For those who missed it, Bloomberg has an admirable piece on the some explanations of the global bond rout:

Between the ECB’s bond buying and the threat of deflation, yields across Europe started to go negative this year, meaning investors were essentially paying for the privilege to lend their money out. That created a spill over effect into bond markets in the rest of the world as investors went in search of a better deal, pulling yields down in those markets too. The average yield across all Germany’s debt went negative about three weeks ago. That seems to have been the straw that broke the camel’s back. Since then that average yield has climbed to the highest level this year. Yields on about $2 trillion of bonds across 12 countries still linger below zero.

The US Department of So-Called Justice has decided a little more regulatory extortion is never a bad thing:

The U.S. Justice Department is set to rip up its agreement not to prosecute UBS Group AG for rigging benchmark interest rates, according to a person familiar with the matter, taking a new step to hold banks accountable for repeat offenses.

The move by the U.S. would be a first for the industry, making good on a March threat by a senior Justice Department official to revoke such agreements and putting banks on notice that these accords can be unwound if misconduct continues.

…

UBS’s cooperation in the currency probe may help shield it from antitrust charges in that matter. However, the bank is still exposed to fraud charges in that case, and any admission of wrongdoing could also put it in violation of an earlier deal the Zurich-based bank struck with the Justice Department.In a December 2012 non-prosecution agreement with the U.S. to resolve a worldwide investigation into the manipulation of the London interbank offered rate, or Libor, UBS promised not to commit crimes for two years.

Don’t bet your bottom dollar on Chicago, Chicago:

Chicago had its credit rating cut to junk by Moody’s Investors Service after the Illinois Supreme Court’s rejection of a state pension-overhaul plan reduced the city’s options for fixing its own underfunded system.

The two-level downgrade to Ba1 affects $8.1 billion of general obligations, which were already the lowest-rated among the 90 biggest U.S. cities, excluding Detroit. The outlook is still negative. Moody’s has dropped the city seven levels since July 2013.

…

The deterioration in the credit standing of the third-most-populous U.S. city underscores how pension promises are squeezing the finances of states and localities nationwide. Moody’s downgrade compounds Chicago’s fiscal struggles: its counterparties can immediately demand as much as $2.2 billion in accelerated principal, accrued interest and termination fees, New York-based Moody’s said in the report.

There’s an interesting piece on Bloomberg about using technology to compete with cheap labour:

A few years ago, in an effort to diversify his company’s offerings, Pomini teamed up with Selvaggia Armani, an artist and designer. The two began working on a series of lamps designed by Armani and manufactured to order on Pomini’s 3D printers. The pieces—some of which include intricate meshwork or interlocking chains that would be difficult to produce using traditional methods—take shape slowly, each layer fused from powdered nylon by a high-power laser. The project was a surprising success: Pomini now works with more than a dozen designers; he introduced 3Dprinted jewelry in 2012. “This is the beauty of this technology,” says Armani, 47. “You can build things that are impossible.”

…

Armani have helped turn northeastern Italy into an unlikely hothouse of innovation. Last year growth in the region was positive for the first time since 2007, at 0.5 percent. Exports rose by 3.5 percent in 2014 and are expected to keep climbing. In the province of Trento, for instance, the public and private sectors together invest some 2 percent of gross domestic product in research and development. At the Centro Moda Canossa—a trade school in Trento for children age 14 to 18 specializing in fashion design and tailoring—the faculty recently added a class in which students incorporate 3D printing, laser cutting, and microcontroller chips into their designs. “You can’t offer a job from the past. Nobody will come,” says Michele Bommassar, 36, the school’s vice director. “You have to offer the jobs of the future.”

Is anybody in Canada listening? No? OK, go back to sleep, then. You’ll want to be rested for the anti-globalization demo.

In other news, Hydro One, having achieved the pinnacle of operating efficiency, has decided to join the Junior Justice League:

A Hydro One employee will be fired following an incident on Sunday when a female television reporter was harassed by Toronto FC fans hurling obscenities while she was doing a live hit.

“Hydro One is taking steps to terminate the employee for violating our Code of Conduct,” Hydro One spokesman Daffyd Roderick said in a statement.

