In honour of May Day, Ontario has a pre-election budget:

Opinion research suggests there are far more swing voters on the Liberals’ left than on their right. So the government’s agenda, which includes a 2014-15 deficit, significantly higher than the one previously forecast, all but abandons hope of appealing to moderate fiscal conservatives. Instead, it is mostly about competing with the NDP.

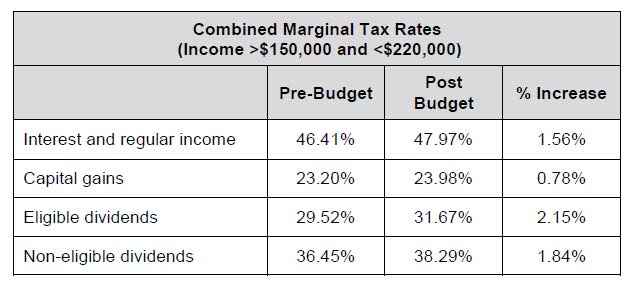

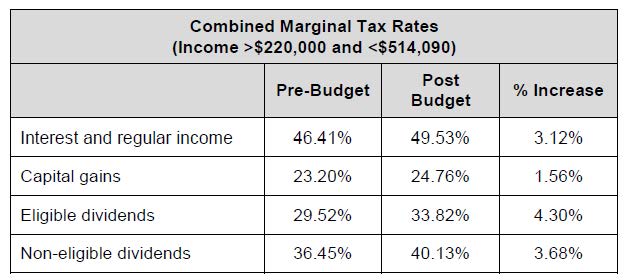

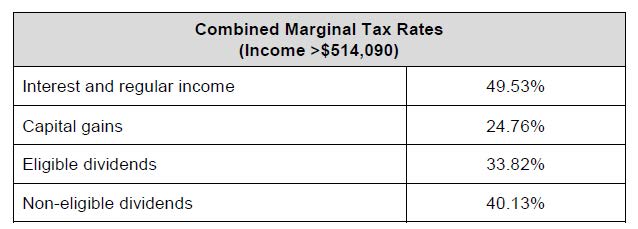

The budget proposes to lower the taxable income threshold for the 13.16% tax rate from $514,090 to $220,000. The budget also adds a new tax rate of 12.16% on taxable income between $150,000 and $220,000. These changes would apply to taxation years ending after December 31, 2013. The new income thresholds would not be adjusted for inflation each year.

Therefore, they estimate:

Click for Big

>

>

Click for Big

Click for Big

… whence we can calculate …

| Ontario 2014 Budget Proposal Effect on Eligible Dividend Equivalency Factors |

||

| Income Range |

Current | Proposed |

| $150-220M | 1.32 | 1.31 |

| $220-514M | 1.32 | 1.31 |

| >$514M | 1.31 | |

So fear not, preferred share fans! Business as usual.

KPMG continues:

The budget proposes a mandatory new provincial pension plan based on the Canada Pension Plan (CPP). The Ontario Retirement Pension Plan (ORPP), which would be introduced in 2017, is intended to provide additional retirement income. The ORPP would be publically administered at arm’s length from the Ontario government.

The plan would require equal contributions shared between employers and employees (not exceeding 1.9% each, or 3.8% in total) up to a maximum annual earnings threshold of $90,000. The threshold would increase each year, consistent with the CPP maximum earnings threshold. Benefits would be earned as contributions are made.

Enrolment into the ORPP would occur in stages, starting with large employers, with contribution rates phased-in over two years. Individuals that already participate in a similar workplace pension plan would not be required to enroll in the ORPP.

…

The budget proposes to introduce a new asset pooling entity to enable pooling pension plan assets in the public sector. The entity would operate at arm’s length from the government. Legislation is expected in spring 2015.

…

The government also said it intends to address the following pension issues:

• Target benefit pension plans

• Regulation of financial planning

• Changes to the funding rules.

Pooling pension plan assets is a well-intentioned dumb idea (see, for example, March 22, 2013). But there will be some nice jobs going for a few lucky arse-suckers; no performance necessary. However, I think auditions for the CEO role at ORPP have already been held, as discussed on October 16, 2013.

Janet McFarland of the Globe points out:

Unlike the CPP, the ORPP will not cover all workers in the province, the government said.

Instead, it will cover about half of Ontario’s 6 million-person work force, excluding the self-employed, all workers whose companies already offer workplace pension plans, and Ontarians working in federally regulated sectors like banking, transportation and telecommunications. The latter group cannot be included because the province does not have jurisdiction over pensions for workers in federal sectors, while the government is excluding those with existing workplace pension plans because it says the program is aimed at those who most need help saving for retirement.

KPMG continues with the revelation that farmers will be getting yet another government cheque:

The budget announces that Ontario will draft legislation to implement a non-refundable income tax credit for farmers who donate food to community food programs, including food banks for donations beginning January 1, 2014.

