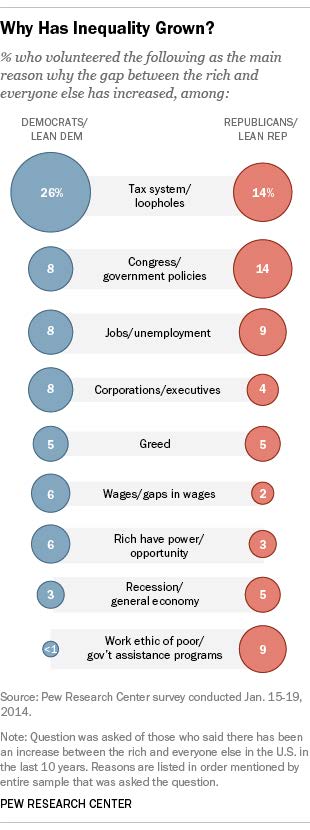

Assiduous Readers will recall that I ascribe increasing income inequality to technology. So I was astonished at the results of a Pew Poll on the subject:

Click for Big

(Sorry for lousy quality; can’t figure it out…)

Technological advance isn’t even mentioned! One possible explanation is that the poll’s question referred to “the rich”, whereas I think of income inequality in terms of quintiles; certainly the response “tax system” has a large effect if we think in terms of the gap between the fabled 1% and the rest of us (particularly in America) rather than, say, the gap between the second and fourth quintile. Even still, however, a lot of billionaires are self-made technologists:

Every year FORBES crunches the numbers to find out which Americans rank the richest–and each year it gets harder to join the exclusive Forbes 400 list. But you don’t have to inherit a fortune to become a Forbes 400 billionaire. In fact, the majority of our Forbes 400 members–273 of them–scrapped their way onto our list through their own efforts.

The self-made differ somewhat from their Forbes 400 counterparts in terms of how they gained their wealth. The most obvious difference between the groups, not surprisingly, is that many of the self-made earned fortunes through technology. A whopping 45 tycoons–nearly 25% of the Forbes 400–made their billions in tech, making it the second-most-popular industry overall for launching onto the Forbes 400.

…

After technology, real estate produced the next largest group of self-made Forbes 400 members.

…

Of course, the self-made and the inheritors share the Number 1 way of getting rich, which has long been “investing”–a catch-all category that describes hedge fund billionaires as well as others, like Warren Buffett, who have stakes in many industries.

We now know the secret of prosperity: corporate welfare:

Ontario Premier Kathleen Wynne is pledging $2.5-billion in new grants to attract more businesses to the province and help others expand.

The 10-year Jobs and Prosperity Fund, announced Monday, will be contained in this week’s budget, which could trigger an election.

Finance Minister Joe Oliver today announced that the Government of Canada successfully issued $1.5 billion in 50-year bonds.

This inaugural ultra-long issue is the first of its kind for the Government and is in line with its commitment since 2012–13 to reallocate short-term bond issuance towards long-term bonds to help reduce refinancing risk.

Quick Facts

- ◾Maturing on December 1, 2064, and with a yield of 2.96 per cent, this issuance will contribute to a reduction in refinancing risk at a low cost, which is consistent with the key objectives of the medium-term debt strategy.

- ◾Alone among the Group of Seven countries, Canada continues to receive the highest possible credit ratings, with a stable outlook, from all the major credit rating agencies.

- ◾Locking in low-cost funding for 50 years benefits taxpayers.

Theophilos Argitis and Cecile Gutscher at Bloomberg tell us:

The government doubled the size of the sale to C$1.5 billion ($1.36 billion) and won a yield 1 basis point below its 3.5 percent 2045 benchmark bond, according to details released by underwriters including BMO Capital Markets, CIBC World Markets Inc., Desjardins Securities and TD Securities Inc. on the Canadian Syndication System.

“From the standpoint of demand from long-duration players like life insurance and pension funds, the duration of a 50-year bond is not much different than a 30-year bond,” said Adrian Miller, director of fixed-income strategies at GMP Securities LLC in New York, by e-mail.

Demand from pension funds is driving purchases of longer-dated bonds to lock in higher returns while also matching liabilities and cutting exposure to equity market volatility. Former Finance Minister Jim Flaherty unveiled the ultra-long bond proposal in the 2013-14 budget as the government said it wanted to extend the maturity of its borrowings with rates at near historic lows.

The bonds, due Dec. 1, 2064, have a 2.75 percent coupon and yield 2.96 percent, one basis point less than the government benchmark note due December 2045 at the time of pricing.

Next WE WANT PERPS! All together, folks! WE WANT PERPS!

Today’s featured business model for budding entrepreneurs is the mug shot game:

California lawmakers took steps on Monday to bar so-called extortion websites from posting mug shots of people who have been arrested and then demanding payment to remove the photographs, even from people who are never charged with a crime.

A bill to make it unlawful to solicit or accept payment to remove, correct or modify mug shots online was unanimously passed by the California state senate on Monday, in the latest effort by more than a dozen U.S. states to stop such practices.

…

In what legislative researchers for the senate called an unintended consequence of laws making mug shots and other arrest information available to the public, a growing industry has developed that publishes mug shots on a website and then charges those depicted in the photos to remove their images.

