SNC-Lavalin thinks it would be helpful if we had a no-fault justice system with no judiciary:

SNC-Lavalin Group Inc. is pressing Canada’s new Liberal government to adopt corporate corruption settlement deals like those in place in the United Kingdom and the United States, saying federal charges laid against the company are hurting its ability to compete against rivals in Group of 7 countries.

…

SNC is expending significant effort explaining its situation and Canada’s legal system to potential clients, Mr. Bruce added in an interview with The Globe and Mail. He said although those conversations are getting easier over time, ongoing reputational issues continue to affect the company’s ability to bid for work.“Effectively, we are locked in the court system,” he said, “[It’s] by trial until you’re either found guilty or not guilty.”

…

Differing interests are at play. SNC wants to resolve the matter without admitting guilt, which could damage its ability to bid for contracts internationally and at home. Ottawa has been trying to get tougher on companies involved in corruption after being rebuked for years on the international stage for its perceived failure to take the matter seriously.Prosecutors in February laid rare corruption and fraud charges against Montreal-based SNC, Canada’s largest engineering firm, related to its business in Libya.

Well, I don’t know why we’re so eager to save Libyans from corruption (Libya is still a foreign country, as far as I know), but that’s a part of law that is currently beside the point. It appears that Mr. Bruce would rather have nice quiet chats with federal bureaucrats regarding allegations of wrongdoing and pay a license fee administrative penalty in lieu of court-ordered fines. He also thinks it would be pleasant to avoid admitting wrongdoing, which will make it much harder for aggrieved third parties to go to what is quaintly known as ‘public court’ to seek redress.

I have no doubt that the law can be improved – and certainly the complete destruction of a company due to relatively limited wrongdoing by a tiny part of it seems disproportionate – but the holus-bolus replacement of the judiciary by well connected political operatives does not sound like much of an improvement to me.

Allister Heath of The Telegraph has some well expressed views on economics:

Seeking to predict the unpredictable has certainly kept a lot of people employed in the City of London, and for good reason: there is an immense and unquenchable appetite for their services. Being proved wrong time and again doesn’t really matter: what counts is the plausibility of the forecast and of the way in which it is delivered. In extremis, economics becomes a branch of showbusiness: entertainment and therapy dressed up as science.

We all want to know what exactly will happen to the economy, interest rates and inflation over the next few years; but economies are complex, non-linear systems that cannot meaningfully be predicted by inputting a few variables into a computer. They are just too random for that – and in any case, the data and statistics at our disposal are too imprecise and subject to endless, drastic revisions. We don’t really know what is happening to the economy today, so how can we possibly know with any degree of precision what will happen in three years’ time? The best we can do is what Nobel prize-winning economist F.A. Hayek called “pattern predictions” and scenario-based forecasts; attempts at spurious accuracy are scientistic rather than scientific, he argued.

It was a mixed, mostly negative day for the Canadian preferred share market, with PerpetualDiscounts off 22bp, FixedResets down 40bp and DeemedRetractibles gaining 15bp. The Performance Highlights table is ridiculously long, as has been the case all year, with a notable preponderance of losers. Volume was slightly below average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 19.88 to be $0.76 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.76 cheap at its bid price of 14.06.

Click for Big

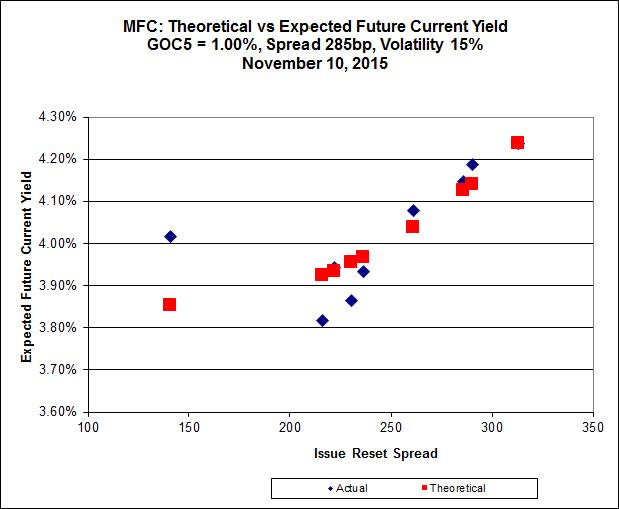

Most expensive is MFC.PR.L, resetting at +216bp on 2019-6-19, bid at 20.70 to be 0.56 rich, while MFC.PR.F resetting at +141bp on 2016-6-19, is bid at 15.00 to be 0.64 cheap.

