Assiduous Reader DR sent me the following query:

Today’s Financial Posts has an article “A better Basel mousetrap to protect taxpayers”, by Finn Poschmann regarding NVCC.

What is your opinion?

A short search brought up the article in question, A Better Basel Mousetrap to Protect Taxpayers, which in turn led me to the proposal by Jeremy Bulow and Paul Klemperer titled Market-Based Bank Capital Regulation:

Today’s regulatory rules, especially the easily-manipulated measures of regulatory capital, have led to costly bank failures. We design a robust regulatory system such that (i) bank losses are credibly borne by the private sector (ii) systemically important institutions cannot collapse suddenly; (iii) bank investment is counter-cyclical; and (iv) regulatory actions depend upon market signals (because the simplicity and clarity of such rules prevents gaming by firms, and forbearance by regulators, as well as because of the efficiency role of prices). One key innovation is “ERNs” (equity recourse notes — superficially similar to, but importantly distinct from, “cocos”) which gradually “bail in” equity when needed. Importantly, although our system uses market information, it does not rely on markets being “right.”

…

Our solution is based on two rules. First, any systemically important financial institution (SIFI) that cannot be quickly wound down must limit the recourse of non-guaranteed creditors to assets posted as collateral plus equity plus unsecured debt that can itself be converted into equity–so these creditors have some recourse but cannot force the institution into re-organization. Second, any debt guaranteed by the government, such as deposit accounts, must be backed by government-guaranteed securities. This second rule can only realistically be thought of as a very long-run ambition – our interim objective would involve a tight ring-fence of government-guaranteed deposits collateralized by assets that are haircut at rates similar to those applied by lenders (including central banks3 and the commercial banks themselves!) to secured borrowers.Specifically: first, we would have banks replace all (non-deposit) existing unsecured debt with “equity recourse notes” (ERNs). ERNs are superficially similar to contingent convertible debt (“cocos”) but have important differences. ERNs would be long-term bonds, subject to certain term-structure requirements, with the feature that any interest or principal payments payable on a date when the stock price is lower than a pre-specified price would be paid in stock at that pre-specified price. The pre-specified price would be required to be no less than (say) 25 percent of the share price on the date the bond was issued. For example, if the stock were selling at $100 on the day a bond was issued and then fell below $25 by the time a payment of $1000 was due, the firm would be required to pay the creditor (1000/25) = 40 shares of stock in lieu of the payment. If the stock rebounded in price, future payments could again be in cash.

Crucially, for ERNs, unlike cocos:

- any payments in shares are at a pre-set share price, not at the current share price or at a discount to it—so ERNs are stabilizing because that price will always be at a premium to the market

- conversion is triggered by market prices, not regulatory values—removing incentives to manipulate regulatory measures, and making it harder for regulators to relax requirements

- conversion is payment-at-a-time, not the entire bond at once (because ERNs become equity in the states that matter to taxpayers, they are, for regulatory purposes, like equity from their date of issuance so there is no reason for faster conversion)–further reducing pressures for “regulatory forbearance” and also largely solving a “multiple equilibria” problem raised in the academic literature

- we would replace all existing unsecured debt with ERNs, not merely a fraction of it—ensuring, as we show below, that ERNs become cheaper to issue when the stock price falls, creating counter-cyclical investment incentives when they are most needed.

OK, so I have difficulties with all this. Their first point is that non-guaranteed creditors “cannot force the institution into re-organization.” Obviously there are many differences of opinion in this, but I take the view that being able to force a company into re-organization – which may include bankruptcy – is one of the hallmarks of a bond. For example, I consider preferred shares to be fixed income – as they have a cap on their total return and they have first-loss protection – but I do not consider them bonds – as they cannot force bankruptcy. The elimination of bankruptcy, although very popular among politicians (who refer to bankruptcy as a form of terrorism) is a very big step; bankruptcy is a very big stick that serves to concentrate the minds of management and directors.

Secondly, they want insured deposits to be offset by government securities. There’s an immediate problem about this in Canada, because insured deposits total $646-billion while government of Canada marketable debt totals $639-billion. You could get around this by saying the CMHC-guaranteed mortgages are OK, but even after years of Spend-Every-Penny pouring fuel on the housing fire, CMHC insurance totals only $559.8-billion (out of a total of $915-billion. At present, Canadian Chartered Banks hold only about $160-billion of government debt. So it would appear that, at the very least, this part of the plan would essentially force the government to continue to insure a ridiculous proportion of Canadian residential mortgages.

