It was a day and a half for the equities markets:

The Standard & Poor’s 500 Index fell into a correction for the first time since 2011 in one of the most volatile trading days ever, as a rout in global equity markets deepened.

It was a day of wild swings as equities plunged at the open before staging a sharp rebound, with the Nasdaq 100 Index by midday nearly erasing a 9.8 percent drop. The Dow Jones Industrial Average dropped 1,000 points in the opening minutes of trading, while the S&P 500 tumbled 5.3 percent and then pared declines before an afternoon wave of renewed selling.

The S&P 500 dropped 3.9 percent to 1,893.21 at 4 p.m. in New York, and closed 11 percent below its May record. The Dow lost 588.40 points, or 3.6 percent, to 15,871.35, after sliding as much as 6.6 percent. The Nasdaq Composite Index retreated 3.8 percent to its lowest level since Oct. 27, trimming an early 8.8 percent skid.

West Texas intermediate oil (WTI) on Monday crashed below $40 (U.S.) a barrel in its biggest one-day drop in almost two months, extending losses as concerns over the health of China’s economy triggered a broad selloff in everything from metals to health and finance.

…

On Monday, WTI oil posted another loss, tumbling more than 5 per cent to $38.24 a barrel. Brent, the global benchmark, fell 6.1 per cent to $42.69 a barrel.

So Canadian equities and the loonie got smacked:

The S&P/TSX index dropped more than 420.9 points or 3.12 per cent to 13,052.74, the worst in almost plunge in almost four years. All 10 main groups fell at least 1 per cent, with the energy sector off 4.3 per cent as WTI crude oil prices slumped near the $38 (U.S.) level. The benchmark Canadian equity gauge has fallen 9.8 per cent this month, headed for a fourth straight monthly decline, the longest such streak since September, 2011.

The Canadian dollar was down nearly half a cent at 75.40 cents (U.S.).

And the news was being talked about even by those with no interest in economics:

The Prime Minister’s Office announced that Stephen Harper spoke with Bank of Canada Governor Stephen Poloz Monday about the latest upheaval in financial markets.

…

The notice made no mention of Finance Minister Joe Oliver, who would normally be the government’s main point of contact with the Bank of Canada.

And so there was an unwelcome guest in the preferred share market today:

Click for Big

At press time, a Bloomberg story timestamped 2:21am reported:

U.S. and European equity-index futures advanced after Monday’s $2.7 trillion global equity wipeout, while the yen retreated with government bonds. Chinese shares headed for the biggest four-day drop in almost 19 years.

Futures on the Standard & Poor’s 500 Index rose 1.2 percent after the U.S. benchmark entered a correction for the first time since 2011. The Shanghai Composite Index took its loss since Wendnesday beyond 20 percent as investors question the government’s ability to stem losses. The dollar strengthened versus major peers as 10-year Treasury yields rose for the first time in five days. Oil climbed 1.4 percent in New York after falling to $38.24 a barrel.

It was a thoroughly appalling day for the Canadian preferred share market; there may have been worse ones during the depths of the Credit Crunch nearly seven years ago, but I can’t think of any offhand. PerpetualDiscounts were down 217bp, FixedResets lost 274bp and DeemedRetractibles were off 94bp. Huge losses in Floaters and SplitShares that would normally be worth special mention are today mere bagatelles. With all that, it may come as a surprise that there was one winner in today’s extraordinarily lengthy Performance Highlights table; but this table also contains fourteen issues losing more than 5%, a level that is usually indicative of a grievous error. Volume was very high, but block action was subdued.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

Here’s TRP:

Click for Big

A big jump in Implied Volatility today, but whether it’s meaningful in the light of such poorly fitting data is another question!

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 19.20 to be $1.58 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $1.60 cheap at its nonsensical bid price of 18.81 (see discussion in the Performance Highlights table).

Click for Big

Another good fit today! There was another massive increase in Implied Volatility today. Two MFC issues had sufficiently poor bid/bid performances over the day to be discussed further in the Performance Highlights table, but those bids were deemed to be reasonable.