Click for Big

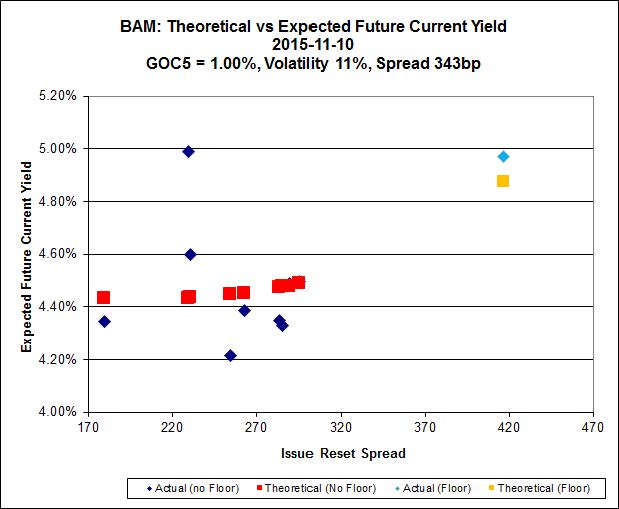

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.54 to be $2.07 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 21.06 and appears to be $1.09 rich.

Click for Big

FTS.PR.K, with a spread of +205bp, and bid at 20.13, looks $0.93 expensive and resets 2019-3-1. FTS.PR.H, with a spread of +145bp and resetting 2020-6-1, is bid at 14.70 and is $0.73 cheap.

Click for Big

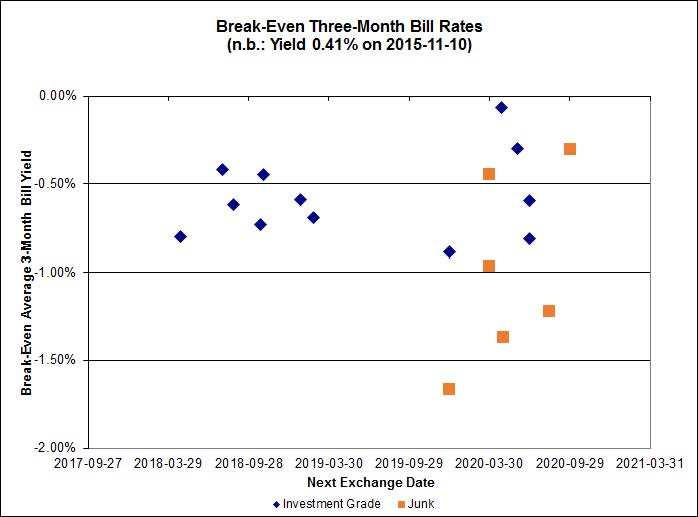

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.58%, with no outliers. There are two junk outliers above 0.00% and two below -2.00%.

