So what’s the worst kind of person to have at the top of an important government agency? A micro-manager who is unfamiliar with the substance of the work:

Expectations were high for [Mary Jo] White, who came to the [Chair of the SEC] job with a reputation as a tough prosecutor. As U.S. Attorney for the Southern District of New York, she took on terrorists and mobsters. Later she became a highly sought-after defense attorney, representing banks and other defendants in government probes. In announcing her nomination in January 2013, President Obama warned the financial industry: “You don’t want to mess with Mary Jo.”

That reputation has been dented at the SEC. The pace of rulemaking has been so slow that some staff have labeled White’s office the cheese cellar: It’s where policy goes to age. The nickname has stuck as proposals and reports have piled up in her office, waiting for her careful, often line-by-line consideration. White’s circumspection has slowed the progress of high-profile rules governing executive pay, broker obligations, and swaps, the financial products that helped fuel the financial crisis.

White had never held a position for which she had to develop complex financial policy. That lack of experience, plus difficulty in developing a consensus on nettlesome issues, has contributed to the agency’s troubles, say critics inside and outside the agency. “You take a commission that faces the most challenging regulatory agenda since its creation and you appoint a nonpolicy person as chair,” says Barbara Roper, director of investor protection for the Consumer Federation of America. The SEC under White “has been as unproductive as I thought it would be.”

My favourite journalist, Matt Levine, takes a good look at the touted FX so-called rigging settlement:

Then there are three bullet points describing other naughtiness that does not rise to the level of antitrust conspiracy. Those bullet points begin:

“We added markup to price quotes using hand signals and/or other internal arrangements or communications.”

“We have, without informing clients, worked limit orders at levels (i.e., prices) better than the limit order price so that we would earn a spread or markup in connection with our execution of such orders.”

“We made decisions not to fill clients’ limit orders at all, or to fill them only in part, in order to profit from a spread or markup in connection with our execution of such orders.”

You might read these sentences as admissions of guilt, or disclosures of crimes, or even apologies. In context — in the context of a disclosure notice sent to clients as part of the bank’s probation for a felony conviction, one paragraph after the apology for the massive antitrust conspiracy — that’s kind of what they look like. And in the banks’ plea agreements, the practices described in those bullet points are listed as “other relevant conduct” for the criminal conspiracy. So I read the bullet points as confessions yesterday, and was puzzled because, while they seem like sharp practices, they don’t quite seem like crimes.

But those bullet points are actually introduced by the phrase, “The Firm has engaged in other practices on occasion, including:.” These are not crimes, just “practices.” And the disclosure notice just describes them. It stops after the bullet points. It never says “and those practices were wrong.” Or “and we’re sorry we did those things.” Or even: “and we’ll stop doing them.”

Because they won’t! Here’s another letter that JPMorgan is sending to its clients along with the disclosure notice.2 This one is not a condition of its probation. Here’s how it starts:

The purpose of this letter is to clarify the nature of the trading relationship between you and the Corporate & Investment Bank at JPMorgan Chase & Co. and its affiliates (together, “JPMorgan” or the “Firm”) and to disclose relevant practices of JPMorgan when acting as a dealer, on a principal basis, in the wholesale spot foreign exchange (“FX”) markets. We want to ensure that there are no ambiguities or misunderstandings regarding those practices.

So: That does not sound like an apology. That sounds downright feisty. The disclosure notice, which JPMorgan has to send, starts with an apology and then goes on to list some things that JPMorgan did in the past. The client letter, which JPMorgan wants to send, starts with a defiant “no ambiguities or misunderstandings” and then goes on to list some things that JPMorgan will keep doing in the future.

So guess what? JPMorgan acts a principal on FX transactions, to the bewildered astonishment of pseudo-portfolio managers and ignorant regulatory lawyers. And they intend to continue acting as principal! How about that, eh? And their job as principal is to make money for their firm, not yours! Isn’t that astonishing? Golly, it sure is different from kindergarten, where teacher told us to work together.

Levine adds a good point, which has me weeping that it is considered necessary to emphasize:

Of course salespeople and traders talk to each other! The salesperson’s job is to help the trader understand how to price a trade for a particular client. If the salesperson thinks it’s in the bank’s interest to add a markup — that is, if the salesperson thinks that the client is not particularly price-sensitive and will not trade away if the price is too high — then the salesperson’s job is to inform the trader.