Most expensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 23.27 to be 0.63 rich, while MFC.PR.J, resetting at +261bp on 2018-3-19, bid at 20.41 to be 0.81 cheap.

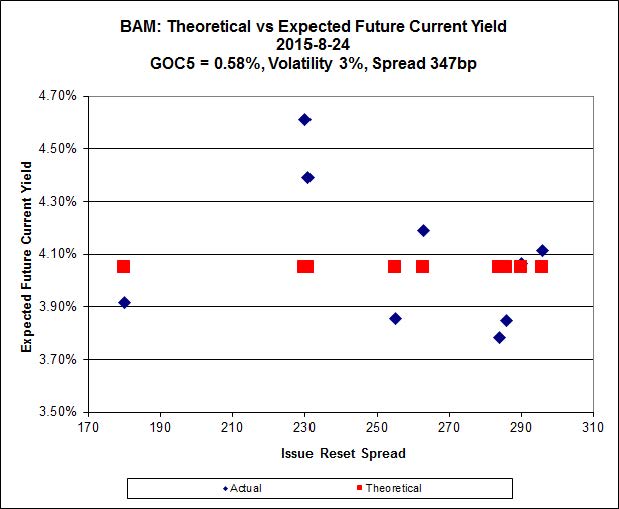

Click for Big

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 15.62 to be $2.16 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 22.60 and appears to be $1.49 rich.

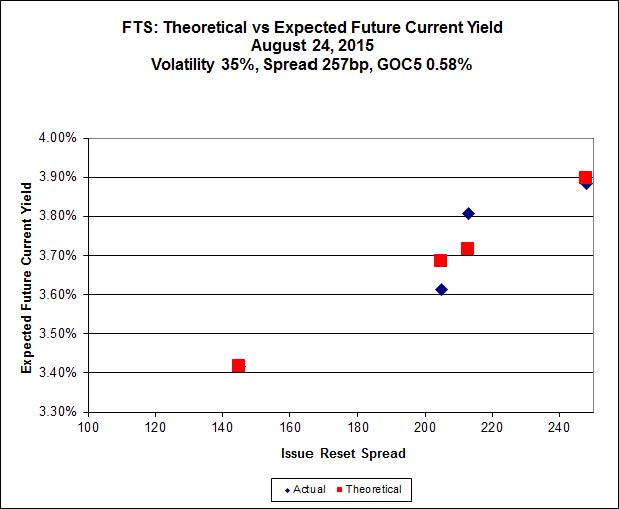

Click for Big

A big jump in Implied Volatility to an unreasonably high level today.

FTS.PR.K, with a spread of +205bp, and bid at 18.20, looks $0.35 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 17.80 and is $0.43 cheap.

Click for Big

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.52%, with no outliers. Note that the distribution is bimodal, with NVCC non-compliant bank issues averaging -0.87% and the unregulated issues averaging -0.02%. There is one junk outlier above +0.80% and three below -1.20%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -2.5738 % | 1,606.6 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -2.5738 % | 2,809.1 |

| Floater | 4.57 % | 4.62 % | 56,066 | 16.12 | 3 | -2.5738 % | 1,708.0 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.4508 % | 2,731.0 |

| SplitShare | 4.71 % | 5.47 % | 56,283 | 3.13 | 3 | -1.4508 % | 3,200.5 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.4508 % | 2,497.2 |

| Perpetual-Premium | 5.78 % | 5.80 % | 63,425 | 14.11 | 9 | -0.9975 % | 2,460.1 |

| Perpetual-Discount | 5.59 % | 5.59 % | 79,394 | 14.48 | 29 | -2.1685 % | 2,527.9 |

| FixedReset | 5.06 % | 4.26 % | 195,595 | 15.30 | 87 | -2.7381 % | 2,087.4 |

| Deemed-Retractible | 5.21 % | 5.34 % | 98,904 | 5.56 | 34 | -0.9440 % | 2,537.7 |