And there are the usual favourite targets:

The budget proposes to increase tobacco tax from 12.350 cents to 13.975 cents per cigarette (i.e., from $24.70 to $27.95 per carton of 200 cigarettes) and per gram of tobacco products (other than cigarettes or cigars). This measure would be effective 12:01am on May 2, 2014. As a result, wholesalers of tobacco tax are required to take an inventory of all tobacco products (except cigars) held at the end of May 1, 2014 and remit additional tax on this inventory.

…

The budget proposes to raise the tax on aviation fuel to 3.7 cents per litre (from 2.7 cents per litre) for 2014, with an additional tax increase of one cent per year until 2018. This measure is effective on Royal Assent, with subsequent rate increases effective on April 1 of 2015, 2016 and 2017.

The NYSE’s getting fined for not ticking sufficient boxes:

As SROs, the NYSE exchanges are required to conduct their operations in accordance and compliance with their own rules as well as the federal securities laws. They are required to file all proposed rules and rule changes with the Commission, which publishes them for public comment, before they take effect. This transparency enables all participants trading on the exchanges to understand how their orders are processed and executed.

According to the SEC’s order instituting settled administrative proceedings, the NYSE exchanges repeatedly engaged in business practices that either violated exchange rules or required a rule when the exchanges had none in effect. For example, all of the NYSE exchanges used an error account maintained at Archipelago Securities to trade out of securities positions taken on as a result of their operations despite not having rules in effect that permitted them to maintain and use such an account. In another example, NYSE Arca failed to execute a certain type of limit order under specified market conditions despite having a rule in effect that stated that NYSE Arca would execute such orders.

…

The SEC’s order finds that the NYSE exchanges violated Section 19(b) and 19(g) of the Securities Exchange Act of 1934 through misconduct that included the following:NYSE, NYSE Arca, and NYSE MKT (formerly NYSE Amex) used an error account maintained at Archipelago Securities to assume and trade out of securities positions without a rule in effect that permitted such trading and in a manner inconsistent with their rules for the routing broker, which limited Archipelago Securities’ activity primarily to outbound and inbound routing of orders on behalf of those exchanges.

NYSE provided co-location services to customers on disparate contractual terms without an exchange rule in effect that permitted and governed the provision of such services on a fair and equitable basis.

NYSE operated a block trading facility (New York Block Exchange) that for a period of time did not function in accordance with the rules submitted by NYSE and approved by the SEC.

NYSE distributed an automated feed of closing order imbalance information to its floor brokers at an earlier time than was specified in NYSE’s rules.NYSE Arca failed to execute Mid-Point Passive Liquidity Orders (MPLOs) in locked markets (where the bid and ask prices are the same) contrary to its exchange rule in effect at the time.

In addition, the SEC’s order finds that NYSE Arca accepted MPLOs in sub-penny amounts for National Market System stocks trading at over $1.00 per share, in violation of Rule 612(a) of Regulation NMS.

The SEC’s order further finds that Archipelago Securities failed to establish and maintain policies reasonably designed to prevent the misuse of material, nonpublic information in connection with error account trading.

Wow – that’s enough to make you faint, huh? I love that last one, it’s classic: Archipelago didn’t actually do anything wrong, they just failed to write down that they wouldn’t do anything wrong.

I was intrigued by an advertisement for a discussion at Rotman on OSFI … until I saw the speakers list:

Stanley Hartt, Counsel, Norton Rose Fulbright; former Deputy Minister of Finance Canada

Hon. Michael Wilson, former Minister of Finance of Canada; Chairman, Barclays Capital Canada Inc.; Chancellor, University of Toronto

Hon. Barbara McDougall, former Minister of State (Finance) of Canada

Smiley boys. Not a single practitioner. Not even a big-bank zombie who will toe the line nicely. Have a nice time.

Manulife’s 14Q1 Quarterly Report casts broad hints that MFC.PR.D will be redeemed:

If the Company redeems, subject to regulatory approval, $450 million of preferred shares which will become redeemable at par in June, we would expect a further 3 point decline in the MCCSR ratio.

Mind you, a redemption of MFC.PR.D (FixedReset, 6.60%+456) will not actually surprise anybody.

