The Fed didn’t hike rates in September largely due to global risks:

Federal Reserve officials put off an interest-rate increase in September because of growing risks, mainly from China, to their outlook for economic growth and inflation even as they continued to say they were on track to raise the target later this year.

Policy makers “agreed that developments over the inter-meeting period had not materially altered the committee’s economic outlook,” according to minutes of the Sept. 16-17 session of the Federal Open Market Committee, released Thursday in Washington. Nonetheless, “the committee decided that it was prudent to wait for additional information confirming that the economic outlook had not deteriorated.”

The FOMC noted that domestic economic conditions, including data on consumer spending and housing, had continued to improve, and the labor market had reached or was close to the committee’s long-run estimates for unemployment.

Still, concerns over China and its potential spillover to other economies “were likely to depress U.S. net exports” and cause further strengthening of the dollar, which could damp inflation in the U.S.

The torrent of global money into California real estate is slowing:

International buyers are accounting for the smallest share of California home sales in at least eight years as prices climb and investors from China, the biggest source of foreign purchases, slow buying, according to the state’s Realtors group.

The share of international buyers fell this year to less than 4 percent, compared with a peak of 8 percent in 2013, the California Association of Realtors said in a report Thursday. The findings are based on a survey conducted in June of about 1,000 real estate agents. Since 2008, the first year agents were surveyed on the subject, results have shown foreigners representing at least 5 percent of transactions.

An influx of foreign money has contributed to soaring real estate prices in the largest U.S. state, particularly in coastal areas where demand is high and new inventory is limited. Buyers from mainland China, Hong Kong and Taiwan made up 43 percent of international purchases in California this year, followed by 8 percent each from Mexico and South Korea, according to the survey.

…

The median price of a California home is expected to climb 6.5 percent this year to $476,300, making it harder to find deals, according to Appleton-Young. Chinese buyers have focused their purchasing on a few areas such as the San Gabriel Valley and Irvine, outside Los Angeles, and parts of the San Francisco Bay area with reputations for quality schools.Across the U.S., buyers from China, Hong Kong and Taiwan spent an estimated $28.6 billion on homes in the 12 months through March, the National Association of Realtors reported in June, more than double the $11.2 billion spent by No. 2 Canada. The average price was $831,800 for Chinese purchasers, compared with $499,600 for all international buyers.

California accounted for 16 percent of U.S. sales to foreign buyers, behind Florida, which had 21 percent, the national association’s report said.

Let’s hope that some of that missing money finds its way into Canada!

Hillary Clinton wrote an op-ed outlining her attack on markets:

My plan would also give regulators the authority they need to reorganize, downsize or even break apart any financial institution that is too large and risky to be managed effectively. It is a comprehensive and flexible approach. It allows regulators to adapt to changing markets and help ensure that large financial firms never pose a danger to our entire economy.

Not because they’re in trouble – because they’re too large and risky! Coming up next … jail terms for those likely to commit an offence! Matt Levine of Bloomberg opines:

And yet you can see the populist appeal. Wall Street, to a lot of people, is Wall Street, and any attack on “Wall Street” sounds good. The political desire is to have a certain quantity of “tough on Wall Street,” but what actually goes into that toughness is arbitrary and unimportant. So Clinton also wants to “reinstate the ‘swaps push-out’ rule for banks’ derivatives trading, which was repealed at the behest of the banking lobby in last year’s budget deal.” I have long thought that swaps push-out is the purest piece of symbolic emotional identification in financial regulation, and I still think that, but for precisely that reason it resonates. No one knows what it does, and no one thinks that it matters, so it is useful as a pure abstract marker of what team you’re on.

But for those of us who are more interested in finance than in politics, this just seems weird. Wall Street is not a monolith, and being “tough on Wall Street” makes no sense. Regulating the parts of Wall Street that you don’t like can help out the parts of Wall Street that you do like. Lots of hedge fund managers will be thrilled by a crackdown on high-frequency trading.15 Cracking down on small automated competitors to banks might be good for banks. There are Wall Street winners and Wall Street losers to all sorts of Wall Street regulation, and a pure quantity theory of toughness elides those differences.