| FloatingReset | 2.38 % | 3.63 % | 48,654 | 5.96 | 9 | -1.0250 % | 2,184.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| ELF.PR.G | Perpetual-Discount | -16.71 % | This is ridiculous. The issue traded 4,000 shares today in a range of 21.50-74, making it one of the better behaved issues, and still the TMX quotes it with a nonsensical bid. I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 18.14 Evaluated at bid price : 18.14 Bid-YTW : 6.65 % |

| TRP.PR.G | FixedReset | -8.91 % | Another ridiculous misquotation from the Toronto Exchange. The issue traded 9,120 shares today in a range of 18.47-22.04, which sounds quite exciting, but the VWAP was 20.62 – only a nickel below yesterday’s closing price – and the closing price was 21.20; so on a close/close basis, the issue is actually a winner! I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 18.81 Evaluated at bid price : 18.81 Bid-YTW : 4.85 % |

| FTS.PR.M | FixedReset | -8.46 % | The issue traded 10,515 shares today in a range of 19.63-21.51 (!) before closing at a quote of 19.70-00. The VWAP was 20.02, so this quotations is actually quite reasonable. Hurray! Send a thank-you card to the Toronto Exchange and bake them a cake! YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 19.70 Evaluated at bid price : 19.70 Bid-YTW : 4.22 % |

| BAM.PR.T | FixedReset | -8.15 % | The issue traded 15,481 shares today in a range of 16.50-17.91 before closing with a quote of 16.45-21. The VWAP was 17.20, but the last twenty-four trades of the day, commencing at 2:48pm, were all at 16.69 and below, so again we can rejoice that the Exchange has not made an obvious error this time. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 16.45 Evaluated at bid price : 16.45 Bid-YTW : 4.77 % |

| FTS.PR.K | FixedReset | -6.67 % | The issue traded 11,870 shares today in a range of 18.08-75 before closing with a quote of 18.20-55. There were eight trades after 3pm, all executed at 18.32 and below, so we’ll give the Exchange a pass on this one as well. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 18.20 Evaluated at bid price : 18.20 Bid-YTW : 4.00 % |

| TD.PF.E | FixedReset | -6.65 % | The issue traded 2,770 shares in a range of 23.97-57 before closing with a quote of 23.02-24.25. The VWAP was 24.17. I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 22.28 Evaluated at bid price : 23.02 Bid-YTW : 3.81 % |

| MFC.PR.M | FixedReset | -6.19 % | The issue traded 10,467 shares in a range of 19.58-21.46 before closing with a quote of 20.14-35. VWAP was 20.29. There were a lot of 100-lots traded after 3pm, some as low as 19.58 but most closer to 20.00, so we can call this a reasonable quote. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.14 Bid-YTW : 6.18 % |

| BAM.PF.B | FixedReset | -5.67 % | The issue traded 18,965 shares today in an extraordinary range of 17.67-20.50 (I don’t think we’ve seen anything like that, at least for a non-special-situation company, since the Credit Crunch!) before closing with a quote of 19.15-20.16. The VWAP was 19.84. All twenty-five trades executed after 3:26pm were at or below the closing bid – some, like four trades totalling 600 shares at 17.67, well below! – so this is a decent bid. Given the day’s action, I’ll cut the market maker a little slack on the closing offer and consequent wide spread. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 19.15 Evaluated at bid price : 19.15 Bid-YTW : 4.56 % |

| ENB.PR.B | FixedReset | -5.54 % | This issue traded 8,250 shares today in a range of 13.20-11, with a VWAP of 13.74, before closing with a quote of 13.64-89, which is quite reasonable. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 13.64 Evaluated at bid price : 13.64 Bid-YTW : 5.74 % |

| MFC.PR.N | FixedReset | -5.39 % | The issue traded 5,925 shares today in a range of 19.80-21.40, with a VWAP of 20.47, before closing with a quote of 20.18-21.45. The last twelve trades of the day, commencing at 3:05pm, were al below 20.00, so the closing bid of 20.18 is reasonable; or, should I say, a reasonable reflection of market conditions! YTW SCENARIO Maturity Type : Hard Maturity1 Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.18 Bid-YTW : 6.09 % |

