Here’s another reason why bubbles are bad:

When the housing market was hot, from the late 1990s to 2006, there were many good jobs that didn’t require a college education. For a certain kind of high school grad, paying tuition started looking like a dodgy proposition.

Then the boom went bust.

For one reason or another, the young construction workers and sales agents who skipped college to enter the workforce never went back, opening a schism between the boom-time workers and the college-going generation that came of age after the economy went splat.

That’s the story sketched out in a new working paper, published by National Bureau of Economic Research, from professors Kerwin Kofi Charles and Erik Hurst at the University of Chicago and Matthew Notowidigdo of Northwestern University. The three used Census Bureau, Department of Education, and Labor Department data to track what they call “college attainment” through the housing cycle.

The NBER wants five bucks for the paper. Good luck with that.

The best economic news all year is the agreement on the TPP:

A free-trade deal that opens a small part of the Canadian dairy market to cheaper foreign imports could spell the beginning of the end for the country’s dairy supply management system, and push inefficient farmers out of business, observers say.

The Trans-Pacific Partnership (TPP) deal, a trade pact among 12 countries including Japan, Vietnam and Australia that was reached in Atlanta on Monday, will give foreign dairy producers access to 3.25 per cent of the Canadian market while increasing duty-free access for Canada’s agricultural exports.

The deal was welcomed by large swaths of the agriculture sector, including pork and beef producers and grain farmers, who expect to see new demand for their goods overseas. But the negative effects are expected to be disproportionately felt by Canada’s dairy farmers, who face the prospect of cheaper foreign competition and the gradual erosion of prices paid by the large food companies that make cheese, butter and milk.

Now to get it ratified…

It was a decent day for the Canadian preferred share market, with PerpetualDiscounts gaining 28bp, FixedResets off 2bp and DeemedRetractibles down 4bp. The Performance Highlights table is skewed towards winners. Volume was average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