Canada’s wealth management industry is asking the Ontario government for tighter regulations to restrict competition in the wealth management industry:

Canada’s wealth management industry is asking the Ontario government for tighter regulations governing financial planners and advisers.

Earlier this year, the province launched an expert committee to review the regulations, and a number of financial industry groups have responded by asking the government to enact a general legislative framework for advisers and planners.

Currently, throughout most of Canada, no general legal framework exists to regulate the activities of individuals who offer financial planning, advice and services. That means that in every province (excluding Quebec) any individual can call himself a financial planner – regardless of certification, designation or educational background.

The absence of a legal framework has raised questions within the industry about proficiency, quality standards and potential conflicts of interest.

… and competition from outfits that are not banks. That’s a real problem. However, the banks have shown their willingness in the past to pay regulators to expand their hegemony over the financial system, so guess what’s going to happen next?

Here’s a feel-good story about Canadian service sector innovation:

Like everyone, Cris Jucan has had his share of frustrating restaurant experiences. He remembers one vividly, a few years ago, when he and his friends were sitting around on a patio waiting to order drinks.

They joked that one of them should call the restaurant – on the phone – and ask that a server be sent over. That’s when the veritable light bulb went off.

Mr. Jucan, with his background in IT, wasted no time in founding Tacit Innovations, a startup that would seek to improve the restaurant experience by allowing patrons to browse menus and order meals with their phones.

…

Toronto-based Tacit Innovations, now up to 15 employees, is one of a growing number of companies tapping into the increasing tech savviness of restaurant owners and their desire to improve efficiencies, profits and customer experiences.

Veritable light bulb? I believe the writer meant “proverbial”.

But how about that preferred share market, eh? It was a walk in the park!

Click for Big

The Canadian preferred share market was hammered today, with PerpetualDiscounts off 45bp, FixedResets losing 169bp and DeemedRetractibles down 78bp. I cannot find sufficient superlatives to describe the Performance Highlights table. Volume was very high.

It is possible that the market was reacting to the news of the new private placement from BMO, which pays 5.85% … if this is a dividend and the bank needs the money that much, then the drop is justified. If the payments are taxed as interest, not so much. I don’t know. Or it could be the market just going down because it felt like it. I don’t know about that, either.

On a cheerier note, the increases in observed Implied Volatility suggest to me that we’re seeing some bottom feeding in the market, with the speculators (and, perhaps, long term buyers) seeking out the lowest-spread, lowest-priced issues (because then they get more leverage to future increases in GOC-5) and supporting their price relative to that of their higher-spread, higher-priced cousins. If so, it implies heightened awareness … and it is also possible that the new BMO issue represents an institutional desire to get in on the action with some serious money. This is what will eventually turn the tide, of course. But not yet!

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

Here’s TRP:

Click for Big

Implied Volatility rocketed upwards today and is now ridiculous.

TRP.PR.A, which resets 2019-12-31 at +192, is bid at 14.55 to be $0.49 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.52 cheap at its bid price of 11.83.

Click for Big

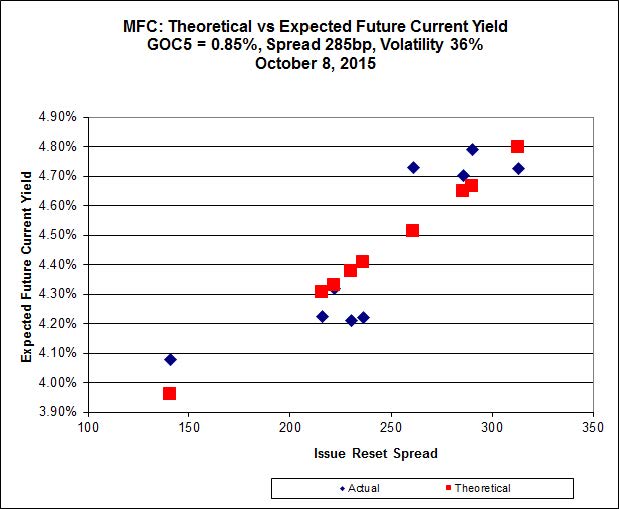

Another good fit today for MFC, with Implied Volatility jumping up.

