Morgan Stanley’s got an interesting view on the next Fed move – more easing!

Morgan Stanley, one of the 22 primary dealers that trade directly with the Fed, says its clients began discussing the possibility that central bankers will resume bond purchases — or cut interest rates to below zero — after a weaker-than-forecast U.S. employment report last week. The firm recommends buying medium-term Treasuries.

Another set of bond purchases would be the fourth round of the Fed’s program known as quantitative easing, dubbed QE4 by traders.

“Almost immediately after September nonfarm payrolls figures flashed on the screen, the phones started ringing,” Matthew Hornbach, Morgan Stanley’s head of global interest rate strategy in New York, wrote in a report Oct. 6. “What’s more likely: QE4 or negative rates?”

Deutsche Bank is writing off $7-billion:

The firm said it expects to book a 5.8 billion-euro writedown as higher capital requirements reduce the value of its investment bank and it adjusts the estimate of what it will receive in the disposal of its Postbank unit. The Frankfurt-based lender also is adding about 1.2 billion euros to its litigation reserves.

…

[Deutsche Bank AG co-Chief Executive Officer John] Cryan is seeking to avoid tapping shareholders for funds while focusing on reorganizing the bank to meet growing demands for buffers from regulators.

…

Deutsche Bank had turned to Postbank to diversify its funding mix by boosting consumer deposits in the midst of the global financial crisis. With its disposal, Deutsche Bank will cut its workforce by about 15,000, and the lender is considering cutting 8,000 additional jobs, a person with knowledge of the matter said last month.

Hillary Clinton attacked the markets today:

Hillary Clinton will propose a tax aimed at penalizing “harmful” high-frequency trading strategies and offer ways to strengthen the Volcker Rule, among other measures, as she unveils another set of proposals Thursday aimed at what she has termed risky Wall Street behavior.

The Democratic presidential front-runner plans to call for a tax targeting trading strategies that rely heavily on order cancellations, a Clinton aide said Wednesday, previewing her announcements on the condition of anonymity.

…

She will also suggest adjusting the Volcker Rule, by eliminating a provision that allows banks to invest up to three percent of their capital in hedge funds and reinstating the “swaps push-out” rule of Dodd-Frank, which was removed last year.

Specifically, certain un-cleared credit default swaps comprised most of the contracts that were included in the push-out rule, or Section 716 of the Dodd-Frank Act. The rule requires banks that wished engaged in this activity to place them in separate affiliates with higher capital requirements. As such, they would not be funded through the deposit gathering activities of banks, seen as an important lesson from the financial crisis.

“It is illogical to repeal the 716 push out requirement,” Federal Deposit Insurance Corporation vice chairman Thomas Hoenig, a former Federal Reserve Bank regional president, said last week. ”The main items that must be pushed out under 716 are uncleared credit default swaps (CDS), equity derivatives and commodities derivatives. These are, in relative terms, much smaller and where the greater risks and capital subsidy is most useful to these banking firms,” he said.

According to industry estimates, such contracts represent only 5 percent of the swaps universe. As Hoenig also noted, most firms have ”broker-dealer affiliates where they can place these activities, but these affiliates are not as richly subsidized, which helps explain these firms’ resistance to 716 push out.”

She also voiced discontent with the TPP:

Democratic presidential candidate Hillary Clinton voiced her opposition Wednesday to the Trans-Pacific Partnership trade deal, bucking her former boss and creating more distance between herself and possible primary rival Vice President Joe Biden.

“What I know about it, as of today, I am not in favor of what I have learned about it,” the former secretary of state said in an interview with PBS News Hour. “I don’t believe it’s going to meet the high bar I have set.”

Clinton was generally supportive of the deal during her four years working in President Barack Obama’s administration and allowed for some wiggle room to still support TPP or other future trade deals. In a written statement sent after the interview was released, she stipulated that she is “continuing to learn about the deals” of the agreement.

…

Vermont Senator Bernie Sanders, Clinton’s main challenger in the race, drew attention to the amount of time it took her to come to a verdict on an issue he has long opposed.“I’m glad that she reached that conclusion,” he told reporters in Washington. “This is a conclusion that I reached on day one.”

