to sell more shares in order to break even. Mr. Clever has actually supplied liquidity to the market, which is exactly what speculators are supposed to do (although he might have to take some liquidity as he squares his books).

There will doubtless be a lot of whimpering about Granny and her purchase of 500 shares. I don’t really care much about Granny and her 500 shares, either. A stock exchange is life in the raw. If Granny wants professional management of her portfolio, she should hire a professional – last time I checked, there were still lots of them around. We do not insist that hospitals provide facilities and diagrams for amateur brain surgeons; why should we insist that stock exchanges provide a straight-forward and predictable environment for amateur stock traders? Granny’s best bet is an ETF, mutual fund or other arrangement to hire a professional to handle her investment needs.

The concern for Granny is all crocodile tears. It comes from incompetent institutional traders who simply aren’t very good at trading; who find themselves in a horrifying world where anybody – just anybody! – with a bit of capital and computer skills can eat their lunch. The controversy regarding HFT is fuelled by monopolists who are watching their monopoly erode and aren’t very happy about it.

The other point is regarding the arbitrary nature of the anti-spoofing, et cetera, rules and I will introduce that point by quoting again from the SEC press release I quoted on April 4:

“The fair and efficient functioning of the markets requires that prices of securities reflect genuine supply and demand,” said Sanjay Wadhwa, senior associate director of the SEC’s New York Regional Office. “Traders who pervert these natural forces by engaging in layering or some other form of manipulative trading invite close scrutiny from the SEC.”

This is total bullshit and reveals that Sanjay Wadhwa doesn’t have a clue about trading strategies (he’s only a lawyer-accountant – I see no evidence that he’s ever traded a single thing in his life. He is “nurturing” though, and golly, isn’t “nurturing” better than “competent” and “knowledgeable” nowadays?).

Genuine supply and demand? Spoofing works – when it does work! – because when there’s a big order on one side of the market, many speculators will back away from it, reasoning that whoever put that order in will end up moving the market (with more confidence, you can then take the orders that didn’t back away. It was exploitation of this behaviour that got Dondero into trouble – see April 4). So, for instance, if trader M. T. Head of Bozo Corp has an order to sell 10,000 shares of XYZ, the market may well evolve as follows:

- Market before Order: 21.50-60, 10×10

- Market immediately after order: 21.50-59, 10×100

- Market shortly after order: 21.40-59, 10×100

So after this happens a few times, Mr. Head wises up a little, and only puts in an order to sell 1,000 shares intending to feed the rest of his 10,000 shares into the market as he gets filled; so the market evolves like this:

- Market before Order: 21.50-60, 10×10

- Market immediately after order: 21.50-59, 10×10

- Market shortly after order: 21.50-59, 10×10

This has a couple of overall effects – spreads have narrowed (from a dime to nine cents) and execution sizes are reduced (since the 10,000 shares will be sold in pieces). In fact, this is exactly what we have seen in the market over the last twenty years.

But, to the chagrin of Sanjay Wadhwa of the SEC, the market prices no longer reflect genuine supply and demand! Oh, the horror! There is true supply of 10,000 shares, but only 1,000 shares are being advertised! Quick, to the lamp-posts! String up the social misfit of a trader who is keeping 9,000 shares secret! He is perverting the natural forces that Sanjay Wadhwa is sworn to defend!

The situation gets even more ridiculous when we remember that iceberg orders are institutionalized and available on many exchanges: M. T. Head could well have put in an iceberg order, giving the exchange an order for 10,000 shares with instructions to show only 1,000 shares at a time … and now it is the exchange that is perverting the natural forces of supply and demand. For some odd reason, Sanjay Wadhwa doesn’t seem particularly offended by this.

He does, however, have hysterics if M. T. Head takes another step to execute his client’s order at a good price, and puts in a spoof buy for 2,000 shares at 20.51, making the complete evolution of the market like this:

- Market before Order: 21.50-60, 10×10

- Market immediately after order: 21.50-59, 10×10

- Market shortly after order: 21.50-59, 10×10

- Market after spoof: 21.51-59, 20×10 ILLEGAL, ILLEGAL ILLEGAL!!! Call the gendarmes!

Mr. Head, as mentioned, is taking a bit of chance here, because his bid for 2,000 at 21.51 could get hit, and if it is he’s got 12,000 shares to sell instead of 10,000. But that’s his problem. But maybe it will work; somebody will see the big bid at 21.51 and consider this to be a good reason to buy 1,000 at 21.59; it’s the same principle as backing off on your orders when you see a big order on the other side. If M. T. Head’s good enough at the game his winnings will exceed his losses, he’ll get more clients and take home more money, which is exactly how the system should be working. In the mean-time, we observe that the spoof order increased market depth and decreased market spread. Why is this wrong? Regrettably, as discussed on April 4, this is exactly what got Joseph Dondero into trouble.