Most expensive is MFC.PR.M, resetting at +236bp on 2019-12-19, bid at 19.02 to be 0.81 rich, while MFC.PR.J resetting at +261bp on 2018-3-19, is bid at 18.29 to be 0.89 cheap.

Click for Big

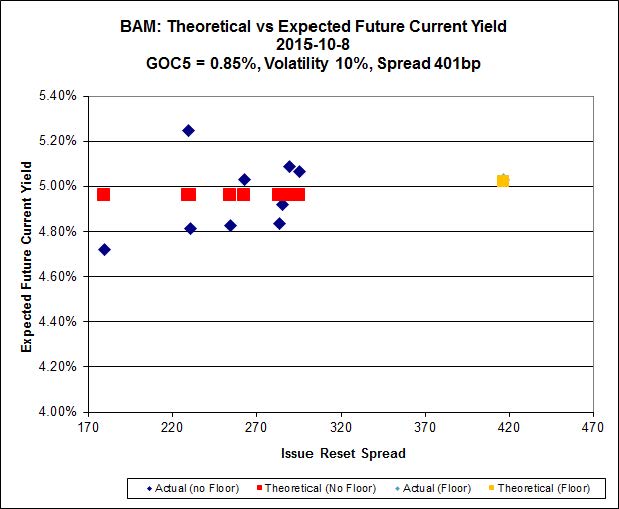

The fit on the BAM issues continues to be horrible, and Implied Volatility actually declined! But the relationship between the BAM FixedResets is just a mess, so I’m not taking it too seriously.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 15.01 to be $0.87 cheap. BAM.PR.X, resetting at +180bp on 2017-6-30 is bid at 14.03 and appears to be $0.67 rich.

Click for Big

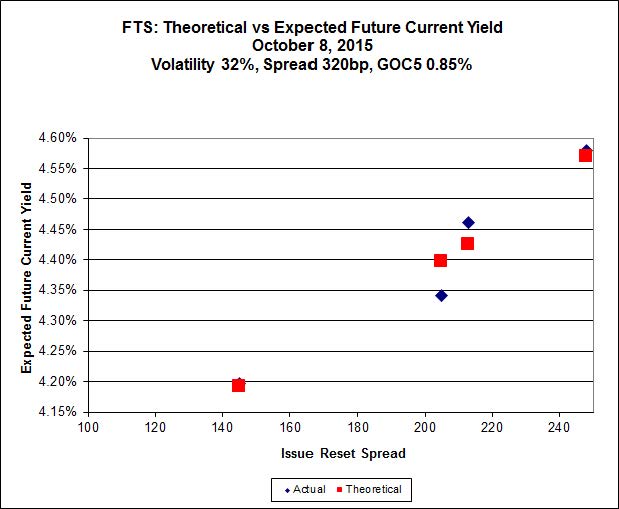

Implied Volatility declined today but remains ridiculously high.

FTS.PR.K, with a spread of +205bp, and bid at 16.70, looks $0.21 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 16.70 and is $0.14 cheap.

