There are a lot of unsolved mysteries in life. How do they get the caramel into a Caramilk bar? Why did that hot chick in high school go out with jerks instead of me? Was Lehman insolvent or merely illiquid?:

At issue that September, six years ago, was whether the Fed could save a major investment bank whose failure might threaten the entire economy.

The firm was Lehman Brothers. And the answer for some inside the Fed was yes, the government could bail out Lehman, according to new accounts by Fed officials who were there at the time.

…

Ben S. Bernanke, the Fed chairman at the time, Henry M. Paulson Jr., the former Treasury Secretary, and Timothy F. Geithner, who was then president of the New York Fed, have all argued that Lehman Brothers was in such a deep hole from its risky real estate investments that Fed did not have the legal authority to rescue it.

…

Whether to save Lehman came down to a crucial question: Did Lehman have enough solid assets to back a loan from the Fed? Finding the answer fell to two teams of financial experts at the New York Fed. Those teams had provisionally concluded that Lehman might, in fact, be a candidate for rescue, but members of those teams said they never briefed Mr. Geithner, who said he did not know of the results.

…

Mr. Bernanke and Mr. Paulson said in recent interviews with The Times that they did not know about the Fed analysis or its conclusions.Interviews with half a dozen Fed officials, who spoke on the condition they not be named, so as not to breach the Fed’s unofficial vow of silence, suggest some Fed insiders believed that the government had the authority to throw Lehman Brothers a lifeline, even if the bank was nearly broke. The Fed earlier came to the rescue of Bear Stearns, after doing little analysis, and only days later saved the American International Group. The government subsequently saved the likes of Bank of America, Citigroup, Goldman Sachs and Morgan Stanley. Ultimately, whether Lehman should have gotten Fed support was a judgment call, not a matter of strict statute, these people said.

…

A group of bankers summoned to the Fed by Mr. Paulson, who was hoping they would mount a private rescue, did not accept Lehman’s $50 billion valuation for its real estate and could not decide whether Lehman was solvent. But potential private rescuers had a motive to lowball Lehman’s value. Fed officials involved in the valuation stressed that the Fed could hold distressed assets for much longer than private parties, allowing time for those assets to recover in value. Also, because the Fed sets monetary policy, it exerts enormous influence over the assets’ ultimate value.“There can’t be any reasonable doubt that had the Fed rescued Lehman, that very act would have pushed up the value of its assets,” [economics professor at Princeton and former vice chairman of the Fed] Mr. [Alan S.] Blinder said.

While the Fed team did not come up with a precise value for Lehman’s illiquid assets, it provided a range that was far more generous in its valuations than the private sector had been.

…

Argument continues today over the value of Lehman’s assets. A report compiled by Anton R. Valukas, a Chicago lawyer, at the behest of the bankruptcy court overseeing Lehman concluded in 2010 that nearly all of the firm’s real estate valuations were reasonable. It also suggested that Lehman’s chaotic bankruptcy caused many of the losses later borne by the firm’s creditors. Other analysts have argued that Lehman was deeply insolvent.Ultimately, the appraisals of the New York Fed teams did not matter. Their preliminary finding was that Lehman was solvent and that what it faced was essentially a bank run, according to members of the group. Researchers working on the value of Lehman’s collateral said they thought they would be delivering those findings to Mr. Geithner that September weekend.

But Mr. Geithner had already been diverted to A.I.G., which was facing its own crisis.

…

Those at the Fed who have contended that Lehman was insolvent have never provided any basis for that conclusion, other than references to the estimates of Wall Street firms and other anecdotal evidence. The Financial Crisis Inquiry Commission asked for such evidence several times, but the Fed never provided it. The members of the New York Fed teams said that they did not prepare a formal, written report, and that no one asked them for any notes or work papers or asked them to elaborate on their findings. Scott G. Alvarez, the Fed’s general counsel, told the commission that there was “no time” that weekend for a written analysis.

All this has become news again because Bernanke used ‘Fed-Speak’ in congressional testimony:

“In congressional testimony immediately after Lehman’s collapse, Paulson and I were deliberately quite vague when discussing whether we could have saved Lehman,” Mr. Bernanke writes [in his new memoir, “The Courage to Act: A Memoir of a Crisis and Its Aftermath.”]. “But we had agreed in advance to be vague because we were intensely concerned that acknowledging our inability to save Lehman would hurt market confidence and increase pressure on other vulnerable firms.”