| ENB.PF.A | FixedReset | -5.34 % | The issue traded 8,491 shares today in a range of 15.34-16.97, with a VWAP of 16.23, before closing with a quote of 16.13-28 – a surprisingly tight quote! Additionally, each of the last 23 trades, commencing at 1:54pm, were inside the closing quote, so for this one we should actually give the market maker a pat on the back. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 16.13 Evaluated at bid price : 16.13 Bid-YTW : 5.53 % |

| HSE.PR.C | FixedReset | -5.34 % | The issue traded 7,290 shares today in a range of 20.00-21.08, with a VWAP of 20.65, before closing with a quote of 20.40-80. The last trade for the day, 100 shares at 1:17pm, was executed at 20.27. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 20.40 Evaluated at bid price : 20.40 Bid-YTW : 4.90 % |

| FTS.PR.G | FixedReset | -5.32 % | The issue traded 4,560 shares today in a range of 16.62-18.57, with a VWAP of 18.07, before closing with a quote of 17.80-50. The last fourteen trades of the day, commencing at 12:12pm, were all inside the closing quote. So it’s OK … kind of a wide spread, but that’s what happens when the devil comes to town! YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 17.80 Evaluated at bid price : 17.80 Bid-YTW : 4.11 % |

| TRP.PR.F | FloatingReset | -5.22 % | The issue traded 4,750 shares today in a range of 12.01-14.28 (!), with a VWAP of 13.74, before closing with a quote of 14.33-50. So the closing bid was above the day high; I think we can call this, if anything, a rather sunny quote! YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 14.33 Evaluated at bid price : 14.33 Bid-YTW : 4.00 % |

| ENB.PR.T | FixedReset | -4.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 14.71 Evaluated at bid price : 14.71 Bid-YTW : 5.65 % |

| NA.PR.W | FixedReset | -4.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 20.20 Evaluated at bid price : 20.20 Bid-YTW : 3.85 % |

| BAM.PR.N | Perpetual-Discount | -4.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 19.97 Evaluated at bid price : 19.97 Bid-YTW : 6.06 % |

| TRP.PR.C | FixedReset | -4.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 12.16 Evaluated at bid price : 12.16 Bid-YTW : 4.54 % |

| RY.PR.M | FixedReset | -4.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 21.63 Evaluated at bid price : 22.00 Bid-YTW : 3.77 % |

| MFC.PR.J | FixedReset | -4.58 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.41 Bid-YTW : 6.03 % |

| IFC.PR.A | FixedReset | -4.58 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.25 Bid-YTW : 8.56 % |

| RY.PR.J | FixedReset | -4.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 21.99 Evaluated at bid price : 22.50 Bid-YTW : 3.76 % |

| FTS.PR.H | FixedReset | -4.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 14.85 Evaluated at bid price : 14.85 Bid-YTW : 3.65 % |

| BMO.PR.Q | FixedReset | -4.41 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.46 Bid-YTW : 4.68 % |

| HSE.PR.E | FixedReset | -4.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 21.03 Evaluated at bid price : 21.03 Bid-YTW : 5.16 % |

| BAM.PR.C | Floater | -4.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 10.28 Evaluated at bid price : 10.28 Bid-YTW : 4.65 % |

| BNS.PR.Z | FixedReset | -4.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.95 Bid-YTW : 5.19 % |

| ENB.PF.C | FixedReset | -4.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 16.31 Evaluated at bid price : 16.31 Bid-YTW : 5.47 % |

| ELF.PR.F | Perpetual-Discount | -3.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 21.94 Evaluated at bid price : 22.18 Bid-YTW : 6.05 % |

| BNS.PR.Y | FixedReset | -3.96 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.87 Bid-YTW : 4.81 % |

| ENB.PR.N | FixedReset | -3.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 15.12 Evaluated at bid price : 15.12 Bid-YTW : 5.66 % |

| GWO.PR.R | Deemed-Retractible | -3.88 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.82 Bid-YTW : 6.79 % |

| NA.PR.S | FixedReset | -3.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 21.15 Evaluated at bid price : 21.15 Bid-YTW : 3.82 % |

