Nothing much happened today in the financial world, although what with the solstice and all, a few preferred share new issue salesmen may have been sacrificed by their clients.

In the real world, though there was marvellous news regarding private space ventures:

Elon Musk’s SpaceX showcased his dream of reusable spacecraft by making a Falcon 9 booster the first piece of an orbital rocket to land back on Earth, minutes after lofting satellites toward orbit.

Space Exploration Technologies Corp. pulled off the soft, vertical touchdown after the two-stage rocket propelled its payload of 11 Orbcomm Inc. satellites aloft. It was the company’s first flight since a fiery blast destroyed a Falcon 9 rocket in June, minutes after lift off.

“Welcome back, baby!” Musk wrote in a Twitter post on his way to the landing zone.

Monday’s mission helped validate Musk’s vision for lower-cost spaceflight and provides SpaceX a boost in his race with fellow billionaire Jeff Bezos to develop craft that can survive fiery blasts and return to Earth to be reused. Instead of ditching the booster, SpaceX used thrusters and sophisticated navigation to steer it from space to Landing Zone 1, a former U.S. Air Force rocket and missile testing range.

Scotia announced the redemption of sub-debt on its pretend-maturity:

Scotiabank (TSX: BNS) (NYSE: BNS) today announced that the Bank intends to redeem all outstanding 6.65% debentures due January 22, 2021 for 100% of their principal amount plus accrued interest to the redemption date. The redemption will occur on January 22, 2016. Formal notice will be delivered to the debenture holders in accordance with the terms and conditions set forth in the related trust indenture.

The redemption has been approved by the Office of the Superintendent of Financial Institutions and will be financed out of the general funds of Scotiabank.

This will assist new issue salesmen to sell ten-year sub-debt as if it should have a spread off five-year Canadas, although from what I understand this doesn’t work as well as it used to:

Investors who leaped into Basel-compliant bonds issued by Canadian banks to great fanfare are likely regretting their haste. A year on, the reward for taking on the risk of bailing out a bank has become much richer.

Relative yields of the bonds have widened 25 basis points this year, the worst performance among Canadian five-year corporate bonds, according to RBC Dominion Securities research. The debt is designed to convert to equity if a bank gets into financial distress, in line with new Basel rules to prevent another financial crisis. The first issue of the debt, called contingent capital bonds, in Canada was by Royal Bank of Canada in July, 2014.

RioCan REIT, proud issuer of REI.PR.A and REI.PR.C, was confirmed at Pfd-3(high) by DBRS:

DBRS Limited (DBRS) has today confirmed RioCan Real Estate Investment Trust’s (RioCan or the Trust) Senior Unsecured Debentures rating and Senior Unsecured Debentures, Series I rating at BBB (high) and its Preferred Trust Units rating at Pfd-3 (high), all with Stable trends. The confirmations reflect RioCan’s near-term enhanced financial flexibility to fund its development pipeline and DBRS’s expectation that financial metrics will return to BBB (high) levels. The confirmations follow RioCan’s announcement to sell its U.S. portfolio of 49 retail properties located in the Northeastern United States and Texas for a total sale price of USD 1.9 billion or $2.7 billion to Blackstone Real Estate Partners VIII (Blackstone; the Transaction).

…

DBRS notes that a positive rating action could occur should RioCan increase the size of its portfolio and reduce its geographic concentration while maintaining EBITDA interest coverage (including capitalized interest) above 3.0 times, such that it is more consistent with the A (low) rating category.

Valener Inc., proud issuer of VNR.PR.A, was confirmed at Pfd-2(low) by DBRS:

DBRS Limited (DBRS) has today confirmed Valener Inc.’s (Valener or the Company) Cumulative Rate Reset Preferred Shares, Series A rating at Pfd-2 (low) with a Stable trend. Valener’s preferred share rating is based on the credit quality of Gaz Métro Limited Partnership (the Partnership), which guarantees the First Mortgage Bonds and Senior Secured Notes (rated “A”) of Gaz Métro inc. The one-notch differential in the ratings of Valener and the Partnership reflects the structural subordination at Valener.

…

As the Company has no bonds/debentures issued, and is not expected to issue any long-term debt in the foreseeable future, its leverage solely consists of its credit facility outstanding. As at September 30, 2015, Valener utilized approximately $120 million of the $200 million credit facility which matures on September 30, 2020. Valener’s debt-to-capital ratio was reasonable at approximately 14.3% as at September 30, 2015. Valener is expected to fund future growth investments in a prudent manner to maintain leverage within the 20% threshold. If Valener is unable to do so on a sustained basis, this could result in a negative rating action. Other key non-consolidated credit metrics have also remained supportive of the current rating category, including cash flow-to-interest at 38.8 times, cash-flow fixed coverage at 10.4 times and cash flow-to-debt at 49.7% in F2015.