…

Of course, there will always be those who believe that the decision was a political one. “I understand why some have concluded that Lehman’s failure was a choice,” Mr. Bernanke writes. “In a way, it is a backhanded compliment: We had shown such resourcefulness to that point, it is hard to imagine that we could not have come up with some solution to Lehman.”He writes that it was simply impossible to save Lehman, pointing to the nearly $200 billion of losses that Lehman’s creditors have since suffered. No one has come forward on the record, nor has any contemporaneous document been produced in the past seven years that said the government had found a way to save the company and specifically chose not to do so for political reasons, a point Mr. Bernanke alludes to in his book. “I do not want the notion that Lehman’s failure could have been avoided, and that its failure was consequently a policy choice, to become the received wisdom, for the simple reason that it is not true,” he writes. “We did everything we could think of to avoid it.”

I certainly hope that the entire episode has become a very high-powered case study at the Fed, other central banks and in business schools on the topic of ‘How decisions get made. I mean, really get made, in high-stakes conditions of total chaos and conflicting opinion.’

After all, emerging economies want to know!

As part of the Trans-Pacific Partnership deal, emerging markets want to know what Federal Reserve Chair Janet Yellen is thinking.

As a sidebar to the largest trade pact in two decades, the U.S. and 11 other Pacific Rim countries agreed not to manipulate foreign-exchange rates and to consult on monetary policies.

Economies like Vietnam and Malaysia, which rely heavily on exports, promised not to devalue their currencies in order to gain a competitive advantage. In exchange, they want to get more insights into U.S. monetary policy.

…

During the negotiations, some of the smaller economies highlighted the far-reaching impact monetary policies in larger developed countries — read the U.S. — have on them, according to a person familiar with the negotiations, who asked not to be named because the details of the talks aren’t public.Participants have agreed that consultations will take place among senior-government officials, although the precise framework has yet to be determined, the person said. And of course, such talks don’t mean the U.S. central bank will need to follow other countries’ wishes.

“Questions about Fed policy will be filtered through the Treasury, and in no way will the Fed be committed or compromised.” said Hufbauer.

DBRS has released a report titled Effect of the Oil Price Shock on Canada, with one line so important I’m going to give it its own blockquote:

Therefore, we view the near term outlook for Canada to be mainly dependent on the external environment.

This should not be news to the meanest intelligence, but turns into a long, boring useless debate every election time. Sure, the governments of the days can do things at the margins, and the things they do at the margins can be good or bad and are important enough to become election issues. I have no problems with that. I do have problems with the idea that Canadian government policy is a significant driver of the Canadian economy.

Anyway, the report states:

There are two areas of concern: the risk that higher U.S. interest rates will lead to sharply higher Canadian mortgage rates, and given the high level of household leverage in an unstable macro environment, this could pose a risk to financial stability. A second and larger concern is how the economy will adjust to a moderate recovery in the United States and to the weaker exchange rate.

So far, the policy response in Canada has averted a Japan- or Eurozone-style crisis, in which jumpstarting domestic demand is proving to be a major challenge. Nevertheless, monetary easing and fiscal tightening have not avoided a shallow recession in Canada. The emphasis in Canada on whether the Federal budget is in surplus or in deficit suggests that the policy choices are limited: the issue is weak growth; not whether the budget is in surplus. Significant fiscal expansion appears to be ruled out, in spite of the recession; and when the economy does return to growth it will almost certainly be a weak recovery. This is the big challenge for the next administration following the elections on October 19.

The flexibility of the economy is associated with labor productivity, and productivity has taken a turn for the worse. This is being driven by a fall in manufacturing, construction, agriculture, and other sectors, and only somewhat offset by services. We suspect that reforms to raise worker productivity and greater investment in infrastructure, could help close the output gap and raise potential GDP.

