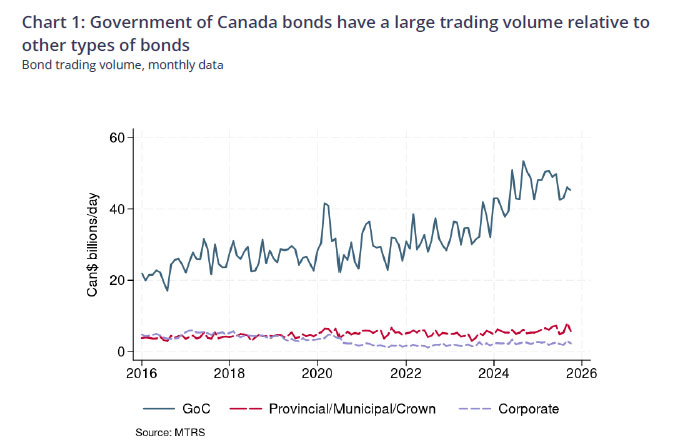

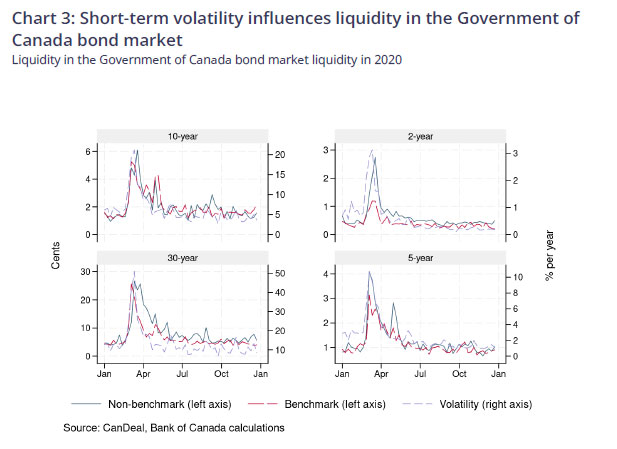

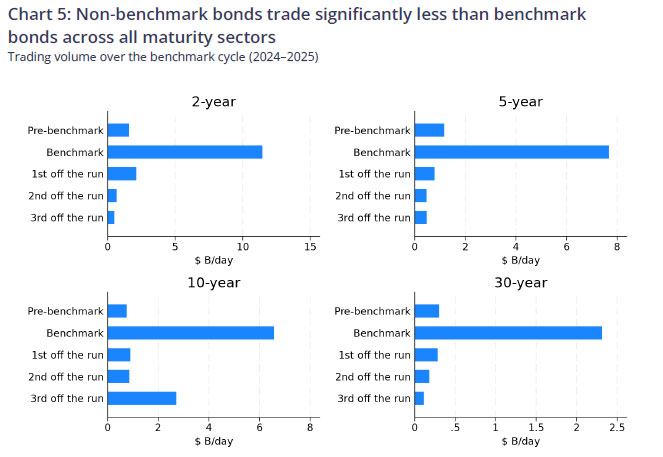

The BoC has released a new Staff Analyical Paper by Petr Kocourek and Adrian Walton titled Government of Canada Fixed-Income Market Ecology II: Government of Canada Bond Dealing:

This paper describes the organization of the market for trading Government of Canada (GoC) bonds. We outline the role of investment dealers in intermediating trading, distributing GoC securities and providing liquidity across the yield curve. We describe the key features of GoC bond trading and the financial market infrastructures that support it. We also review dealers’ risk-management and funding practices, with a focus on interest rate hedging and the use of benchmark bonds and related derivatives. The structure of the GoC bond market reflects both prudential and dealer-specific regulatory frameworks. As well, it reflects dealers’ ability to manage inventory, basis risk and short-term volatility—factors that shape trading costs and liquidity conditions in both benchmark and non-benchmark bonds.

There are some useful charts:

For those left wondering about how much all this liquidity is worth, I recommend my article Credit Spreads and Default Risk. This includes a chart from the BoE that is very illuminating.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4971 % | 2,493.0 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4971 % | 4,727.1 |

| Floater | 5.78 % | 6.07 % | 57,958 | 13.71 | 3 | 0.4971 % | 2,724.3 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3477 % | 3,664.4 |

| SplitShare | 4.76 % | 4.28 % | 82,416 | 2.99 | 5 | 0.3477 % | 4,376.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3477 % | 3,414.4 |

| Perpetual-Premium | 5.70 % | 5.76 % | 84,205 | 14.06 | 7 | 0.2677 % | 3,070.2 |

| Perpetual-Discount | 5.61 % | 5.71 % | 47,737 | 14.27 | 28 | 0.1753 % | 3,370.9 |

| FixedReset Disc | 5.88 % | 5.89 % | 131,983 | 13.78 | 27 | 0.1843 % | 3,200.8 |

| Insurance Straight | 5.50 % | 5.59 % | 61,903 | 14.52 | 22 | 0.6664 % | 3,307.3 |

| FloatingReset | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1843 % | 3,807.6 |

| FixedReset Prem | 5.96 % | 4.68 % | 83,523 | 2.04 | 21 | -0.1478 % | 2,661.0 |

| FixedReset Bank Non | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1843 % | 3,271.8 |