Click for Big

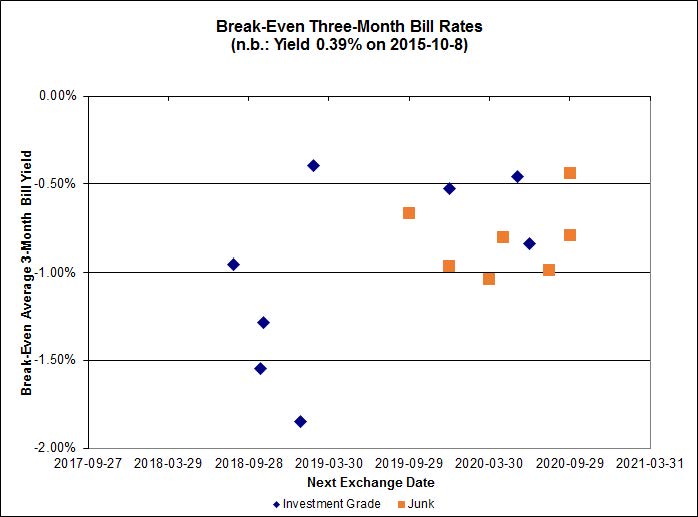

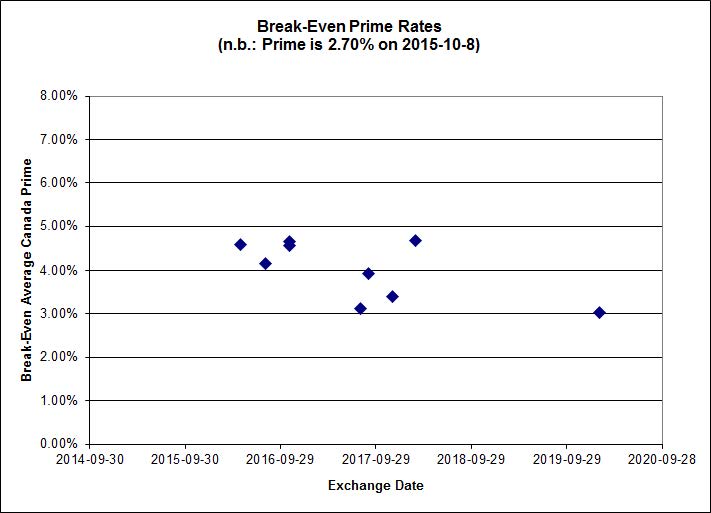

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.00%, with two outliers above 0.00% and two below -2.00%. The distribution is bimodal, with bank NVCC non-compliant pairs averaging -1.55% and other issues averaging -0.23%. There are three junk outliers above 0.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1667 % | 1,574.2 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1667 % | 2,752.4 |

| Floater | 4.72 % | 4.73 % | 63,976 | 16.01 | 3 | 0.1667 % | 1,673.5 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2496 % | 2,762.6 |

| SplitShare | 4.34 % | 5.06 % | 71,512 | 4.47 | 5 | -0.2496 % | 3,237.6 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2496 % | 2,526.1 |

| Perpetual-Premium | 5.92 % | 5.87 % | 57,953 | 14.00 | 5 | -0.8087 % | 2,458.2 |

| Perpetual-Discount | 5.75 % | 5.80 % | 78,691 | 14.19 | 33 | -0.4507 % | 2,478.4 |

| FixedReset | 5.31 % | 4.85 % | 196,358 | 14.95 | 76 | -1.6946 % | 1,921.5 |

| Deemed-Retractible | 5.32 % | 5.42 % | 101,858 | 5.47 | 33 | -0.7806 % | 2,501.5 |

| FloatingReset | 2.68 % | 4.88 % | 62,838 | 5.83 | 9 | -0.7755 % | 2,043.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| MFC.PR.J | FixedReset | -5.53 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.29 Bid-YTW : 7.75 % |

| TD.PF.E | FixedReset | -4.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 20.01 Evaluated at bid price : 20.01 Bid-YTW : 4.59 % |

| MFC.PR.G | FixedReset | -4.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.57 Bid-YTW : 7.08 % |

| RY.PR.J | FixedReset | -4.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 19.29 Evaluated at bid price : 19.29 Bid-YTW : 4.66 % |

| TRP.PR.E | FixedReset | -4.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 16.04 Evaluated at bid price : 16.04 Bid-YTW : 5.30 % |

| TD.PF.D | FixedReset | -4.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 19.37 Evaluated at bid price : 19.37 Bid-YTW : 4.64 % |

| TRP.PR.D | FixedReset | -4.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 15.82 Evaluated at bid price : 15.82 Bid-YTW : 5.28 % |

| TRP.PR.G | FixedReset | -4.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 5.30 % |

| RY.PR.M | FixedReset | -3.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 4.68 % |

| NA.PR.W | FixedReset | -3.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 17.42 Evaluated at bid price : 17.42 Bid-YTW : 4.64 % |

| MFC.PR.I | FixedReset | -3.57 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.72 Bid-YTW : 7.03 % |