It was a modestly negative day for the Canadian preferred share market, with PerpetualDiscounts off 7bp, FixedResets down 9bp and DeemedRetractibles losing 36bp. The Performance Highlights table is very long considering the placid overall numbers. Volume was very high.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

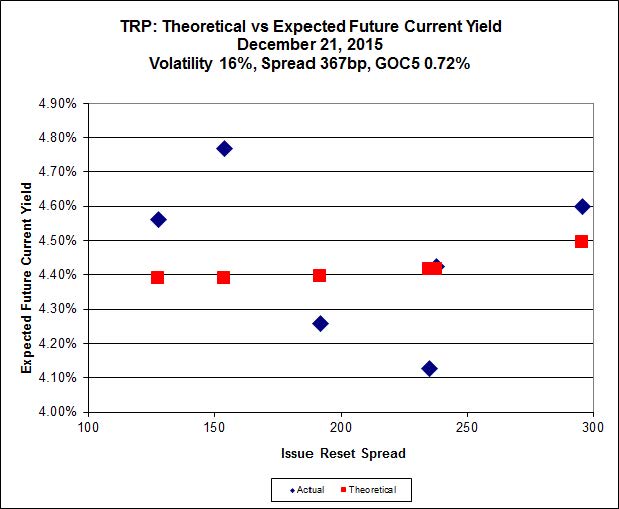

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 18.60 to be $1.22 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $1.02 cheap at its bid price of 11.85.

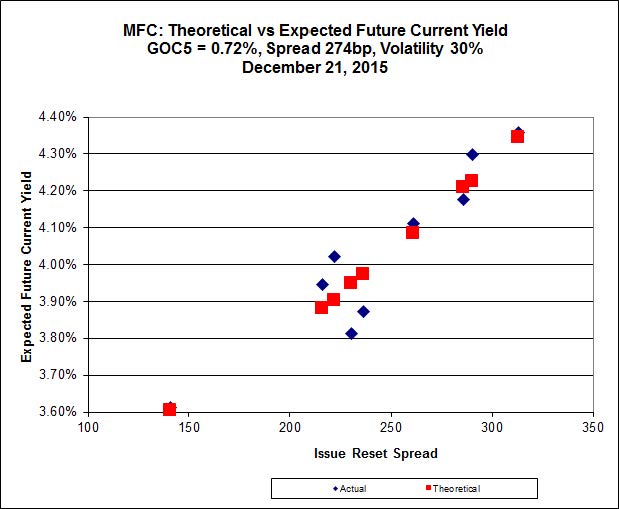

Click for Big

Most expensive is MFC.PR.N, resetting at +230bp on 2020-3-19, bid at 19.80 to be 0.68 rich, while MFC.PR.K, resetting at +222bp on 2018-9-19, is bid at 18.28 to be 0.55 cheap.

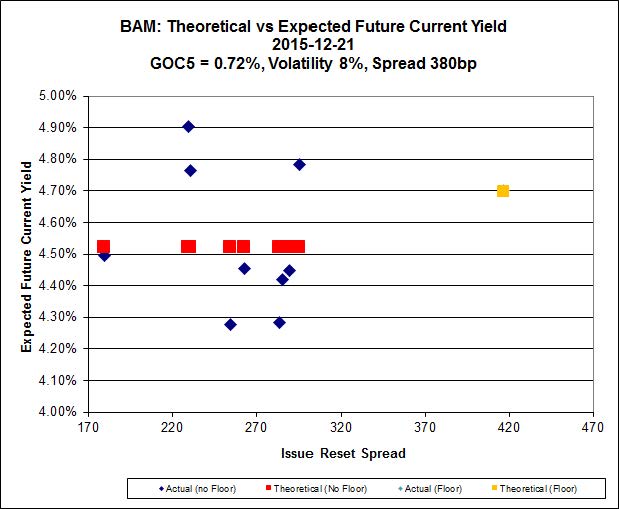

Click for Big

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 15.40 to be $1.30 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 20.78 and appears to be $1.09 rich.

