The FOMC stood pat today:

The Federal Open Market Committee approved the following statement for release by a 12 – 0 vote:

The Committee decided to maintain the target range for the federal funds rate at 3-1/2 to 3-3/4 percent, in support of the Federal Reserve’s dual mandate. The Committee reaffirmed its policy of maintaining ample reserves in the banking system.

Economic activity is expanding at a solid pace despite elevated uncertainty that owes, in part, to the conflict in the Middle East. Productivity growth and capital investment are strong. Job gains have kept pace with the workforce, and the unemployment rate has changed little.

Inflation remains elevated relative to the Committee’s 2 percent goal, in part reflecting supply shocks that have driven price increases in certain sectors, including energy. The Committee will deliver price stability.

“The committee will deliver price stability”? That sounds more like a Republican talking point than a central bank pronouncement … well, we’ll see. And there’s a lot less economic substance in this release than I like to see. Nevertheless, it carried unanimously, as was so eagerly trumpetted in the first line, which surprises me. Maybe Trump-toadyism has taken over. Maybe everybody just wants to be nice to Warsh at his first meeting. I certainly don’t know.

But the opacity continued into the press conference:

But as determined as Warsh said the Fed was to modernizing and fixing the economy’s problems, Warsh was noticeably less willing to provide detailed answers about the Fed’s decision-making process or thoughts on broader economic topics than Powell. Warsh often referred back to the Fed’s brief statement about the economy rather than expounding upon it.

In an answer that Warsh acknowledged was purposefully “curt,” he said: “I’ve got nothing more to say than the statement itself.” In another, he noted, “I can’t do much better than the committee just did. So let me restate it.”

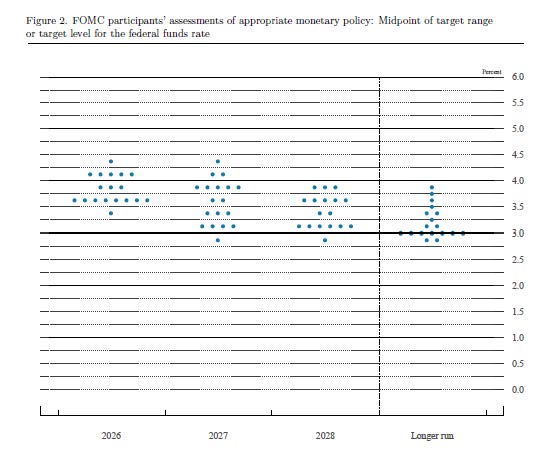

The Fed’s economic projections still include the dot-plot:

Ben Werschkul comments:

The Federal Reserve’s latest “dot plot,” outlining policymakers’ interest rate projections, revealed a sharp shift in central bankers’ expectations.

Not only are rate cuts almost surely off the table for the rest of the year, but there is also a sharply higher chance of a hike before the end of 2026.

Nine policymakers who participated in the exercise projected at least one hike, with six even suggesting multiple hikes could be in the offing.

…

The median forecast for interest rates at the end of 2027 remains unchanged at the current rate of 3.50% to 3.75%.The projection is a sharp change from the outlook released in March, which had maintained a median forecast for one rate cut in 2026 and two in total by the end of 2027.

The equity markets responded poorly:

Major North American stock indexes immediately turned lower after the U.S. Federal Reserve kept interest rates unchanged as investors interpreted the accompanying details as being hawkish.

Short-term bonds yields spiked, as did the U.S. dollar against major currencies. The Canadian dollar traded at its lowest since 2025, at just above the 71 cents US level, down about a third of a cent for the session.

The U.S. two-year bond yield rocketed 9 basis points higher, a large one-day move. Short-term U.S. interest-rate futures are now pricing in a bigger chance that the Federal Reserve will deliver a rate hike by September than opt to keep rates where they are.

The shift in market-based rate-path expectations comes after the Fed said it would leave the policy rate in its current 3.50%-3.75% range at this time, but a near-majority of policymakers penciled a rate hike by the end of 2026 to combat higher inflation.

PerpetualDiscounts now yield 5.66%, equivalent to 7.36% interest at the standard conversion factor of 1.3x. Long corporates yielded 4.89% on 2026-06-17. Therefore the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) has widened to 245bp from the 235bp reported June 10.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 5.62 % | 6.01 % | 24,221 | 14.82 | 1 | 0.0000 % | 2,611.0 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.4220 % | 4,902.1 |

| Floater | 5.55 % | 5.65 % | 40,972 | 14.50 | 3 | 1.4220 % | 2,825.1 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1742 % | 3,630.4 |

| SplitShare | 4.80 % | 4.50 % | 50,660 | 2.75 | 5 | -0.1742 % | 4,335.5 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1742 % | 3,382.7 |

| Perpetual-Premium | 5.70 % | 5.74 % | 73,099 | 14.10 | 7 | -0.0851 % | 3,064.5 |