| IFC.PR.A | FixedReset | -3.45 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.40 Bid-YTW : 9.39 % |

| BMO.PR.Y | FixedReset | -3.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 19.31 Evaluated at bid price : 19.31 Bid-YTW : 4.77 % |

| HSE.PR.E | FixedReset | -3.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 21.66 Evaluated at bid price : 22.00 Bid-YTW : 5.01 % |

| TD.PR.T | FloatingReset | -3.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.86 Bid-YTW : 5.01 % |

| TD.PF.C | FixedReset | -3.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 17.85 Evaluated at bid price : 17.85 Bid-YTW : 4.49 % |

| TRP.PR.A | FixedReset | -3.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 14.55 Evaluated at bid price : 14.55 Bid-YTW : 4.93 % |

| IFC.PR.C | FixedReset | -2.98 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.54 Bid-YTW : 7.48 % |

| BAM.PR.X | FixedReset | -2.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 14.03 Evaluated at bid price : 14.03 Bid-YTW : 4.98 % |

| TD.PF.F | Perpetual-Discount | -2.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 22.18 Evaluated at bid price : 22.53 Bid-YTW : 5.43 % |

| TD.PF.A | FixedReset | -2.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 18.20 Evaluated at bid price : 18.20 Bid-YTW : 4.42 % |

| TD.PF.B | FixedReset | -2.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 18.22 Evaluated at bid price : 18.22 Bid-YTW : 4.41 % |

| NA.PR.S | FixedReset | -2.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 18.06 Evaluated at bid price : 18.06 Bid-YTW : 4.65 % |

| BMO.PR.W | FixedReset | -2.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 17.98 Evaluated at bid price : 17.98 Bid-YTW : 4.49 % |

| MFC.PR.H | FixedReset | -2.55 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.05 Bid-YTW : 6.38 % |

| SLF.PR.E | Deemed-Retractible | -2.54 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.60 Bid-YTW : 7.87 % |

| SLF.PR.C | Deemed-Retractible | -2.51 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.40 Bid-YTW : 7.96 % |

| POW.PR.A | Perpetual-Discount | -2.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 23.20 Evaluated at bid price : 23.50 Bid-YTW : 5.98 % |

| BAM.PF.G | FixedReset | -2.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 19.08 Evaluated at bid price : 19.08 Bid-YTW : 5.09 % |

| BMO.PR.T | FixedReset | -2.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 18.20 Evaluated at bid price : 18.20 Bid-YTW : 4.47 % |

| SLF.PR.G | FixedReset | -2.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.50 Bid-YTW : 9.04 % |

| RY.PR.Z | FixedReset | -2.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 18.80 Evaluated at bid price : 18.80 Bid-YTW : 4.30 % |

| SLF.PR.B | Deemed-Retractible | -2.32 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.66 Bid-YTW : 7.48 % |

| BNS.PR.C | FloatingReset | -2.29 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.31 Bid-YTW : 4.94 % |

| SLF.PR.D | Deemed-Retractible | -2.26 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.43 Bid-YTW : 7.94 % |

| SLF.PR.I | FixedReset | -2.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.98 Bid-YTW : 7.31 % |

| FTS.PR.H | FixedReset | -2.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 13.70 Evaluated at bid price : 13.70 Bid-YTW : 4.25 % |

| GWO.PR.I | Deemed-Retractible | -2.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.14 Bid-YTW : 7.49 % |

| SLF.PR.A | Deemed-Retractible | -2.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.60 Bid-YTW : 7.46 % |

| BAM.PR.R | FixedReset | -1.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 15.01 Evaluated at bid price : 15.01 Bid-YTW : 5.32 % |

| GWO.PR.G | Deemed-Retractible | -1.94 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.27 Bid-YTW : 6.87 % |

| RY.PR.O | Perpetual-Discount | -1.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 22.18 Evaluated at bid price : 22.53 Bid-YTW : 5.53 % |

| CM.PR.P | FixedReset | -1.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 17.72 Evaluated at bid price : 17.72 Bid-YTW : 4.52 % |

