Bank of Montreal has announced:

a domestic public offering of $350 million of Non-Cumulative 5-Year Rate Reset Class B Preferred Shares Series 38 (Non-Viability Contingent Capital (NVCC)) (the “Preferred Shares Series 38”). The offering will be underwritten on a bought-deal basis by a syndicate of underwriters led by BMO Capital Markets. The Bank has granted to the underwriters an option to purchase up to an additional $50 million of the Preferred Shares Series 38 exercisable at any time up to 48 hours before closing.

The Preferred Shares Series 38 will be issued to the public at a price of $25.00 per share. Holders will be entitled to receive non-cumulative preferential fixed quarterly dividends for the initial period ending February 25, 2022, as and when declared by the Board of Directors of the Bank, payable in the amount of $0.303125 per share, to yield 4.85 per cent annually.

Subject to regulatory approval, on or after February 25, 2022, the Bank may redeem the Preferred Shares Series 38 in whole or in part at par. On February 25, 2022, the dividend rate will reset and will reset thereafter every five years to be equal to the 5-Year Government of Canada Bond Yield plus 4.06 per cent. Subject to certain conditions, holders may elect to convert any or all of their Preferred Shares Series 38 into an equal number of Non-Cumulative Floating Rate Class B Preferred Shares Series 39 (Non-Viability Contingent Capital (NVCC)) (“Preferred Shares Series 39”) on February 25, 2022, and on February 25 of every fifth year thereafter. Holders of the Preferred Shares Series 39 will be entitled to receive non-cumulative preferential floating rate quarterly dividends, as and when declared by the Board of Directors of the Bank, equal to the then 3-month Government of Canada Treasury Bill Yield plus 4.06 per cent. Subject to certain conditions, holders may elect to convert any or all of their Preferred Shares Series 39 into an equal number of Preferred Shares Series 38 on February 25, 2027, and on February 25 of every fifth year thereafter.

The anticipated closing date is October 21, 2016. The net proceeds from the offering will be used by the Bank for general banking purposes.

They later announced:

that as a result of strong investor demand for its previously announced domestic public offering of $350 million of Non-Cumulative 5-Year Rate Reset Class B Preferred Shares Series 38 (Non-Viability Contingent Capital (NVCC)), the size of the offering has been increased to $600 million. As announced earlier today, the revised offering will be underwritten on a bought-deal basis by a syndicate led by BMO Capital Markets.

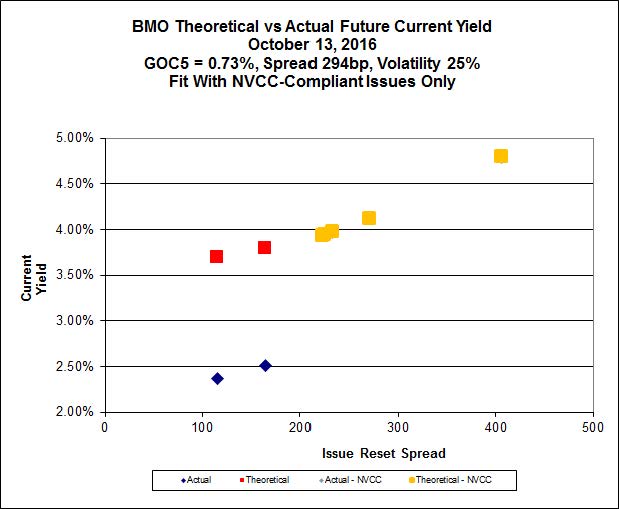

As has often been the case lately, Implied Volatility analysis results in a chart that can be interpreted in two ways:

Click for Big

The curve fits very well, with a very high Implied Volatility. If one takes the view that GOC-5 rates will increase dramatically over the next few years, the low-spread, low-price issues will be preferred (as this will lead to capital gains on these issues, but not the new one since the call provision caps the expected price); if one takes the view that the current GOC yield curve represents the new normal, then the new issue will be preferred (as one will then expect Implied Volatility to decrease, flattening the fitted curve, resulting in capital losses for the low-spread issues).