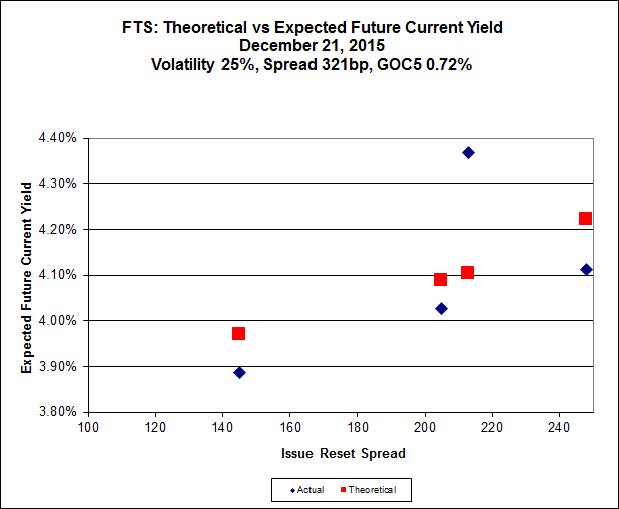

Click for Big

FTS.PR.M, with a spread of +248bp, and bid at 19.48, looks $0.51 expensive and resets 2019-12-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 16.31 and is $1.05 cheap.

Click for Big

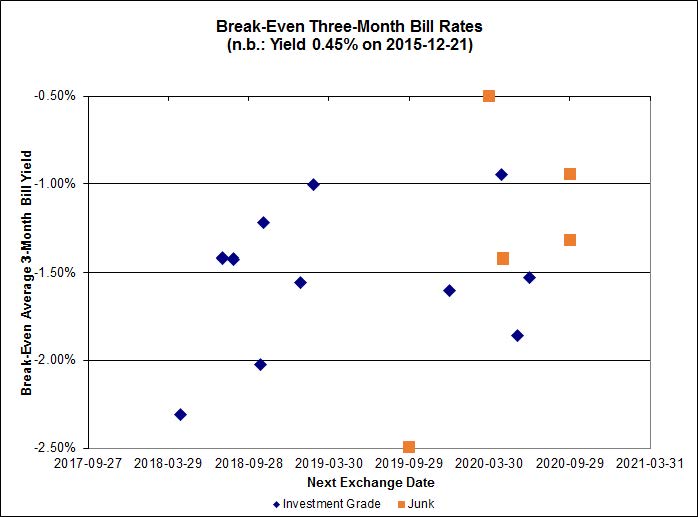

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.44%, with one outlier above -0.50%. There are five junk outliers above -0.50%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 5.12 % | 6.24 % | 34,043 | 16.35 | 1 | -3.5636 % | 1,513.5 |

| FixedFloater | 7.17 % | 6.35 % | 38,939 | 15.79 | 1 | 0.3788 % | 2,721.9 |

| Floater | 4.21 % | 4.31 % | 83,269 | 16.81 | 4 | 0.6949 % | 1,816.2 |

| OpRet | 4.86 % | 4.13 % | 26,335 | 0.68 | 1 | 0.1192 % | 2,738.6 |

| SplitShare | 4.83 % | 6.01 % | 84,147 | 1.86 | 6 | -0.0361 % | 3,199.9 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0361 % | 2,496.7 |

| Perpetual-Premium | 5.83 % | 5.90 % | 97,956 | 13.93 | 7 | -0.0686 % | 2,486.7 |

| Perpetual-Discount | 5.79 % | 5.87 % | 105,174 | 14.05 | 33 | -0.0666 % | 2,476.3 |

| FixedReset | 5.26 % | 4.64 % | 273,504 | 14.67 | 81 | -0.0881 % | 1,966.0 |

| Deemed-Retractible | 5.25 % | 5.32 % | 139,767 | 5.29 | 33 | -0.3552 % | 2,555.9 |

| FloatingReset | 2.84 % | 4.28 % | 68,806 | 5.66 | 11 | -0.9637 % | 2,086.8 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| VNR.PR.A | FixedReset | -5.37 % | Not real. The issue traded 6,560 shares today in a range of 18.64-20.12 before closing at 18.31-09, 2×2. VWAP was 19.42. I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 18.31 Evaluated at bid price : 18.31 Bid-YTW : 5.03 % |

| FTS.PR.M | FixedReset | -4.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 19.46 Evaluated at bid price : 19.46 Bid-YTW : 4.39 % |

| CIU.PR.C | FixedReset | -4.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 12.81 Evaluated at bid price : 12.81 Bid-YTW : 4.15 % |

| IAG.PR.G | FixedReset | -4.24 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.40 Bid-YTW : 7.10 % |

| BNS.PR.B | FloatingReset | -3.93 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.50 Bid-YTW : 4.81 % |

| BAM.PR.E | Ratchet | -3.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 25.00 Evaluated at bid price : 13.26 Bid-YTW : 6.24 % |

| FTS.PR.G | FixedReset | -3.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 16.31 Evaluated at bid price : 16.31 Bid-YTW : 4.64 % |