“Respect for all people is ingrained in the code and our values. We are committed to a work environment where discrimination or harassment of any type is met with zero tolerance.”

So now, not only will universities like Dalhousie be able to administer the extra-judicial flavour of the month (as discussed on January 6) but any two-bit corporation will be able to do the same. So we are beginning to see a reversion to the good old days, when your employer had the ability to regulate every aspect of your life … it will be interesting to learn when unions become popular again, which will happen as soon as enough people get fed up with the abuse and fearful of its consequences – especially when it results from an essentially random occurance of internet pile-on.

It was a negative day for the Canadian preferred share market, with PerpetualDiscounts losing 26bp, FixedResets off 4bp and DeemedRetractibles down 8bp. FixedResets dominated both ends of the Performance Highlights table. Volume was extremely high.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

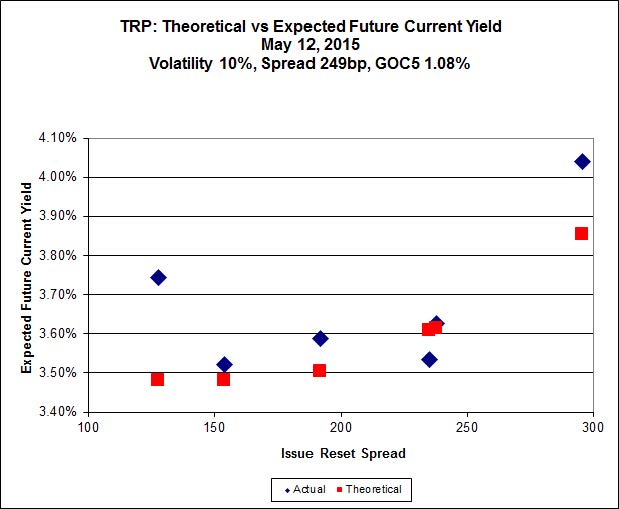

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 24.26 to be $0.49 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $1.21 cheap at its bid price of 25.00.

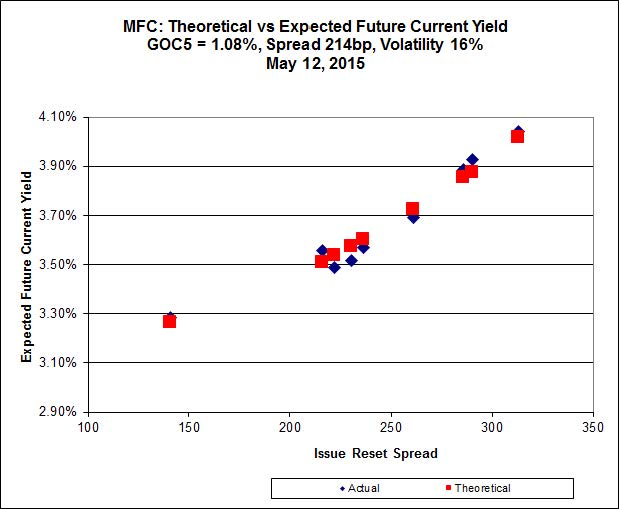

Click for Big

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.N, resetting at +230 on 2020-3-19, bid at 24.04 to be $0.40 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 25.33 to be $0.35 cheap.

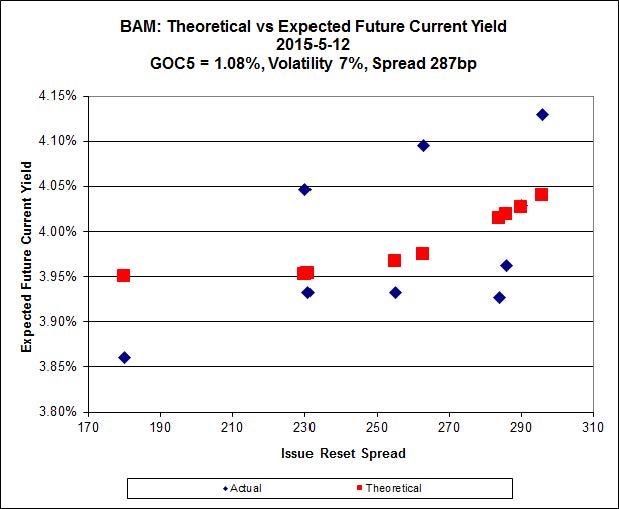

Click for Big

The cheapest issue relative to its peers is BAM.PF.B, resetting at +263bp on 2019-3-31, bid at 22.65 to be $0.69 cheap. BAM.PF.G, resetting at +284bp 2020-6-30 is bid at 24.96 and appears to be $0.55 rich.

