Brookfield Office Properties Inc., a subsidiary of Brookfield Property Partners, has announced:

the completion of its previously announced Preferred Shares, Series CC issue in the amount C$200 million. The offering was underwritten by a syndicate of underwriters led by TD Securities Inc., CIBC Capital Markets, RBC Capital Markets and Scotiabank. On April 18, 2016, the syndicate agreed to purchase 6,000,000 Preferred Shares, Series CC at C$25.00 per share and has since exercised its option in full to purchase an additional 2,000,000 shares at the same offering price.

The Preferred Shares, Series CC will yield 6.00% annually for the initial period ending June 30, 2021. Net proceeds from the issue will be added to the general funds of Brookfield Office Properties and be used for general corporate purposes, including, but not limited to, redemption of existing preferred shares, repayment of revolving debt, acquisitions, capital expenditures and working capital needs.

The Preferred Shares, Series CC will commence trading on the Toronto Stock Exchange on April 27, 2016 under the ticker symbol BPO.PR.C.

BPO.PR.C is a FixedReset, 6.00%+518M600, announced April 18. The issue will be tracked by HIMIPref™ but relegated to the Scraps index on credit concerns.

The issue traded 898,337 shares today (consolidated exchanges) in a range of 25.10-25 before closing at 25.18-21, 26×25. This is reasonably close to the expected value, given that the TXPL total return index returned +1.45% from April 18 to April 27. Vital statistics are:

| BPO.PR.C | FixedReset | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-06-30 Maturity Price : 25.00 Evaluated at bid price : 25.18 Bid-YTW : 5.88 % |

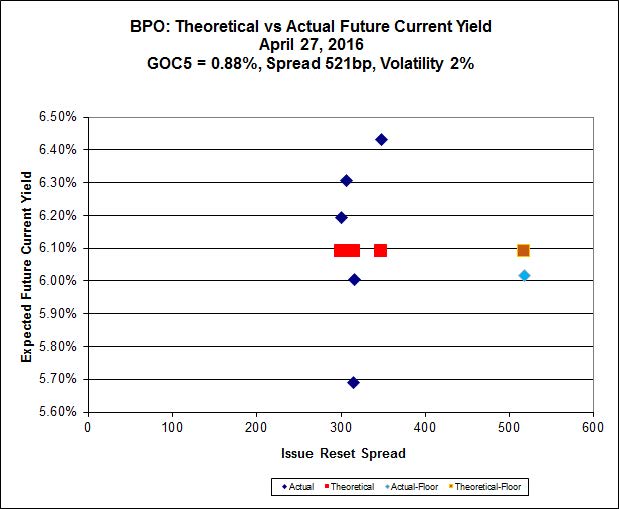

Implied Volatility analysis shows the same peculiar behaviour as was noted on the announcement date, with BPO.PR.N (resetting at +307 on 2016-6-30) and BPO.PR.R (+348 on 2016-9-30) both showing a far higher Expected Future Current Yield than the new issue, despite the new issue’s far higher Issue Reset Spread.

Click for Big

Why did you specify a maturity date 2021-06-30? There is “Conversion at the Option of the Holder” clause like there is with the still extant Series J & K. I think this Series CC is perpetual, not (essentially) puttable after 5 years.

The output of the YTW scenario is not particularly sophisticated.

The line above the “Maturity Date” is “Maturity Type : Call”; therefore the YTW scenario is a call at $25.00 on 2021-6-30.

Other Maturity types are “Hard Maturity”, “Limit Maturity” and “Option Certainty”.

I see. BTW I mean to say there is *no* “Conversion at the Option of the Holder” clause for this Series CC, whereas the Series J & K has it.

I am mystified as to why BPO.PR.C has a YTM of ~5.7% and YTW of ~5%, whereas BPO.PR.N and BPO.PR.R have YTM of ~6% and plenty of room for capital appreciation.

I am mystified …

Me too, if it’s any consolation to you.

[…] was issued as a FixedReset, 6.00%+518M600, that commenced trading 2016-4-27 after being announced 2016-4-18. It reset to 6.12% in 2021 with no conversion. The issue has been […]