So today the Prime Minister’s Office admitted the oil price drop is bad via one of its flunkies:

The plunge in oil prices is “on the whole” a negative for Canada’s economy and may delay its return to full potential, Bank of Canada Deputy Governor Tim Lane said.

“We will closely monitor its broader impacts on growth and the delay it may cause to the economy’s return to its production potential,” Lane said in a speech today in Madison, Wisconsin.

Economists are interpreting his remarks as confirmation the central bank will hold off raising interest rates for the time being. Governor Stephen Poloz and fellow members of the bank’s governing council will publish their next rate decision on Jan. 21, along with a quarterly policy report that will provide a detailed impact analysis of falling oil prices.

…

Canada’s dollar rose 0.2 percent to C$1.1953 per U.S. dollar at 3:58 p.m. Toronto time. It has depreciated by more than 10 percent in the last six months, as the price of benchmark crude oil has plunged 54 percent. A depreciating currency makes Canadian goods cheaper to foreign customers.“Despite the mitigating factors I enumerated, lower oil prices are likely, on the whole, to be bad for Canada,” Lane said. “Estimating the magnitude of that overall impact requires carefully analyzing the interplay between the various effects as they work through the economy.”

Suncor Energy Inc. (SU), Canada’s largest oil company, said it will cut 1,000 jobs, lower its 2015 capital budget by about 13 percent and delay projects to weather collapsing prices.

The company will spend C$1 billion ($836 million) less this year than originally forecast in November, following Canadian Natural Resources Ltd. (CNQ) in revising its budget lower this week. Suncor also plans to reduce operating expenses by C$600 million to C$800 million in two years, according to a company statement today.

So what do you do when you have too much oil?

Refiners, tankage firms and traders that invested in oil storage capacity are benefiting as the slump in crude to below $45 a barrel deepened what’s called contango, a relatively rare situation where prices for oil delivery later this year are higher than current prices. Vitol Group, Mercuria Energy Group Ltd. and Gunvor Group Ltd. are among the commodity houses poised to profit by storing oil and petroleum products to sell in the future.

“There is significant storage demand from traders wanting to cash in on that specific opportunity,” Martijn den Drijver, an analyst at SNS Securities in Amsterdam, said in an interview.

Mercuria, the fourth-largest independent oil trader, owns about 40 million barrels of storage in locations from Texas, South Africa and China to Belgium and the Netherlands, according to its website. The firm is looking primarily at its land-based storage facilities to play the contango, said Matt Lauer, a spokesman for the company with major trading operations in Geneva. Mercuria hasn’t moved to secure any floating storage in tankers at sea

I mentioned the Caisse’s intention to build transit in Quebec yesterday. DBRS is sanguine, but assumes independence:

DBRS Limited (DBRS) today notes that the Caisse de dép?t et placement du Québec (the Caisse) has entered into an agreement with the Government of Québec (the Government) to execute major infrastructure projects in the province. This new agreement is consistent with the Caisse’s strategy to grow its private market holdings, particularly infrastructure investments, amid the current low interest rate environment. Further, it allows the Caisse to capitalize on its unique understanding of the Québec market and address growing infrastructure needs in the province. Additionally, the Caisse’s current Québec concentration levels will not be affected. DBRS notes that the agreement is of a commercial nature, and importantly, the independence of the Caisse is a key feature and is by no means compromised by this agreement. This move has no implications on DBRS’s current ratings of the Caisse or its financing subsidiary, CDP Financial Inc.

…

Operationalization of the agreement will be dependent upon the introduction of legislative amendments, which is expected in the coming months. The new legislation will allow for the creation of the new infrastructure subsidiary, CDPQ Infra. Also, it will expand the Caisse’s current practice of merely investing in infrastructure projects, to accommodate the new business model, which will include project planning, development, construction and operation. Once established, it is expected that over time CDPQ Infra will expand its mandate to build, finance and operate infrastructure projects globally.