| BAM.PF.B | FixedReset | -1.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 17.30 Evaluated at bid price : 17.30 Bid-YTW : 5.22 % |

| BAM.PF.F | FixedReset | -1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 18.85 Evaluated at bid price : 18.85 Bid-YTW : 5.13 % |

| FTS.PR.K | FixedReset | -1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 16.70 Evaluated at bid price : 16.70 Bid-YTW : 4.63 % |

| MFC.PR.M | FixedReset | -1.76 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.02 Bid-YTW : 7.16 % |

| CM.PR.Q | FixedReset | -1.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 19.80 Evaluated at bid price : 19.80 Bid-YTW : 4.54 % |

| PWF.PR.S | Perpetual-Discount | -1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 20.53 Evaluated at bid price : 20.53 Bid-YTW : 5.86 % |

| GWO.PR.H | Deemed-Retractible | -1.63 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.16 Bid-YTW : 7.20 % |

| CU.PR.C | FixedReset | -1.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 18.40 Evaluated at bid price : 18.40 Bid-YTW : 4.48 % |

| MFC.PR.L | FixedReset | -1.60 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.81 Bid-YTW : 7.87 % |

| RY.PR.N | Perpetual-Discount | -1.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 22.44 Evaluated at bid price : 22.74 Bid-YTW : 5.53 % |

| RY.PR.H | FixedReset | -1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 18.70 Evaluated at bid price : 18.70 Bid-YTW : 4.37 % |

| BMO.PR.S | FixedReset | -1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 18.80 Evaluated at bid price : 18.80 Bid-YTW : 4.43 % |

| CM.PR.O | FixedReset | -1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 18.51 Evaluated at bid price : 18.51 Bid-YTW : 4.43 % |

| BAM.PF.A | FixedReset | -1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 18.42 Evaluated at bid price : 18.42 Bid-YTW : 5.23 % |

| GWO.PR.R | Deemed-Retractible | -1.41 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.05 Bid-YTW : 7.22 % |

| BNS.PR.B | FloatingReset | -1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.15 Bid-YTW : 4.88 % |

| GWO.PR.L | Deemed-Retractible | -1.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.26 Bid-YTW : 6.13 % |

| PWF.PR.T | FixedReset | -1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 20.43 Evaluated at bid price : 20.43 Bid-YTW : 4.08 % |

| MFC.PR.N | FixedReset | -1.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.71 Bid-YTW : 7.31 % |

| GWO.PR.P | Deemed-Retractible | -1.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.36 Bid-YTW : 6.41 % |

| PWF.PR.G | Perpetual-Premium | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 24.51 Evaluated at bid price : 24.74 Bid-YTW : 5.97 % |

| PWF.PR.H | Perpetual-Premium | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 24.21 Evaluated at bid price : 24.50 Bid-YTW : 5.87 % |

| BSC.PR.C | SplitShare | -1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2020-09-22 Maturity Price : 19.71 Evaluated at bid price : 19.73 Bid-YTW : 4.04 % |

| BNS.PR.Q | FixedReset | -1.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.51 Bid-YTW : 4.12 % |

| PWF.PR.O | Perpetual-Premium | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 24.36 Evaluated at bid price : 24.66 Bid-YTW : 5.88 % |

| PWF.PR.L | Perpetual-Discount | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 21.98 Evaluated at bid price : 22.21 Bid-YTW : 5.74 % |

| BAM.PF.E | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 17.61 Evaluated at bid price : 17.61 Bid-YTW : 5.18 % |

| MFC.PR.B | Deemed-Retractible | -1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.40 Bid-YTW : 7.51 % |

| TD.PR.Y | FixedReset | -1.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.32 Bid-YTW : 4.23 % |

| BAM.PR.Z | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 18.81 Evaluated at bid price : 18.81 Bid-YTW : 5.22 % |

| FTS.PR.J | Perpetual-Discount | -1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 5.74 % |

| BNS.PR.Y | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.31 Bid-YTW : 6.22 % |

| W.PR.J | Perpetual-Discount | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 22.90 Evaluated at bid price : 23.17 Bid-YTW : 6.06 % |