Click for Big

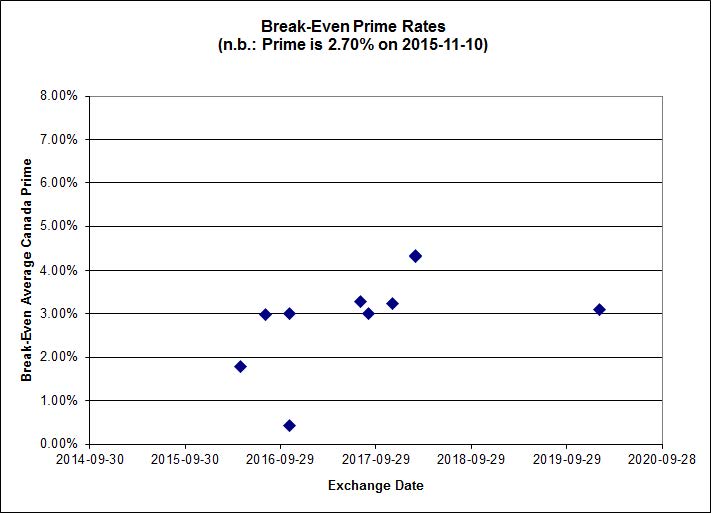

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 4.38 % | 5.26 % | 29,300 | 17.51 | 1 | -2.4375 % | 1,774.8 |

| FixedFloater | 5.80 % | 5.04 % | 30,124 | 17.48 | 1 | 2.4375 % | 3,366.9 |

| Floater | 3.85 % | 3.87 % | 62,651 | 17.66 | 3 | 3.2828 % | 2,050.6 |

| OpRet | 4.85 % | 4.70 % | 34,609 | 0.78 | 1 | 0.0792 % | 2,714.3 |

| SplitShare | 4.75 % | 5.61 % | 152,298 | 4.38 | 5 | 0.0901 % | 3,200.3 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0901 % | 2,497.0 |

| Perpetual-Premium | 5.81 % | -1.33 % | 90,302 | 0.08 | 6 | 0.2584 % | 2,502.4 |

| Perpetual-Discount | 5.52 % | 5.61 % | 82,634 | 14.47 | 33 | -0.2220 % | 2,592.8 |

| FixedReset | 4.77 % | 4.51 % | 220,525 | 15.59 | 76 | -0.4037 % | 2,144.1 |

| Deemed-Retractible | 5.16 % | 5.20 % | 108,816 | 5.42 | 34 | 0.1478 % | 2,588.7 |

| FloatingReset | 2.55 % | 3.78 % | 54,678 | 5.79 | 10 | -0.3886 % | 2,201.9 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.R | FixedReset | -2.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 16.54 Evaluated at bid price : 16.54 Bid-YTW : 5.23 % |

| SLF.PR.G | FixedReset | -2.52 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.45 Bid-YTW : 8.46 % |

| GWO.PR.N | FixedReset | -2.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.00 Bid-YTW : 9.84 % |

| BAM.PR.E | Ratchet | -2.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 25.00 Evaluated at bid price : 15.61 Bid-YTW : 5.26 % |

| HSE.PR.A | FixedReset | -2.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 14.77 Evaluated at bid price : 14.77 Bid-YTW : 4.84 % |

| FTS.PR.H | FixedReset | -2.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 14.70 Evaluated at bid price : 14.70 Bid-YTW : 4.31 % |

| PWF.PR.P | FixedReset | -2.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 14.65 Evaluated at bid price : 14.65 Bid-YTW : 4.54 % |

| TD.PF.C | FixedReset | -1.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 19.92 Evaluated at bid price : 19.92 Bid-YTW : 4.28 % |

| SLF.PR.H | FixedReset | -1.84 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.66 Bid-YTW : 7.18 % |

| BNS.PR.Y | FixedReset | -1.73 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.45 Bid-YTW : 5.37 % |

| BAM.PF.G | FixedReset | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 21.71 Evaluated at bid price : 22.08 Bid-YTW : 4.60 % |

| CU.PR.F | Perpetual-Discount | -1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 20.71 Evaluated at bid price : 20.71 Bid-YTW : 5.45 % |

| MFC.PR.K | FixedReset | -1.59 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.42 Bid-YTW : 6.19 % |

| NA.PR.W | FixedReset | -1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 20.06 Evaluated at bid price : 20.06 Bid-YTW : 4.29 % |

| BNS.PR.Z | FixedReset | -1.42 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.80 Bid-YTW : 5.77 % |