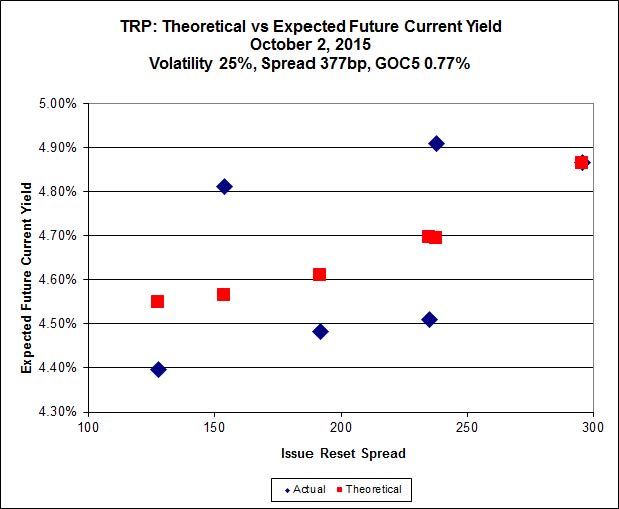

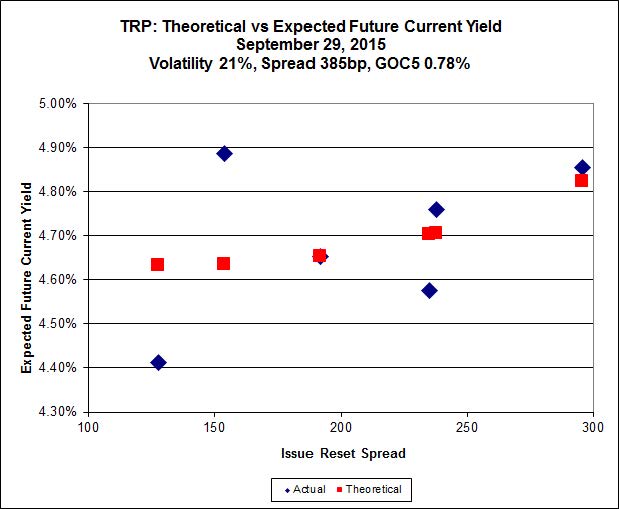

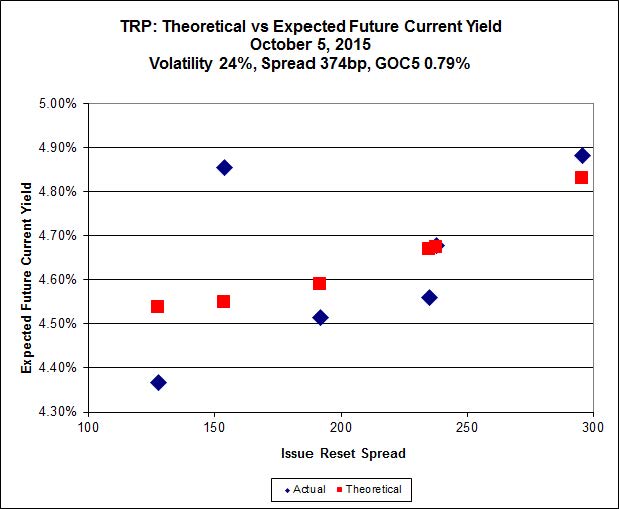

Here’s TRP:

Click for Big

Implied Volatility remained at an unreasonable level today.

TRP.PR.B, which resets 2020-6-30 at +128, is bid at 11.85 to be $0.44 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.81 cheap at its bid price of 12.00.

