National Bank of Canada has announced:

that it has entered into an agreement with a group of underwriters led by National Bank Financial Inc. for the issuance on a bought deal basis of 10 million non-cumulative 5-year rate reset first preferred shares series 34 (non-viability contingent capital (NVCC)) (the “Series 34 Preferred Shares”) at a price of $25.00 per share, to raise gross proceeds of $250 million.

National Bank has granted the underwriters an option to purchase, on the same terms, up to an additional 2 million Series 34 Preferred Shares. This option is exercisable in whole or in part by the underwriters at any time up to two business days prior to closing. The gross proceeds raised under the offering will be $300 million should this option be exercised in full.

The Series 34 Preferred Shares will yield 5.60% annually, payable quarterly, as and when declared by the Board of Directors of National Bank, for the initial period ending May 15, 2021. The first of such dividends, if declared, shall be payable on May 15, 2016. Thereafter, the dividend rate will reset every five years at a level of 490 basis points over the then 5-year Government of Canada bond yield. Subject to regulatory approval, National Bank may redeem the Series 34 Preferred Shares in whole or in part at par on May 15, 2021 and on May 15 every five years thereafter.

Holders of the Series 34 Preferred Shares will have the right to convert their shares into an equal number of non-cumulative floating rate first preferred shares series 35 (non-viability contingent capital (NVCC)) (the “Series 35 Preferred Shares”), subject to certain conditions, on May 15, 2021, and on May 15 every five years thereafter. Holders of the Series 35 Preferred Shares will be entitled to receive quarterly floating dividends, as and when declared by the Board of Directors of National Bank, equal to the 90-day Government of Canada Treasury Bill rate plus 490 basis points.

The net proceeds of the offering will be used for general corporate purposes and added to National Bank’s capital base. The expected closing date is on or about January 22, 2016. National Bank intends to file in Canada a prospectus supplement to its December 1, 2014 base shelf prospectus in respect of this issue.

They later announced:

that as a result of strong investor demand for its previously announced domestic public offering of non-cumulative 5-year rate reset first preferred shares series 34 (non-viability contingent capital (NVCC)) (the “Series 34 Preferred Shares”), the size of the offering has been increased to 16 million shares. The gross proceeds of the offering will now be $400 million. The offering will be underwritten by a syndicate led by National Bank Financial Inc. The expected closing date is on or about January 22, 2016. National Bank will make an application to list the Series 34 Preferred Shares as of the closing date on the Toronto Stock Exchange.

The net proceeds of the offering will be used for general corporate purposes and added to National Bank’s capital base.

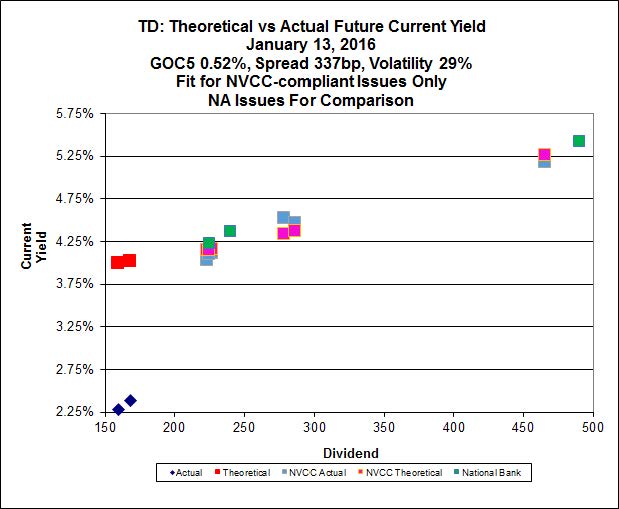

Implied Volatility analysis is not possible for the NA issues, since there are only three of them including the new issue. However, comparison to today’s analysis for TD shows that the issue is attractively priced. The very high level of Implied Volatility leads to the conclusion that there is a very high degree of directional bias in the pricing of TD’s NVCC-compliant FixedResets. As this bias recedes (assuming that it ever does!), Implied Volatility will decline, the curve will flatten and the higher-spread issues (most notably the new issues) will significantly outperform the lower-spread issues.