However, a good argument can be made that allowing spoofing will actually improve the market for naïve real money. As noted above, speculative bidders will drop their bids in the face of a large offer, believing that it is a naïve seller who will eventually execute at any price he can get (and vice versa for naïve buyers, of course). Along comes Granny, with her market order to sell 100 shares and hits one of those reduced bids and gets less money than she would have had there not been a large seller in the market at that time. If, however, spoofing is allowed, then there will be less certainty regarding the future course of prices, which should result in the speculative bidders not dropping their prices so much – or perhaps not dropping them at all. So the bid-offer spread is not so adversely impacted and Granny gets a better price. Isn’t that good? There’s no evidence that I know of that this will actually be the case; but there is no evidence I know of that it doesn’t, either; it would be interesting to see a few controlled experiments, but the SEC is more interested in grandstanding.

Another example of supply-and-demand uncertainty is a case where I have a client who has 10,000 shares of XYZ and 10,000 shares of ABC, both of which are trading around $20, which – as far as I can tell – is fair value. My client asks me to raise $20,000 because he wants to buy a car. So, wishing to do the best for my client, I put in two orders:

- Sell 1,000 XYZ at 20.10, and

- Sell 1,000 ABC at 20.10

Two orders! I’m trying to do the best for my client and get him the best price possible … if I get can sell 1,000 shares at 20.10, he’ll have $100 more than if he sold them at $20.00 … maybe $100 isn’t all that much, but given the choice between $100 in my client’s pocket and $100 in somebody else’s client’s pocket, I know what I like best – and it’s my job to get best execution for my client.

I’m taking a bit of a chance: maybe both offers will get lifted, I’ll have raised too much money, and I’ll have to reinvest the excess, possibly taking a loss on that part of the transaction. Well – that’s my problem. It’s my job to take calculated risks on behalf of my clients – isn’t that what investment is all about? – and in my judgement, for this package of transactions, given market conditions and my evaluation of fair value, this is a calculated risk worth taking.

“But”, shrieks Sanjay Wadhwa, spittle dribbling from his chin, “what about the Holy Supply and Demand? You are putting offers for 2,000 shares on the market when you really only wanting to supply 1,000 shares! Evil, evil, evil! To the lamp-posts!”

So I have to explain that there’s nothing actually illegal about my actions; they happen to be on the right side of an idiotic arbitrary line.

So the result of these precious little anti-spoofing rules are:

- increased spreads

- decreased depth

- lots of arbitrary rules for traders to remember

- lots of employment for lawyers, accountants, lawyer-accountants and other box-tickers to enforce these rules

- the occasional ‘Gotcha!’ when the authorities find a technical violation and decide to enforce these rules

You don’t believe in ‘Gotcha!’? Ask David Berry about ‘Gotcha!’. He only got off because (i) He had enough money to fight the case, and (ii) There was enough at stake to make it worthwhile fighting the case. Ask Fabulous Fab about ‘Gotcha!’.

It’s a pretty screwy system, if you ask me.

Rob Carrick of the Globe wrote an article recently titled Real estate or stocks – which will make you richer?, concluding that as an investment, stocks are better, based in part on the following figures:

Canadian Real-Estate

vs.

Canadian Equities |

Period Ending

2013-12-31 |

S&P/TSX Composite Total Return Index |

National Average Resale Housing Price |

| 10 Years |

7.97% |

5.4% |

| 20 Years |

8.28% |

4.5% |

| 30 Years |

8.52% |

5.5% |

He also notes that:

Property taxes, furnishings, maintenance, improvements, insurance and mortgage interest all have to be factored into calculations of how much money is being made on housing.

There’s also a cost to investing, of course. But it’s much more contained and predictable than a house, where costly repairs could be needed at any time. A do-it-yourself investor might pay 0.5 per cent of the value of her account assets in fees and commissions per year, while an investor with an adviser might pay 1 to 1.5 per cent. Even if you lower stock market returns by this amount, you still get a better result than housing.

He neglected to factor in taxes, but this was addressed in the comments. I’ll also point out that national average housing price figures are suspect due to quality improvements.

In the end, I take the view that a house is not an investment. It’s a place to live. All in, if owning makes sense for you – i.e, you can afford it, you have enough stability in your life that you can settle down, that sort of thing – you should own. Then you can paint when you feel like painting. In the long run, house prices aren’t going to appreciate more than people’s salaries improve, although one might get fancy and specify that the price of a house in your price bracket will appreciate according to the improvement in salaries of the people who can afford to buy it, which is a much different thing what with income inequality and all. I have a friend who bought an entry level condo ten years ago, visions of immense riches dancing in her eyes … she’s now sold it in disgust, as it has appreciated in price by about as much as the improvement in salaries of people who buy entry level condos, which ain’t much.