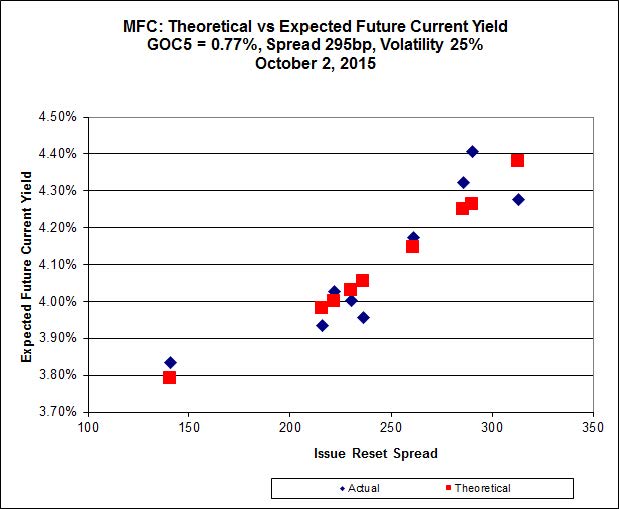

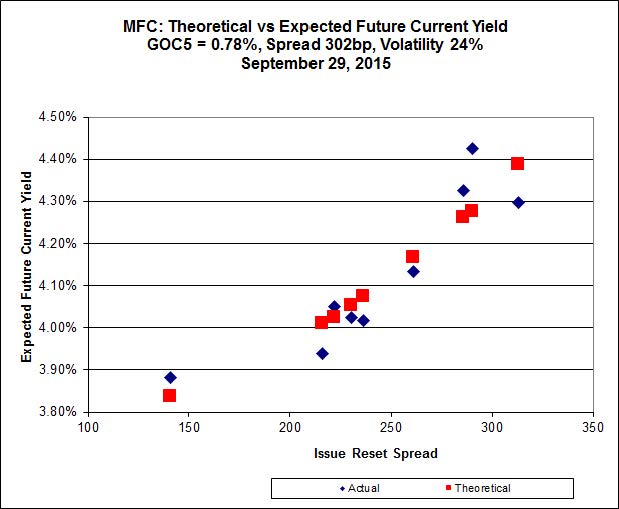

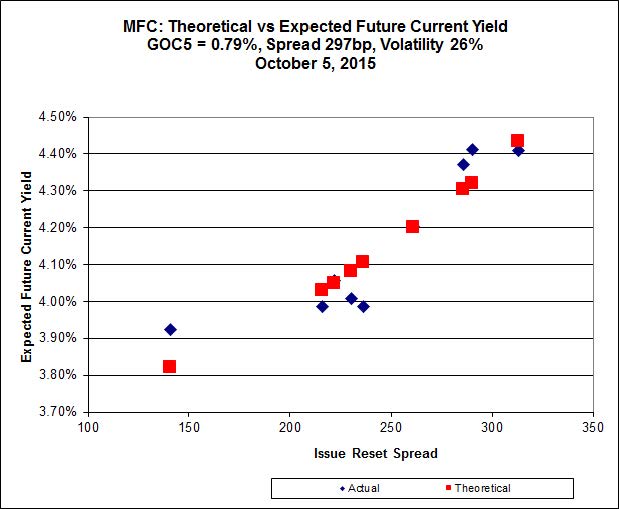

Click for Big

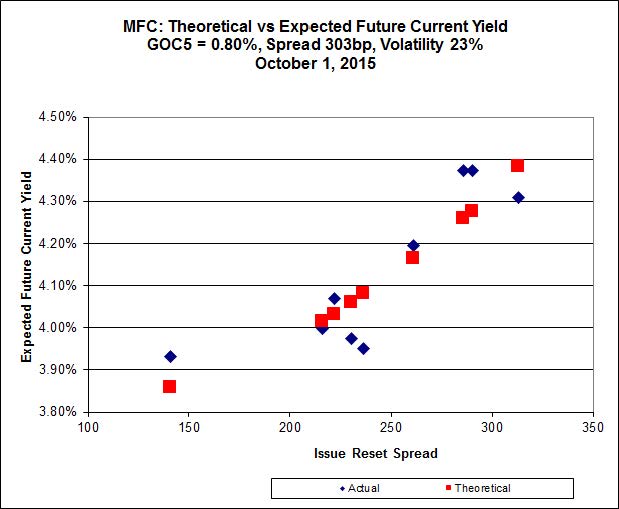

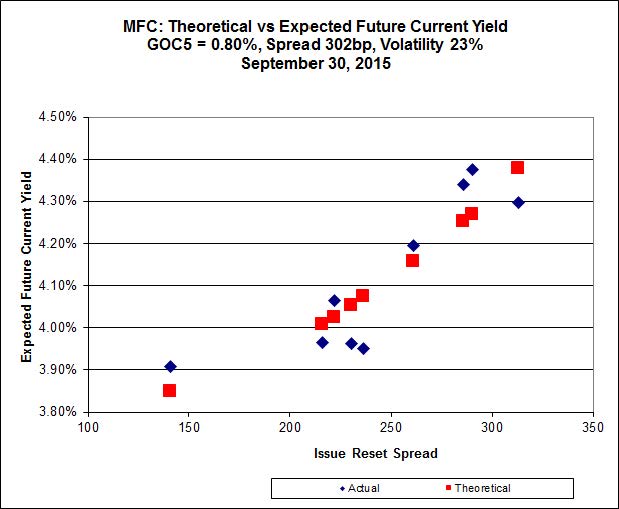

Another good fit today for MFC, with Implied Volatility climbing a bit.

Most expensive is MFC.PR.M, resetting at +236bp on 2019-12-19, bid at 19.75 to be 0.56 rich, while MFC.PR.G resetting at +280bp on 2016-12-19, is bid at 20.91 to be 0.44 cheap.