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts gaining 8bp, FixedResets down 55bp and DeemedRetractibles off 2bp. The Performance Highlights table is suitably lengthy with quite a few FixedReset losers and one solitary winner – a PerpetualDiscount. Volume was very low.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

- based on Implied Volatility Theory only

- are relative only to other FixedResets from the same issuer

- assume constant GOC-5 yield

- assume constant Implied Volatility

- assume constant spread

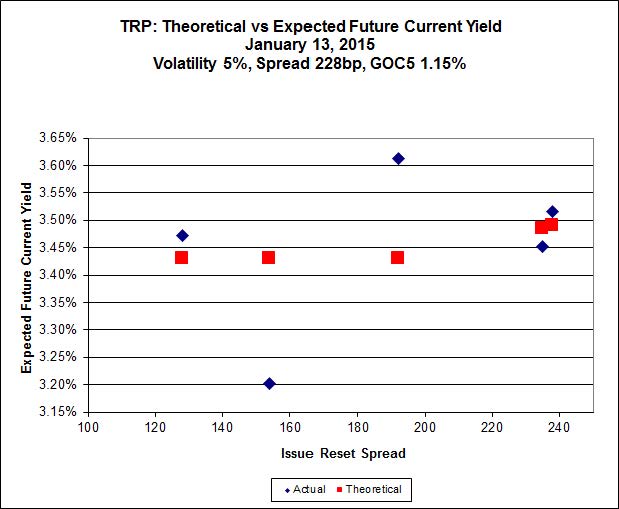

Here’s TRP:

Click for Big

So according to this, TRP.PR.A, bid at 21.66, is $1.12 cheap, but it has already reset (at +192). TRP.PR.C, bid at 21.00 and resetting at +154bp on 2016-1-30 is $1.39 rich.

Click for Big

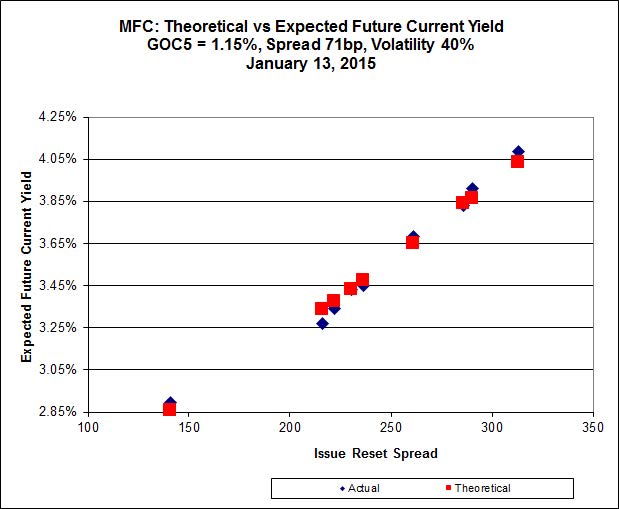

MFC.PR.F continues to be on the line defined by its peers. Implied Volatility continues to be a conundrum. It is far too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Click for Big

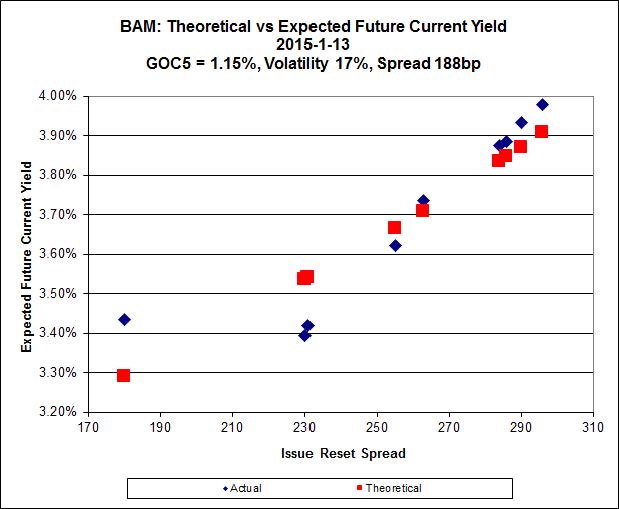

There continues to be cheapness in the lowest-spread issue, BAM.PR.X, resetting at +180bp on 2017-6-30, which is bid at 21.48 and appears to be $0.94 cheap, while BAM.PR.R, resetting at +230bp 2016-6-30 is bid at 25.41 and appears to be $1.02 rich.

It seems clear that the higher-spread issues define a curve with significantly more Implied Volatility than is calculated when the low-spread outlier is included.