| FTS.PR.K | FixedReset | -2.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 17.20 Evaluated at bid price : 17.20 Bid-YTW : 4.36 % |

| MFC.PR.L | FixedReset | -2.51 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.25 Bid-YTW : 7.51 % |

| HSE.PR.C | FixedReset | -2.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 16.35 Evaluated at bid price : 16.35 Bid-YTW : 6.17 % |

| CU.PR.C | FixedReset | -2.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 18.36 Evaluated at bid price : 18.36 Bid-YTW : 4.37 % |

| HSE.PR.E | FixedReset | -2.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 17.95 Evaluated at bid price : 17.95 Bid-YTW : 6.08 % |

| BNS.PR.D | FloatingReset | -2.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.45 Bid-YTW : 6.76 % |

| PWF.PR.A | Floater | -1.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 12.35 Evaluated at bid price : 12.35 Bid-YTW : 3.86 % |

| BAM.PF.E | FixedReset | -1.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 19.12 Evaluated at bid price : 19.12 Bid-YTW : 4.63 % |

| BAM.PR.T | FixedReset | -1.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 15.90 Evaluated at bid price : 15.90 Bid-YTW : 4.94 % |

| ENB.PR.A | Perpetual-Discount | -1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 22.61 Evaluated at bid price : 22.86 Bid-YTW : 6.07 % |

| PWF.PR.T | FixedReset | -1.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 21.82 Evaluated at bid price : 22.10 Bid-YTW : 3.72 % |

| BNS.PR.C | FloatingReset | -1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.78 Bid-YTW : 4.78 % |

| CM.PR.Q | FixedReset | -1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 19.30 Evaluated at bid price : 19.30 Bid-YTW : 4.64 % |

| PWF.PR.K | Perpetual-Discount | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 21.45 Evaluated at bid price : 21.45 Bid-YTW : 5.87 % |

| MFC.PR.K | FixedReset | -1.24 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.28 Bid-YTW : 7.38 % |

| PVS.PR.B | SplitShare | -1.24 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2019-01-10 Maturity Price : 25.00 Evaluated at bid price : 23.90 Bid-YTW : 6.04 % |

| MFC.PR.J | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.25 Bid-YTW : 6.32 % |

| BAM.PF.F | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 20.25 Evaluated at bid price : 20.25 Bid-YTW : 4.67 % |

| RY.PR.F | Deemed-Retractible | -1.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.46 Bid-YTW : 4.95 % |

| MFC.PR.G | FixedReset | -1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.05 Bid-YTW : 6.02 % |

| PWF.PR.P | FixedReset | -1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 13.50 Evaluated at bid price : 13.50 Bid-YTW : 4.36 % |

| MFC.PR.I | FixedReset | -1.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.43 Bid-YTW : 5.83 % |

| GWO.PR.Q | Deemed-Retractible | -1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.50 Bid-YTW : 6.65 % |

| BNS.PR.L | Deemed-Retractible | -1.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.70 Bid-YTW : 4.87 % |

| BAM.PF.D | Perpetual-Discount | 1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 19.85 Evaluated at bid price : 19.85 Bid-YTW : 6.21 % |

| BMO.PR.Z | Perpetual-Discount | 1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 22.86 Evaluated at bid price : 23.25 Bid-YTW : 5.41 % |

| RY.PR.I | FixedReset | 1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.10 Bid-YTW : 3.84 % |

| BMO.PR.T | FixedReset | 1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 17.98 Evaluated at bid price : 17.98 Bid-YTW : 4.41 % |

| BNS.PR.A | FloatingReset | 1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.61 Bid-YTW : 4.28 % |

| BAM.PF.G | FixedReset | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 20.78 Evaluated at bid price : 20.78 Bid-YTW : 4.57 % |

| CIU.PR.A | Perpetual-Discount | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 19.82 Evaluated at bid price : 19.82 Bid-YTW : 5.87 % |

| SLF.PR.G | FixedReset | 1.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.98 Bid-YTW : 8.68 % |

| BAM.PF.H | FixedReset | 1.17 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-12-31 Maturity Price : 25.00 Evaluated at bid price : 26.00 Bid-YTW : 4.10 % |

| BAM.PR.N | Perpetual-Discount | 1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 19.37 Evaluated at bid price : 19.37 Bid-YTW : 6.17 % |

| RY.PR.J | FixedReset | 1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 19.41 Evaluated at bid price : 19.41 Bid-YTW : 4.54 % |

| PVS.PR.D | SplitShare | 1.39 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2021-10-08 Maturity Price : 25.00 Evaluated at bid price : 22.65 Bid-YTW : 6.55 % |