| FixedReset Ins Non | 5.26 % | 5.33 % | 90,583 | 14.62 | 14 | 0.1561 % | 3,141.4 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| NA.PR.K | FixedReset Prem | -3.67 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2029-05-01 Maturity Price : 25.00 Evaluated at bid price : 27.06 Bid-YTW : 5.11 % |

| GWO.PR.Y | Insurance Straight | -3.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 20.00 Evaluated at bid price : 20.00 Bid-YTW : 5.64 % |

| BN.PF.E | FixedReset Disc | -1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 22.53 Evaluated at bid price : 23.35 Bid-YTW : 5.85 % |

| CIU.PR.A | Perpetual-Discount | -1.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 20.24 Evaluated at bid price : 20.24 Bid-YTW : 5.73 % |

| SLF.PR.G | FixedReset Ins Non | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 19.41 Evaluated at bid price : 19.41 Bid-YTW : 5.56 % |

| PWF.PR.O | Perpetual-Premium | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 24.85 Evaluated at bid price : 25.06 Bid-YTW : 5.86 % |

| BN.PF.C | Perpetual-Discount | 1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 21.23 Evaluated at bid price : 21.23 Bid-YTW : 5.83 % |

| MFC.PR.B | Insurance Straight | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 21.75 Evaluated at bid price : 22.00 Bid-YTW : 5.29 % |

| BN.PR.B | Floater | 1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 13.10 Evaluated at bid price : 13.10 Bid-YTW : 6.07 % |

| PVS.PR.L | SplitShare | 1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2030-06-30 Maturity Price : 25.00 Evaluated at bid price : 26.00 Bid-YTW : 4.51 % |

| SLF.PR.C | Insurance Straight | 1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 21.51 Evaluated at bid price : 21.77 Bid-YTW : 5.11 % |

| MFC.PR.C | Insurance Straight | 1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 21.54 Evaluated at bid price : 21.80 Bid-YTW : 5.17 % |

| GWO.PR.S | Insurance Straight | 1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 23.14 Evaluated at bid price : 23.40 Bid-YTW : 5.61 % |

| SLF.PR.E | Insurance Straight | 1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 21.59 Evaluated at bid price : 21.85 Bid-YTW : 5.14 % |

| GWO.PR.T | Insurance Straight | 1.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 22.90 Evaluated at bid price : 23.19 Bid-YTW : 5.55 % |

| FTS.PR.H | FixedReset Disc | 2.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 19.70 Evaluated at bid price : 19.70 Bid-YTW : 5.53 % |

| FTS.PR.K | FixedReset Disc | 2.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 22.85 Evaluated at bid price : 23.74 Bid-YTW : 5.32 % |

| CCS.PR.C | Insurance Straight | 2.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 22.93 Evaluated at bid price : 23.20 Bid-YTW : 5.39 % |

| SLF.PR.D | Insurance Straight | 2.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 21.44 Evaluated at bid price : 21.70 Bid-YTW : 5.12 % |

| MFC.PR.J | FixedReset Ins Non | 2.74 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2028-03-19 Maturity Price : 25.00 Evaluated at bid price : 25.50 Bid-YTW : 5.06 % |

| CU.PR.F | Perpetual-Discount | 3.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 20.39 Evaluated at bid price : 20.39 Bid-YTW : 5.56 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| SLF.PR.D | Insurance Straight | 109,800 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 21.44 Evaluated at bid price : 21.70 Bid-YTW : 5.12 % |

| IFC.PR.M | Perpetual-Premium | 35,850 | YTW SCENARIO Maturity Type : Option Certainty Maturity Date : 2056-03-10 Maturity Price : 25.00 Evaluated at bid price : 25.22 Bid-YTW : 5.60 % |

| IFC.PR.A | FixedReset Ins Non | 25,200 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 21.63 Evaluated at bid price : 22.05 Bid-YTW : 5.37 % |

| GWO.PR.R | Insurance Straight | 20,000 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 21.30 Evaluated at bid price : 21.30 Bid-YTW : 5.65 % |

| BN.PF.F | FixedReset Disc | 17,500 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 23.25 Evaluated at bid price : 24.86 Bid-YTW : 5.87 % |

| BN.PR.M | Perpetual-Discount | 16,869 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-10 Maturity Price : 20.82 Evaluated at bid price : 20.82 Bid-YTW : 5.82 % |

| There were 8 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| See TMX DataLinx: ‘Last’ != ‘Close’ and the posts linked therein for an idea of why these quotes are so horrible. | ||

| Issue | Index | Quote Data and Yield Notes |

| NA.PR.K | FixedReset Prem | Quote: 27.06 – 28.31 Spot Rate : 1.2500 Average : 0.7161 YTW SCENARIO |

| GWO.PR.G | Insurance Straight | Quote: 23.48 – 24.87 Spot Rate : 1.3900 Average : 0.9898 YTW SCENARIO |

| GWO.PR.Y | Insurance Straight | Quote: 20.00 – 21.13 Spot Rate : 1.1300 Average : 0.8005 YTW SCENARIO |

| GWO.PR.Q | Insurance Straight | Quote: 22.80 – 23.65 Spot Rate : 0.8500 Average : 0.5457 YTW SCENARIO |

| CU.PR.C | FixedReset Disc | Quote: 24.80 – 25.80 Spot Rate : 1.0000 Average : 0.7155 YTW SCENARIO |

| IFC.PR.I | Insurance Straight | Quote: 24.02 – 25.00 Spot Rate : 0.9800 Average : 0.7344 YTW SCENARIO |