Bank of Montreal has announced:

a Basel III-compliant domestic public offering of $300 million of Non-Cumulative 5-Year Rate Reset Class B Preferred Shares Series 31 (the “Preferred Shares Series 31”). The offering will be underwritten on a bought-deal basis by a syndicate of underwriters led by BMO Capital Markets.

The Preferred Shares Series 31 will be issued to the public at a price of $25.00 per share. Holders will be entitled to receive non-cumulative preferential fixed quarterly dividends for the initial period ending November 25, 2019, as and when declared by the board of directors of the Bank, payable in the amount of $0.2375 per share, to yield 3.80 per cent annually.

Subject to regulatory approval, on or after November 25, 2019, the Bank may redeem the Preferred Shares Series 31 in whole or in part at par. On November 25, 2019, the dividend rate will reset and will reset thereafter every five years to be equal to the 5-Year Government of Canada Bond Yield plus 2.22 per cent. Subject to certain conditions, holders may elect to convert any or all of their Preferred Shares Series 31 into an equal number of Non-Cumulative Floating Rate Class B Preferred Shares Series 32 (“Preferred Shares Series 32”) on November 25, 2019, and on November 25 of every fifth year thereafter. Holders of the Preferred Shares Series 32 will be entitled to receive non-cumulative preferential floating rate quarterly dividends, as and when declared by the board of directors of the Bank, equal to the then 3-month Government of Canada Treasury Bill yield plus 2.22 per cent. Subject to certain conditions, holders may elect to convert any or all of their Preferred Shares Series 32 into an equal number of Preferred Shares Series 31 on November 25, 2024, and on November 25 of every fifth year thereafter.

The anticipated closing date is July 30, 2014. The net proceeds from the offering will be used by the Bank for general corporate purposes.

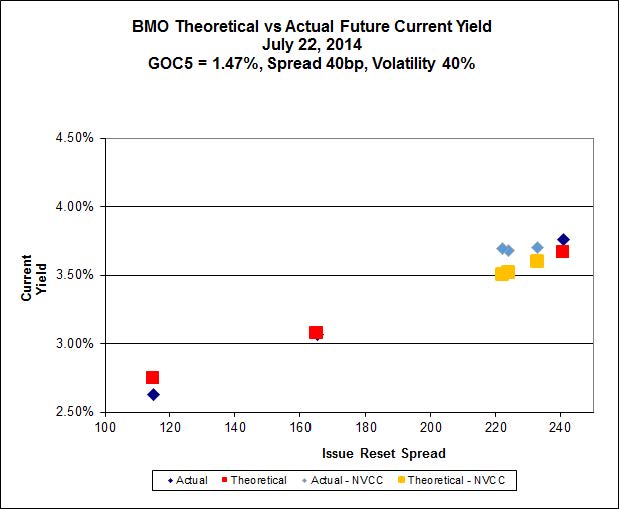

The Implied Volatility calculation for BMO FixedResets is very interesting – it appears that the slope of the three NVCC-compliant issues is much less than the 40% calculation that is obtained when all issues, including those which are not NVCC-compliant and therefore virtually certain to be called on one of the next two possible dates – are thrown into the mix.

Click for Big

Of course, the range of Issue Reset Spreads for the NVCC compliant issues is very small, and the issue price has been used for the new issue calculations, so one cannot draw many conclusions just yet, but … we will see!