The NA issues are priced very close to the TD curve, with perhaps a slight premium.

Note that the NVCC non-compliant issues are so obviously differentiated from the NVCC-compliant ones that they are not included in the calculation, although they are shown in the chart.

On the other hand, the directional bias could be quite right! There will be many among us who think that +490 is an utterly ridiculous spread for solid bank – NVCC or no NVCC – and that spreads will narrow once memories of 2015 fade. Given this particular scenario, the lower-spread issues will shine: a calculation based on projected calculated values of 250bp Spread and 10% Implied Volatility implies that the extant TD NVCC-compliant preferreds will enjoy total capital gains in the area of 35% which, if achieved in a reasonable timeframe, will dwarf the yield advantage of the new issue for which capital gains will be a big fat zero.

So pays yer money and takes yer chances, gents, roll up, roll up! If you think current market conditions are the new normal, you’ll like the new issue. If you think this is a transitory crash, you won’t.

Click for Big

Hi James…it’s fairly clear that the market is operating under the assumption that all the banks’ non compliant debt will be redeemed over the next 5 years or so, since it will no longer qualify as tier 1 capital. Heaven forbid this… but, if the GOC 5yr maintains its current level (or lower), is there any chance that the banks choose to extend some of the issues beyond the deemed retraction date, and keep them as some other form of capital (other than tier 1)? I’m thinking of the fixed resets with particularly tight spreads (ex. BNS.PR.Z).

Very good question LD as I do share that concern. A RY discretionary broker told me they would be redeemed as it is too costly to maintain for the banks once it is no longer Tier 1. I don’t see why. Even if it is not Tier 1 anymore, it looks like very cheap money such that I don’t see the rationale of raising capital at 5.50% to buy back cheaper shares. I look forward reading James’ answer to your question.

i agree, the banks will look very closely at the value of redeeming such cheap capital (seriously, 1.50 over 5y Canadas is desperately cheap), but keep in mind that it’s all about the 3m/5y spread and general credit spreads. so five years from now, can you imagine spreads being even narrower than what it is for BNS.Z? so then it’s a no-brainer for the banks to redeem, especially since they’re not Tier 1. but imagine if the situation was similar to what it is today, with massive yield spreads, so the value of redeeming cheap capital may be very limited, even if it’s not Tier 1. on the other hand, if BNS.Z has got a small issue size, then the bank may redeem it if spreads are narrower than today but not too narrow, so the cost of redeeming is low. in other words, lots of moving parts and it’s just too early to know what will be in five years, enjoy the uncertainty.

Consider the possibility of the GoC5y being below 0, which is entirely possible considering how they define it in some prospecti. Does that mean that a low spread reset could actually reset at a negative rate? If that is possible, then a low price will result in an even bigger negative effective yield.

Any ideas?

Since the conversation has evolved a bit, I will clarify my questions.

1) Do the banks have the option to keep extending the non-compliant preferred shares?

2) If so, what will the issuer compare the preferred with to decide if they will extend, or redeem? Is it reasonable to assume it will be the relevant bank’s 5yr bond yield (currently 2% ish) adjusted by the equivalency factor, plus some assumption about a seniority spread?

3) Is there another motivation that would cause the banks to want to get these things off the balance sheet?

Thanks

fed, that’s a really good question, which i suppose the Swiss and Germans and Japanese may already have had to deal with. anyway, i’ve checked a couple of recent pref prospectuses and i don’t see any reference in them for the words “zero” or “negative,” which i presume means that the question is simply not addressed at all. so it would seem that it could, theoretically, reset at negative but the issuer would have no way of enforcing a negative yield, so practically the worst would be zero. i can’t even imagine what such a pref would be trading at, that’s why the floor resets are so valuable, again, of course as James has pointed out, only if you believe that yields are going to stay this low for a very VERY long time.

James may give better detail of the Basel 3 – OSFI rule impacts, but I’ll echo that Louisprefs response is on point – it is becoming much more expensive for banks to hold non tier 1 capital – the impact is more complicated than just the rate the debt pays at (impact on required capital ratios etc). All the banks can, and routinely do, issue paper paying interest rates as low or lower than their current cheapest reset dividends.