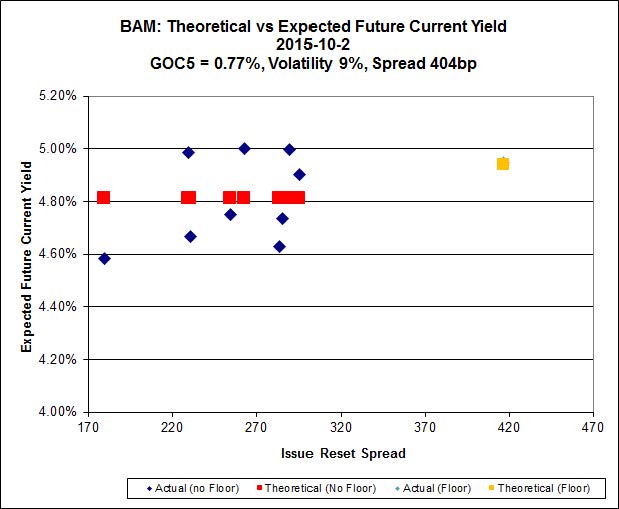

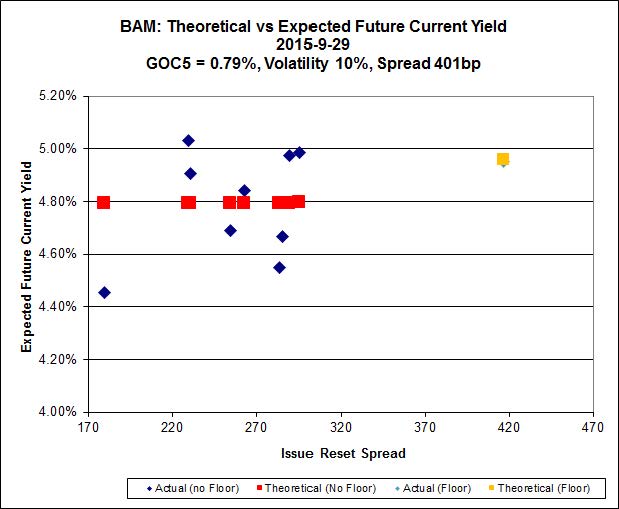

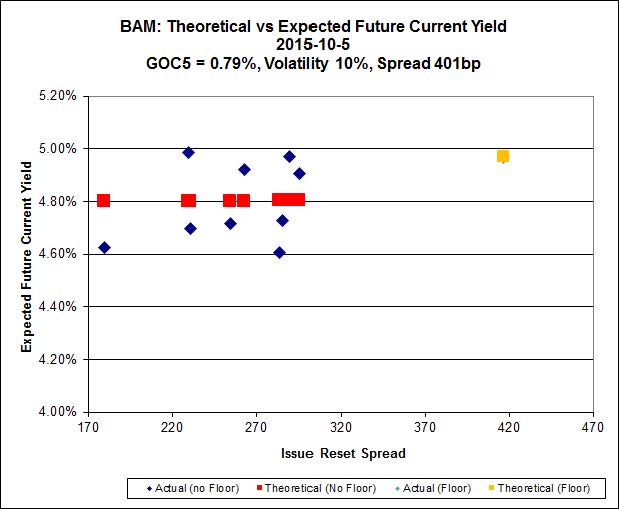

Click for Big

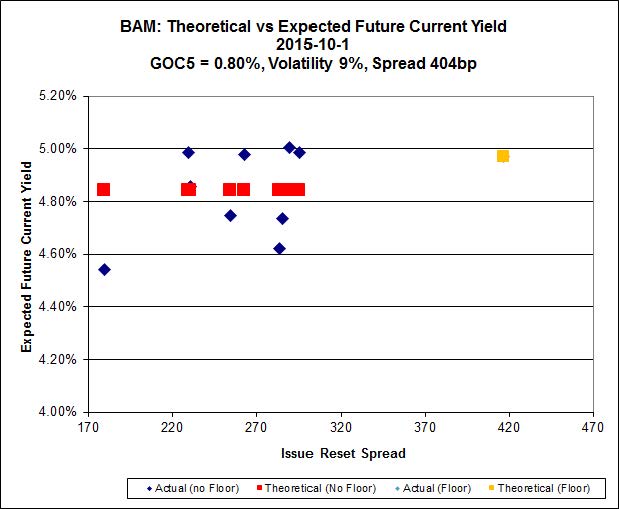

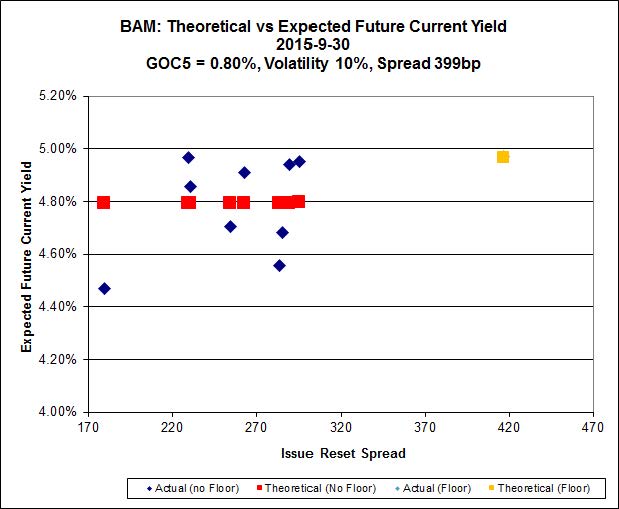

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PF.A, resetting at +290bp on 2018-9-30, bid at 18.56 to be $0.65 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 19.70 and appears to be $0.80 rich.

