The Fed is making sure that nobody takes them for granted:

Federal Reserve Chair Janet Yellen and New York Fed President William Dudley both said the central bank could boost interest rates as soon as next month.

“At this point, I see the U.S. economy as performing well,” Yellen said on Wednesday in testimony before the House Financial Services Committee in Washington. If economic data continue to point to growth and firmer prices, a December rate hike would be a “live possibility,” she said. Speaking in New York hours later, Dudley said he agreed with the chair, but “let’s see what the data shows.”

The Federal Open Market Committee said in its October statement that it will consider raising interest rates at its “next meeting,” citing “solid” rates of household spending and business investment. Yellen’s and Dudley’s comments reinforced the idea that next month is in the crosshairs for an increase, and placed the focus on upcoming employment and other economic data.

The market noticed:

Bonds are falling around the world as traders increased odds to more than 50 percent that the Federal Reserve will raise interest rates this year.

Benchmark 10-year Treasury yields climbed to a seven-week high of 2.24 percent on Wednesday after Fed Chair Janet Yellen said policy makers may move as soon as their December meeting. German yields reached a two-week high. Australian 10-year yields rose for a sixth day Thursday.

It was a strong day for the Canadian preferred share market, with PerpetualDiscounts up 52bp, FixedResets winning 77bp and DeemedRetractibles gaining 15bp. There are a lot of winners on the Performance Highlights table! Volume was well above average.

PerpetualDiscounts now yield 5.62%, equivalent to 7.31% interest at the standard equivalency factor of 1.3x. Long corporates now yield a little under 4.4%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 290bp, a very significant narrowing from the 310bp reported October 28.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

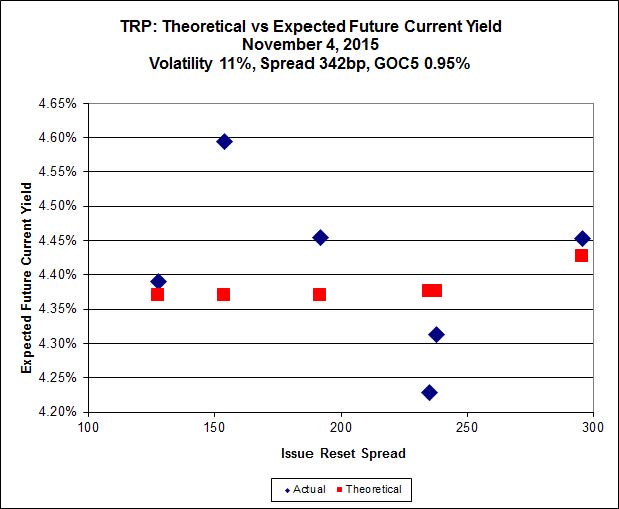

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 19.51 to be $0.65 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.69 cheap at its bid price of 13.55.

Click for Big

Most expensive is MFC.PR.N, resetting at +230bp on 2020-3-19, bid at 20.48 to be 0.75 rich, while MFC.PR.I resetting at +286bp on 2017-9-19, is bid at 21.41 to be 0.63 cheap.

Click for Big

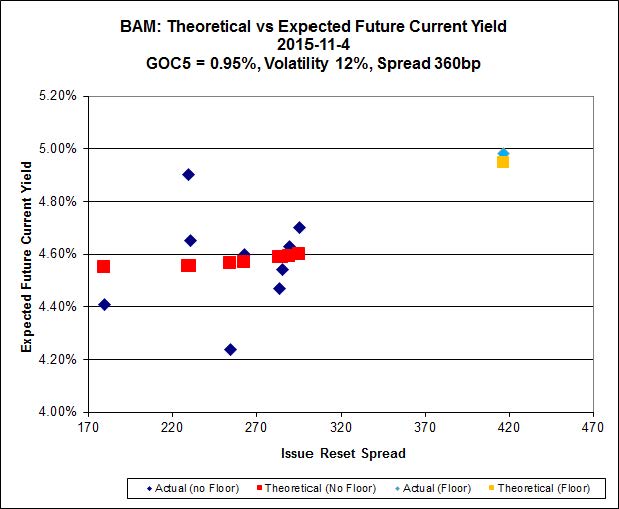

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.58 to be $1.26 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 20.65 and appears to be $1.48 rich.