The regulatory weenies get a much more sympathetic hearing in another article:

The manipulation didn’t stop at putting in low fixes, the traders quoted by the FCA also were attempting to trigger client stops for their own ends.

In the example the FCA gives, a client had placed to stop loss order to buy GBP77 million at the rate of 95 against another currency. The Barclays trader attempts to get the currency to trade at 97 so he could sell the full GBP77 million to the client at 96.5. Barclays would profit from this stop loss order if the average rate they bought GBP in the market was lower than this stop stop loss order.

Good for the Barclays guys! As principals, they had absolutely zero duty to their counterparty, who was a complete moron for placing a stop order in the first place. Let’s just hope that the twerp who placed that order has gone bankrupt and is now spending his days naked and hungry in a London alleyway.

It may be that the US 10-Year Break Even Inflation Rate has found a new level:

Demand at Thursday’s $13 billion auction of U.S. Treasury Inflation-Protected Securities, or TIPS, declined from the previous sale in March. The offering attracted the lowest demand since September 2014, when oil prices were collapsing, bringing down a key measure of bond-market inflation forecasts along with them.

“We’re just simply not too wrought up about inflation expectations at the moment,” said Jim Vogel, interest-rate strategist with FTN Financial in Memphis, Tennessee.

The U.S. 10-year break-even rate, a gauge of the inflation outlook derived from the yield difference between Treasuries and index-linked securities, was at 1.87 percentage points, up from a low this year of 1.53 percent on Jan. 13. That made TIPS less attractive on Thursday.

The CPPIB has reported annual returns to March 31, 2015:

CPPIB measures its performance against a market-based benchmark, the Reference Portfolio, representing a passive portfolio of public market investments that can reasonably be expected to generate the long-term returns needed to help sustain the CPP at the current contribution rate.

In fiscal 2015, the CPP Fund’s gross return of 18.7% outperformed the Reference Portfolio delivering $3.6 billion in gross dollar value-added (DVA) above the Reference Portfolio’s return, after external management fees and transaction costs. Net of all CPPIB costs, the investment portfolio exceeded the benchmark’s return by 1.3%, producing $2.8 billion in net DVA.

“Dollar value-added is an important measure as it shows the difference between active investments made relative to their benchmarks in dollar terms. We will maintain a greater focus on total Fund – absolute as well as relative – returns, by continuing to develop and apply our capabilities more widely to portfolio management,” said Mr. Wiseman. “Our attention to both measures helps maximize returns, CPPIB’s objective, in the best interests of current and future beneficiaries, since the source of pension benefits is the total Fund. To reduce volatility, DVA is particularly valuable when it is generated as loss reduction in negative market conditions. Both total returns and DVA can vary widely from year-to-year depending on market conditions. Accordingly, both measures must be looked at over longer periods of at least one market cycle, such as five years or more.”

Given our long-term view and risk-return accountability framework, we track cumulative value-added returns since the April 1, 2006, inception of the Reference Portfolio. Cumulative value-added over the past nine years totals $5.8 billion, after all costs.

They also talked a lot about nominal and real returns, which I think is a mistake – they’re just setting themselves up for criticism in a bad year. I confess I am a little troubled by the asset mix:

Click for Big

18.7% private equity! That’s a lot! And I continue to be convinced that at some point we’re going to see a big wave of scandals resulting from too many people playing too many games for too long with private equity valuations…

And it’s about time for me to complain again about pricing trends in education:

The college building boom is coming to New York City’s elite private schools.

With interest rates poised to rise, the Ivy League stepping stones are selling tax-exempt debt at the fastest pace in over a decade to keep their edge. Riverdale Country School in the Bronx, Saint Ann’s School in Brooklyn and La Scuola d’Italia Guglielmo Marconi near Central Park plan to sell almost $150 million of bonds to pay for projects, including a new six-lane pool and musical ensemble rooms.

The borrowing reflects the competitive pressure to replace decades-old buildings and dangle the latest amenities to draw the children of New York’s wealthiest. Tuition runs as high as $45,600 a year, in a city where half the households earn less than $52,000.