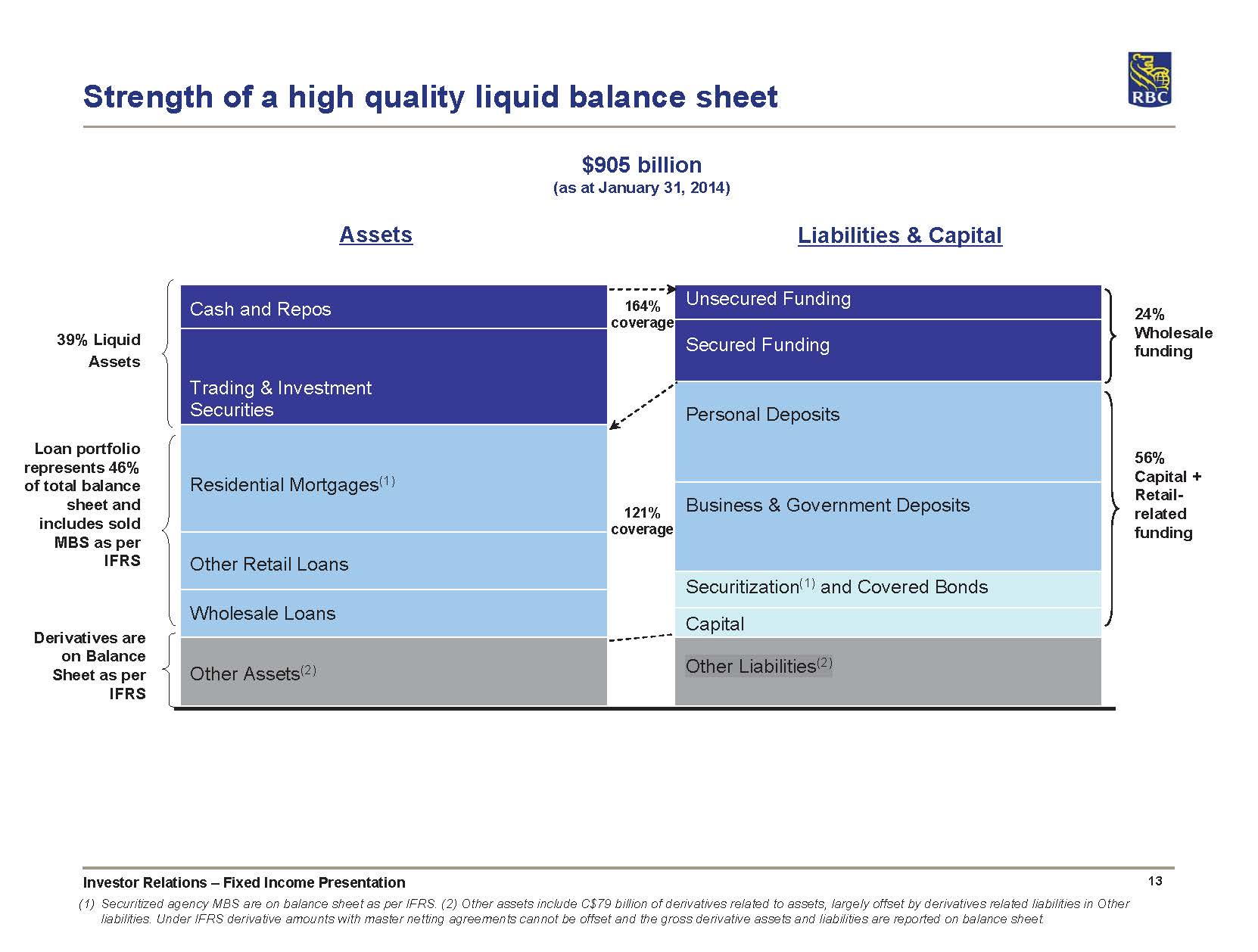

And, specifically, they want all (non-deposit) existing unsecured debt with “equity recourse notes”. OK, so how much is that? Looking at recent figures from RBC:

Click for Big

So roughly a quarter of Royal Bank’s liabilities would become ERNs …. and who’s going to buy it? It’s forcibly convertible into equity long before the point of non-viability – that’s the whole point – so for risk management purposes it is equity. If held by another bank, it will attract a whopping capital charge (or if it doesn’t, it should) and it can’t be held by institutional bond portfolios (or if it is, it shouldn’t be). I have real problems with this.

The paper makes several entertaining points about bank regulation:

The regulatory system distorts incentives in several ways. One of the motivations for Citigroup to sell out of Smith, Barney at what was generally believed to be a low price, was that it allowed Citi to book an increase in regulatory capital. Conversely, selling risky “toxic assets” with a regulatory value greater than market is discouraged because doing so raises capital requirements even while reducing risk.[footnote].

[Footnote reads] : Liquidity reduction is another consequence of the current regulatory system, as firms will avoid price-discovery by avoiding buying as well as selling over-marked assets. For example, Goldman Sachs stood ready to sell assets at marks that AIG protested were too low, but AIG did not take up these offers. See Goldman Sachs (2009). For an example of traders not buying even though they claimed the price was too low, see the FCIC transcript of a July 30, 2007 telephone call between AIG executives. “We can’t mark any of our positions, and obviously that’s what saves us having this enormous mark to market. If we start buying the physical bonds back … then any accountant is going to turn around and say, well, John, you know you traded at 90, you must be able to mark your bonds then.” Duarte (2012) discusses the recent trend of European banks to meet their requirements to raise regulatory capital by repurchasing their own junk bonds, arguably increasing the exposure of government insurers.

However, don’t get me wrong on this: the basic idea – of conversion to a pre-set value of stock once the market breaches that pre-set value – is one that I’ve been advocating for a long time. They are similar in spirit to McDonald CoCos, which were first discussed on PrefBlog under the heading Contingent Capital with a Dual Price Trigger (regrettably, the authors did not discuss McDonald’s proposal in their paper). ERNs are ‘high-trigger’ instruments, and therefore will help serve to avert a crisis, rather than merely mitigate one, as is the case with OSFI’s NVCC rules; I have long advocated high triggers.

My basic problem is simply that the authors:

- Require too many ERNs as a proportion of capital, and

- Seek to Ban the Bond

However, it may easily be argued that these objections are mere matters of detail.

Hi James, pow.pr.d has had some healthy volume lately and the price is marching towards $25.00. Do you see this being called soon by Power Corp ?

Thanks

I wouldn’t hold my breath, if you’re hoping for it!

It has the lowest coupon of the five POW Straight Perpetuals, and is actually rather nastily priced: at today’s last bid of 24.60, it doesn’t have much upside (since gains will be constrained by the call schedule) and has full downside in the event of market yield increases.

Not really, I am enjoying the dividend as its one i bought when the world was ending in 2009 so probably have enjoyed all the capital appreciation allready,just clipping coupons from here on in.