Click for Big

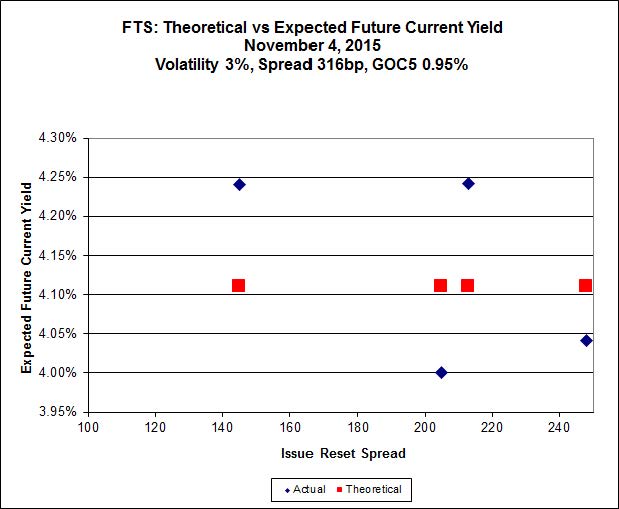

FTS.PR.K, with a spread of +205bp, and bid at 18.75, looks $0.50 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 18.15 and is $0.58 cheap.

Click for Big

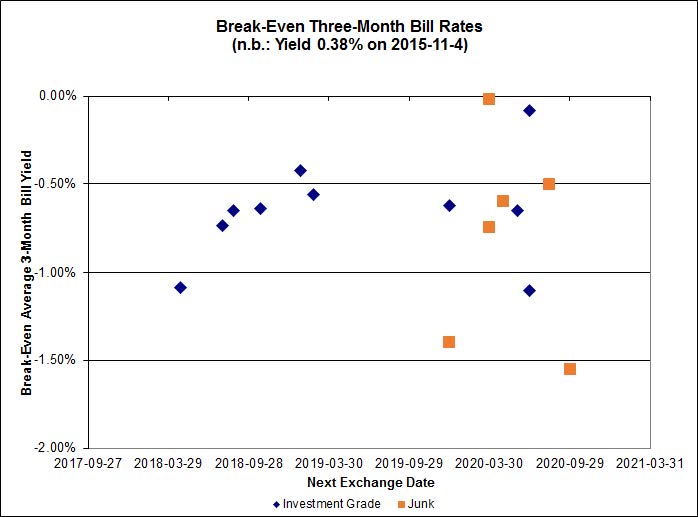

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.53%, with two outliers above 0.00% and none below -2.00%. There are three junk outliers above 0.00% and one below -2.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 4.40 % | 5.28 % | 31,280 | 17.50 | 1 | 0.3226 % | 1,768.0 |

| FixedFloater | 6.11 % | 5.35 % | 31,293 | 17.11 | 1 | 5.0676 % | 3,194.3 |

| Floater | 4.16 % | 4.21 % | 62,859 | 16.96 | 3 | 0.8593 % | 1,896.3 |

| OpRet | 4.83 % | 4.20 % | 33,402 | 0.80 | 1 | 0.1184 % | 2,722.9 |

| SplitShare | 4.76 % | 5.81 % | 155,377 | 4.39 | 5 | -0.1144 % | 3,191.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1144 % | 2,489.7 |

| Perpetual-Premium | 5.82 % | 1.33 % | 81,667 | 0.08 | 6 | 0.1859 % | 2,495.6 |

| Perpetual-Discount | 5.53 % | 5.62 % | 81,348 | 14.44 | 33 | 0.5173 % | 2,586.8 |