But attacking the market is quite fashionable – even Blackrock is in on the action:

BlackRock Inc., the world’s biggest asset manager, has its own remedy for days of extraordinary volatility in the U.S. equity market: Shut it down.

Among the fund company’s suggestions: The entire $23 trillion market should automatically come to a halt if a certain number of shares stop trading, giving traders time to regroup on a wild day, according to BlackRock. Tweaking the rules on halts and making all stock openings electronic are among other ideas in a paper published Wednesday by the firm.

…

Among other concerns are the widespread use of stop orders by retail investors, which many on Wall Street believe contributed to the volatility. Two people familiar with the matter said there have been discussions with brokers that offer stop orders about educating their clients on how to use them.While stop orders sound like they can protect an investor, they actually send an instruction to an exchange to execute a trade immediately at any price, commonly known as a market order. In volatile markets, that can mean orders to sell securities as prices are plunging. Data from NYSE show that it had nine times the number of market orders on Aug. 24 compared with an average day. Market orders as a percent of executed volume were four times higher than usual.

“Excessive use of market and stop-loss orders that seek ‘liquidity at any price’ inflamed the situation,” said the BlackRock paper, which recommended investors use limit orders instead.

As we all know by now, Canadians have a right to buy a house wherever they want at a price of their own choosing. This God-given right is attracting wider attention:

Despite British Columbia’s aversion to pipelines and affection for pot, housing affordability has pushed both aside as the number one issue raised by area residents in the run-up to Canada’s election this month. It’s not completely surprising given that Vancouver has become North America’s most expensive city.

Surging purchase prices have triggered protest movements like #donthave1million, started by a group of young professionals frustrated at being shut out of home ownership. They complain of having to delay starting families as they remain bunked in with roommates, often into their 30s and beyond.

The affordability issue speaks to broader campaign themes: the difficulty young people face getting established in the labor market, the economic anxieties of the middle class, growing concerns about income inequality, support for families with children. Residents also increasingly point fingers at wealthy Chinese immigrants and investors whose lavish embrace of the Pacific metropolis of 2.5 million has inspired reality TV shows with such gaudy names as “Ultra Rich Asian Girls in Vancouver.”

It’s happening in Japan, too:

Realty agencies in Beijing are organizing twice-monthly tours to Tokyo and Osaka, where 40 Chinese at a time come for three-day property-shopping trips, seeking safe places to invest their cash abroad. They’re being prompted by the yen’s decline to 22-year lows and excitement over the 2020 Tokyo Olympics driving up prices, as they did in Beijing in 2008. Property tours will soon start from Shanghai too.

Partly as a result of nascent Chinese buying, Tokyo apartment prices have reached the highest levels since the early 1990s, up 11 percent over two years, according to the Real Estate Economic Institute Co.

…

While the home price-to-income ratio — the cost of a home relative to a buyer’s average annual income — rose to more than 10 times in Tokyo last year, according to according to property appraisal company Tokyo Kantei Co., it’s still below the 18 times it reached during the bubble era in the late 1980s and early 1990s.

Yet another federal candidate has been dumped by his party:

A party spokeswoman said Tuesday night that Grewal’s comments “are not reflective of the views of the Conservative Party of Canada.”

We are getting to the point at which only three all-encompassing political stances, carefully vetted by the party leaders’ offices, will be permitted in the House of Commons. This will give us more opportunity to complain that MPs are nothing more than trained seals, so that’s good, right?

It was another poor day for the Canadian preferred share market, with PerpetualDiscounts down 18bp, FixedResets off 5bp and DeemedRetractibles losing 33bp. Insurance issues and TRP were again prominent on the bad side of the lengthy Performance Highlights table. Volume was high.