| ENB.PR.F | FixedReset | -3.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 14.82 Evaluated at bid price : 14.82 Bid-YTW : 5.53 % |

| MFC.PR.I | FixedReset | -3.67 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.81 Bid-YTW : 5.42 % |

| BAM.PR.R | FixedReset | -3.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 15.62 Evaluated at bid price : 15.62 Bid-YTW : 4.93 % |

| ENB.PF.E | FixedReset | -3.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 16.41 Evaluated at bid price : 16.41 Bid-YTW : 5.48 % |

| BMO.PR.S | FixedReset | -3.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 21.05 Evaluated at bid price : 21.05 Bid-YTW : 3.74 % |

| PWF.PR.S | Perpetual-Discount | -3.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 5.65 % |

| BNS.PR.D | FloatingReset | -3.31 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.46 Bid-YTW : 4.62 % |

| BMO.PR.W | FixedReset | -3.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 20.40 Evaluated at bid price : 20.40 Bid-YTW : 3.73 % |

| MFC.PR.G | FixedReset | -3.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.69 Bid-YTW : 5.44 % |

| GWO.PR.H | Deemed-Retractible | -3.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.05 Bid-YTW : 6.70 % |

| ENB.PF.G | FixedReset | -3.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 16.75 Evaluated at bid price : 16.75 Bid-YTW : 5.41 % |

| BAM.PF.C | Perpetual-Discount | -2.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 20.25 Evaluated at bid price : 20.25 Bid-YTW : 6.10 % |

| ENB.PR.P | FixedReset | -2.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 14.88 Evaluated at bid price : 14.88 Bid-YTW : 5.56 % |

| IFC.PR.C | FixedReset | -2.87 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.30 Bid-YTW : 6.15 % |

| FTS.PR.F | Perpetual-Discount | -2.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 21.86 Evaluated at bid price : 22.10 Bid-YTW : 5.56 % |

| BAM.PR.M | Perpetual-Discount | -2.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 20.11 Evaluated at bid price : 20.11 Bid-YTW : 6.01 % |

| SLF.PR.I | FixedReset | -2.75 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.15 Bid-YTW : 5.00 % |

| ENB.PR.J | FixedReset | -2.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 16.05 Evaluated at bid price : 16.05 Bid-YTW : 5.36 % |

| BAM.PR.K | Floater | -2.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 10.35 Evaluated at bid price : 10.35 Bid-YTW : 4.62 % |

| W.PR.H | Perpetual-Discount | -2.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 23.42 Evaluated at bid price : 23.71 Bid-YTW : 5.87 % |

| BAM.PF.D | Perpetual-Discount | -2.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 20.55 Evaluated at bid price : 20.55 Bid-YTW : 6.07 % |

| SLF.PR.H | FixedReset | -2.55 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.10 Bid-YTW : 6.23 % |

| SLF.PR.E | Deemed-Retractible | -2.51 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.27 Bid-YTW : 7.28 % |

| SLF.PR.D | Deemed-Retractible | -2.49 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.13 Bid-YTW : 7.32 % |

| POW.PR.B | Perpetual-Discount | -2.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 23.10 Evaluated at bid price : 23.36 Bid-YTW : 5.80 % |

| MFC.PR.L | FixedReset | -2.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.00 Bid-YTW : 6.09 % |

| PWF.PR.R | Perpetual-Premium | -2.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 23.92 Evaluated at bid price : 24.40 Bid-YTW : 5.67 % |

| POW.PR.G | Perpetual-Premium | -2.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 23.92 Evaluated at bid price : 24.40 Bid-YTW : 5.80 % |

| TD.PF.B | FixedReset | -2.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 20.79 Evaluated at bid price : 20.79 Bid-YTW : 3.71 % |

| CM.PR.P | FixedReset | -2.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 20.51 Evaluated at bid price : 20.51 Bid-YTW : 3.76 % |

| TD.PF.D | FixedReset | -2.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 22.29 Evaluated at bid price : 23.01 Bid-YTW : 3.72 % |