Click for Big

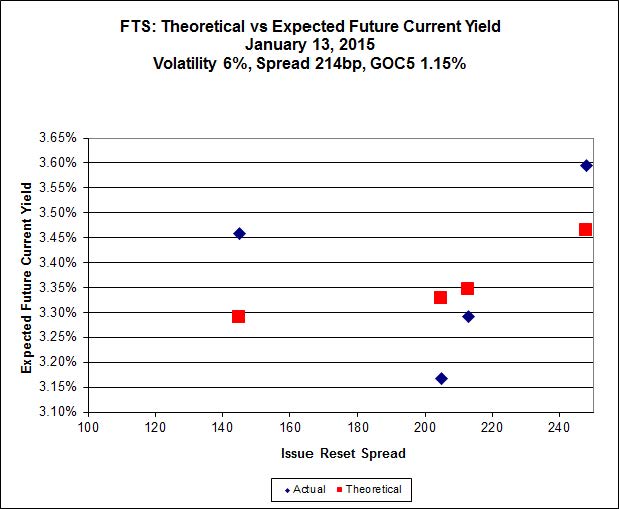

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 18.80, looks $0.96 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp, and bid at 25.26, looks $1.23 expensive and resets 2019-3-1

Click for Big

Pairs equivalence is all over the map.

And, yeah, Bell is still having network problems, and I am still using my ‘phone as a Wi-Fi hotspot. But don’t worry! Our beloved government will continue to protect us from the evils of American competition, so nobody will lose his job over this fiasco.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.9206 % | 2,561.9 |

| FixedFloater | 4.44 % | 3.62 % | 21,713 | 18.27 | 1 | -0.0115 % | 3,983.3 |

| Floater | 2.96 % | 3.07 % | 56,883 | 19.57 | 4 | -0.9206 % | 2,723.5 |

| OpRet | 4.04 % | 1.43 % | 97,225 | 0.43 | 1 | 0.0000 % | 2,755.3 |

| SplitShare | 4.25 % | 3.95 % | 35,160 | 3.63 | 5 | 0.2187 % | 3,212.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 2,519.4 |

| Perpetual-Premium | 5.44 % | -4.90 % | 57,908 | 0.08 | 19 | 0.0620 % | 2,498.5 |

| Perpetual-Discount | 5.15 % | 5.03 % | 101,405 | 15.36 | 16 | 0.0793 % | 2,690.0 |

| FixedReset | 4.20 % | 3.48 % | 203,213 | 16.70 | 77 | -0.5543 % | 2,549.3 |

| Deemed-Retractible | 4.95 % | 0.85 % | 100,479 | 0.13 | 39 | -0.0244 % | 2,620.5 |

| FloatingReset | 2.69 % | 1.97 % | 61,140 | 3.44 | 7 | -0.3894 % | 2,486.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BNS.PR.Y | FixedReset | -4.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.50 Bid-YTW : 3.90 % |

| PWF.PR.A | Floater | -2.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-13 Maturity Price : 19.76 Evaluated at bid price : 19.76 Bid-YTW : 2.68 % |

| IFC.PR.A | FixedReset | -2.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.11 Bid-YTW : 4.86 % |

| ENB.PR.F | FixedReset | -2.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-13 Maturity Price : 22.41 Evaluated at bid price : 23.02 Bid-YTW : 4.11 % |

| PWF.PR.P | FixedReset | -2.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-13 Maturity Price : 21.23 Evaluated at bid price : 21.23 Bid-YTW : 3.41 % |

| BAM.PR.X | FixedReset | -1.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-13 Maturity Price : 21.48 Evaluated at bid price : 21.48 Bid-YTW : 3.76 % |

| ENB.PR.D | FixedReset | -1.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-13 Maturity Price : 22.09 Evaluated at bid price : 22.48 Bid-YTW : 4.09 % |

| HSE.PR.A | FixedReset | -1.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-13 Maturity Price : 20.80 Evaluated at bid price : 20.80 Bid-YTW : 3.67 % |

| ENB.PR.N | FixedReset | -1.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-13 Maturity Price : 22.53 Evaluated at bid price : 23.32 Bid-YTW : 4.17 % |

| MFC.PR.B | Deemed-Retractible | -1.81 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.84 Bid-YTW : 5.32 % |