| Perpetual-Discount | 5.58 % | 5.66 % | 40,906 | 14.34 | 28 | 0.2125 % | 3,378.3 |

| FixedReset Disc | 5.63 % | 5.86 % | 125,180 | 13.92 | 19 | 0.0159 % | 3,303.6 |

| Insurance Straight | 5.49 % | 5.50 % | 47,154 | 14.63 | 22 | -0.2160 % | 3,280.8 |

| FloatingReset | 4.64 % | 4.65 % | 21,926 | 16.20 | 1 | 0.0000 % | 4,093.2 |

| FixedReset Prem | 5.94 % | 4.57 % | 90,437 | 2.35 | 29 | 0.1744 % | 2,647.2 |

| FixedReset Bank Non | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0159 % | 3,377.0 |

| FixedReset Ins Non | 5.15 % | 5.27 % | 69,882 | 14.60 | 14 | 0.1649 % | 3,206.9 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| GWO.PR.H | Insurance Straight | -3.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-06-17 Maturity Price : 20.99 Evaluated at bid price : 20.99 Bid-YTW : 5.80 % |

| FTS.PR.F | Perpetual-Discount | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-06-17 Maturity Price : 22.71 Evaluated at bid price : 23.00 Bid-YTW : 5.36 % |

| ENB.PR.H | FixedReset Disc | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-06-17 Maturity Price : 23.19 Evaluated at bid price : 23.50 Bid-YTW : 5.69 % |

| ENB.PF.E | FixedReset Disc | 1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-06-17 Maturity Price : 22.64 Evaluated at bid price : 23.55 Bid-YTW : 6.00 % |

| BN.PF.A | FixedReset Prem | 1.17 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2028-09-30 Maturity Price : 25.00 Evaluated at bid price : 25.90 Bid-YTW : 4.98 % |

| GWO.PR.T | Insurance Straight | 1.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-06-17 Maturity Price : 22.66 Evaluated at bid price : 22.90 Bid-YTW : 5.63 % |

| PWF.PR.Z | Perpetual-Discount | 3.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-06-17 Maturity Price : 22.74 Evaluated at bid price : 23.03 Bid-YTW : 5.66 % |

| PWF.PR.A | Floater | 3.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-06-17 Maturity Price : 14.64 Evaluated at bid price : 14.64 Bid-YTW : 5.39 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BN.PF.I | FixedReset Prem | 43,700 | YTW SCENARIO Maturity Type : Call Maturity Date : 2027-03-31 Maturity Price : 25.00 Evaluated at bid price : 25.27 Bid-YTW : 3.75 % |

| PWF.PR.P | FixedReset Disc | 37,500 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-06-17 Maturity Price : 20.56 Evaluated at bid price : 20.56 Bid-YTW : 5.73 % |

| IFC.PR.C | FixedReset Ins Non | 35,000 | YTW SCENARIO Maturity Type : Call Maturity Date : 2026-09-30 Maturity Price : 25.00 Evaluated at bid price : 25.03 Bid-YTW : 2.59 % |

| ENB.PR.P | FixedReset Disc | 26,700 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-06-17 Maturity Price : 23.03 Evaluated at bid price : 24.03 Bid-YTW : 5.86 % |

| PWF.PR.T | FixedReset Prem | 25,100 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-06-17 Maturity Price : 23.48 Evaluated at bid price : 25.08 Bid-YTW : 5.44 % |

| POW.PR.I | Perpetual-Premium | 15,100 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-06-17 Maturity Price : 24.61 Evaluated at bid price : 25.01 Bid-YTW : 5.74 % |

| There were 3 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| See TMX DataLinx: ‘Last’ != ‘Close’ and the posts linked therein for an idea of why these quotes are so horrible. | ||

| Issue | Index | Quote Data and Yield Notes |

| IFC.PR.A | FixedReset Ins Non | Quote: 22.00 – 23.34 Spot Rate : 1.3400 Average : 1.0033 YTW SCENARIO |

| GWO.PR.H | Insurance Straight | Quote: 20.99 – 21.78 Spot Rate : 0.7900 Average : 0.4762 YTW SCENARIO |

| BN.PF.M | FixedReset Prem | Quote: 25.75 – 26.62 Spot Rate : 0.8700 Average : 0.7404 YTW SCENARIO |

| ENB.PF.K | FixedReset Prem | Quote: 25.46 – 25.85 Spot Rate : 0.3900 Average : 0.2664 YTW SCENARIO |

| CU.PR.J | Perpetual-Discount | Quote: 21.66 – 22.18 Spot Rate : 0.5200 Average : 0.4139 YTW SCENARIO |

| IFC.PR.K | Insurance Straight | Quote: 23.85 – 24.90 Spot Rate : 1.0500 Average : 0.9491 YTW SCENARIO |

[…] PerpetualDiscounts now yield 5.67%, equivalent to 7.37% interest at the standard conversion factor of 1.3x. Long corporates yielded 4.94% on 2026-06-17. Therefore the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) has remained at the 245bp reported June 17. […]