RioCan Real Estate Investment Trust, proud issuer of REI.PR.A and REI.PR.C, was confirmed at Pfd-3(high) by DBRS:

DBRS has today confirmed the ratings of RioCan Real Estate Investment Trust’s (RioCan or the Trust) Senior Unsecured Debentures and Senior Unsecured Debentures, Series 1, at BBB (high) and Preferred Trust Units at Pfd-3 (high), all with Stable trends. While the confirmation acknowledges RioCan’s steady growth in operating income and improvement in financial metrics over the past several years, the ratings continue to be constrained by the Trust’s high distribution payout ratio. DBRS notes that a positive rating action could occur, should the Trust continue to improve its EBITDA coverage (including capitalized interest) above 3.0 times (x) and lower its distribution payout ratio such that it is more consistent with the A (low) rating category.

…

In terms of financial profile, RioCan is expected to continue to pay out essentially all of its internally generated cash flow in the form of distributions. DBRS anticipates RioCan will continue to fund investments with proceeds from asset dispositions and debt as the Trust recycles its asset base toward high-quality properties in growing urban markets. As such, DBRS expects RioCan’s key financial metrics will improve modestly within the current rating category in the near term (EBITDA interest coverage in the 2.70x to 2.90x range), based on continued growth in operating income and lower weighted-average interest rate.

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts off 8bp, FixedResets up 7bp and DeemedRetractibles gaining 5bp. Volatility was average. Volume was above average.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0721 % | 2,411.2 |

| FixedFloater | 4.65 % | 3.89 % | 31,846 | 17.72 | 1 | -0.1468 % | 3,688.9 |

| Floater | 3.02 % | 3.17 % | 50,371 | 19.31 | 4 | 0.0721 % | 2,603.5 |

| OpRet | 4.35 % | -4.17 % | 34,458 | 0.09 | 2 | -0.0580 % | 2,699.9 |

| SplitShare | 4.80 % | 4.33 % | 62,863 | 4.21 | 5 | 0.0635 % | 3,090.3 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0580 % | 2,468.8 |

| Perpetual-Premium | 5.54 % | -5.62 % | 104,322 | 0.08 | 13 | -0.0393 % | 2,388.3 |

| Perpetual-Discount | 5.39 % | 5.38 % | 110,415 | 14.62 | 23 | -0.0817 % | 2,501.8 |

| FixedReset | 4.61 % | 3.50 % | 198,351 | 4.39 | 78 | 0.0653 % | 2,543.7 |

| Deemed-Retractible | 5.02 % | -2.22 % | 143,576 | 0.15 | 42 | 0.0459 % | 2,501.5 |

| FloatingReset | 2.67 % | 2.42 % | 181,581 | 4.06 | 5 | 0.1033 % | 2,484.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| IAG.PR.A | Deemed-Retractible | -1.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.35 Bid-YTW : 6.03 % |

| ELF.PR.H | Perpetual-Discount | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-04-28 Maturity Price : 24.09 Evaluated at bid price : 24.50 Bid-YTW : 5.64 % |

| MFC.PR.F | FixedReset | 1.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.48 Bid-YTW : 4.10 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| FTS.PR.H | FixedReset | 274,458 | Nesbitt crossed blocks of 226,900 and 15,000, both at 21.78. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-04-28 Maturity Price : 21.43 Evaluated at bid price : 21.75 Bid-YTW : 3.69 % |

| BMO.PR.S | FixedReset | 262,013 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2019-05-25 Maturity Price : 25.00 Evaluated at bid price : 25.49 Bid-YTW : 3.60 % |

| FTS.PR.G | FixedReset | 159,810 | Nesbitt crossed 156,300 at 24.90. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-04-28 Maturity Price : 23.16 Evaluated at bid price : 24.85 Bid-YTW : 3.78 % |

| MFC.PR.E | FixedReset | 117,613 | Nesbitt crossed 113,100 at 25.54. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-09-19 Maturity Price : 25.00 Evaluated at bid price : 25.52 Bid-YTW : 1.83 % |

| CM.PR.G | Perpetual-Premium | 102,212 | Nesbitt crossed 92,200 at 25.30. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-05-31 Maturity Price : 25.00 Evaluated at bid price : 25.22 Bid-YTW : -4.58 % |

| ENB.PR.T | FixedReset | 93,670 | TD crossed 80,000 at 24.50. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-04-28 Maturity Price : 23.00 Evaluated at bid price : 24.55 Bid-YTW : 4.16 % |

| There were 39 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PR.G | FixedFloater | Quote: 20.41 – 20.98 Spot Rate : 0.5700 Average : 0.3780 YTW SCENARIO |

| TRP.PR.A | FixedReset | Quote: 23.51 – 23.99 Spot Rate : 0.4800 Average : 0.3059 YTW SCENARIO |

| TD.PR.G | FixedReset | Quote: 24.99 – 25.30 Spot Rate : 0.3100 Average : 0.1713 YTW SCENARIO |

| MFC.PR.E | FixedReset | Quote: 25.52 – 25.83 Spot Rate : 0.3100 Average : 0.1935 YTW SCENARIO |

| ENB.PR.N | FixedReset | Quote: 25.01 – 25.30 Spot Rate : 0.2900 Average : 0.1940 YTW SCENARIO |

| ELF.PR.H | Perpetual-Discount | Quote: 24.50 – 24.75 Spot Rate : 0.2500 Average : 0.1670 YTW SCENARIO |