The BoC has released a new Staff analytical paper by Bruno Feunou, Jean-Sébastien Fontaine, Rishi Vala titled Macro News in Market Moves: Classifying News through Asset Co-movements:

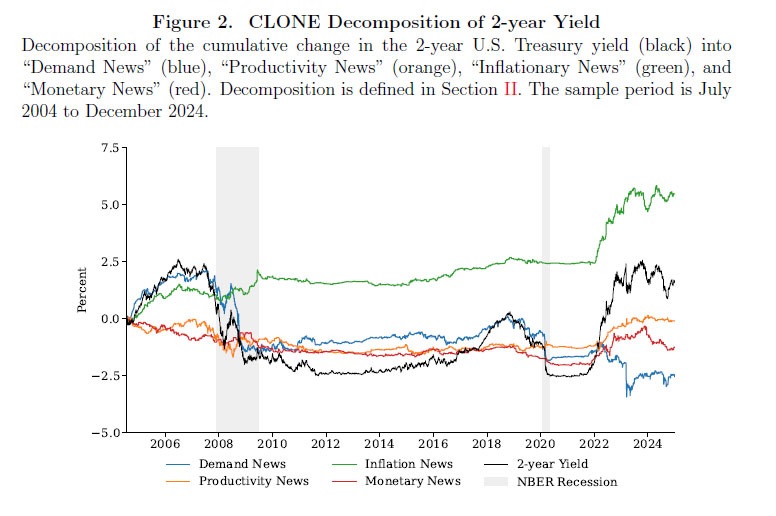

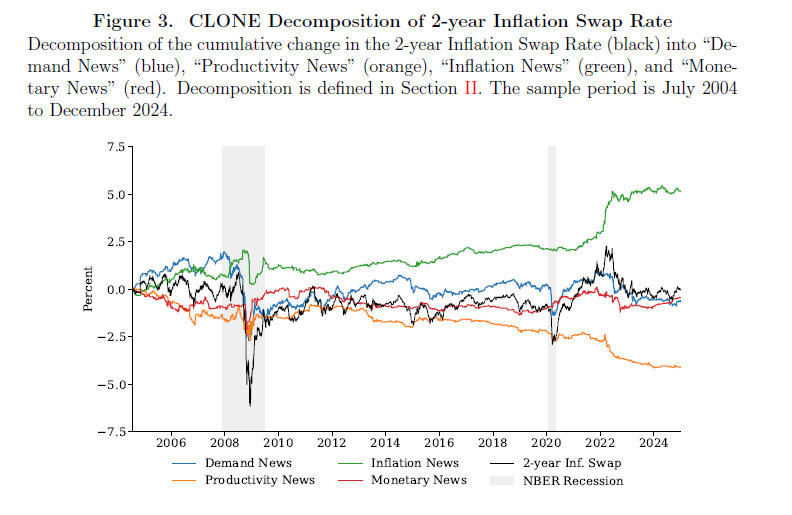

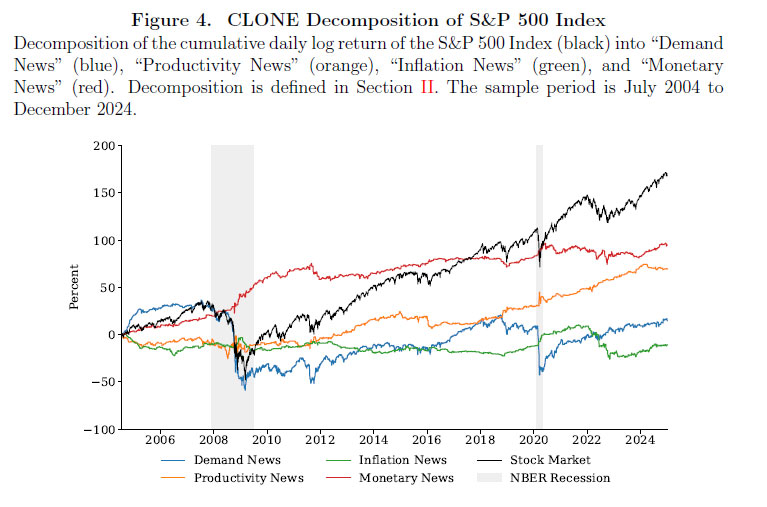

This paper introduces CLONE (Classification Of News), a method that decomposes asset price movements into four types of macroeconomic news—aggregate demand, productivity, inflation, and monetary policy—based on joint changes in prices of stocks, bonds, and inflation swaps. CLONE’s simplicity and forward-looking focus enable the identification of real-time economic signals that are critical for understanding market behavior and guiding policy decisions. We show that from 2004 to 2024 aggregate demand news historically dominated daily variation in asset prices, while inflation and monetary policy news have gained importance since 2021. We validate our method against sign-restricted VAR models and apply it to major U.S. macroeconomic data releases, providing insights into how market participants interpret and react to forward-looking information. We discuss several benefits of our approach relative to the standard sign restriction method.