The big value to a house, as far as I can tell, is that the mortgage represents forced saving. Every month you pay $1,500 on your mortgage, $1,000 of that is reducing principal and represents saving; by the time you’ve done this for 25 years, you have something worth having, especially since you’ve kept pace with inflation – however defined – on the entire value. Mind you, that might be an old-fashioned thought, nowadays, what with people taking out lines of credit … it’s even easier than selling part of your portfolio when you need some cash for something important.

DBRS confirmed BCE at Pfd-3(high):

It should be noted that BCE’s ratings are based primarily on the ratings of Bell Canada and reflect the structural subordination of debt (currently none outstanding) and its preferred share obligations relative to Bell Canada.

…

In terms of financial profile, DBRS expects Bell Canada’s leverage to be appropriate for the current rating category by mid-2015, following modest debt reduction and low-single-digit growth in EBITDA. DBRS expects Bell Canada to use the majority of its free cash flow and ~$700 million of proceeds from the Astral divestitures toward spectrum auction purchases and debt reduction. As such, DBRS forecasts Bell Canada’s gross debt-to-EBITDA will stand at approximately 2.1x at the end of 2014. DBRS continues to expect the Company to reduce its gross debt-to-EBITDA ratio to below 2.0x by mid-2015. DBRS notes that failure by Bell Canada to deleverage as expected could result in a negative rating action.

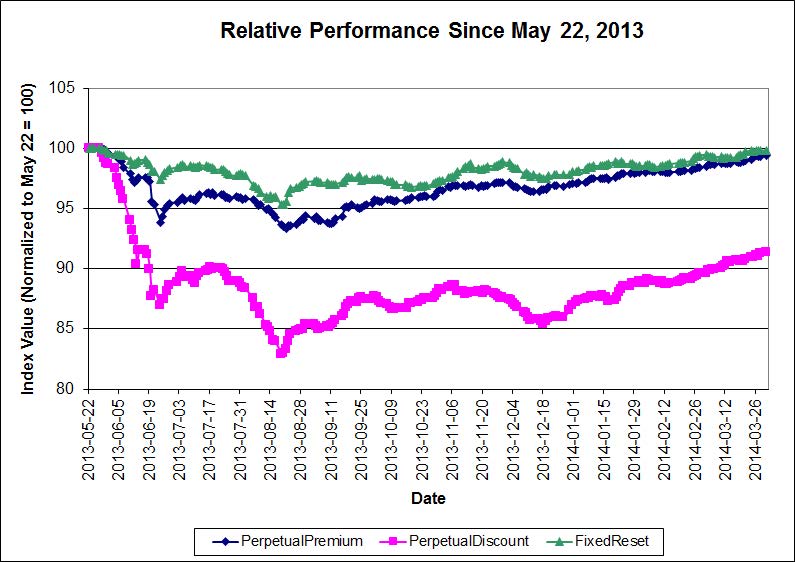

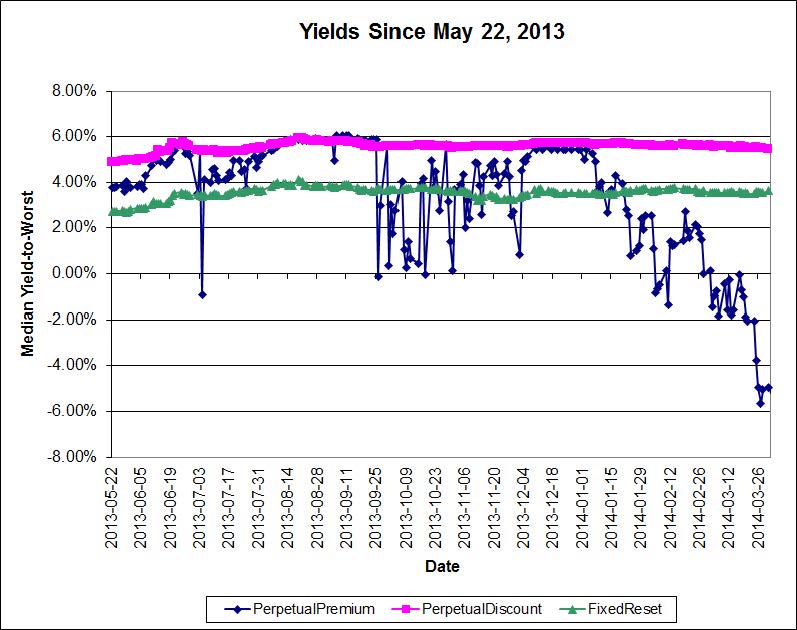

It was a positive day for the Canadian preferred share market, with PerpetualDiscounts up 8bp, FixedResets winning 11bp and DeemedRetractibles gaining 5bp. Volatility was modest. Volume was low.

