Today’s news was the FOMC release:

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that the current 0 to 1/4 percent target range for the federal funds rate remains appropriate. In determining whether it will be appropriate to raise the target range at its next meeting, the Committee will assess progress–both realized and expected–toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. The Committee anticipates that it will be appropriate to raise the target range for the federal funds rate when it has seen some further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term.

…

Voting against the action was Jeffrey M. Lacker, who preferred to raise the target range for the federal funds rate by 25 basis points at this meeting.

Jeanna Smialek of Bloomberg notes:

The Fed removed a line from September’s statement saying that global economic and financial developments “may restrain economic activity somewhat,” saying Wednesday only that the central bank is monitoring the international situation. The committee also added a reference to the possibility of increasing the rate “at its next meeting” based on “realized and expected” progress in reaching goals.

“The Fed is clearly signaling that the default plan is to raise rates in December,” said Dean Maki, chief economist at Point72 Asset Management in Stamford, Connecticut. “It signals that something needs to prevent them from hiking in December rather than that something needs to happen for them to raise.”

And clearly, a lot of players agreed with that analysis … at least, for today:

Traders see a 46 percent chance that the central bank will raise its benchmark rate from near zero at its next meeting, according to data compiled by Bloomberg. That’s up from 37 percent before policy makers said Wednesday that they kept the target unchanged and planned to assess whether to lift it in December. The calculation assumes the effective fed funds rate averages 0.375 percent after the first hike.

Deutsche Bank has provided a lesson to all bank dividend worshippers:

Deutsche Bank AG said it plans to suspend dividends for two years as co-Chief Executive Officer John Cryan seeks to improve capital levels and returns by cutting costs.

The bank, which has paid a dividend since Germany’s postwar reconstruction, plans to recommend resuming payouts from fiscal year 2017, Deutsche Bank said in a statement from Frankfurt on Wednesday. The bank wants to lift its common equity Tier 1 ratio, a key measure of financial strength, to at least 12.5 percent by the end of 2018.

The Canadian Securities Administrators have released a report by Prof. Douglas Cumming titled A Dissection of Mutual Fund Fees, Flows, and Performance which has attracted the usual outrage from the usual suspects:

The report, coupled with the regulatory changes outlined in CRM2, is expected to put additional pressure on advisers to consider switching from a commission-based business model to fee-based practices.

Currently, 32 per cent of advisers say investors question their fees, according to research by Accenture. With the investment landscape starting to shift, the number of advisers moving to a fee-based platform will start to rise, says Kendra Thompson, Accenture’s North America lead for Wealth and Asset Management Services.

Sadly, what has not yet been investigated is whether investment outcomes on an investor basis are better or worse with a direct payment model; that’s the crucial part. Joe Lunchbucket will not pay his advisor to do nothing; therefore, he will have to go to a robo-advisor if he wants any advice at all, which he doesn’t (he’ll just buy a GIC). And, says the report:

Funds that sell more through affiliated dealers tend to perform worse.

Regression analyses comparing across funds and over the sample period indicate that funds which receive higher levels of affiliated dealer flows experience lower future alpha on average. Funds that were in the top quartile in terms of receiving affiliated dealer flows on average experienced a reduction in future monthly alpha by 0.2% relative to those funds that did not receive any affiliated dealer flows. The regression analyses indicate similar findings for stand-alone funds that can be purchased directly, and for fund-of-funds that can and cannot be purchased directly, but there were some differences in these effects at different points in time.

And why should advisors be competent anyway? This is Canada. Competence doesn’t matter:

The Quebec government and its giant pension fund are coming to the rescue of Bombardier Inc. with a significant investment in its C Series airliner program, a move designed to soothe investor fears over the plane maker’s cash situation and get the jet to market.

Quebec’s Liberal government and the Caisse de dépôt et placement du Québec will together commit more than $1-billion to Bombardier in an announcement expected Thursday morning ahead of the company’s latest earnings report, said one person with knowledge of the situation. The exact amount remained unclear. “You can’t move the needle with less than that,” the person said.