| FixedReset | 4.93 % | 4.44 % | 211,682 | 15.52 | 76 | 0.7749 % | 2,074.1 |

| Deemed-Retractible | 5.18 % | 5.20 % | 111,220 | 5.43 | 34 | 0.1496 % | 2,578.5 |

| FloatingReset | 2.56 % | 3.76 % | 56,694 | 5.81 | 10 | 0.3895 % | 2,184.8 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| CU.PR.H | Perpetual-Discount | -1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 23.20 Evaluated at bid price : 23.50 Bid-YTW : 5.58 % |

| VNR.PR.A | FixedReset | -1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 20.35 Evaluated at bid price : 20.35 Bid-YTW : 4.68 % |

| TRP.PR.B | FixedReset | -1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 12.70 Evaluated at bid price : 12.70 Bid-YTW : 4.33 % |

| W.PR.H | Perpetual-Discount | 1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 23.99 Evaluated at bid price : 24.24 Bid-YTW : 5.72 % |

| IFC.PR.A | FixedReset | 1.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.16 Bid-YTW : 8.91 % |

| BAM.PR.M | Perpetual-Discount | 1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 21.07 Evaluated at bid price : 21.07 Bid-YTW : 5.71 % |

| BMO.PR.S | FixedReset | 1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 19.31 Evaluated at bid price : 19.31 Bid-YTW : 4.37 % |

| SLF.PR.H | FixedReset | 1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.75 Bid-YTW : 7.68 % |

| TD.PR.Z | FloatingReset | 1.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.81 Bid-YTW : 3.59 % |

| BAM.PR.B | Floater | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 11.40 Evaluated at bid price : 11.40 Bid-YTW : 4.18 % |

| CU.PR.D | Perpetual-Discount | 1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 22.24 Evaluated at bid price : 22.59 Bid-YTW : 5.41 % |

| BAM.PF.D | Perpetual-Discount | 1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 21.28 Evaluated at bid price : 21.56 Bid-YTW : 5.74 % |

| RY.PR.J | FixedReset | 1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 21.20 Evaluated at bid price : 21.20 Bid-YTW : 4.29 % |

| CU.PR.G | Perpetual-Discount | 1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 5.37 % |

| BMO.PR.Z | Perpetual-Discount | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 23.76 Evaluated at bid price : 24.10 Bid-YTW : 5.18 % |

| BMO.PR.Q | FixedReset | 1.31 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.82 Bid-YTW : 5.46 % |

| BAM.PF.B | FixedReset | 1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 19.46 Evaluated at bid price : 19.46 Bid-YTW : 4.77 % |

| MFC.PR.B | Deemed-Retractible | 1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.55 Bid-YTW : 6.81 % |

| NA.PR.S | FixedReset | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 19.82 Evaluated at bid price : 19.82 Bid-YTW : 4.36 % |

| TRP.PR.H | FloatingReset | 1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 11.77 Evaluated at bid price : 11.77 Bid-YTW : 3.58 % |

| TRP.PR.D | FixedReset | 1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 19.30 Evaluated at bid price : 19.30 Bid-YTW : 4.44 % |

| TRP.PR.F | FloatingReset | 1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 14.42 Evaluated at bid price : 14.42 Bid-YTW : 4.04 % |

| IAG.PR.G | FixedReset | 1.64 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.75 Bid-YTW : 5.78 % |

| BAM.PR.R | FixedReset | 1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 16.58 Evaluated at bid price : 16.58 Bid-YTW : 5.00 % |

| FTS.PR.M | FixedReset | 1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 21.22 Evaluated at bid price : 21.22 Bid-YTW : 4.23 % |

| CM.PR.Q | FixedReset | 1.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 21.43 Evaluated at bid price : 21.70 Bid-YTW : 4.23 % |

| GWO.PR.N | FixedReset | 1.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.95 Bid-YTW : 9.67 % |

| TRP.PR.E | FixedReset | 1.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 19.51 Evaluated at bid price : 19.51 Bid-YTW : 4.46 % |