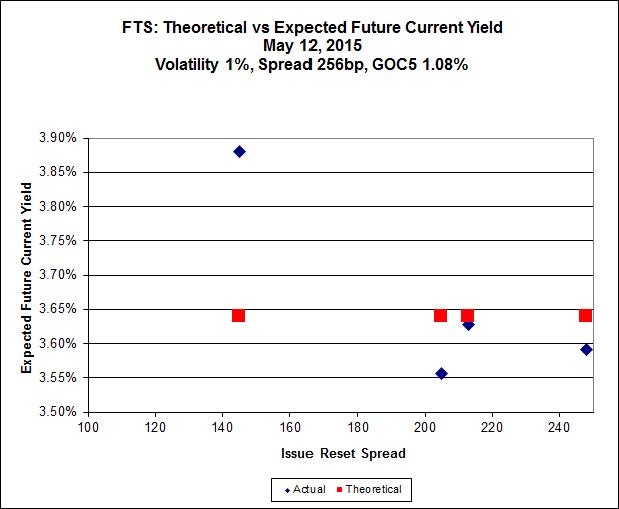

Click for Big

FTS.PR.H, with a spread of +145bp, and bid at 16.30, looks $1.08 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 22.00 and is $0.50 rich.

Click for Big

Investment-grade pairs predict an average over the next five-odd years of about 0.40%, but TRP.PR.A / TRP.PR.F remains an outlier at -0.39%. On the junk side, the FFH.PR.E / FFH.PR.F pair is at -1.12%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1104 % | 2,309.1 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1104 % | 4,037.3 |

| Floater | 3.14 % | 3.27 % | 54,838 | 19.02 | 4 | 0.1104 % | 2,454.7 |

| OpRet | 4.41 % | -2.65 % | 39,132 | 0.14 | 2 | 0.1178 % | 2,771.8 |

| SplitShare | 4.58 % | 4.80 % | 59,082 | 3.34 | 3 | -0.3594 % | 3,221.6 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1178 % | 2,534.6 |

| Perpetual-Premium | 5.45 % | 2.18 % | 66,363 | 0.08 | 18 | 0.0283 % | 2,521.2 |

| Perpetual-Discount | 5.05 % | 5.07 % | 119,922 | 15.35 | 15 | -0.2559 % | 2,782.3 |

| FixedReset | 4.38 % | 3.73 % | 273,092 | 16.33 | 86 | -0.0363 % | 2,424.7 |

| Deemed-Retractible | 4.91 % | 3.51 % | 110,294 | 0.78 | 35 | -0.0752 % | 2,645.4 |

| FloatingReset | 2.58 % | 2.91 % | 62,405 | 6.19 | 7 | -0.0243 % | 2,338.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| MFC.PR.L | FixedReset | -3.76 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.76 Bid-YTW : 4.76 % |

| SLF.PR.H | FixedReset | -3.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.70 Bid-YTW : 5.10 % |

| FTS.PR.H | FixedReset | -2.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-12 Maturity Price : 16.30 Evaluated at bid price : 16.30 Bid-YTW : 3.84 % |

| FTS.PR.K | FixedReset | -1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-12 Maturity Price : 21.70 Evaluated at bid price : 22.00 Bid-YTW : 3.72 % |

| ENB.PR.T | FixedReset | -1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-12 Maturity Price : 20.20 Evaluated at bid price : 20.20 Bid-YTW : 4.56 % |

| PWF.PR.P | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-12 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 3.60 % |