We can all sleep sounder in our beds knowing that anti-terrorism laws are having their intended effect:

J. Dennis Hastert, the former speaker of the House, pleaded guilty on Wednesday to trying to evade federal banking laws, telling a district judge here that he had known what he was doing was wrong.

The plea brought a quick, quiet finish to a proceeding that had startled many in Washington who once knew Mr. Hastert as one of the nation’s most powerful leaders, and in Yorkville, Ill., his rural hometown, who remembered Mr. Hastert as their winning high school wrestling coach.

Prosecutors said they believed that federal guidelines called for a sentence of up to six months in prison. But the judge, Thomas M. Durkin of Federal District Court, indicated that he would not decide on Mr. Hastert’s punishment before reading a presentencing report. Sentencing was scheduled for Feb. 29.

Mr. Hastert told the judge why he had structured bank withdrawals in an attempt to avoid detection. “I didn’t want them to know how I would spend the money,” he said. Asked whether he understood at the time that his conduct was wrong, he said yes.

Well, OK, Hastert may not exactly be a terrorist. Not technically, if you want to get pedantic about it, like some of those effete elites. But being a blackmail victim is pretty close to being a terrorist, right? Indistinguishable for all practical, real-world, common-sense purposes. It just shows the need for more intrusive laws and a larger budget for our wise masters in the security forces.

And here’s a great story to finish off – drones ‘n’ guns:

A judge on Monday decided that William Merideth, the Kentucky, US, man who got busted for shooting down a drone that had been flying over his property, had a right to take that thing out.

The hearing, in Bullitt County, lasted just over 2 hours.

The incident happened in July.

Merideth’s sunbathing daughters had come in from the back garden to tell their father about a drone flying overhead.

After police arrested Merideth for taking the drone out with his shotgun and three blasts of Number 8 birdshot, he claimed that the drone’s operator, neighbor David Boggs, was violating his privacy by hovering his drone over Merideth’s property and spying on his family.

Police in the town of Hillview arrested Merideth and charged him with wanton endangerment and criminal mischief for firing his gun within city limits.

It was another mixed day for the Canadian preferred share market, with PerpetualDiscounts up 34bp, FixedResets off 13bp and DeemedRetractibles gaining 14bp. The Performance Highlights table is its usual enormous self. Volume was well above average.

PerpetualDiscounts now yield 5.71%, equivalent to 7.42% interest at the standard equivalency factor of 7.42%. Long corporates now yield about 4.3%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 310bp, a significant narrowing from the 320bp reported October 21.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

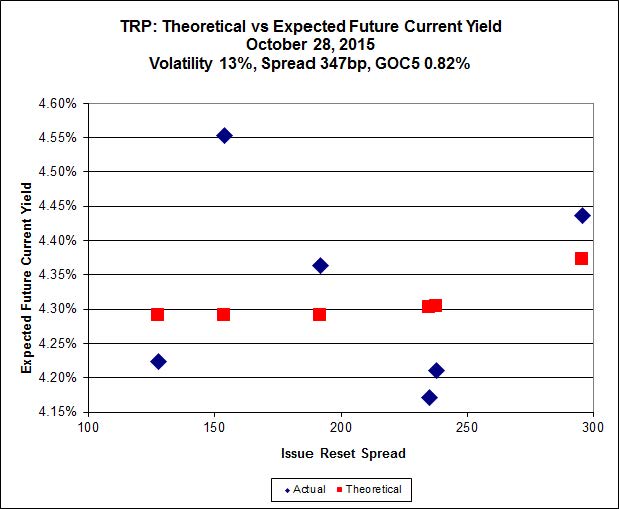

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 19.00 to be $0.58 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.79 cheap at its bid price of 12.96.