| FTS.PR.J | Perpetual-Discount | -2.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 21.43 Evaluated at bid price : 21.75 Bid-YTW : 5.47 % |

| ENB.PR.H | FixedReset | -2.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 13.60 Evaluated at bid price : 13.60 Bid-YTW : 5.46 % |

| BAM.PF.E | FixedReset | -2.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 20.30 Evaluated at bid price : 20.30 Bid-YTW : 4.34 % |

| POW.PR.D | Perpetual-Discount | -2.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 22.07 Evaluated at bid price : 22.30 Bid-YTW : 5.67 % |

| SLF.PR.A | Deemed-Retractible | -2.19 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.32 Bid-YTW : 6.87 % |

| GWO.PR.L | Deemed-Retractible | -2.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.68 Bid-YTW : 5.99 % |

| BAM.PF.A | FixedReset | -2.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 21.40 Evaluated at bid price : 21.40 Bid-YTW : 4.36 % |

| BMO.PR.T | FixedReset | -2.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 21.42 Evaluated at bid price : 21.42 Bid-YTW : 3.58 % |

| TRP.PR.A | FixedReset | -2.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 15.13 Evaluated at bid price : 15.13 Bid-YTW : 4.55 % |

| MFC.PR.H | FixedReset | -2.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.27 Bid-YTW : 4.79 % |

| BIP.PR.A | FixedReset | -2.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 21.05 Evaluated at bid price : 21.05 Bid-YTW : 5.14 % |

| ENB.PR.Y | FixedReset | -2.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 15.03 Evaluated at bid price : 15.03 Bid-YTW : 5.39 % |

| GWO.PR.G | Deemed-Retractible | -2.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.26 Bid-YTW : 6.34 % |

| CM.PR.O | FixedReset | -2.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 21.61 Evaluated at bid price : 21.90 Bid-YTW : 3.57 % |

| MFC.PR.K | FixedReset | -1.97 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.87 Bid-YTW : 6.06 % |

| GWO.PR.I | Deemed-Retractible | -1.94 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.25 Bid-YTW : 6.82 % |

| SLF.PR.B | Deemed-Retractible | -1.93 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.57 Bid-YTW : 6.76 % |

| PWF.PR.P | FixedReset | -1.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 16.00 Evaluated at bid price : 16.00 Bid-YTW : 3.53 % |

| SLF.PR.C | Deemed-Retractible | -1.83 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.25 Bid-YTW : 7.24 % |

| ENB.PR.D | FixedReset | -1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 14.25 Evaluated at bid price : 14.25 Bid-YTW : 5.52 % |

| HSE.PR.G | FixedReset | -1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 21.64 Evaluated at bid price : 22.00 Bid-YTW : 4.90 % |

| PWF.PR.F | Perpetual-Discount | -1.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 23.38 Evaluated at bid price : 23.67 Bid-YTW : 5.59 % |

| CM.PR.Q | FixedReset | -1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 22.16 Evaluated at bid price : 22.79 Bid-YTW : 3.77 % |

| TD.PF.A | FixedReset | -1.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 20.89 Evaluated at bid price : 20.89 Bid-YTW : 3.70 % |

| PVS.PR.C | SplitShare | -1.73 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2017-12-10 Maturity Price : 25.00 Evaluated at bid price : 24.42 Bid-YTW : 5.89 % |

| POW.PR.A | Perpetual-Premium | -1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 24.25 Evaluated at bid price : 24.55 Bid-YTW : 5.77 % |

| TD.PF.C | FixedReset | -1.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 20.74 Evaluated at bid price : 20.74 Bid-YTW : 3.71 % |

| GWO.PR.S | Deemed-Retractible | -1.65 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.51 Bid-YTW : 5.67 % |

| RY.PR.I | FixedReset | -1.61 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.46 Bid-YTW : 3.48 % |

| PWF.PR.K | Perpetual-Discount | -1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 22.12 Evaluated at bid price : 22.40 Bid-YTW : 5.57 % |

| PVS.PR.B | SplitShare | -1.57 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2019-01-10 Maturity Price : 25.00 Evaluated at bid price : 24.51 Bid-YTW : 4.96 % |