From a review of OSFI guidelines, I’m not sure they are even allowed to not retire these prefs – it looks like a straight ‘retire 10% per year’ – ? James ? – if you don’t know, I’ll dig a little more next week.

Prefs are an equity security and fully paid when issued – there is no provision to call on holders to pay in the case of negative rates. Equity holdings are limited liability. Fwiw, negative rate bonds are typically issued with a 0 or small coupon and sold at a premium to face – the negative yield comes from the capital loss. Banks can give negative rates (ie charge you) on deposits.

is there any chance that the banks choose to extend some of the issues beyond the deemed retraction date, and keep them as some other form of capital (other than tier 1)? I’m thinking of the fixed resets with particularly tight spreads (ex. BNS.PR.Z).

Yes, this is a risk, albeit a small one, I think. For instance look at National Bank’s recent presentation. They did C$750M7Y Senior Unsecured 2.105% Mar 22 and C$850M 3Y Senior Unsecured 1.951% Dec 17. The coupons on those are very tiny … when you account for the fact that interest payments are tax deductible and dividend payments aren’t, you see that preferreds are still pretty expensive relative to bonds even when they reset at only +150bp. Of course, preferreds are perpetual, but I’m not sure how much they care about that.

NVCC non-compliant issues will have the same status as senior debt when it leaves the Tier 1 calculation.

The big worry is that the banks will seek to add NVCC compliance to the trust indentures by shareholder vote. Although most people here are sophisticated enough to want a LOT of money for a ‘yes’ vote, not everybody is so sophisticated. This is one reason why I find the DC.PR.C Plan of Arrangement so fascinating.

Even if it is not Tier 1 anymore, it looks like very cheap money such that I don’t see the rationale of raising capital at 5.50% to buy back cheaper shares. I look forward reading James’ answer to your question.

Well, let’s go back to BNS.PR.Z, which recently reset at 2.063%, which is the equivalent of 2.68% interest (the banks have to take the dividends out of after-tax profit).

BNS 3.367% 2025-12-8 is callable in 2020 at par and trades in accordance with its pretend-maturity to yield 3.34% according to Perimeter.

But they have a public bond (I don’t know whether it’s a deposit note or senior debt but at this moment it doesn’t make much difference. It trades to yield 1.88%.

So that’s an 80bp funding advantage for the actual bond against the low-spread FixedReset, even at today’s low GOC-5 yield. On the other hand, the FixedReset has be advantage of being perpetual money.

All in all, I’d say that it will be called on grounds of cost; perhaps not at the very next opportunity in 2021, but … eventually! Because, I say, eventually five-year Canadas will pay a positive real rate of return, and once they start doing that again, the funding advantage for senior debt will be much more impressive.

Consider the possibility of the GoC5y being below 0, which is entirely possible considering how they define it in some prospecti. Does that mean that a low spread reset could actually reset at a negative rate? If that is possible, then a low price will result in an even bigger negative effective yield.

Well, they would have to be well below zero before the indicated preferred rate went below zero, even the low-spread issues in the 130bp-180bp range!

Even in Europe, five year AAA governments are yielding -0.25%.

Some floating-rate coupons have turned negative – see, for example, the “Realkredit Danmark Annual Report 2015”:

I believe that in practice a floor of zero has been established in Europe, but that’s a whole topic in itself. There are two problems:

I) Nobody has ever thought about this. So there’s nothing in the prospectus, nothing in law, nothing anywhere. The borrowers are pretty happy with zero, anyway!

ii) Remember the Husky Energy Installment Receipts from the ’90’s? Worth $15 on issue, since the common was at $30 and it was essentially a warrant with an exercise price of $15.00. There was a LOT of fraud with those things; the brokers went nuts trying to trade things with negative prices; a lot of the ‘buyers’ bought a lot of the Receipts, got paid a lot of money for taking on the liability, and then disappeared, leaving the brokerages on the hook.

So basically on this one I’ve consulted my Official Portfolio Management Magic Eight-Ball and determined that the answer is “Reply Hazy. Try Again”.