In common with the Ontario government, the Canadian preferred share market celebrated May Day with a very nice pop; PerpetualDiscounts winning 50bp, FixedResets gaining 22bp and DeemedRetractibles up 23bp. Volatility was suitably present, with Floating Rate issues getting hit (gee, I guess the yanking of government policy rates has been postponed again). Volume was above average.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.8667 % | 2,383.1 |

| FixedFloater | 4.63 % | 3.86 % | 30,731 | 17.76 | 1 | -0.2913 % | 3,712.4 |

| Floater | 3.06 % | 3.20 % | 50,589 | 19.22 | 4 | -0.8667 % | 2,573.1 |

| OpRet | 4.35 % | -7.65 % | 33,842 | 0.09 | 2 | 0.0774 % | 2,701.0 |

| SplitShare | 4.79 % | 4.41 % | 64,508 | 4.20 | 5 | -0.0475 % | 3,095.2 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0774 % | 2,469.8 |

| Perpetual-Premium | 5.53 % | -6.05 % | 100,223 | 0.08 | 15 | 0.0367 % | 2,393.1 |

| Perpetual-Discount | 5.32 % | 5.38 % | 116,194 | 14.86 | 21 | 0.4975 % | 2,527.8 |

| FixedReset | 4.52 % | 3.43 % | 210,691 | 4.15 | 75 | 0.2171 % | 2,557.2 |

| Deemed-Retractible | 4.99 % | -4.45 % | 144,871 | 0.15 | 42 | 0.2335 % | 2,516.3 |

| FloatingReset | 2.68 % | 2.29 % | 135,783 | 4.22 | 6 | 0.0396 % | 2,494.6 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.B | Floater | -1.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-01 Maturity Price : 16.47 Evaluated at bid price : 16.47 Bid-YTW : 3.21 % |

| BAM.PR.K | Floater | -1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-01 Maturity Price : 16.43 Evaluated at bid price : 16.43 Bid-YTW : 3.22 % |

| CU.PR.D | Perpetual-Discount | 1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-01 Maturity Price : 23.96 Evaluated at bid price : 24.35 Bid-YTW : 5.09 % |

| POW.PR.D | Perpetual-Discount | 1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-01 Maturity Price : 23.42 Evaluated at bid price : 23.72 Bid-YTW : 5.30 % |

| ENB.PR.B | FixedReset | 1.16 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-06-01 Maturity Price : 25.00 Evaluated at bid price : 25.24 Bid-YTW : 3.92 % |

| TRP.PR.B | FixedReset | 1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-01 Maturity Price : 21.16 Evaluated at bid price : 21.16 Bid-YTW : 3.60 % |

| PWF.PR.L | Perpetual-Discount | 1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-01 Maturity Price : 24.25 Evaluated at bid price : 24.55 Bid-YTW : 5.21 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BNS.PR.Q | FixedReset | 113,795 | TD crossed blocks of 50,000 and 60,000, both at 25.55. YTW SCENARIO Maturity Type : Call Maturity Date : 2018-10-25 Maturity Price : 25.00 Evaluated at bid price : 25.52 Bid-YTW : 3.13 % |

| RY.PR.L | FixedReset | 100,175 | TD crossed blocks of 50,000 and 30,000, both at 26.55. YTW SCENARIO Maturity Type : Call Maturity Date : 2019-02-24 Maturity Price : 25.00 Evaluated at bid price : 26.52 Bid-YTW : 2.85 % |

| TD.PR.K | FixedReset | 75,783 | TD crossed 62,900 at 25.33. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-07-31 Maturity Price : 25.00 Evaluated at bid price : 25.29 Bid-YTW : 1.67 % |

| TD.PR.O | Deemed-Retractible | 74,091 | TD crossed 60,600 at 25.76. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-05-31 Maturity Price : 25.25 Evaluated at bid price : 25.65 Bid-YTW : -13.69 % |

| GWO.PR.F | Deemed-Retractible | 63,688 | TD crossed 60,000 at 25.45. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-05-31 Maturity Price : 25.00 Evaluated at bid price : 25.42 Bid-YTW : -8.36 % |

| BAM.PF.E | FixedReset | 56,905 | Scotia crossed 35,000 at 25.10. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-01 Maturity Price : 23.14 Evaluated at bid price : 25.10 Bid-YTW : 4.19 % |

| There were 41 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| GWO.PR.I | Deemed-Retractible | Quote: 22.44 – 22.99 Spot Rate : 0.5500 Average : 0.3403 YTW SCENARIO |

| CU.PR.F | Perpetual-Discount | Quote: 22.40 – 22.86 Spot Rate : 0.4600 Average : 0.2808 YTW SCENARIO |

| HSB.PR.C | Deemed-Retractible | Quote: 25.29 – 25.59 Spot Rate : 0.3000 Average : 0.1812 YTW SCENARIO |

| TD.PR.R | Deemed-Retractible | Quote: 26.63 – 26.98 Spot Rate : 0.3500 Average : 0.2381 YTW SCENARIO |

| POW.PR.B | Perpetual-Discount | Quote: 24.64 – 24.96 Spot Rate : 0.3200 Average : 0.2130 YTW SCENARIO |

| PWF.PR.E | Perpetual-Premium | Quote: 25.20 – 25.50 Spot Rate : 0.3000 Average : 0.2152 YTW SCENARIO |