| RY.PR.W | Perpetual-Discount | -1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 23.59 Evaluated at bid price : 23.86 Bid-YTW : 5.15 % |

| RY.PR.N | Perpetual-Discount | -1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 23.82 Evaluated at bid price : 24.16 Bid-YTW : 5.16 % |

| PWF.PR.E | Perpetual-Discount | -1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 23.99 Evaluated at bid price : 24.24 Bid-YTW : 5.72 % |

| W.PR.J | Perpetual-Discount | -1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 23.69 Evaluated at bid price : 24.00 Bid-YTW : 5.90 % |

| GWO.PR.Q | Deemed-Retractible | -1.37 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.68 Bid-YTW : 6.04 % |

| BAM.PR.Z | FixedReset | -1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 21.51 Evaluated at bid price : 21.51 Bid-YTW : 4.42 % |

| TRP.PR.B | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 12.00 Evaluated at bid price : 12.00 Bid-YTW : 4.13 % |

| GWO.PR.M | Deemed-Retractible | -1.29 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2019-03-31 Maturity Price : 25.00 Evaluated at bid price : 25.32 Bid-YTW : 5.72 % |

| MFC.PR.C | Deemed-Retractible | -1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.50 Bid-YTW : 7.15 % |

| RY.PR.L | FixedReset | -1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.30 Bid-YTW : 3.63 % |

| CU.PR.G | Perpetual-Discount | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 20.46 Evaluated at bid price : 20.46 Bid-YTW : 5.53 % |

| BMO.PR.Y | FixedReset | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 22.73 Evaluated at bid price : 23.89 Bid-YTW : 3.57 % |

| TD.PR.Z | FloatingReset | -1.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.66 Bid-YTW : 3.63 % |

| RY.PR.H | FixedReset | -1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 21.26 Evaluated at bid price : 21.26 Bid-YTW : 3.63 % |

| CU.PR.F | Perpetual-Discount | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 20.50 Evaluated at bid price : 20.50 Bid-YTW : 5.52 % |

| IAG.PR.G | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.08 Bid-YTW : 4.21 % |

| VNR.PR.A | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 19.75 Evaluated at bid price : 19.75 Bid-YTW : 4.52 % |

| PVS.PR.D | SplitShare | -1.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2021-10-08 Maturity Price : 25.00 Evaluated at bid price : 23.75 Bid-YTW : 5.47 % |

| GWO.PR.N | FixedReset | -1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.55 Bid-YTW : 7.86 % |

| GWO.PR.P | Deemed-Retractible | -1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.40 Bid-YTW : 5.89 % |

| TRP.PR.D | FixedReset | 1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 18.99 Evaluated at bid price : 18.99 Bid-YTW : 4.23 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TRP.PR.E | FixedReset | 94,877 | RBC bought two blocks of 25,000 each from Scotia, both at 19.20. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 19.20 Evaluated at bid price : 19.20 Bid-YTW : 4.26 % |

| BMO.PR.L | Deemed-Retractible | 37,430 | Nesbitt crossed 21,500 at 25.56. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-09-23 Maturity Price : 25.50 Evaluated at bid price : 25.56 Bid-YTW : 2.64 % |

| CM.PR.O | FixedReset | 32,005 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 21.61 Evaluated at bid price : 21.90 Bid-YTW : 3.57 % |

| IGM.PR.B | Perpetual-Premium | 27,800 | Nesbitt crossed 25,000 at 25.35. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 25.00 Evaluated at bid price : 25.32 Bid-YTW : 5.88 % |

| SLF.PR.A | Deemed-Retractible | 27,791 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.32 Bid-YTW : 6.87 % |

| RY.PR.Z | FixedReset | 27,499 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-24 Maturity Price : 21.15 Evaluated at bid price : 21.15 Bid-YTW : 3.61 % |

| There were 48 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| ELF.PR.G | Perpetual-Discount | Quote: 18.14 – 21.50 Spot Rate : 3.3600 Average : 1.9784 YTW SCENARIO |