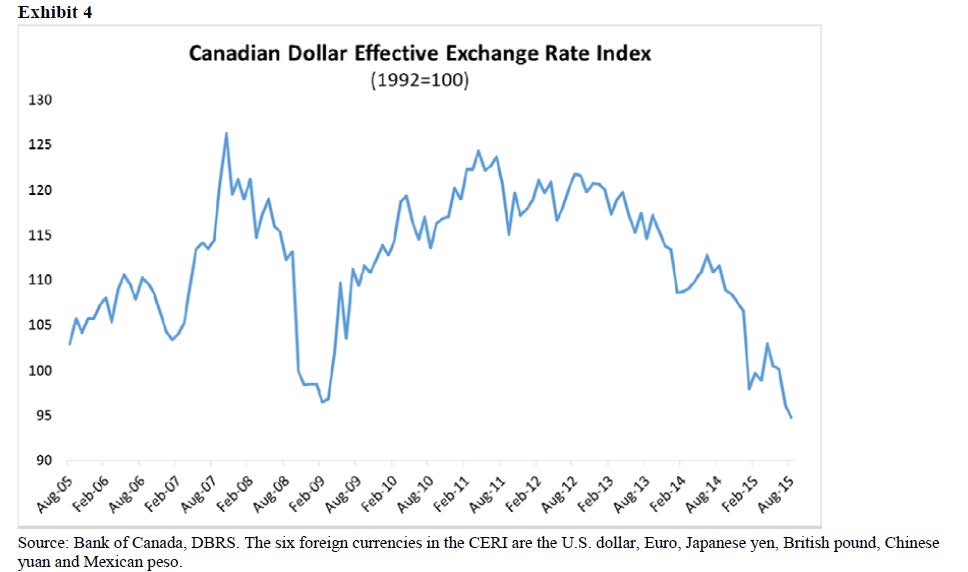

It would be interesting to learn just what “reforms to raise worker productivity” DBRS has in mind; the TPP will help a little, but only a little. As briefly mentioned on September 21, I don’t see how anybody could spend a lot of capital on productivity equipment when you know it will just get dusty every time the index goes above 110:

Click for Big

But “greater investment in infrastructure”? That should be a no-brainer, especially since Canada’s infrastructure is crumbling. But instead we are blessed with morons who believe balancing the budget each and every year is a sign of fiscal responsibility and nobody ever talks about the more important ‘through-the-cycle’ figure; preferring instead to discuss a modern version of sumptuary laws.

The International Monetary Fund cast a pessimistic view on Canada’s economic prospects for next year, warning that the depressed commodity prices that have slowed the Canadian and global economies in 2015 will remain a major threat to growth in 2016.

In its quarterly World Economic Outlook, entitled Adjusting to Lower Commodity Prices, the IMF once again reduced its gross domestic product forecasts for both Canada and the world as a whole, extending and deepening this year’s trend of falling expectations. The global finance agency’s forecast for Canadian GDP growth in 2015 is now just 1 per cent – down a half a percentage point from the previous forecast in July, and down 1.3 percentage points from a year ago.

On a cheerier note, the US is finding that spying costs money:

Safe Harbor was adopted by the European Commission in 2000 and recognizes a set of privacy principles by the U.S. Department of Commerce “as providing adequate protection for the purposes of personal data transfers from the EU,” according to the EU executive body. It has become a key trans-Atlantic data transfer mechanism, with more than 4,000 U.S. companies self-certified under it.

…

The ECJ struck down the Safe Harbor decision without providing companies with the option of a transition period. It will affect “countless organizations, who are now considering whether to turn to other data transfer mechanisms, including standard contractual clauses or consent, instead of relying on the current Safe Harbor,” said Bridget Treacy, a lawyer and privacy specialist at law firm Hunton & Williams. EU-U.S. data transfers now have to be blocked by national data protection authorities if they’re asked to investigate.

While two trends combine in an interesting way: small-scale equity crowdfunding for a drone manufacturer!

UAS Drone Corp., a developer of unmanned aerial vehicles for the law enforcement and first responder market (the “Company”), announced that it has commenced its Initial Public Offering of its common stock. The offering is being conducted directly by officers and directors of the Company through the Fundable.com equity crowdfunding platform.

It was back to normal for the Canadian preferred share market today, with PerpetualDiscounts off 13bp, FixedResets losing 52bp and DeemedRetractibles down 32bp. There is yet another lengthy Performance Highlights table, with insurance issues and TRP notable in the bad part. Volume was above average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

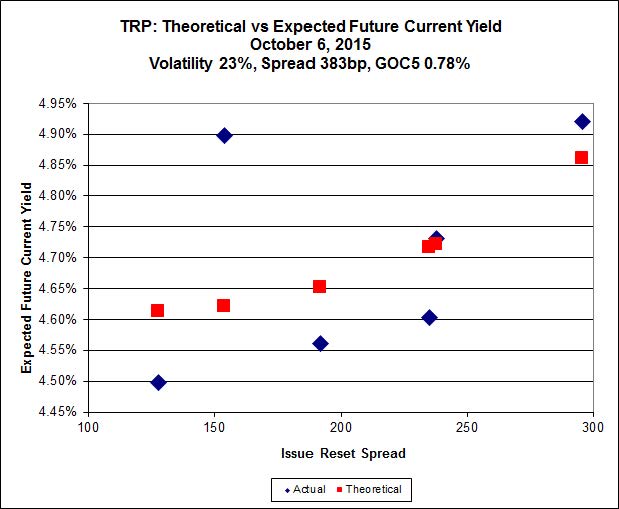

Here’s TRP:

Click for Big

Implied Volatility remained at an unreasonable level today.