| W.PR.H | Perpetual-Discount | 1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 22.77 Evaluated at bid price : 23.05 Bid-YTW : 5.99 % |

| TRP.PR.F | FloatingReset | 1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 12.95 Evaluated at bid price : 12.95 Bid-YTW : 4.51 % |

| BNS.PR.D | FloatingReset | 1.57 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.81 Bid-YTW : 6.13 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BAM.PF.H | FixedReset | 120,965 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 23.13 Evaluated at bid price : 24.95 Bid-YTW : 4.94 % |

| CU.PR.I | FixedReset | 100,754 | Scotia crossed blocks of 35,000 and 20,000, both at 24.96. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 23.12 Evaluated at bid price : 24.91 Bid-YTW : 4.43 % |

| TD.PF.D | FixedReset | 80,593 | RBC crossed 48,500 at 19.60. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 19.37 Evaluated at bid price : 19.37 Bid-YTW : 4.64 % |

| TRP.PR.D | FixedReset | 61,504 | Nesbitt crossed 27,200 at 16.05. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 15.82 Evaluated at bid price : 15.82 Bid-YTW : 5.28 % |

| RY.PR.P | Perpetual-Discount | 50,315 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 23.63 Evaluated at bid price : 23.95 Bid-YTW : 5.51 % |

| RY.PR.J | FixedReset | 43,403 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-08 Maturity Price : 19.29 Evaluated at bid price : 19.29 Bid-YTW : 4.66 % |

| There were 54 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TD.PR.T | FloatingReset | Quote: 20.86 – 21.68 Spot Rate : 0.8200 Average : 0.5423 YTW SCENARIO |

| CU.PR.C | FixedReset | Quote: 18.40 – 19.30 Spot Rate : 0.9000 Average : 0.6277 YTW SCENARIO |

| TD.PF.C | FixedReset | Quote: 17.85 – 18.50 Spot Rate : 0.6500 Average : 0.4686 YTW SCENARIO |

| TD.PF.F | Perpetual-Discount | Quote: 22.53 – 22.95 Spot Rate : 0.4200 Average : 0.2636 YTW SCENARIO |

| TRP.PR.A | FixedReset | Quote: 14.55 – 15.27 Spot Rate : 0.7200 Average : 0.5715 YTW SCENARIO |

| W.PR.H | Perpetual-Discount | Quote: 23.05 – 23.70 Spot Rate : 0.6500 Average : 0.5042 YTW SCENARIO |

“FixedResets losing 169bp”

Likely a surprise to anyone using ZPR as a FR market facsimile. It was UP 10bp today! On second look it turns out ZPR’s market price and NAV diverged significantly but even it was only down 76bp.

It’s silly season again in the USA , attacking the job and wealth creators is always in fashion. The last group of people to create efficiency in a market is the group who are the least efficient, those politicians who have created huge debt which is unsustainable at higher interest rates and reduced rates to create asset bubbles which will certainly pop . I won’t even mention that their donor base is Wall Street, I guess I just did! I am so thankful to live in Canada where reasonable is usually the watchword and where parties who have gone off the rails ( Alberta) are punished so badly that the extreme is voted in to swing the pendulum back and shake constituents back to reality the next time. The best thing we ever did was make the Senate a useless appendage that cannot block or pass anything that really matters.

To be honest, I can’t figure out why RY.PR.W is down 10.5%. Anyone know? All comments welcome.

Likely a surprise to anyone using ZPR as a FR market facsimile. It was UP 10bp today!

There are two major differences:

i) The universe used for my FixedReset index is investment-grade only, with only minor filtering due to volume

ii) My indices are calculated bid/bid, while ZPR and TXPL are close/close.

I can’t figure out why RY.PR.W is down 10.5%.

It seems to be trading a bit more like a PerpetualDiscount than a DeemedRetractible. Some participants may have forgotten it is exchangeable for shares at the issuer’s option.

Hi jiHymas, thanks for the quick and late night response. Why would RBC ever exchange the series W? It’s trading below redemption price and they would be forced to use $25 for the conversion. No?

Thanks again