| ENB.PR.Y | FixedReset | -1.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-13 Maturity Price : 21.67 Evaluated at bid price : 22.02 Bid-YTW : 4.22 % |

| TRP.PR.F | FloatingReset | -1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-13 Maturity Price : 21.34 Evaluated at bid price : 21.62 Bid-YTW : 3.24 % |

| BAM.PR.T | FixedReset | -1.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-13 Maturity Price : 23.64 Evaluated at bid price : 25.30 Bid-YTW : 3.48 % |

| BAM.PR.R | FixedReset | -1.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-13 Maturity Price : 23.89 Evaluated at bid price : 25.41 Bid-YTW : 3.49 % |

| IFC.PR.C | FixedReset | -1.65 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2016-09-30 Maturity Price : 25.00 Evaluated at bid price : 25.60 Bid-YTW : 2.86 % |

| BAM.PF.B | FixedReset | -1.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-13 Maturity Price : 23.32 Evaluated at bid price : 25.30 Bid-YTW : 3.76 % |

| TRP.PR.A | FixedReset | -1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-13 Maturity Price : 21.25 Evaluated at bid price : 21.25 Bid-YTW : 3.75 % |

| ENB.PR.T | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-13 Maturity Price : 22.15 Evaluated at bid price : 22.72 Bid-YTW : 4.17 % |

| FTS.PR.H | FixedReset | -1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-13 Maturity Price : 18.80 Evaluated at bid price : 18.80 Bid-YTW : 3.62 % |

| FTS.PR.M | FixedReset | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-13 Maturity Price : 23.25 Evaluated at bid price : 25.25 Bid-YTW : 3.65 % |

| CU.PR.E | Perpetual-Discount | 1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-13 Maturity Price : 24.18 Evaluated at bid price : 24.60 Bid-YTW : 5.02 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BNS.PR.Y | FixedReset | 202,830 | Scotia crossed 200,000 at 23.48. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.50 Bid-YTW : 3.90 % |

| ENB.PR.N | FixedReset | 124,932 | Nesbitt crossed 117,900 at 23.55. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-13 Maturity Price : 22.53 Evaluated at bid price : 23.32 Bid-YTW : 4.17 % |

| ENB.PF.G | FixedReset | 120,513 | Nesbitt crossed 117,900 at 24.57. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-13 Maturity Price : 22.95 Evaluated at bid price : 24.50 Bid-YTW : 4.06 % |

| BMO.PR.P | FixedReset | 107,124 | RBC crossed 100,000 at 25.40. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-02-25 Maturity Price : 25.00 Evaluated at bid price : 25.35 Bid-YTW : -0.33 % |

| POW.PR.G | Perpetual-Premium | 91,647 | TD crossed 40,000 at 26.25. RBC crossed 50,000 at the same price. YTW SCENARIO Maturity Type : Call Maturity Date : 2021-04-15 Maturity Price : 25.00 Evaluated at bid price : 26.21 Bid-YTW : 4.72 % |

| GWO.PR.P | Deemed-Retractible | 45,825 | TD crossed 40,000 at 25.85. YTW SCENARIO Maturity Type : Call Maturity Date : 2020-03-31 Maturity Price : 25.25 Evaluated at bid price : 25.95 Bid-YTW : 4.81 % |

| There were 14 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BNS.PR.Y | FixedReset | Quote: 22.50 – 23.45 Spot Rate : 0.9500 Average : 0.5676 YTW SCENARIO |

| ENB.PR.N | FixedReset | Quote: 23.32 – 23.84 Spot Rate : 0.5200 Average : 0.3432 YTW SCENARIO |

| PWF.PR.A | Floater | Quote: 19.76 – 20.75 Spot Rate : 0.9900 Average : 0.8253 YTW SCENARIO |

| ENB.PR.D | FixedReset | Quote: 22.48 – 22.85 Spot Rate : 0.3700 Average : 0.2220 YTW SCENARIO |

| BAM.PF.B | FixedReset | Quote: 25.30 – 25.69 Spot Rate : 0.3900 Average : 0.2487 YTW SCENARIO |

| GWO.PR.I | Deemed-Retractible | Quote: 23.42 – 23.84 Spot Rate : 0.4200 Average : 0.2968 YTW SCENARIO |