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 17.00 to be $0.41 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.71 cheap at its bid price of 11.84.

Click for Big

Another good fit today for MFC, with Implied Volatility climbing substantially.

Most expensive is MFC.PR.M, resetting at +236bp on 2019-12-19, bid at 19.51 to be 0.71 rich, while MFC.PR.F resetting at +141bp on 2016-6-19, is bid at 14.04 to be 0.28 cheap.

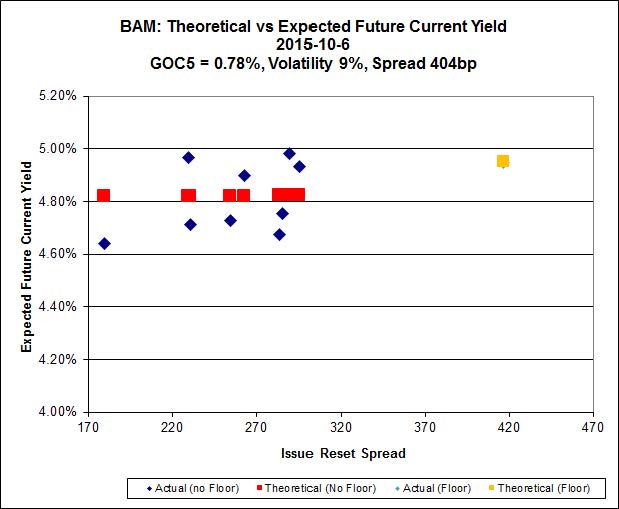

Click for Big

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PF.A, resetting at +290bp on 2018-9-30, bid at 18.47 to be $0.61 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 19.36 and appears to be $0.59 rich.

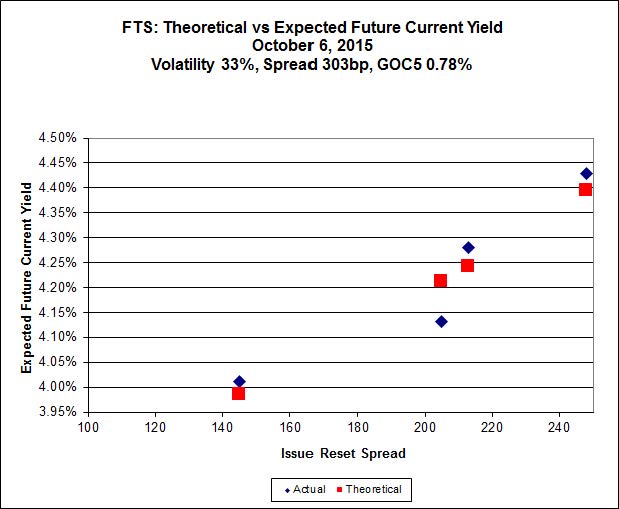

Click for Big

Implied Volatility increased again today to an even more ridiculously high level.

FTS.PR.K, with a spread of +205bp, and bid at 17.12, looks $0.32 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 17.00 and is $0.15 cheap.

Click for Big

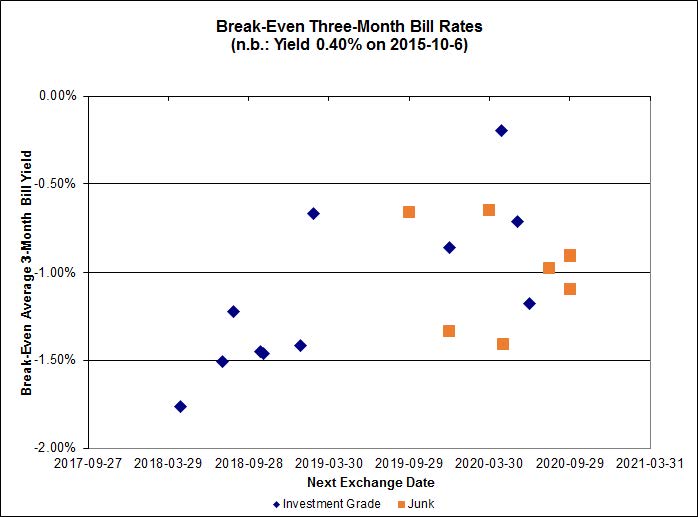

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.02%, with one outlier above 0.00%. The distribution is bimodal, with bank NVCC non-compliant pairs averaging -1.36% and other issues averaging -0.55%. There are three junk outliers above 0.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.6956 % | 1,571.1 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.6956 % | 2,746.9 |