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0000 % |

2,477.0 |

| FixedFloater |

4.67 % |

3.96 % |

36,409 |

17.47 |

1 |

0.5435 % |

3,635.3 |

| Floater |

2.94 % |

3.06 % |

50,058 |

19.61 |

4 |

0.0000 % |

2,674.5 |

| OpRet |

4.37 % |

-3.60 % |

32,841 |

0.15 |

2 |

-0.0387 % |

2,690.0 |

| SplitShare |

4.81 % |

4.35 % |

63,904 |

4.26 |

5 |

0.0636 % |

3,088.1 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.0387 % |

2,459.8 |

| Perpetual-Premium |

5.56 % |

-3.08 % |

102,359 |

0.09 |

13 |

0.1989 % |

2,381.4 |

| Perpetual-Discount |

5.45 % |

5.44 % |

122,165 |

14.66 |

23 |

0.0788 % |

2,472.9 |

| FixedReset |

4.69 % |

3.64 % |

204,925 |

4.21 |

79 |

0.1084 % |

2,526.2 |

| Deemed-Retractible |

5.04 % |

1.45 % |

149,191 |

0.14 |

42 |

0.0471 % |

2,482.7 |

| FloatingReset |

2.64 % |

2.45 % |

185,058 |

4.29 |

5 |

0.1601 % |

2,467.9 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| GWO.PR.N |

FixedReset |

-1.02 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.37

Bid-YTW : 4.39 % |

| PWF.PR.T |

FixedReset |

1.05 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2019-01-31

Maturity Price : 25.00

Evaluated at bid price : 25.94

Bid-YTW : 3.31 % |

| VNR.PR.A |

FixedReset |

1.07 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2017-10-15

Maturity Price : 25.00

Evaluated at bid price : 25.36

Bid-YTW : 3.90 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| TRP.PR.A |

FixedReset |

63,140 |

Nesbitt crossed 49,100 at 23.53.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-04-07

Maturity Price : 22.72

Evaluated at bid price : 23.35

Bid-YTW : 3.91 % |

| ENB.PR.N |

FixedReset |

57,925 |

TD crossed 50,000 at 24.95.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2018-12-01

Maturity Price : 25.00

Evaluated at bid price : 24.93

Bid-YTW : 4.18 % |

| TD.PR.P |

Deemed-Retractible |

56,520 |

RBC crossed 49,900 at 26.11.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-05-07

Maturity Price : 25.75

Evaluated at bid price : 26.03

Bid-YTW : -11.63 % |

| TRP.PR.B |

FixedReset |

53,890 |

Nesbitt crossed 50,000 at 20.27.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-04-07

Maturity Price : 20.30

Evaluated at bid price : 20.30

Bid-YTW : 3.80 % |

| MFC.PR.K |

FixedReset |

52,900 |

Nesbitt crossed 50,000 at 24.88.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2018-09-19

Maturity Price : 25.00

Evaluated at bid price : 24.90

Bid-YTW : 3.96 % |

| ENB.PR.D |

FixedReset |

46,800 |

TD crossed 40,000 at 24.34.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-04-07

Maturity Price : 23.00

Evaluated at bid price : 24.32

Bid-YTW : 4.15 % |

| There were 20 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| TD.PR.I |

FixedReset |

Quote: 25.28 – 25.72

Spot Rate : 0.4400

Average : 0.2585

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-07-31

Maturity Price : 25.00

Evaluated at bid price : 25.28

Bid-YTW : 1.44 % |

| ELF.PR.H |

Perpetual-Discount |

Quote: 24.45 – 24.81

Spot Rate : 0.3600

Average : 0.2167

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-04-07

Maturity Price : 24.04

Evaluated at bid price : 24.45

Bid-YTW : 5.63 % |

| GWO.PR.Q |

Deemed-Retractible |

Quote: 24.08 – 24.38

Spot Rate : 0.3000

Average : 0.1870

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.08

Bid-YTW : 5.65 % |

| CM.PR.E |

Perpetual-Premium |

Quote: 25.35 – 25.60

Spot Rate : 0.2500

Average : 0.1527

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-05-07

Maturity Price : 25.00

Evaluated at bid price : 25.35

Bid-YTW : -15.03 % |

| GWO.PR.N |

FixedReset |

Quote: 22.37 – 22.64

Spot Rate : 0.2700

Average : 0.1759

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.37

Bid-YTW : 4.39 % |

| IAG.PR.F |

Deemed-Retractible |

Quote: 25.92 – 26.19

Spot Rate : 0.2700

Average : 0.1957

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2018-03-31

Maturity Price : 25.25

Evaluated at bid price : 25.92

Bid-YTW : 5.16 % |