…

To lure students, U.S. universities have borrowed more than $250 billion in the municipal market over the past decade for labs, dormitories and gyms with features like rock-climbing walls. For public colleges, it’s a way to attract higher-paying out-of-state students. For private ones, to best the competition.The approach has caught on in New York, where some 234,000 pupils, almost one-fifth of the total, attend private schools.

…

The New York schools are borrowing through Build NYC Resource Corp., a city agency that allows non-profits to raise money in the municipal-bond market. The schools repay investors, who are willing to accept lower interest rates because the income isn’t taxed. Build NYC receives fees for arranging the sales. It isn’t on the hook if they default.

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts up 22bp, FixedResets off 16bp and DeemedRetractibles gaining 4bp. Enbridge FixedResets dominated the “return challenged” section of the Performance Highlights table. Volume was below average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

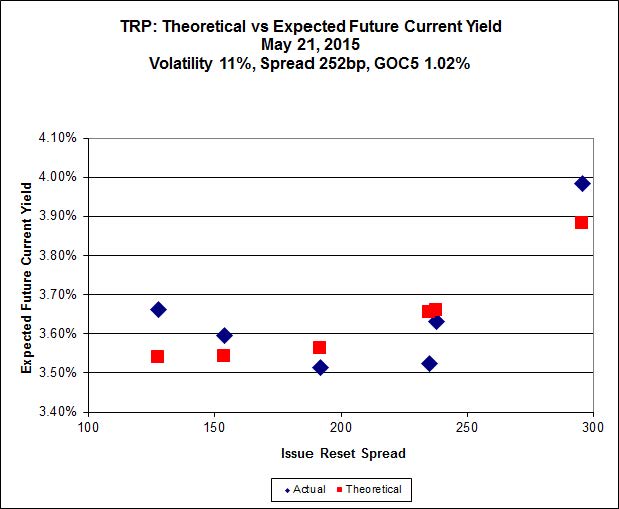

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 23.90 to be $0.84 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $0.66 cheap at its bid price of 24.98.

Click for Big

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.M, resetting at +236 on 2019-12-19, bid at 24.55 to be $0.62 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 25.10 to be $0.61 cheap.

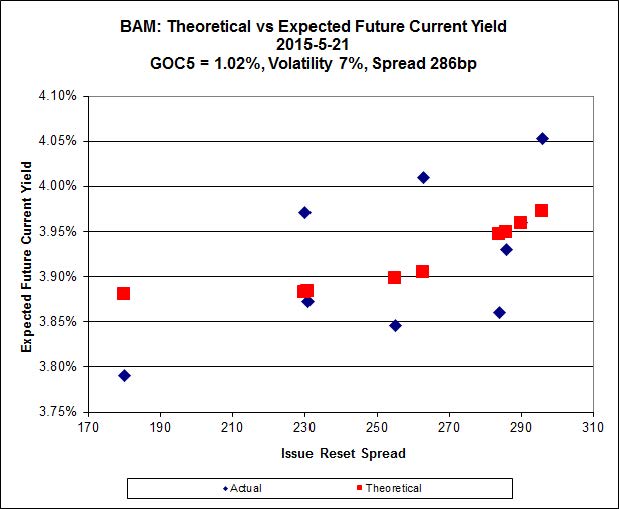

Click for Big

The cheapest issue relative to its peers is BAM.PF.B, resetting at +263bp on 2019-3-31, bid at 22.76 to be $0.61 cheap. BAM.PF.G, resetting at +284bp 2020-6-30 is bid at 25.00 and appears to be $0.55 rich.

Click for Big

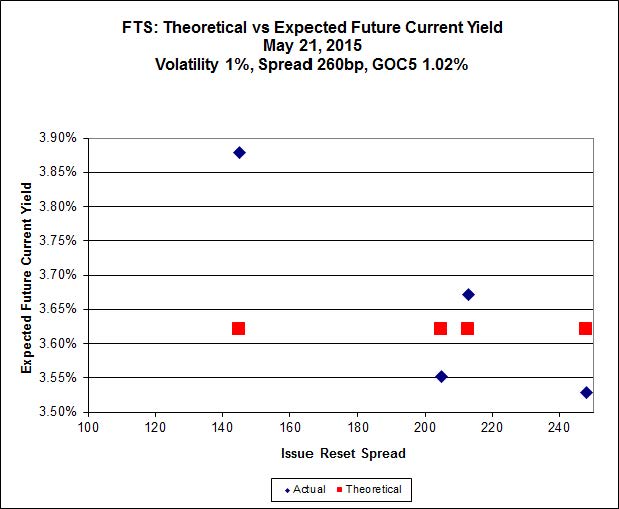

FTS.PR.H, with a spread of +145bp, and bid at 15.92, looks $1.14 cheap and resets 2015-6-1. FTS.PR.M, with a spread of +248bp and resetting 2019-12-1, is bid at 24.80 and is $0.63 rich.