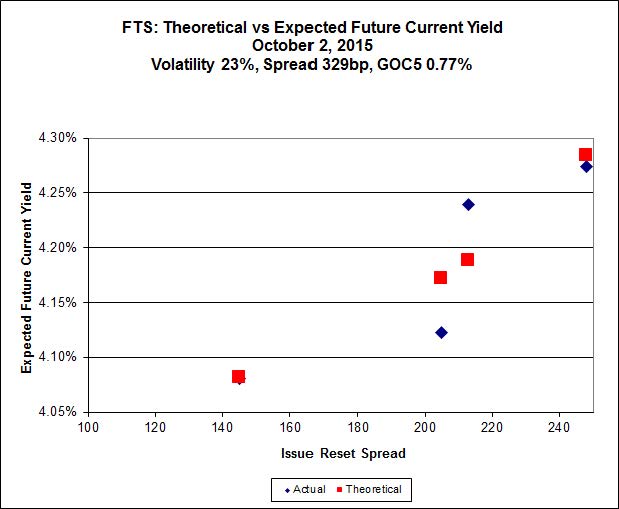

Click for Big

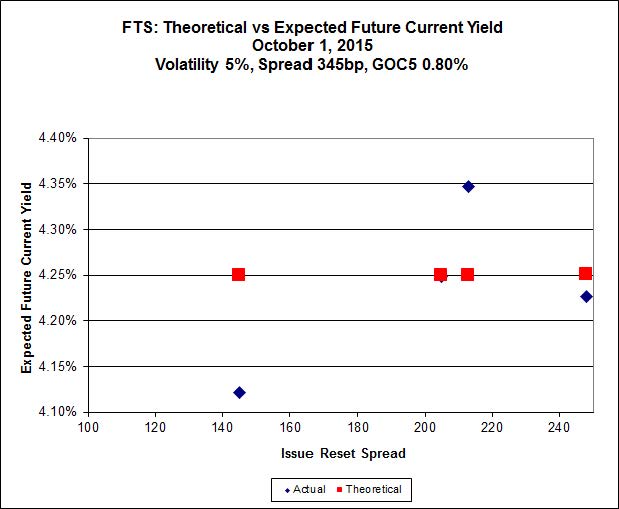

Implied Volatility leaped upwards again today, from an unreasonably high level to a ridiculously high level.

FTS.PR.K, with a spread of +205bp, and bid at 17.32, looks $0.35 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 17.04 and is $0.30 cheap.