| Floater | 4.73 % | 4.76 % | 63,766 | 15.97 | 3 | -0.6956 % | 1,670.1 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0215 % | 2,762.3 |

| SplitShare | 4.34 % | 4.91 % | 69,457 | 4.47 | 5 | 0.0215 % | 3,237.2 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0215 % | 2,525.8 |

| Perpetual-Premium | 5.83 % | 5.84 % | 56,523 | 13.87 | 5 | -0.1586 % | 2,468.9 |

| Perpetual-Discount | 5.70 % | 5.78 % | 73,751 | 14.21 | 33 | -0.1346 % | 2,494.2 |

| FixedReset | 5.21 % | 4.84 % | 195,388 | 15.10 | 76 | -0.5192 % | 1,955.7 |

| Deemed-Retractible | 5.26 % | 5.20 % | 102,429 | 5.48 | 33 | -0.3225 % | 2,529.6 |

| FloatingReset | 2.66 % | 4.62 % | 63,931 | 5.84 | 9 | -0.0239 % | 2,057.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.B | FixedReset | -3.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 11.45 Evaluated at bid price : 11.45 Bid-YTW : 4.59 % |

| MFC.PR.J | FixedReset | -2.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.65 Bid-YTW : 6.77 % |

| MFC.PR.K | FixedReset | -2.80 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.03 Bid-YTW : 7.59 % |

| MFC.PR.L | FixedReset | -2.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.00 Bid-YTW : 7.72 % |

| MFC.PR.H | FixedReset | -2.65 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.64 Bid-YTW : 6.00 % |

| SLF.PR.I | FixedReset | -2.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.55 Bid-YTW : 6.90 % |

| MFC.PR.I | FixedReset | -2.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.45 Bid-YTW : 6.53 % |

| FTS.PR.M | FixedReset | -1.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 18.40 Evaluated at bid price : 18.40 Bid-YTW : 4.76 % |

| BAM.PF.G | FixedReset | -1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 19.36 Evaluated at bid price : 19.36 Bid-YTW : 5.01 % |

| MFC.PR.G | FixedReset | -1.58 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.58 Bid-YTW : 6.40 % |

| RY.PR.Z | FixedReset | -1.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 18.73 Evaluated at bid price : 18.73 Bid-YTW : 4.32 % |

| RY.PR.H | FixedReset | -1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 18.73 Evaluated at bid price : 18.73 Bid-YTW : 4.36 % |

| TRP.PR.D | FixedReset | -1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 16.70 Evaluated at bid price : 16.70 Bid-YTW : 5.00 % |

| TRP.PR.A | FixedReset | -1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 14.80 Evaluated at bid price : 14.80 Bid-YTW : 4.84 % |

| BMO.PR.T | FixedReset | -1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 18.53 Evaluated at bid price : 18.53 Bid-YTW : 4.38 % |

| MFC.PR.N | FixedReset | -1.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.01 Bid-YTW : 7.09 % |

| TRP.PR.C | FixedReset | -1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 11.84 Evaluated at bid price : 11.84 Bid-YTW : 4.94 % |

| TRP.PR.E | FixedReset | -1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 4.99 % |

| RY.PR.M | FixedReset | -1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 19.50 Evaluated at bid price : 19.50 Bid-YTW : 4.49 % |

| SLF.PR.D | Deemed-Retractible | -1.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.10 Bid-YTW : 7.46 % |

| SLF.PR.E | Deemed-Retractible | -1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.25 Bid-YTW : 7.41 % |

| MFC.PR.M | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.51 Bid-YTW : 6.81 % |

| GWO.PR.Q | Deemed-Retractible | -1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.81 Bid-YTW : 6.47 % |

| FTS.PR.K | FixedReset | -1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 17.12 Evaluated at bid price : 17.12 Bid-YTW : 4.51 % |

| IFC.PR.C | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.19 Bid-YTW : 7.01 % |