…

At its core, CLONE classifies each day based on the realized combination of daily price changes of U.S. stocks, bonds, and inflation swaps.2 These daily asset price changes capture forward-looking responses to “news” because asset prices reflect expectations (and uncertainties) about future payoffs sensitive to economic outcomes, and new information, or “news”, leads to revisions in those expectations. We interpret each realized combination of asset price changes as reflecting the dominant news affecting markets on that day. Under our framework, each day reflects either (1) news of future aggregate demand, (2) news of future inflation, (3) news of future productivity, or (4) news of future monetary policy.

…

CLONE’s simplicity is also its key limitation. Since we identify each day with one news type, we ignore the possibility that certain days can signal more than one news type , and we can attribute noisy days with no news to a given news type. However, if news tends to disperse slowly over time, a bulk of the classification errors average out when we aggregate the daily identification to the monthly or quarterly frequency. In Section IV, we more formally discuss how our assignment of a single news type to each day can be interpreted as inferring the dominant source of news on that day, and how CLONE produces qualitatively similar conclusions as traditional SVARs.

We introduce CLONE, a simple and transparent decomposition of asset price movements. CLONE classifies the type of macroeconomic news revealed from stocks, bond yields, and inflation swap rates. The news components identified by CLONE exhibit persistent effects on asset prices, produce qualitatively similar conclusions to those obtained from sign-restricted SVARs, and align well with revisions in professional forecasters’ and businesses’ expectations of macroeconomic and financial variables in the direction we would expect.

We show that aggregate demand news accounts for the largest share of daily variation in the S&P 500, the 2-year U.S. Treasury yield, and the 2-year inflation swap rate over 2004–2024. More recently, between 2021 and 2024, the importance of inflation and monetary news increased markedly, reflecting a shift in the dominant drivers of asset price movements.

Finally, we examine the information content of FOMC announcements and major U.S. macroeconomic data releases. While FOMC communications are traditionally associated with monetary policy news, they have increasingly conveyed information about inflation in recent years. At the same time, we find that productivity-related news plays a central role in explaining stock market returns and movements in inflation swap rates, highlighting an additional and often underappreciated dimension of information revealed at policy and data announcements.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1490 % | 2,486.8 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1490 % | 4,715.4 |

| Floater | 5.79 % | 6.08 % | 59,177 | 13.72 | 3 | 0.1490 % | 2,717.5 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0394 % | 3,661.5 |

| SplitShare | 4.77 % | 4.26 % | 81,190 | 3.00 | 5 | -0.0394 % | 4,372.7 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0394 % | 3,411.7 |

| Perpetual-Premium | 5.71 % | 5.73 % | 89,282 | 14.02 | 7 | -0.1705 % | 3,063.5 |

| Perpetual-Discount | 5.60 % | 5.70 % | 52,739 | 14.30 | 28 | 0.2418 % | 3,379.2 |

| FixedReset Disc | 5.87 % | 5.76 % | 128,930 | 13.94 | 27 | -0.0708 % | 3,205.4 |

| Insurance Straight | 5.52 % | 5.58 % | 65,073 | 14.57 | 22 | 0.7069 % | 3,297.1 |

| FloatingReset | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0708 % | 3,813.1 |

| FixedReset Prem | 5.94 % | 4.45 % | 90,348 | 2.49 | 21 | 0.0711 % | 2,669.6 |

| FixedReset Bank Non | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0708 % | 3,276.5 |

| FixedReset Ins Non | 5.27 % | 5.20 % | 101,834 | 14.69 | 14 | 0.4177 % | 3,139.6 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BN.PR.T | FixedReset Disc | -5.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 20.50 Evaluated at bid price : 20.50 Bid-YTW : 6.20 % |

| GWO.PR.R | Insurance Straight | -2.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 21.10 Evaluated at bid price : 21.10 Bid-YTW : 5.70 % |