PerpetualDiscounts now yield 5.79%, equivalent to 7.53% interest at the standard equivalency factor of 1.3x. Long corporates now yield a little over 4.2%, so the pre-tax interest-equivalent spread is now about 330bp, a slight (and perhaps spurious) widening from the 325bp reported September 30.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

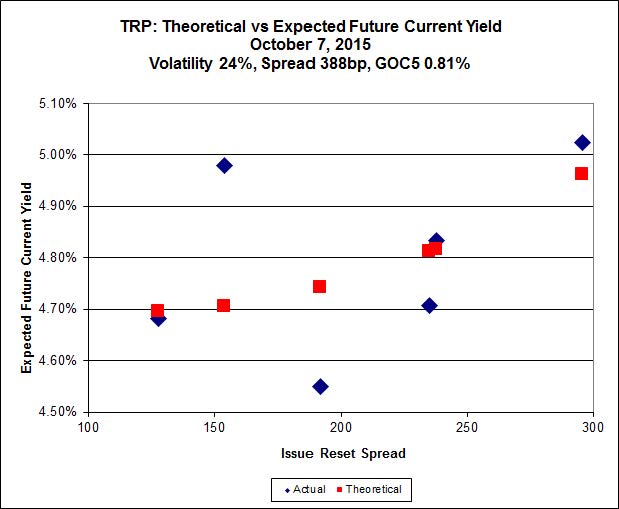

Here’s TRP:

Click for Big

Implied Volatility remained at an unreasonable level today.

TRP.PR.A, which resets 2019-12-31 at +192, is bid at 15.00 to be $0.61 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.69 cheap at its bid price of 11.80.

Click for Big

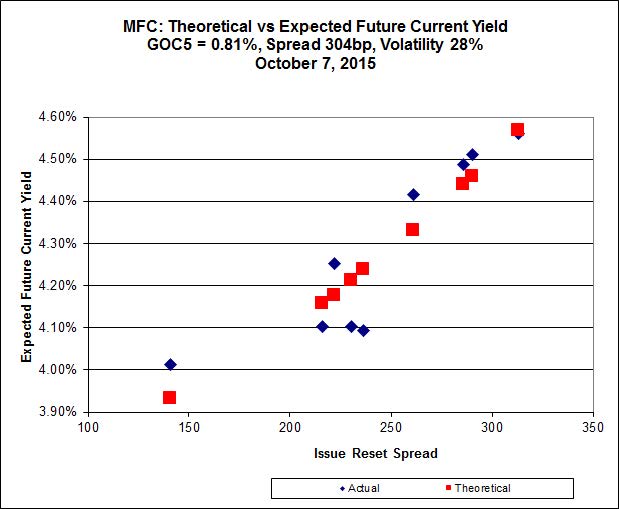

Another good fit today for MFC, with Implied Volatility easing a bit.

Most expensive is MFC.PR.M, resetting at +236bp on 2019-12-19, bid at 19.36 to be 0.66 rich, while MFC.PR.J resetting at +261bp on 2018-3-19, is bid at 19.36 to be 0.38 cheap.

Click for Big

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 15.31 to be $0.82 cheap. BAM.PR.X, resetting at +180bp on 2017-6-30 is bid at 14.45 and appears to be $0.91 rich.

Click for Big

Implied Volatility increased again today to an even more ridiculously high level.

FTS.PR.K, with a spread of +205bp, and bid at 17.00, looks $0.37 expensive and resets 2019-3-1. FTS.PR.M, with a spread of +248bp and resetting 2019-12-1, is bid at 18.05 and is $0.18 cheap.

Click for Big

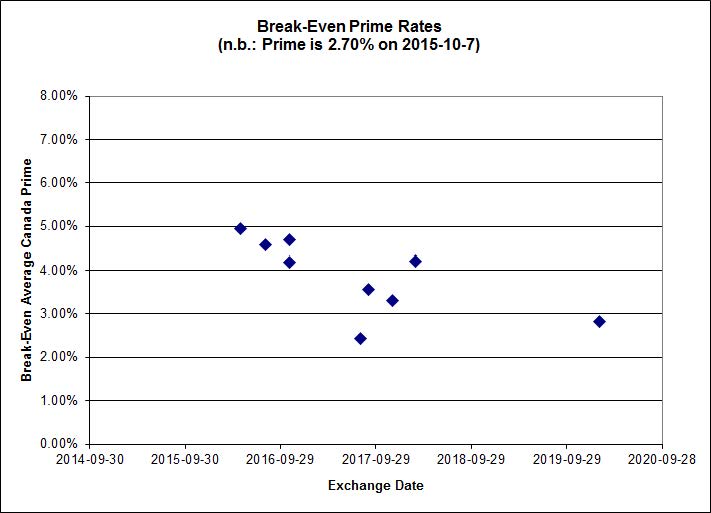

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.01%, with one outlier above 0.00%. The distribution is bimodal, with bank NVCC non-compliant pairs averaging -1.32% and other issues averaging -0.57%. There are three junk outliers above 0.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0334 % | 1,571.6 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0334 % | 2,747.8 |