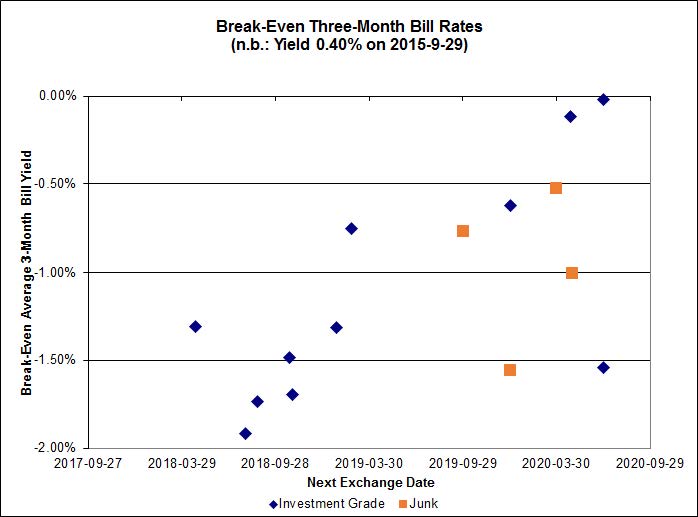

Click for Big

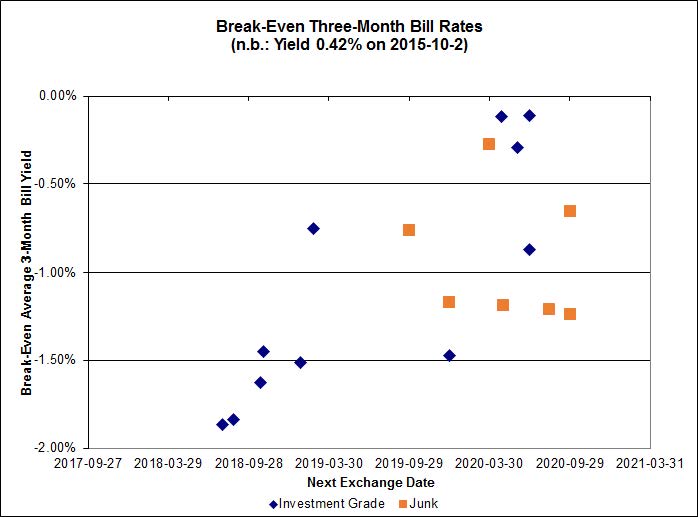

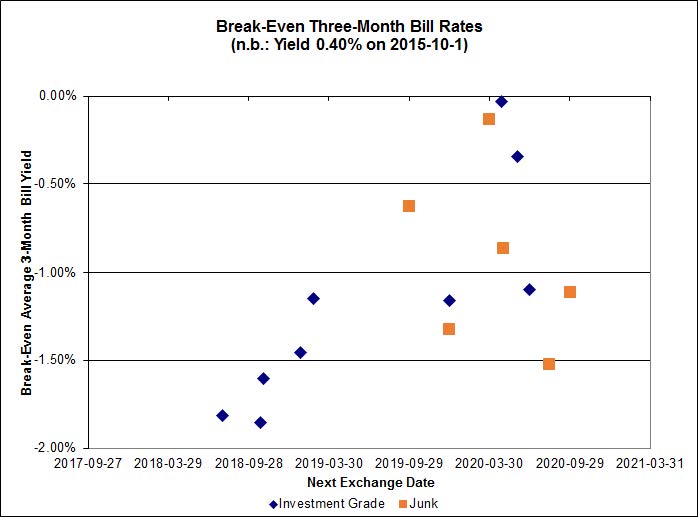

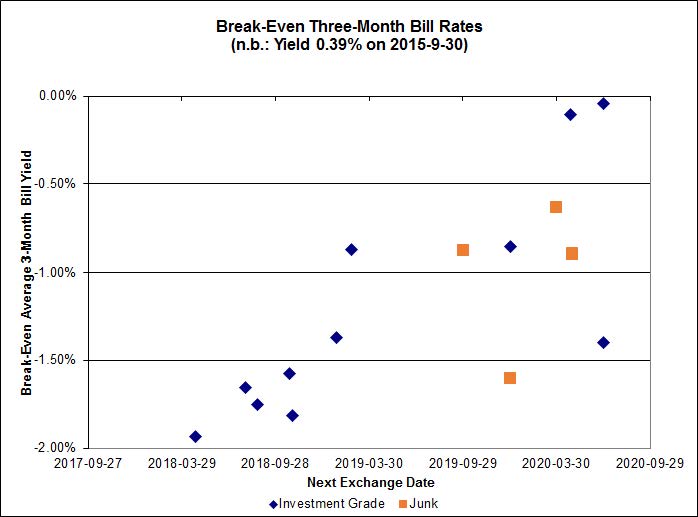

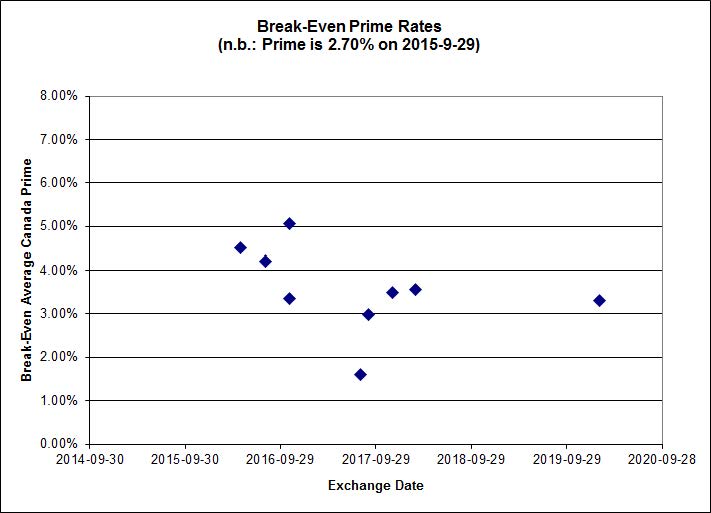

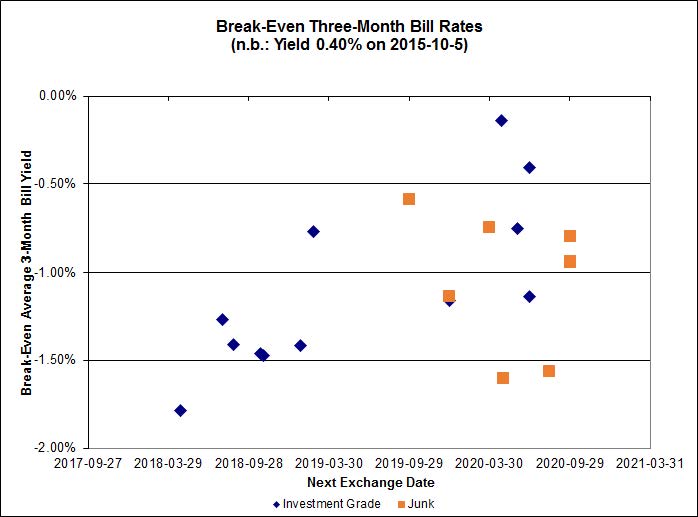

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.10%, with no outliers. The distribution is bimodal, with bank NVCC non-compliant pairs averaging -1.37% and other issues averaging -0.72%. There are three junk outliers above 0.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.3399 % | 1,582.1 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.3399 % | 2,766.2 |