| TRP.PR.G | FixedReset | Quote: 18.81 – 22.05 Spot Rate : 3.2400 Average : 1.9794 YTW SCENARIO |

| TD.PF.E | FixedReset | Quote: 23.02 – 24.25 Spot Rate : 1.2300 Average : 0.6641 YTW SCENARIO |

| MFC.PR.N | FixedReset | Quote: 20.18 – 21.45 Spot Rate : 1.2700 Average : 0.7800 YTW SCENARIO |

| BAM.PF.B | FixedReset | Quote: 19.15 – 20.16 Spot Rate : 1.0100 Average : 0.6249 YTW SCENARIO |

| BAM.PR.T | FixedReset | Quote: 16.45 – 17.21 Spot Rate : 0.7600 Average : 0.4528 YTW SCENARIO |

Please correct me if I am wrong and missing something huge.

The way I see it, the market is shunning preferred shares (both perpetuals, rate resets, and others) for some reason. In any case, the price for preferreds are now very low. A person with money to invest in fixed income should be buying these up in quantity, because regardless of what happens, barring corporate bankruptcy of course, these shares will give very good yields, even at low reset values, and may even produce good capital gains once the martlet stabilizes. I am thinking on the long term, of course.

” ..the price for preferreds are now very low”

because something is “low” doesn’t mean it won’t go lower.

I am also buying. Although I agree it could go lower… Doubled my preferred position about a month ago. Too early. Ugh. Still small but I hold little other fixed income. Bought another bit on Monday.

Now I hold all 3 ELF issues as well as the common. Also have small positions in all the Enbridge USD prefs with an emphasis on the ones that reset first at USG 5yr +314 and +315.

Well, as I stated in the post eMail To A Client, preferreds of all stripes were looking pretty good as fixed income investments towards the end of July. Now, of course, more so – subject, of course, to all the usual risks that involve investment in preferred shares in general and perpetual instruments in general.

Will they go up? Will they go down? If you can answer ‘who cares?’ then they are quite attractive.

Hey would you answer ‘who cares?’ Is that because barring default, yields are so good, that only high inflation (for perpetuals) and lots can hurt these investments?

Sorry, I pressed submit too fast. My apologies.

How would you answer ‘who cares?’ Is that because, barring default, yields are so good that only high inflation (for perpetuals) can hurt these investments?

Is this perhaps a situation of comparing a perpetual from a major bank paying x % and a 5 year GIC from that same bank paying perhaps about 40 % of x ?

I wrote an essay a while back titled Security of Income vs. Security of Principal.

The big question in Fixed Income investing is the degree of emphasis placed on these two contradictory objectives.

Preferred shares, generally speaking, excel at ‘Security of Income’ (and I say that with full knowledge of dividend rate cuts on FixedResets lately), and are lousy at ‘Security of Principal’. So, therefore, they will be attractive to somebody who wants an income stream and will allocate only that capital they do not expect to need in the short (or even medium) term.

I read your essay. Thanks again.

A fair bit was confusing, but I got the general ideas.

I understand why you would say ‘who cares’ if the pref value increases or decreases because the income is stable. Also, if interest rates drop, a perpetual pref is more likely to be recalled, and you get your principal back in full or more, unless you bought at a premium.

The problem I see is with a rate reset pref, where you may end up with a lower income than expected if interest rates drop. Would this not result in no security of either income or principal?

The problem I see is with a rate reset pref, where you may end up with a lower income than expected if interest rates drop.

Yes, that’s a problem; on the other hand, you have a degree of inflation protection.

Would this not result in no security of either income or principal?

Relative to a Straight Perpetual, Security of Principal is enhanced because you are no longer exposed to parallel shifts in the yield curve (although, of course, you retain 100% exposure to changes in spreads).

Security of Income … well, because of the built-in inflation protection, you have a degree of enhanced security; you don’t have to worry so much about twenty years of high inflation will erode your real income. On the other hand, of course, nominal income will be less secure.

Maybe that article will have to be re-written sometime with another axis to reflect inflation effects! But the general principal remains sound, although more complex.