| IFC.PR.G | FixedReset Ins Non | -2.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 23.47 Evaluated at bid price : 24.90 Bid-YTW : 5.49 % |

| CCS.PR.C | Insurance Straight | -2.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 22.21 Evaluated at bid price : 22.48 Bid-YTW : 5.55 % |

| POW.PR.C | Perpetual-Premium | -2.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 24.84 Evaluated at bid price : 25.07 Bid-YTW : 5.87 % |

| PWF.PR.S | Perpetual-Discount | -1.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 20.85 Evaluated at bid price : 20.85 Bid-YTW : 5.83 % |

| CU.PR.F | Perpetual-Discount | -1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 19.80 Evaluated at bid price : 19.80 Bid-YTW : 5.73 % |

| ENB.PR.B | FixedReset Disc | 1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 21.40 Evaluated at bid price : 21.72 Bid-YTW : 5.99 % |

| MFC.PR.B | Insurance Straight | 1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 21.81 Evaluated at bid price : 22.05 Bid-YTW : 5.28 % |

| GWO.PR.Q | Insurance Straight | 1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 22.72 Evaluated at bid price : 23.01 Bid-YTW : 5.59 % |

| BN.PF.E | FixedReset Disc | 1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 22.68 Evaluated at bid price : 23.65 Bid-YTW : 5.65 % |

| BN.PR.N | Perpetual-Discount | 2.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 20.85 Evaluated at bid price : 20.85 Bid-YTW : 5.81 % |

| BN.PR.R | FixedReset Disc | 2.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 21.53 Evaluated at bid price : 21.87 Bid-YTW : 5.83 % |

| MFC.PR.L | FixedReset Ins Non | 3.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 23.23 Evaluated at bid price : 24.72 Bid-YTW : 5.09 % |

| MFC.PR.J | FixedReset Ins Non | 4.02 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2028-03-19 Maturity Price : 25.00 Evaluated at bid price : 25.60 Bid-YTW : 4.82 % |

| CU.PR.H | Perpetual-Discount | 7.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 23.85 Evaluated at bid price : 24.10 Bid-YTW : 5.47 % |

| GWO.PR.T | Insurance Straight | 23.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 22.80 Evaluated at bid price : 23.09 Bid-YTW : 5.57 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| PWF.PR.P | FixedReset Disc | 52,908 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 20.10 Evaluated at bid price : 20.10 Bid-YTW : 5.60 % |

| FTS.PR.M | FixedReset Disc | 48,404 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 23.20 Evaluated at bid price : 24.78 Bid-YTW : 5.31 % |

| MFC.PR.L | FixedReset Ins Non | 41,194 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 23.23 Evaluated at bid price : 24.72 Bid-YTW : 5.09 % |

| BN.PF.G | FixedReset Disc | 28,680 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 23.07 Evaluated at bid price : 24.60 Bid-YTW : 5.75 % |

| BN.PR.R | FixedReset Disc | 22,000 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-05 Maturity Price : 21.53 Evaluated at bid price : 21.87 Bid-YTW : 5.83 % |

| TD.PF.A | FixedReset Prem | 19,675 | YTW SCENARIO Maturity Type : Call Maturity Date : 2029-10-31 Maturity Price : 25.00 Evaluated at bid price : 25.73 Bid-YTW : 4.26 % |

| There were 16 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| See TMX DataLinx: ‘Last’ != ‘Close’ and the posts linked therein for an idea of why these quotes are so horrible. | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.Q | FixedReset Ins Non | Quote: 25.39 – 27.57 Spot Rate : 2.1800 Average : 1.2014 YTW SCENARIO |

| SLF.PR.E | Insurance Straight | Quote: 21.50 – 22.90 Spot Rate : 1.4000 Average : 0.8207 YTW SCENARIO |

| BN.PR.T | FixedReset Disc | Quote: 20.50 – 21.99 Spot Rate : 1.4900 Average : 1.0694 YTW SCENARIO |

| IFC.PR.G | FixedReset Ins Non | Quote: 24.90 – 25.89 Spot Rate : 0.9900 Average : 0.5707 YTW SCENARIO |

| GWO.PR.R | Insurance Straight | Quote: 21.10 – 22.10 Spot Rate : 1.0000 Average : 0.6266 YTW SCENARIO |

| CCS.PR.C | Insurance Straight | Quote: 22.48 – 23.60 Spot Rate : 1.1200 Average : 0.8222 YTW SCENARIO |