Clearstream is a competitor to Euroclear, i.e., it performs the same role as CDS does in the Canadian market (although I’m sure a specialist could point out differences.

Here’s what Clearstream has to say about negative coupons on FRNs:

For what its worth, last February on its conference call, Atlantic Power, said they would effectively use a floor of zero for the reference interest rate if interest rates went negative.

“Unidentified Analyst:

Okay, great. And then on the preferred there was – wasn’t any mention as I see the dividend decline and there was a rate reset. And a couple of questions, where do you see that is obviously they had a severe discount to liquidity preference.

So the implied IRR if there’s going to be liquidity event it would be quite high on those. But also with reset is there any floor in that or if government rates go negative is there a chance where you just use the negative rate as the base to determine the spread?

James J. Moore:

Yeah, there’s a spread above that government rate. So and that spread is 4.18%, but I think that that would be the floor to break one negative I don’t think that we get the negative type of spread would be floor of 4.18.”

1) Do the banks have the option to keep extending the non-compliant preferred shares?

Yes. The NVCC rules only relate to whether they may be included in Tier 1 Capital, they do not force redemption.

2) If so, what will the issuer compare the preferred with to decide if they will extend, or redeem? Is it reasonable to assume it will be the relevant bank’s 5yr bond yield (currently 2% ish) adjusted by the equivalency factor, plus some assumption about a seniority spread?

There will also be an accounting for the fact that the preferreds are perpetual money. This is worth some premium over the five-year new-issue Senior Bond yield.

The Seniority Spread will be of very minor importance. While it will be included in the equity section of the balance sheet, people don’t really look at debt-to-equity for banks all that much. They will be looking at the capital ratios, which will not be affected by how much NVCC non-compliant preferreds are outstanding (once the rule has been phased in completely). Of course, the fed’s ‘bail-in’ rules, of which we haven’t heard much lately, are a wild-card for just about everything.

3) Is there another motivation that would cause the banks to want to get these things off the balance sheet?

I think the decision will be strictly economic.

From a review of OSFI guidelines, I’m not sure they are even allowed to not retire these prefs – it looks like a straight ‘retire 10% per year’ – ? James ? – if you don’t know, I’ll dig a little more next week

Not quite. The banks are not forced to retire NVCC non-compliant capital, it’s just that the amount they’re able to include in Tier 1 declines by 10% per year from a base set on the effective date of the year.

Yeah, there’s a spread above that government rate. So and that spread is 4.18%, but I think that that would be the floor to break one negative I don’t think that we get the negative type of spread would be floor of 4.18.”

To be perfectly frank, I have no idea what that actually means.

Hello, with regard to the td fixed resets, can you please provide an example or two of these that have the Potential upside as mentioned as a possibility in the above post.

Thanks.

Regarding the concerns expressed by some of one day having a negative return on their prefs (the kind of concern that might explain why prefs are nowadays priced so low), I totally agree with nebulousanalyst above comment:

“Prefs are an equity security and fully paid when issued – there is no provision to call on holders to pay in the case of negative rates. Equity holdings are limited liability.”

It is trite law that a shareholder’s liability cannot exceed its initial investment. So, even if 5 years Canadas were to reach an effective rate of – 1.5% percent, a resetable at say +125bps would at worst pay 0%.

I would also like to know if James agree with nebelousanalyst (as I also do) that:

“negative rate bonds are typically issued with a 0 or small coupon and sold at a premium to face – the negative yield comes from the capital loss. Banks can give negative rates (ie charge you) on deposits.”

It seems to me totally irrealistic to even think that Canada 5 years bond could go below zero. Canada is not a safe heaven for cash (unlike with Switzerland) because of its currency linked to oil prices. The Bank of Canada could charge a negative rate for deposits by bank but, still, no one would agree to pay a premium on Canadian bonds for an effective negative return. The reason why people do it with Switzerland or Japan is that they also get exchange rate protection, a feature Canadian bonds are clearly not offering.

with regard to the td fixed resets, can you please provide an example or two of these that have the Potential upside as mentioned as a possibility in the above post.