| Floater | 4.70 % | 4.74 % | 63,423 | 16.00 | 3 | -1.3399 % | 1,681.8 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3012 % | 2,761.7 |

| SplitShare | 4.34 % | 4.96 % | 67,257 | 3.01 | 5 | 0.3012 % | 3,236.5 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3012 % | 2,525.3 |

| Perpetual-Premium | 5.82 % | 5.82 % | 55,817 | 13.87 | 5 | 0.2704 % | 2,472.8 |

| Perpetual-Discount | 5.69 % | 5.78 % | 74,297 | 14.21 | 33 | 0.2760 % | 2,497.5 |

| FixedReset | 5.18 % | 4.77 % | 185,711 | 15.18 | 76 | -0.0179 % | 1,965.9 |

| Deemed-Retractible | 5.25 % | 5.16 % | 98,237 | 5.49 | 33 | -0.0398 % | 2,537.8 |

| FloatingReset | 2.65 % | 4.65 % | 63,206 | 5.84 | 9 | 0.2415 % | 2,058.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| PWF.PR.T | FixedReset | -5.64 % | Not real. The issue traded 4,613 shares today in a range of 22.00-32 before closing at 20.76-22.09, 2×2. I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 20.76 Evaluated at bid price : 20.76 Bid-YTW : 4.09 % |

| MFC.PR.H | FixedReset | -2.50 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.23 Bid-YTW : 5.64 % |

| SLF.PR.J | FloatingReset | -2.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.91 Bid-YTW : 9.88 % |

| SLF.PR.H | FixedReset | -1.92 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.35 Bid-YTW : 7.78 % |

| BAM.PR.B | Floater | -1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 10.01 Evaluated at bid price : 10.01 Bid-YTW : 4.75 % |

| BNS.PR.P | FixedReset | -1.77 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.85 Bid-YTW : 3.86 % |

| BIP.PR.A | FixedReset | -1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 20.10 Evaluated at bid price : 20.10 Bid-YTW : 5.50 % |

| BAM.PR.K | Floater | -1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 10.15 Evaluated at bid price : 10.15 Bid-YTW : 4.69 % |

| CM.PR.Q | FixedReset | -1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 19.70 Evaluated at bid price : 19.70 Bid-YTW : 4.56 % |

| CU.PR.C | FixedReset | -1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 4.34 % |

| PWF.PR.P | FixedReset | -1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 14.30 Evaluated at bid price : 14.30 Bid-YTW : 4.31 % |

| FTS.PR.M | FixedReset | -1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 4.66 % |

| MFC.PR.F | FixedReset | -1.34 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.02 Bid-YTW : 9.67 % |

| RY.PR.L | FixedReset | -1.24 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.71 Bid-YTW : 4.22 % |

| GWO.PR.G | Deemed-Retractible | -1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.89 Bid-YTW : 6.47 % |

| GWO.PR.I | Deemed-Retractible | -1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.80 Bid-YTW : 7.04 % |

| BMO.PR.M | FixedReset | -1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.51 Bid-YTW : 4.05 % |

| BAM.PF.G | FixedReset | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 19.70 Evaluated at bid price : 19.70 Bid-YTW : 4.92 % |

| CU.PR.H | Perpetual-Discount | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 22.87 Evaluated at bid price : 23.25 Bid-YTW : 5.73 % |

| BAM.PF.A | FixedReset | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 18.56 Evaluated at bid price : 18.56 Bid-YTW : 5.19 % |

| RY.PR.N | Perpetual-Discount | 1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 22.69 Evaluated at bid price : 23.04 Bid-YTW : 5.28 % |

| ELF.PR.F | Perpetual-Discount | 1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 22.60 Evaluated at bid price : 22.85 Bid-YTW : 5.81 % |