| RY.PR.P | Perpetual-Discount | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 23.80 Evaluated at bid price : 24.14 Bid-YTW : 5.46 % |

| TD.PR.T | FloatingReset | -1.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.50 Bid-YTW : 4.48 % |

| CU.PR.H | Perpetual-Discount | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 22.65 Evaluated at bid price : 23.00 Bid-YTW : 5.79 % |

| FTS.PR.H | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 13.90 Evaluated at bid price : 13.90 Bid-YTW : 4.19 % |

| SLF.PR.B | Deemed-Retractible | -1.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.50 Bid-YTW : 6.92 % |

| TRP.PR.G | FixedReset | -1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 5.01 % |

| POW.PR.G | Perpetual-Discount | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 23.54 Evaluated at bid price : 24.00 Bid-YTW : 5.84 % |

| RY.PR.L | FixedReset | 1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.00 Bid-YTW : 4.01 % |

| W.PR.J | Perpetual-Discount | 1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 22.60 Evaluated at bid price : 22.85 Bid-YTW : 6.15 % |

| TD.PF.D | FixedReset | 1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 20.44 Evaluated at bid price : 20.44 Bid-YTW : 4.39 % |

| PWF.PR.T | FixedReset | 2.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 21.23 Evaluated at bid price : 21.23 Bid-YTW : 4.00 % |

| CM.PR.Q | FixedReset | 2.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 20.15 Evaluated at bid price : 20.15 Bid-YTW : 4.45 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.P | Perpetual-Discount | 449,729 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 23.80 Evaluated at bid price : 24.14 Bid-YTW : 5.46 % |

| BAM.PF.H | FixedReset | 363,175 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 23.15 Evaluated at bid price : 25.02 Bid-YTW : 4.92 % |

| MFC.PR.G | FixedReset | 108,946 | Desjardins crossed 100,000 at 20.90. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.58 Bid-YTW : 6.40 % |

| RY.PR.D | Deemed-Retractible | 68,286 | RBC crossed 23,800 at 24.85, bought 16,000 from TD at 24.80 and crossed another 19,700 at 24.81. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.79 Bid-YTW : 4.78 % |

| BMO.PR.W | FixedReset | 38,320 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-06 Maturity Price : 18.35 Evaluated at bid price : 18.35 Bid-YTW : 4.39 % |

| RY.PR.B | Deemed-Retractible | 37,701 | RBC crossed 27,700 at 24.85. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.84 Bid-YTW : 4.95 % |

| There were 40 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| VNR.PR.A | FixedReset | Quote: 18.30 – 20.99 Spot Rate : 2.6900 Average : 1.5067 YTW SCENARIO |

| MFC.PR.F | FixedReset | Quote: 14.04 – 15.75 Spot Rate : 1.7100 Average : 1.0198 YTW SCENARIO |

| GWO.PR.N | FixedReset | Quote: 13.70 – 14.50 Spot Rate : 0.8000 Average : 0.5412 YTW SCENARIO |

| GWO.PR.P | Deemed-Retractible | Quote: 23.80 – 24.50 Spot Rate : 0.7000 Average : 0.4559 YTW SCENARIO |

| TRP.PR.D | FixedReset | Quote: 16.70 – 17.34 Spot Rate : 0.6400 Average : 0.4508 YTW SCENARIO |

| TD.PF.C | FixedReset | Quote: 18.20 – 18.70 Spot Rate : 0.5000 Average : 0.3132 YTW SCENARIO |

It seems that there is always an excuse not to balance the budget. So now we only need to balance is through the cycle. Just how long is this cycle suppose to be?

The federal government has been running deficits from 2009 through 2015 and the current surplus does not reflect the recent severe drop in commodity prices.

If we really need infrastructure upgrades then raise taxes, I’m willing to pay my share.

Just how long is this cycle suppose to be?

Show me some credible estimates including at least one significant recession and I’ll let you know.

The current governments of both Canada and Ontariowe have both adopted the technique that worked so well for Flaherty when he was busy undermining Ontariowe’s finances: talk up a balanced budget in good times, while ignoring both the question of paying for the last recession and saving for the next one.

I note that the Parliamentary Budget Office’s publication Fiscal Sustainability Report 2015 uses a 75-year horizon and – you will be gratified to learn – projects a long-term federal government surplus.

However, it also envisages exponentially growing provincial debt and a continuation of the stated ‘no deficits, ever’ policy, which I believe is neither desirable nor politically feasible. I also note that the PBO claimed a structural federal deficit as of 2010; and as of 2014.