| RY.PR.Q | FixedReset | 1.43 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-05-24 Maturity Price : 25.00 Evaluated at bid price : 25.58 Bid-YTW : 5.05 % |

| TRP.PR.B | FixedReset | 1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 10.96 Evaluated at bid price : 10.96 Bid-YTW : 4.66 % |

| BIP.PR.A | FixedReset | 1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 19.80 Evaluated at bid price : 19.80 Bid-YTW : 5.50 % |

| BNS.PR.Y | FixedReset | 1.51 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.20 Bid-YTW : 5.61 % |

| BMO.PR.W | FixedReset | 1.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 18.03 Evaluated at bid price : 18.03 Bid-YTW : 4.36 % |

| CU.PR.I | FixedReset | 1.56 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-12-01 Maturity Price : 25.00 Evaluated at bid price : 25.42 Bid-YTW : 4.20 % |

| BAM.PR.B | Floater | 1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 10.97 Evaluated at bid price : 10.97 Bid-YTW : 4.31 % |

| BAM.PF.A | FixedReset | 1.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 20.35 Evaluated at bid price : 20.35 Bid-YTW : 4.63 % |

| NA.PR.Q | FixedReset | 1.75 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.95 Bid-YTW : 3.48 % |

| BMO.PR.S | FixedReset | 1.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 18.60 Evaluated at bid price : 18.60 Bid-YTW : 4.37 % |

| CM.PR.O | FixedReset | 1.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 18.47 Evaluated at bid price : 18.47 Bid-YTW : 4.42 % |

| CM.PR.P | FixedReset | 2.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 4.43 % |

| BMO.PR.Q | FixedReset | 2.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.75 Bid-YTW : 5.46 % |

| BAM.PR.K | Floater | 2.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 10.80 Evaluated at bid price : 10.80 Bid-YTW : 4.38 % |

| MFC.PR.F | FixedReset | 3.73 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.74 Bid-YTW : 8.93 % |

| TRP.PR.A | FixedReset | 4.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 15.50 Evaluated at bid price : 15.50 Bid-YTW : 4.49 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| FTS.PR.E | OpRet | 222,000 | Nesbitt crossed blocks of 200,000 and 20,000, both at 25.22. YTW SCENARIO Maturity Type : Soft Maturity Maturity Date : 2016-08-31 Maturity Price : 25.00 Evaluated at bid price : 25.20 Bid-YTW : 4.13 % |

| RY.PR.Q | FixedReset | 205,155 | National bought 13,500 from anonymous at 25.50; Desjardins sold 10,000 to RBC and another 10,600 to National, both at 25.60. YTW SCENARIO Maturity Type : Call Maturity Date : 2021-05-24 Maturity Price : 25.00 Evaluated at bid price : 25.58 Bid-YTW : 5.05 % |

| RY.PR.J | FixedReset | 131,479 | Scotia crossed 100,000 at 19.35. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 19.41 Evaluated at bid price : 19.41 Bid-YTW : 4.54 % |

| RY.PR.D | Deemed-Retractible | 102,550 | RBC crossed 100,000 at 24.80. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.62 Bid-YTW : 4.88 % |

| BNS.PR.E | FixedReset | 70,870 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-04-25 Maturity Price : 25.00 Evaluated at bid price : 25.65 Bid-YTW : 4.98 % |

| TD.PF.B | FixedReset | 55,622 | TD crossed 31,000 at 18.12. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-21 Maturity Price : 18.17 Evaluated at bid price : 18.17 Bid-YTW : 4.39 % |

| There were 72 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| ENB.PR.A | Perpetual-Discount | Quote: 22.86 – 23.50 Spot Rate : 0.6400 Average : 0.4216 YTW SCENARIO |

| ELF.PR.H | Perpetual-Discount | Quote: 23.03 – 23.67 Spot Rate : 0.6400 Average : 0.4305 YTW SCENARIO |

| BNS.PR.B | FloatingReset | Quote: 21.50 – 22.13 Spot Rate : 0.6300 Average : 0.4220 YTW SCENARIO |

| BAM.PF.D | Perpetual-Discount | Quote: 19.85 – 20.41 Spot Rate : 0.5600 Average : 0.3747 YTW SCENARIO |

| FTS.PR.I | FloatingReset | Quote: 11.26 – 11.92 Spot Rate : 0.6600 Average : 0.4953 YTW SCENARIO |

| RY.PR.D | Deemed-Retractible | Quote: 24.62 – 25.09 Spot Rate : 0.4700 Average : 0.3102 YTW SCENARIO |