Each of the lower spread TD NVCC-compliant issues, TD.PF.A, TD.PF.B and TD.PF.C, may be expected to experience capital gains in excess of 30% IF market conditions change such that the spread is 250bp and Implied Volatility is 10%.

Please note that:

i) That’s a big if!

ii) Issues with a similar Issue Reset Spread and price will be expected to perform similarly, provided that such a change reflects overall market conditions

iii) this ignores the potential for changes in credit quality.

iv) I’m posting this solely because I mentioned the scenario in the main post and I feel it incumbent on me to back it up. PrefBlog is not a forum for advice, I am not your investment advisor and this is mentioned for the purpose of illustrating differences in return distribution under one specific scenario only. As noted in the main post, a plausible alternative scenario (that current conditions represent a version of the new normal) results in projected returns for higher-spread issues outperforming.

v) Materials are provided via PrefBlog for you to do this sort of what-if scenario analysis for yourself. See Implied Volatility for FixedResets and the associated calculator.

would also like to know if James agree with nebelousanalyst (as I also do) that:

“negative rate bonds are typically issued with a 0 or small coupon and sold at a premium to face – the negative yield comes from the capital loss. Banks can give negative rates (ie charge you) on deposits.”

Yes, that’s merely a statement of fact, but we’re talking about extant issues, not new issues. As the Clearstream notice partially copied above indicates, it’s not all cut and dried; a lot will have to do with specific wording in the prospectus and how eager the issuer is to ding the shareholders.

This has never been tested in court. As has happened so often in recent years, we’re in uncharted territory here.

no one would agree to pay a premium on Canadian bonds for an effective negative return.

They were saying this in Europe ten years ago and look what happened. I happen to agree with your opinion; but … I could be wrong!

LouisPref and myself did mention extant issues – under our current securities laws these are limited liability holdings

LouisPref and myself did mention extant issues – under our current securities laws these are limited liability holdings

Well, OK … but the FRNs mentioned in the Clearstream notice are presumably also limited liability holdings, so I’d want to wait to see a court case!

One thing that occurs to me is that amounts due to the issuer could be collected by reducing the par value of the securities.

James,

Could this be added to PrefInfo?

Thanks,

Peter

Could this be added to PrefInfo?

NA.PR.X. Done.

Interesting that NA now has another issue:

https://www.nbc.ca/en/about-us/news/news-room/press-releases/2016/20160602-National-Bank-of-Canada-Announces-NVCC-Preferred-Share-Offering.html

250 Million Issue, NVCC FixedReset, 5.40%+466.

I picked up some of that new NA issue this morning and there’s something I’m curious about. I ordered them through my Scotia iTrade account and ended up getting 30% of what I ordered. My question is: did everyone else who ordered this issue get the same 30% fill rate or does it vary between financial institutions and does it also depend on the size of your account (ie. are the big fish treated better than the small fry)?

I ordered just 100 shares through RBC direct investing. But they gave me none. 🙁

Offering was increased to 16M shares for gross proceeds of $400M.

NA.PR.X traded 10x normal volume of 130,000 shares and fell 13¢ to close at $26.

See New Issue: NA FixedReset, 5.40%+466, NVCC.

@Brian – getting pro-rated on new issues is standard if its a decent deal – I dread the deals I don’t get pro-rated on. The books closed really quickly on this issue (less than 1 hour through some channels).

You may get a different fill ratio at different institutions, and through different divisions (the firm may get an allocation, then sub allocate pools to through different divisions).

Retail clients stand a better chance of a higher % fill by putting in for larger size, very quickly, through a full service broker, particularly if that broker’s firm is one of the lead book runners.

Institutional clients get pro-rated on these deals too (and did on this one).

This is not to brag about anything but just to show that this is probably one of the few remaining advantages of dealing through full service brokers. Today (that is 3 business day after the above complaints of prorated or no fills with discount brokers) I was offered this new issue without stated limit on quantity but, in all fairness, with a broker aware that I normally order (and get) either 1000 or 1200 shares on new issues. I said “no thank you” this time eventhough I am happy to see the slightly lower coupon compared with the earlier issue.

… I should have phrased my above last sentence differently. A reset formula at +466 is still very high but it is, at last, a thightening compared with the earlier issues.