| MFC.PR.M | FixedReset | 2.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.55 Bid-YTW : 6.24 % |

| TD.PF.D | FixedReset | 2.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 21.54 Evaluated at bid price : 21.85 Bid-YTW : 4.20 % |

| W.PR.J | Perpetual-Discount | 2.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 24.19 Evaluated at bid price : 24.45 Bid-YTW : 5.77 % |

| MFC.PR.G | FixedReset | 2.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.87 Bid-YTW : 5.75 % |

| NA.PR.W | FixedReset | 2.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 19.35 Evaluated at bid price : 19.35 Bid-YTW : 4.30 % |

| TRP.PR.A | FixedReset | 2.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 16.11 Evaluated at bid price : 16.11 Bid-YTW : 4.59 % |

| PWF.PR.P | FixedReset | 2.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 14.07 Evaluated at bid price : 14.07 Bid-YTW : 4.47 % |

| MFC.PR.F | FixedReset | 2.51 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.71 Bid-YTW : 9.28 % |

| MFC.PR.J | FixedReset | 2.61 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.81 Bid-YTW : 6.16 % |

| TRP.PR.C | FixedReset | 2.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 13.55 Evaluated at bid price : 13.55 Bid-YTW : 4.53 % |

| HSE.PR.A | FixedReset | 3.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 13.94 Evaluated at bid price : 13.94 Bid-YTW : 4.88 % |

| MFC.PR.H | FixedReset | 3.32 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.06 Bid-YTW : 5.30 % |

| BAM.PR.X | FixedReset | 3.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 15.59 Evaluated at bid price : 15.59 Bid-YTW : 4.66 % |

| BAM.PR.G | FixedFloater | 5.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 25.00 Evaluated at bid price : 15.55 Bid-YTW : 5.35 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| MFC.PR.M | FixedReset | 96,860 | Scotia crossed 28,000 at 20.40; RBC crossed 39,700 at the same price. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.55 Bid-YTW : 6.24 % |

| BAM.PR.B | Floater | 56,793 | TD crossed 32,300 at 11.40. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 11.40 Evaluated at bid price : 11.40 Bid-YTW : 4.18 % |

| CM.PR.Q | FixedReset | 51,617 | Scotia crossed 42,500 at 21.60. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 21.43 Evaluated at bid price : 21.70 Bid-YTW : 4.23 % |

| PVS.PR.E | SplitShare | 48,600 | Recent new issue. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-10-31 Maturity Price : 25.00 Evaluated at bid price : 24.37 Bid-YTW : 5.99 % |

| BMO.PR.S | FixedReset | 47,305 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 19.31 Evaluated at bid price : 19.31 Bid-YTW : 4.37 % |

| TRP.PR.E | FixedReset | 46,885 | Scotia crossed 30,000 at 19.31. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-04 Maturity Price : 19.51 Evaluated at bid price : 19.51 Bid-YTW : 4.46 % |

| There were 46 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TRP.PR.B | FixedReset | Quote: 12.70 – 13.50 Spot Rate : 0.8000 Average : 0.5240 YTW SCENARIO |

| VNR.PR.A | FixedReset | Quote: 20.35 – 21.05 Spot Rate : 0.7000 Average : 0.4684 YTW SCENARIO |

| TD.PF.A | FixedReset | Quote: 19.52 – 19.99 Spot Rate : 0.4700 Average : 0.3230 YTW SCENARIO |

| NA.PR.Q | FixedReset | Quote: 24.76 – 25.09 Spot Rate : 0.3300 Average : 0.2074 YTW SCENARIO |

| RY.PR.N | Perpetual-Discount | Quote: 23.50 – 23.78 Spot Rate : 0.2800 Average : 0.1971 YTW SCENARIO |

| TD.PR.Y | FixedReset | Quote: 24.01 – 24.50 Spot Rate : 0.4900 Average : 0.4123 YTW SCENARIO |