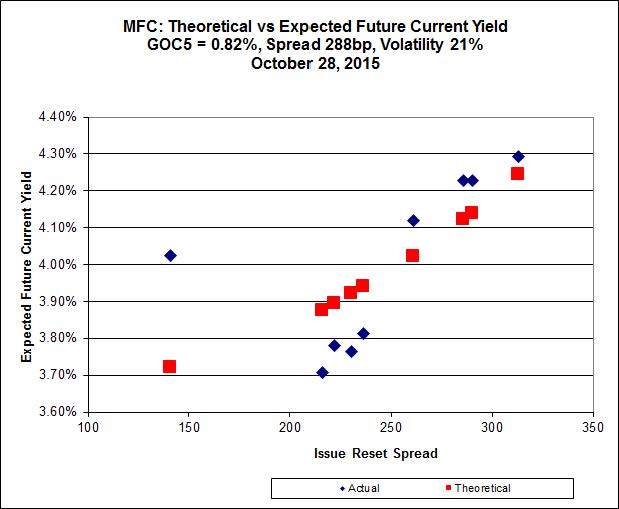

Click for Big

Most expensive is MFC.PR.L, resetting at +216bp on 2019-6-19, bid at 20.09 to be 0.87 rich, while MFC.PR.F resetting at +141bp on 2016-6-19, is bid at 13.85 to be 1.13 cheap.

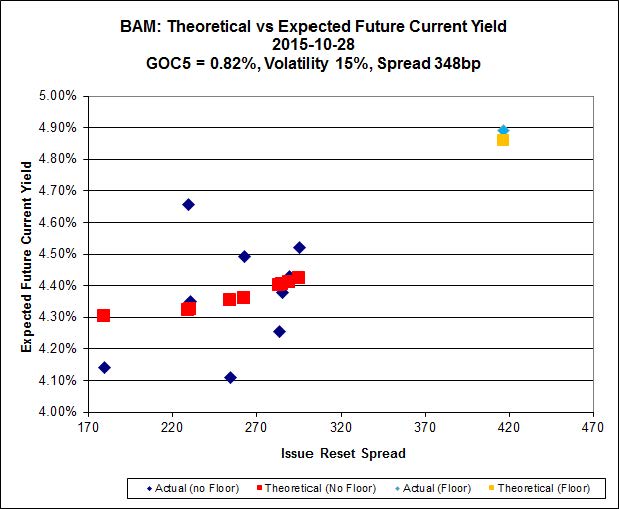

Click for Big

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.75 to be $1.30 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 20.50 and appears to be $1.14 rich.

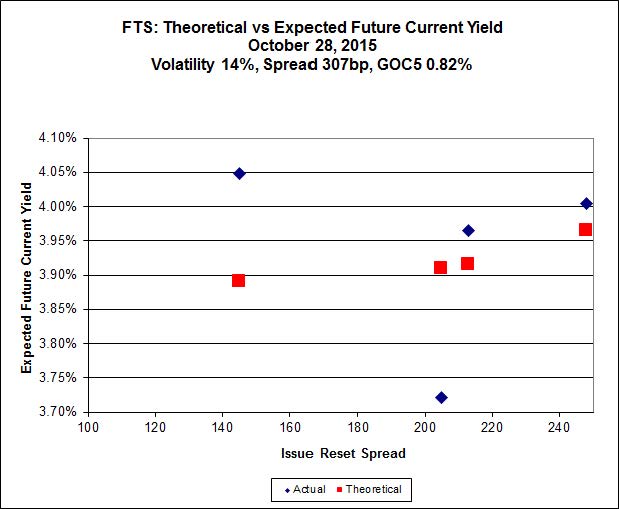

Click for Big

FTS.PR.K, with a spread of +205bp, and bid at 19.28, looks $0.93 expensive and resets 2019-3-1. FTS.PR.H, with a spread of +145bp and resetting 2020-6-1, is bid at 14.02 and is $0.57 cheap.