| BAM.PR.Z | FixedReset | -1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 21.61 Evaluated at bid price : 22.02 Bid-YTW : 4.69 % |

| BIP.PR.A | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 21.96 Evaluated at bid price : 22.45 Bid-YTW : 5.13 % |

| IFC.PR.A | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.50 Bid-YTW : 8.77 % |

| TD.PF.D | FixedReset | -1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 22.00 Evaluated at bid price : 22.51 Bid-YTW : 4.18 % |

| BAM.PR.T | FixedReset | -1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 4.86 % |

| CM.PR.O | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 20.18 Evaluated at bid price : 20.18 Bid-YTW : 4.33 % |

| BMO.PR.R | FloatingReset | -1.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.00 Bid-YTW : 3.43 % |

| BAM.PF.A | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 21.40 Evaluated at bid price : 21.73 Bid-YTW : 4.67 % |

| BNS.PR.D | FloatingReset | -1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.55 Bid-YTW : 5.56 % |

| BMO.PR.M | FixedReset | -1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.50 Bid-YTW : 3.36 % |

| GWO.PR.G | Deemed-Retractible | 1.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.78 Bid-YTW : 6.02 % |

| PWF.PR.T | FixedReset | 1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 21.96 Evaluated at bid price : 22.31 Bid-YTW : 3.96 % |

| BNS.PR.R | FixedReset | 1.49 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.55 Bid-YTW : 3.77 % |

| TD.PF.E | FixedReset | 1.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 22.54 Evaluated at bid price : 23.50 Bid-YTW : 4.06 % |

| BAM.PR.G | FixedFloater | 2.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 25.00 Evaluated at bid price : 16.39 Bid-YTW : 5.04 % |

| BAM.PR.C | Floater | 2.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 12.08 Evaluated at bid price : 12.08 Bid-YTW : 3.95 % |

| BAM.PR.B | Floater | 3.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 12.42 Evaluated at bid price : 12.42 Bid-YTW : 3.84 % |

| BAM.PR.K | Floater | 3.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 12.31 Evaluated at bid price : 12.31 Bid-YTW : 3.87 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BMO.PR.Q | FixedReset | 59,221 | RBC crossed 50,000 at 21.15. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.08 Bid-YTW : 5.39 % |

| BAM.PF.B | FixedReset | 36,725 | RBC crossed 20,000 at 20.72. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 20.70 Evaluated at bid price : 20.70 Bid-YTW : 4.62 % |

| SLF.PR.I | FixedReset | 32,392 | TD crossed 25,500 at 22.25. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.27 Bid-YTW : 5.46 % |

| RY.PR.H | FixedReset | 28,927 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 20.21 Evaluated at bid price : 20.21 Bid-YTW : 4.24 % |

| CM.PR.P | FixedReset | 27,250 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 19.65 Evaluated at bid price : 19.65 Bid-YTW : 4.34 % |

| TRP.PR.D | FixedReset | 25,496 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-10 Maturity Price : 19.30 Evaluated at bid price : 19.30 Bid-YTW : 4.60 % |

| There were 28 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PR.E | Ratchet | Quote: 15.61 – 16.75 Spot Rate : 1.1400 Average : 0.7178 YTW SCENARIO |

| TRP.PR.H | FloatingReset | Quote: 11.90 – 13.00 Spot Rate : 1.1000 Average : 0.6943 YTW SCENARIO |

| TRP.PR.G | FixedReset | Quote: 21.43 – 22.25 Spot Rate : 0.8200 Average : 0.5642 YTW SCENARIO |

| FTS.PR.G | FixedReset | Quote: 19.50 – 20.09 Spot Rate : 0.5900 Average : 0.3725 YTW SCENARIO |

| SLF.PR.G | FixedReset | Quote: 15.45 – 15.95 Spot Rate : 0.5000 Average : 0.3313 YTW SCENARIO |

| RY.PR.W | Perpetual-Discount | Quote: 23.30 – 23.78 Spot Rate : 0.4800 Average : 0.3209 YTW SCENARIO |