| Floater | 4.73 % | 4.74 % | 63,225 | 16.00 | 3 | 0.0334 % | 1,670.7 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2627 % | 2,769.5 |

| SplitShare | 4.33 % | 4.98 % | 70,767 | 3.01 | 5 | 0.2627 % | 3,245.7 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2627 % | 2,532.4 |

| Perpetual-Premium | 5.88 % | 5.80 % | 56,812 | 2.80 | 5 | 0.3778 % | 2,478.2 |

| Perpetual-Discount | 5.72 % | 5.79 % | 74,105 | 14.18 | 33 | -0.1820 % | 2,489.6 |

| FixedReset | 5.21 % | 4.83 % | 195,704 | 15.13 | 76 | -0.0541 % | 1,954.7 |

| Deemed-Retractible | 5.28 % | 5.15 % | 102,660 | 5.48 | 33 | -0.3339 % | 2,521.2 |

| FloatingReset | 2.66 % | 4.53 % | 63,560 | 5.84 | 9 | 0.0805 % | 2,059.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| SLF.PR.H | FixedReset | -4.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.50 Bid-YTW : 8.46 % |

| TRP.PR.B | FixedReset | -2.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 11.16 Evaluated at bid price : 11.16 Bid-YTW : 4.72 % |

| POW.PR.D | Perpetual-Discount | -2.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 5.85 % |

| CU.PR.C | FixedReset | -2.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 18.70 Evaluated at bid price : 18.70 Bid-YTW : 4.41 % |

| FTS.PR.M | FixedReset | -1.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 18.05 Evaluated at bid price : 18.05 Bid-YTW : 4.85 % |

| PWF.PR.K | Perpetual-Discount | -1.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 5.77 % |

| SLF.PR.A | Deemed-Retractible | -1.73 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.03 Bid-YTW : 7.17 % |

| SLF.PR.B | Deemed-Retractible | -1.63 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.15 Bid-YTW : 7.15 % |

| MFC.PR.F | FixedReset | -1.50 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.83 Bid-YTW : 9.86 % |

| SLF.PR.C | Deemed-Retractible | -1.49 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.90 Bid-YTW : 7.60 % |

| MFC.PR.J | FixedReset | -1.48 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.36 Bid-YTW : 6.98 % |

| ELF.PR.F | Perpetual-Discount | -1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 22.09 Evaluated at bid price : 22.37 Bid-YTW : 5.94 % |

| MFC.PR.C | Deemed-Retractible | -1.33 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.03 Bid-YTW : 7.59 % |

| TRP.PR.E | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 16.78 Evaluated at bid price : 16.78 Bid-YTW : 5.06 % |

| TRP.PR.G | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 18.76 Evaluated at bid price : 18.76 Bid-YTW : 5.08 % |

| PWF.PR.T | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 20.70 Evaluated at bid price : 20.70 Bid-YTW : 4.03 % |

| BAM.PR.R | FixedReset | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 15.31 Evaluated at bid price : 15.31 Bid-YTW : 5.21 % |

| MFC.PR.K | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.81 Bid-YTW : 7.76 % |

| GWO.PR.G | Deemed-Retractible | -1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.71 Bid-YTW : 6.59 % |

| POW.PR.B | Perpetual-Discount | -1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 22.56 Evaluated at bid price : 22.82 Bid-YTW : 5.88 % |

| TRP.PR.D | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 16.50 Evaluated at bid price : 16.50 Bid-YTW : 5.06 % |

| GWO.PR.R | Deemed-Retractible | -1.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.35 Bid-YTW : 7.02 % |

| MFC.PR.B | Deemed-Retractible | -1.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.62 Bid-YTW : 7.36 % |

| ELF.PR.H | Perpetual-Discount | -1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 22.85 Evaluated at bid price : 23.22 Bid-YTW : 5.93 % |