Click for Big

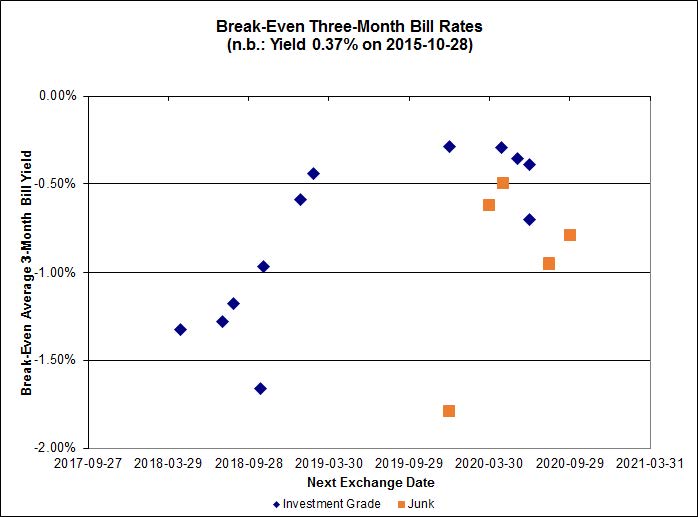

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.79%, with no outliers. The distribution is bimodal, with bank NVCC non-compliant pairs averaging -0.97% and other issues averaging -0.43%. There are four junk outliers above 0.00% and one below -2.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2987 % | 1,759.7 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2987 % | 3,076.8 |

| Floater | 4.22 % | 4.25 % | 60,723 | 16.89 | 3 | 0.2987 % | 1,870.7 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1386 % | 2,747.5 |

| SplitShare | 4.37 % | 5.53 % | 83,552 | 2.94 | 5 | 0.1386 % | 3,219.9 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1386 % | 2,512.3 |

| Perpetual-Premium | 5.85 % | 5.78 % | 69,169 | 2.74 | 5 | -0.0080 % | 2,488.0 |

| Perpetual-Discount | 5.59 % | 5.71 % | 79,179 | 14.32 | 33 | 0.3419 % | 2,553.5 |

| FixedReset | 4.91 % | 4.40 % | 215,443 | 15.94 | 76 | -0.1263 % | 2,080.0 |

| Deemed-Retractible | 5.20 % | 5.19 % | 112,648 | 5.45 | 33 | 0.1378 % | 2,567.3 |

| FloatingReset | 2.47 % | 3.74 % | 60,904 | 5.82 | 9 | -0.0816 % | 2,172.4 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.C | FixedReset | -3.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 12.96 Evaluated at bid price : 12.96 Bid-YTW : 4.55 % |

| PWF.PR.T | FixedReset | -3.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 20.85 Evaluated at bid price : 20.85 Bid-YTW : 4.02 % |

| TRP.PR.B | FixedReset | -2.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 12.43 Evaluated at bid price : 12.43 Bid-YTW : 4.26 % |

| BAM.PF.B | FixedReset | -2.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 19.20 Evaluated at bid price : 19.20 Bid-YTW : 4.72 % |

| GWO.PR.N | FixedReset | -2.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.81 Bid-YTW : 9.64 % |

| BAM.PR.Z | FixedReset | -2.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 20.91 Evaluated at bid price : 20.91 Bid-YTW : 4.71 % |

| HSE.PR.E | FixedReset | -2.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 22.40 Evaluated at bid price : 23.16 Bid-YTW : 4.75 % |

| BAM.PF.E | FixedReset | -1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 20.50 Evaluated at bid price : 20.50 Bid-YTW : 4.45 % |

| FTS.PR.H | FixedReset | -1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 14.02 Evaluated at bid price : 14.02 Bid-YTW : 4.18 % |

| FTS.PR.G | FixedReset | -1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 18.60 Evaluated at bid price : 18.60 Bid-YTW : 4.19 % |

| BAM.PR.R | FixedReset | -1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 16.75 Evaluated at bid price : 16.75 Bid-YTW : 4.79 % |

| FTS.PR.M | FixedReset | -1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 20.60 Evaluated at bid price : 20.60 Bid-YTW : 4.26 % |

| MFC.PR.F | FixedReset | -1.42 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.85 Bid-YTW : 9.93 % |

| BAM.PF.A | FixedReset | -1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 4.60 % |

| BMO.PR.M | FixedReset | -1.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.54 Bid-YTW : 3.33 % |