Click for Big

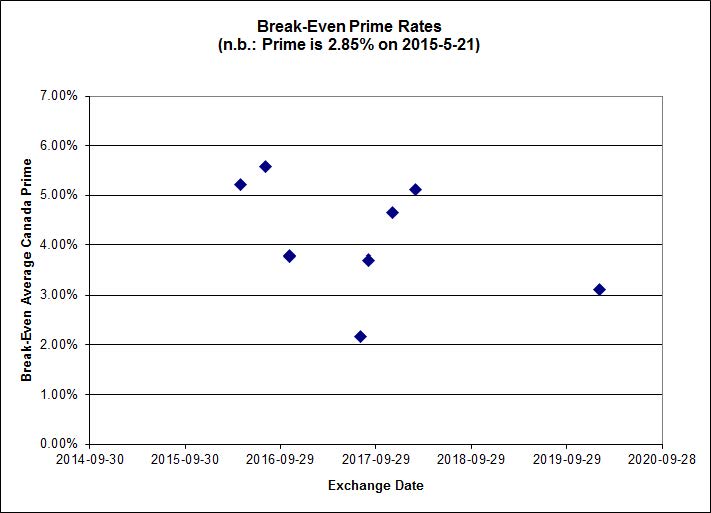

Investment-grade pairs predict an average over the next five-odd years of about 0.30%, including the TRP.PR.A / TRP.PR.F at -0.45%. On the junk side, the FFH.PR.E / FFH.PR.F pair is at -1.24%, while DC.PR.B / DC.PR.D has leapt upwards to +1.26%. It’s a far cry from, for instance, March 30 when the latter pair had a break-even rate of -2.87% … since then, the price spread has narrowed from $4.00 to $0.28, while the total returns are -11.68% and +3.81%, respectively.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.3675 % | 2,283.6 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.3675 % | 3,992.8 |

| Floater | 3.18 % | 3.35 % | 54,243 | 18.84 | 4 | -1.3675 % | 2,427.6 |

| OpRet | 4.45 % | -7.20 % | 32,945 | 0.11 | 2 | -0.2172 % | 2,776.9 |

| SplitShare | 4.60 % | 4.70 % | 61,797 | 3.36 | 3 | 0.2019 % | 3,241.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2172 % | 2,539.2 |

| Perpetual-Premium | 5.47 % | 2.93 % | 63,815 | 0.08 | 18 | 0.0022 % | 2,516.9 |

| Perpetual-Discount | 5.06 % | 5.07 % | 118,712 | 15.35 | 15 | 0.2184 % | 2,782.0 |

| FixedReset | 4.41 % | 3.80 % | 271,530 | 16.08 | 86 | -0.1570 % | 2,413.8 |

| Deemed-Retractible | 4.93 % | 3.52 % | 109,143 | 0.83 | 35 | 0.0355 % | 2,636.3 |

| FloatingReset | 2.57 % | 2.92 % | 58,733 | 6.16 | 7 | -0.0304 % | 2,333.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.C | Floater | -1.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 14.90 Evaluated at bid price : 14.90 Bid-YTW : 3.38 % |

| BAM.PR.B | Floater | -1.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 15.04 Evaluated at bid price : 15.04 Bid-YTW : 3.35 % |

| RY.PR.M | FixedReset | -1.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 22.85 Evaluated at bid price : 24.25 Bid-YTW : 3.74 % |

| BAM.PR.K | Floater | -1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 14.80 Evaluated at bid price : 14.80 Bid-YTW : 3.40 % |

| ENB.PR.B | FixedReset | -1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 19.05 Evaluated at bid price : 19.05 Bid-YTW : 4.67 % |