| BMO.PR.Y | FixedReset | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 20.15 Evaluated at bid price : 20.15 Bid-YTW : 4.42 % |

| FTS.PR.K | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 17.32 Evaluated at bid price : 17.32 Bid-YTW : 4.46 % |

| W.PR.H | Perpetual-Discount | 1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 22.22 Evaluated at bid price : 22.50 Bid-YTW : 6.13 % |

| GWO.PR.Q | Deemed-Retractible | 1.32 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.08 Bid-YTW : 6.30 % |

| BAM.PF.E | FixedReset | 1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 17.71 Evaluated at bid price : 17.71 Bid-YTW : 5.14 % |

| RY.PR.O | Perpetual-Discount | 1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 22.73 Evaluated at bid price : 23.08 Bid-YTW : 5.27 % |

| ELF.PR.H | Perpetual-Discount | 1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 23.25 Evaluated at bid price : 23.65 Bid-YTW : 5.82 % |

| BMO.PR.T | FixedReset | 1.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 18.79 Evaluated at bid price : 18.79 Bid-YTW : 4.32 % |

| TRP.PR.B | FixedReset | 1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 11.85 Evaluated at bid price : 11.85 Bid-YTW : 4.44 % |

| TD.PF.D | FixedReset | 1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 20.33 Evaluated at bid price : 20.33 Bid-YTW : 4.48 % |

| TD.PR.T | FloatingReset | 1.81 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.90 Bid-YTW : 4.26 % |

| TRP.PR.F | FloatingReset | 2.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 12.85 Evaluated at bid price : 12.85 Bid-YTW : 4.54 % |

| BAM.PF.B | FixedReset | 2.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 17.38 Evaluated at bid price : 17.38 Bid-YTW : 5.19 % |

| IFC.PR.A | FixedReset | 2.55 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.10 Bid-YTW : 8.77 % |

| FTS.PR.H | FixedReset | 3.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 14.05 Evaluated at bid price : 14.05 Bid-YTW : 4.14 % |

| HSE.PR.E | FixedReset | 4.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 22.07 Evaluated at bid price : 22.60 Bid-YTW : 4.86 % |

| TRP.PR.D | FixedReset | 5.61 % | Simply a reversal of Friday‘s nonsense. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 16.94 Evaluated at bid price : 16.94 Bid-YTW : 4.92 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BAM.PF.H | FixedReset | 189,650 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 23.14 Evaluated at bid price : 24.97 Bid-YTW : 4.93 % |

| BAM.PR.B | Floater | 152,937 | Desjardins crossed 125,500 at 10.11. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 10.01 Evaluated at bid price : 10.01 Bid-YTW : 4.75 % |

| BAM.PR.K | Floater | 130,304 | Desjardins crossed 123,400 at 10.32. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 10.15 Evaluated at bid price : 10.15 Bid-YTW : 4.69 % |

| RY.PR.P | Perpetual-Discount | 42,185 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 24.05 Evaluated at bid price : 24.41 Bid-YTW : 5.40 % |

| BMO.PR.W | FixedReset | 35,340 | TD crossed 18,000 at 18.42. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 18.26 Evaluated at bid price : 18.26 Bid-YTW : 4.41 % |

| TRP.PR.D | FixedReset | 30,544 | Scotia crossed 13,800 at 16.65. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-05 Maturity Price : 16.94 Evaluated at bid price : 16.94 Bid-YTW : 4.92 % |

| There were 35 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| PWF.PR.T | FixedReset | Quote: 20.76 – 22.09 Spot Rate : 1.3300 Average : 0.8123 YTW SCENARIO |

| SLF.PR.H | FixedReset | Quote: 17.35 – 17.84 Spot Rate : 0.4900 Average : 0.3403 YTW SCENARIO |

| MFC.PR.H | FixedReset | Quote: 22.23 – 22.69 Spot Rate : 0.4600 Average : 0.3320 YTW SCENARIO |

| MFC.PR.F | FixedReset | Quote: 14.02 – 14.41 Spot Rate : 0.3900 Average : 0.2631 YTW SCENARIO |

| GWO.PR.G | Deemed-Retractible | Quote: 22.89 – 23.35 Spot Rate : 0.4600 Average : 0.3424 YTW SCENARIO |

| BMO.PR.M | FixedReset | Quote: 23.51 – 23.95 Spot Rate : 0.4400 Average : 0.3281 YTW SCENARIO |