| SLF.PR.D | Deemed-Retractible | -1.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.88 Bid-YTW : 7.61 % |

| TD.PF.E | FixedReset | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 21.05 Evaluated at bid price : 21.05 Bid-YTW : 4.37 % |

| GWO.PR.I | Deemed-Retractible | -1.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.58 Bid-YTW : 7.19 % |

| BAM.PF.G | FixedReset | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 19.56 Evaluated at bid price : 19.56 Bid-YTW : 4.96 % |

| FTS.PR.J | Perpetual-Discount | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 21.22 Evaluated at bid price : 21.22 Bid-YTW : 5.67 % |

| HSE.PR.A | FixedReset | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 13.30 Evaluated at bid price : 13.30 Bid-YTW : 4.89 % |

| BAM.PF.E | FixedReset | 1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 17.80 Evaluated at bid price : 17.80 Bid-YTW : 5.12 % |

| TD.PF.C | FixedReset | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 18.41 Evaluated at bid price : 18.41 Bid-YTW : 4.35 % |

| BSC.PR.C | SplitShare | 1.22 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2016-09-22 Maturity Price : 19.71 Evaluated at bid price : 19.95 Bid-YTW : 2.89 % |

| BAM.PF.A | FixedReset | 1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 18.70 Evaluated at bid price : 18.70 Bid-YTW : 5.15 % |

| BAM.PF.B | FixedReset | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 17.62 Evaluated at bid price : 17.62 Bid-YTW : 5.12 % |

| TRP.PR.A | FixedReset | 1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 15.00 Evaluated at bid price : 15.00 Bid-YTW : 4.77 % |

| RY.PR.H | FixedReset | 1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 4.30 % |

| RY.PR.J | FixedReset | 1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 20.25 Evaluated at bid price : 20.25 Bid-YTW : 4.43 % |

| RY.PR.Z | FixedReset | 2.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 19.25 Evaluated at bid price : 19.25 Bid-YTW : 4.20 % |

| BAM.PR.X | FixedReset | 3.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 14.45 Evaluated at bid price : 14.45 Bid-YTW : 4.83 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BAM.PF.H | FixedReset | 170,510 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 23.16 Evaluated at bid price : 25.05 Bid-YTW : 4.91 % |

| CU.PR.I | FixedReset | 89,211 | RBC crossed 25,000 at 25.05. Nesbitt crossed blocks of 25,000 and 20,000, both at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 23.15 Evaluated at bid price : 25.01 Bid-YTW : 4.41 % |

| RY.PR.P | Perpetual-Discount | 82,029 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 23.72 Evaluated at bid price : 24.05 Bid-YTW : 5.48 % |

| RY.PR.Z | FixedReset | 61,910 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 19.25 Evaluated at bid price : 19.25 Bid-YTW : 4.20 % |

| TRP.PR.G | FixedReset | 34,621 | RBC crossed 24,200 at 18.90. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 18.76 Evaluated at bid price : 18.76 Bid-YTW : 5.08 % |

| TRP.PR.D | FixedReset | 34,264 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-07 Maturity Price : 16.50 Evaluated at bid price : 16.50 Bid-YTW : 5.06 % |

| There were 48 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TD.PF.B | FixedReset | Quote: 18.71 – 21.40 Spot Rate : 2.6900 Average : 1.4675 YTW SCENARIO |

| POW.PR.D | Perpetual-Discount | Quote: 21.50 – 22.24 Spot Rate : 0.7400 Average : 0.4471 YTW SCENARIO |

| MFC.PR.C | Deemed-Retractible | Quote: 20.03 – 20.50 Spot Rate : 0.4700 Average : 0.3171 YTW SCENARIO |

| TRP.PR.A | FixedReset | Quote: 15.00 – 15.56 Spot Rate : 0.5600 Average : 0.4087 YTW SCENARIO |

| PWF.PR.K | Perpetual-Discount | Quote: 21.50 – 21.88 Spot Rate : 0.3800 Average : 0.2317 YTW SCENARIO |

| BNS.PR.D | FloatingReset | Quote: 18.52 – 18.89 Spot Rate : 0.3700 Average : 0.2346 YTW SCENARIO |