| ENB.PF.C | FixedReset | -1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 21.31 Evaluated at bid price : 21.31 Bid-YTW : 4.59 % |

| ENB.PF.E | FixedReset | -1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 21.32 Evaluated at bid price : 21.32 Bid-YTW : 4.62 % |

| ENB.PF.A | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 21.37 Evaluated at bid price : 21.37 Bid-YTW : 4.59 % |

| GWO.PR.N | FixedReset | -1.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.03 Bid-YTW : 6.52 % |

| ENB.PR.D | FixedReset | -1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 19.09 Evaluated at bid price : 19.09 Bid-YTW : 4.65 % |

| TRP.PR.B | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 15.70 Evaluated at bid price : 15.70 Bid-YTW : 3.83 % |

| ENB.PR.H | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 18.34 Evaluated at bid price : 18.34 Bid-YTW : 4.58 % |

| ENB.PR.J | FixedReset | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 21.12 Evaluated at bid price : 21.12 Bid-YTW : 4.52 % |

| ENB.PR.Y | FixedReset | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 19.45 Evaluated at bid price : 19.45 Bid-YTW : 4.63 % |

| ENB.PF.G | FixedReset | -1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 21.45 Evaluated at bid price : 21.75 Bid-YTW : 4.53 % |

| PWF.PR.S | Perpetual-Discount | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 24.38 Evaluated at bid price : 24.80 Bid-YTW : 4.86 % |

| BMO.PR.T | FixedReset | 1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 23.10 Evaluated at bid price : 24.65 Bid-YTW : 3.38 % |

| FTS.PR.K | FixedReset | 1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 21.32 Evaluated at bid price : 21.61 Bid-YTW : 3.80 % |

| CIU.PR.C | FixedReset | 1.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 16.70 Evaluated at bid price : 16.70 Bid-YTW : 3.77 % |

| TRP.PR.C | FixedReset | 1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 17.80 Evaluated at bid price : 17.80 Bid-YTW : 3.79 % |

| TRP.PR.D | FixedReset | 1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 22.57 Evaluated at bid price : 23.41 Bid-YTW : 3.78 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BNS.PR.Y | FixedReset | 103,869 | TD crossed blocks of 49,200 and 49,900, both at 23.43. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.35 Bid-YTW : 3.00 % |

| HSE.PR.A | FixedReset | 75,913 | RBC crossed 71,700 at 17.28. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 17.21 Evaluated at bid price : 17.21 Bid-YTW : 4.26 % |

| FTS.PR.M | FixedReset | 70,980 | RBC crossed 55,000 at 24.90. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 23.13 Evaluated at bid price : 24.80 Bid-YTW : 3.60 % |

| RY.PR.K | FloatingReset | 59,900 | TD crossed 50,000 at 24.25. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.32 Bid-YTW : 2.94 % |

| TRP.PR.A | FixedReset | 53,133 | Scotia crossed blocks of 18,000 and 20,000, both at 21.00. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-21 Maturity Price : 20.92 Evaluated at bid price : 20.92 Bid-YTW : 3.72 % |

| IFC.PR.C | FixedReset | 48,858 | Nesbitt crossed 40,000 at 24.80. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.80 Bid-YTW : 4.00 % |

| There were 24 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| RY.PR.M | FixedReset | Quote: 24.25 – 24.82 Spot Rate : 0.5700 Average : 0.3455 YTW SCENARIO |

| RY.PR.K | FloatingReset | Quote: 24.32 – 24.98 Spot Rate : 0.6600 Average : 0.4455 YTW SCENARIO |

| FTS.PR.H | FixedReset | Quote: 15.92 – 16.49 Spot Rate : 0.5700 Average : 0.4132 YTW SCENARIO |

| HSE.PR.E | FixedReset | Quote: 25.47 – 25.79 Spot Rate : 0.3200 Average : 0.2137 YTW SCENARIO |

| ELF.PR.H | Perpetual-Premium | Quote: 25.22 – 25.54 Spot Rate : 0.3200 Average : 0.2245 YTW SCENARIO |

| HSE.PR.A | FixedReset | Quote: 17.21 – 17.51 Spot Rate : 0.3000 Average : 0.2112 YTW SCENARIO |