| FTS.PR.K | FixedReset | -1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 19.28 Evaluated at bid price : 19.28 Bid-YTW : 4.01 % |

| MFC.PR.J | FixedReset | 1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.81 Bid-YTW : 6.06 % |

| NA.PR.W | FixedReset | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 19.27 Evaluated at bid price : 19.27 Bid-YTW : 4.21 % |

| BNS.PR.O | Deemed-Retractible | 1.10 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2015-11-27 Maturity Price : 25.50 Evaluated at bid price : 25.73 Bid-YTW : -5.91 % |

| MFC.PR.L | FixedReset | 1.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.09 Bid-YTW : 6.29 % |

| GWO.PR.R | Deemed-Retractible | 1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.10 Bid-YTW : 6.59 % |

| SLF.PR.H | FixedReset | 1.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.45 Bid-YTW : 7.78 % |

| SLF.PR.A | Deemed-Retractible | 1.34 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.92 Bid-YTW : 6.64 % |

| MFC.PR.M | FixedReset | 1.46 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.85 Bid-YTW : 5.97 % |

| W.PR.H | Perpetual-Discount | 1.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 23.69 Evaluated at bid price : 23.96 Bid-YTW : 5.78 % |

| TRP.PR.D | FixedReset | 1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 4.41 % |

| BMO.PR.W | FixedReset | 2.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 19.30 Evaluated at bid price : 19.30 Bid-YTW : 4.20 % |

| CM.PR.O | FixedReset | 2.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 19.52 Evaluated at bid price : 19.52 Bid-YTW : 4.22 % |

| BAM.PR.X | FixedReset | 2.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 15.82 Evaluated at bid price : 15.82 Bid-YTW : 4.43 % |

| MFC.PR.K | FixedReset | 3.24 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.10 Bid-YTW : 6.19 % |

| W.PR.J | Perpetual-Discount | 3.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 24.22 Evaluated at bid price : 24.48 Bid-YTW : 5.76 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| IFC.PR.A | FixedReset | 261,020 | Desjardins crossed blocks of 151,800 shares, 81,500 and 23,200, all at 16.33. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.16 Bid-YTW : 8.80 % |

| NA.PR.S | FixedReset | 236,830 | Nesbitt crossed 148,100 at 19.90 and 80,000 at 20.00. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 20.00 Evaluated at bid price : 20.00 Bid-YTW : 4.21 % |

| RY.PR.Z | FixedReset | 160,125 | Scotia crossed 50,000 at 19.72. Nesbitt crossed 75,000 at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 19.65 Evaluated at bid price : 19.65 Bid-YTW : 4.06 % |

| TRP.PR.D | FixedReset | 103,595 | Scotia crossed 80,000 at 18.80. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 4.41 % |

| TRP.PR.E | FixedReset | 92,740 | Scotia crossed 80,000 at 19.00. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 4.47 % |

| BMO.PR.S | FixedReset | 64,701 | Scotia crossed 50,000 at 19.80. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-28 Maturity Price : 19.80 Evaluated at bid price : 19.80 Bid-YTW : 4.23 % |

| There were 43 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.M | FixedReset | Quote: 20.85 – 21.73 Spot Rate : 0.8800 Average : 0.5792 YTW SCENARIO |

| HSE.PR.E | FixedReset | Quote: 23.16 – 23.70 Spot Rate : 0.5400 Average : 0.3735 YTW SCENARIO |

| ELF.PR.H | Perpetual-Discount | Quote: 23.85 – 24.25 Spot Rate : 0.4000 Average : 0.2552 YTW SCENARIO |

| TRP.PR.C | FixedReset | Quote: 12.96 – 13.40 Spot Rate : 0.4400 Average : 0.3107 YTW SCENARIO |

| BAM.PR.Z | FixedReset | Quote: 20.91 – 21.35 Spot Rate : 0.4400 Average : 0.3134 YTW SCENARIO |

| CU.PR.G | Perpetual-Discount | Quote: 20.50 – 21.00 Spot Rate : 0.5000 Average : 0.3737 YTW SCENARIO |