Nothing happened today, but there was a nice column from Megan McArdle of Bloomberg regarding the Intregity case before SCOTUS that I mentioned on October 3:

But the law is never simple and intuitive, in large part because case law is made by the difficulty of hard corner cases. The briefs run through some of this history. For example: Does your employer have to pay you for your commuting time? That doesn’t seem reasonable; employees could relocate to the far exurbs and get themselves time and a half for hours spent driving and singing along to “Free Fallin’.” Okay, but what if you work in an airport, and at the end of your commute is a lengthy trip through the Transportation Security Administration lines? Should you get paid for what is essentially a mandatory 15 minutes added to your commute? A court said no; the TSA line is not part of your primary duties. Okay, how about if you work in a nuclear power plant, where, for the sake of the neighbors, everyone is rigorously searched and subject to radiation screenings? I can see the workers’ argument there, but a court ruled against them.

The workers’ brief tries to distinguish those cases from the Amazon case. The TSA case seems pretty easy: The security screening is not there for the benefit of the employer; it’s there because it’s required by law. You can’t demand that your employer pay you for commuting just because they’re located in the middle of an extended 15-mph zone. The security checks at the Amazon warehouse, on the other hand, are exclusively for the benefit of the employer, who is trying to prevent theft.

It was a positive day for the Canadian preferred share market, with PerpetualDiscounts winning 11bp, FixedResets gaining 3bp and DeemedRetractibles up 5bp. Volatility was minimal. Volume was very low.

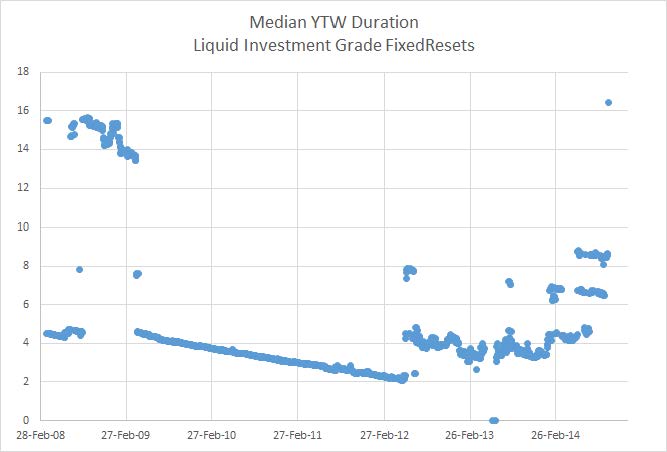

Interestingly, due to microscopic pricing changes, the median YTW-Duration (the YTW-Duration is the duration of the Yield-to-Worst scenario) of the FixedReset subindex is now in the ‘perpetual’ range, for the first time since April, 2009. After recovering from the pricing slump that gave rise to that scenario, there followed a long period during which the bulk of the issues in the index were the huge-spread bank FixedResets, which reduced their expected term by one day every day. In May, 2012, new issuance started making things more interesting with a series in the range of four (median expectation was a call of a relatively new issue at the first opportunity), a series starting at eight and declining to about 6.5 (median expectation is the Deemed Maturity of a bank issue 2022-1-31) and a third, relatively recent series at about 8.5 (median expectation is the Deemed Maturity of an insurance issue, 2025-1-31). And today … continued low yields for the Government of Canada 5-year bond, massive issuance of relatively low-spread FixedResets and calls of the higher-spread issues have tipped the balance to perpetuity. Fun times! This median YTW-Duration figure will almost certainly be volatile for the next year or so.

Click for Big

For those who are obsessive about such things, the median issue is BAM.PF.F, which at its bid of 25.25, HIMIPref™ calculates as having a 4.32% yield to Call 2019-9-30 and (given a GOC-5 yield of 1.58%), has a yield to perpetuity of 4.31%. At its closing bid of 25.26 on Friday, its YTW scenario was the call 2019-9-30 to yield 4.30%; I was using 1.61% as the GOC-5 yield on Friday. I told you the changes were microscopic!

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 3.12 % | 3.11 % | 23,252 | 19.46 | 1 | 0.0833 % | 2,675.9 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0138 % | 4,123.9 |

| Floater | 2.89 % | 3.04 % | 59,187 | 19.66 | 4 | 0.0138 % | 2,769.1 |

| OpRet | 4.04 % | 0.57 % | 107,599 | 0.08 | 1 | 0.1975 % | 2,734.6 |

| SplitShare | 4.30 % | 4.04 % | 90,913 | 3.86 | 5 | -0.0558 % | 3,143.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1975 % | 2,500.5 |

| Perpetual-Premium | 5.47 % | 0.12 % | 79,085 | 0.08 | 18 | 0.0852 % | 2,448.8 |

| Perpetual-Discount | 5.32 % | 5.14 % | 95,476 | 15.09 | 18 | 0.1149 % | 2,587.4 |

| FixedReset | 4.21 % | 3.74 % | 174,527 | 16.41 | 73 | 0.0256 % | 2,554.6 |

| Deemed-Retractible | 5.02 % | 2.29 % | 103,280 | 0.23 | 42 | 0.0477 % | 2,563.1 |

| FloatingReset | 2.57 % | -7.01 % | 80,929 | 0.08 | 6 | 0.0704 % | 2,554.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| CIU.PR.C | FixedReset | -1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-10-06 Maturity Price : 20.51 Evaluated at bid price : 20.51 Bid-YTW : 3.71 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PF.A | FixedReset | 48,112 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-10-06 Maturity Price : 23.17 Evaluated at bid price : 25.05 Bid-YTW : 3.70 % |

| TD.PF.B | FixedReset | 41,338 | Scotia crossed 10,000 at 25.08. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-10-06 Maturity Price : 23.19 Evaluated at bid price : 25.04 Bid-YTW : 3.70 % |

| RY.PR.A | Deemed-Retractible | 41,292 | TD crossed 35,000 at 25.40. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-05-24 Maturity Price : 25.00 Evaluated at bid price : 25.40 Bid-YTW : 2.70 % |

| FTS.PR.M | FixedReset | 37,510 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-10-06 Maturity Price : 23.19 Evaluated at bid price : 25.12 Bid-YTW : 3.95 % |

| BAM.PF.C | Perpetual-Discount | 30,497 | RBC crossed 24,700 at 21.50. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-10-06 Maturity Price : 21.48 Evaluated at bid price : 21.48 Bid-YTW : 5.69 % |

| ENB.PR.F | FixedReset | 29,824 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-10-06 Maturity Price : 23.04 Evaluated at bid price : 24.35 Bid-YTW : 4.13 % |

| There were 18 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| CIU.PR.C | FixedReset | Quote: 20.51 – 21.24 Spot Rate : 0.7300 Average : 0.5827 YTW SCENARIO |

| BAM.PR.E | Ratchet | Quote: 24.04 – 24.45 Spot Rate : 0.4100 Average : 0.2970 YTW SCENARIO |

| PWF.PR.R | Perpetual-Premium | Quote: 25.94 – 26.30 Spot Rate : 0.3600 Average : 0.2499 YTW SCENARIO |

| POW.PR.C | Perpetual-Premium | Quote: 25.35 – 25.58 Spot Rate : 0.2300 Average : 0.1589 YTW SCENARIO |

| BAM.PF.B | FixedReset | Quote: 24.67 – 24.95 Spot Rate : 0.2800 Average : 0.2098 YTW SCENARIO |

| BAM.PF.D | Perpetual-Discount | Quote: 21.68 – 21.89 Spot Rate : 0.2100 Average : 0.1458 YTW SCENARIO |