| IFC.PR.A | FixedReset | -1.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.80 Bid-YTW : 5.51 % |

| PWF.PR.S | Perpetual-Discount | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-12 Maturity Price : 23.92 Evaluated at bid price : 24.32 Bid-YTW : 4.95 % |

| GWO.PR.I | Deemed-Retractible | -1.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.75 Bid-YTW : 5.26 % |

| MFC.PR.H | FixedReset | 1.01 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-03-19 Maturity Price : 25.00 Evaluated at bid price : 26.05 Bid-YTW : 2.64 % |

| BMO.PR.T | FixedReset | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-12 Maturity Price : 23.06 Evaluated at bid price : 24.55 Bid-YTW : 3.33 % |

| BAM.PR.R | FixedReset | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-12 Maturity Price : 20.88 Evaluated at bid price : 20.88 Bid-YTW : 4.16 % |

| BAM.PR.X | FixedReset | 1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-12 Maturity Price : 18.65 Evaluated at bid price : 18.65 Bid-YTW : 4.08 % |

| GWO.PR.N | FixedReset | 1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.35 Bid-YTW : 6.13 % |

| NA.PR.W | FixedReset | 1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-12 Maturity Price : 23.00 Evaluated at bid price : 24.50 Bid-YTW : 3.37 % |

| TRP.PR.C | FixedReset | 1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-12 Maturity Price : 18.60 Evaluated at bid price : 18.60 Bid-YTW : 3.52 % |

| BMO.PR.S | FixedReset | 1.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-12 Maturity Price : 23.22 Evaluated at bid price : 24.92 Bid-YTW : 3.35 % |

| BAM.PR.T | FixedReset | 2.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-12 Maturity Price : 21.27 Evaluated at bid price : 21.55 Bid-YTW : 4.01 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BAM.PF.F | FixedReset | 127,583 | Desjardins crossed 100,000 at 24.85; TD crossed 25,000 at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-12 Maturity Price : 23.16 Evaluated at bid price : 24.86 Bid-YTW : 3.96 % |

| CM.PR.Q | FixedReset | 115,410 | Nesbitt crossed 76,800 at 25.00; TD crossed 25,000 at 24.97. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-12 Maturity Price : 23.10 Evaluated at bid price : 24.85 Bid-YTW : 3.69 % |

| RY.PR.H | FixedReset | 82,086 | Desjardins crossed 20,000 at 24.62; RBC crossed 40,400 at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-12 Maturity Price : 23.08 Evaluated at bid price : 24.61 Bid-YTW : 3.34 % |

| ENB.PR.H | FixedReset | 63,230 | RBC crossed blocks of 23,600 and 26,400, both at 18.86. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-12 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 4.46 % |

| RY.PR.C | Deemed-Retractible | 59,095 | Nesbitt crossed 50,000 at 25.25. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-11-24 Maturity Price : 25.00 Evaluated at bid price : 25.18 Bid-YTW : 2.95 % |

| ENB.PR.T | FixedReset | 51,581 | RBC crossed 40,000 at 20.45. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-12 Maturity Price : 20.20 Evaluated at bid price : 20.20 Bid-YTW : 4.56 % |

| There were 52 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.M | FixedReset | Quote: 24.09 – 24.97 Spot Rate : 0.8800 Average : 0.5983 YTW SCENARIO |

| IAG.PR.G | FixedReset | Quote: 25.95 – 26.50 Spot Rate : 0.5500 Average : 0.4134 YTW SCENARIO |

| RY.PR.Z | FixedReset | Quote: 24.46 – 24.94 Spot Rate : 0.4800 Average : 0.3657 YTW SCENARIO |

| PWF.PR.F | Perpetual-Discount | Quote: 25.01 – 25.29 Spot Rate : 0.2800 Average : 0.1688 YTW SCENARIO |

| GWO.PR.F | Deemed-Retractible | Quote: 25.61 – 25.98 Spot Rate : 0.3700 Average : 0.2603 YTW SCENARIO |

| BAM.PF.B | FixedReset | Quote: 22.65 – 22.99 Spot Rate : 0.3400 Average : 0.2306 YTW SCENARIO |