Assiduous Reader prefobsessed sent me a link to another Barry Critchley column titled Preferred shareholders, but in name only; he is incensed by the voting rights on the proposed takeover of Capstone. I have updated the post titled CSE.PR.A Ownership to Change?.

As reported by the Globe, Bank of Canada Deputy Governor Lawrence Schembri has given a speech titled Connecting the Dots: Elevated Household Debt and the Risk to Financial Stability. It’s really a reiteration of the same old song – Central Planning Now! – and there is one leap of logic that is rather conspicuous:

A broad-based decline in house prices would, in turn, have large direct effects on Canadian lenders and mortgage insurers. Results from stress tests show, however, that there are sufficient buffers in the financial system to withstand such a scenario.19 For example, the six largest Canadian banks, which hold roughly 70 per cent of outstanding mortgages, have increased the quantity and quality of their capital in recent years and are well diversified across regions and sectors. In addition, most of the mortgages they hold are supported by government-backed mortgage insurance programs or by high homeowner equity.

Nonetheless, if such a decline in house prices occurred, the impact on the broader Canadian economy and the financial system would be large.

Despite this, he does not call for a simple reduction the amount of CMHC insurance outstanding; preferring instead a politicized exercise in winner-picking:

Adopting macroprudential measures. In the immediate aftermath of the crisis, household debt and house prices resumed growing faster than disposable income in response to the lower interest rates and the recovering Canadian economy. The federal government and a number of agencies worked together to mitigate this growing systemic vulnerability. The Bank’s analysis of these vulnerabilities helped to inform these decisions.

For example, the federal government tightened rules for government-supported mortgage insurance four times over five years, starting in 2008. In December 2015, the federal government made a fifth change, increasing the minimum down payment for houses valued at from $500,000 to $1 million.For its part, the Office of the Superintendent of Financial Institutions (OSFI) released new guidance on mortgage underwriting and mortgage insurance that implemented enhanced global standards.24 In December, OSFI announced that it would issue for public consultation proposed rules for how much capital the banks and mortgage insurers must hold against vulnerable insured mortgages.

These measures help to limit access to borrowing to the most creditworthy households, for example, those with higher credit scores, and thus complement the accommodative monetary policy of the Bank of Canada by better targeting the stimulus to those households with the capacity to borrow.

The CMHC is the issue. As he emphasizes, the Feds have a considerable amount of wrong-way risk on their books … a decline in housing will lead to an increase in federal debt (via bail-out of the CMHC) at the same time as a recession (or worse!) demands running a deficit. Clearly, the CHMC insurance outstanding should be cut back.

But it’s more fun to pick winners, obviously.

The head of EnCana gives us an idea of how bad the oil & gas situation really is:

“The job reductions not only at Encana but across the industry have been as severe as I’ve ever seen in 33 years,” CEO Doug Suttles said in a conference call with investors after the company released its fourth quarter results.

Last year, as oil prices took a nosedive, the company laid off 19 per cent of its workers. It began 2015 with 3,129 employees, meaning it ended the year with about 2,500 staff.

Encana did not say how many jobs would be affected by the latest round of layoffs. But based on last year’s figures, it’s expected another 500 people would lose their jobs this year.

“This will bring us to about 55 per cent reduction from just over two years ago,” Suttles said.

And it’s not just the producers who are scrambling to assure funding:

Enbridge Inc. plans to raise C$2 billion ($1.5 billion) in a share sale to shore up its finances in the midst of an oil price rout.

The Canadian pipeline company agreed with a group of lenders to issue 49.14 million common shares from treasury in a so-called bought deal, according to a statement. The funds will be used to pay short-term debt, the company said.

Canadian energy companies face a wave of debt maturities over the next five years that could make it challenging for them to access financing as investors drive up borrowing costs and shun commodities-related debt. Oil has plunged about 70 percent since mid-2014, sapping revenue.

Enbridge’s sale follows to other bought deals in the past week. Whitecap Resources Inc. and Raging River Exploration Inc. both raised C$95 million in the past week through equity raises of their own to pay down debt and fund capital expenditures.

So perhaps we should be grateful that Pembina Pipeline Corporation, proud issuer of PPL.PR.A, PPL.PR.C, PPL.PR.E, PPL.PR.G, PPL.PR.I and PPL.PR.K, was confirmed at Pfd-3 by DBRS:

DBRS Limited (DBRS) has today confirmed the Issuer Rating and Senior Unsecured Notes rating of Pembina Pipeline Corporation (Pembina or the Company) at BBB, and the Company’s Preferred Shares at Pfd-3. The trends remain Stable. The confirmations largely reflect DBRS’s view that Pembina continues to maintain solid credit metrics and liquidity in the current significantly lower energy price environment, and has executed most of its major capital projects within budget and on schedule.

…

Pembina is currently pursuing a number of large capital projects in 2016 and 2017, mainly on its conventional pipelines, and natural gas and natural gas liquids (NGL) processing plants. Most projects are supported by ToP or FFS commitments from the producers for a significant portion of the designed capacity. Capex in 2016 and 2017 is estimated to be approximately $2.1 and $1.0 billion, respectively. As a result, substantial free cash flow deficits are expected to be incurred over the next two years. During this period, Pembina faces several challenges, such as (1) significant project execution risk relating to potential cost overruns and project delays, and (2) financing free cash flow deficits in a prudent manner as to maintain credit metrics at or close to current levels to be consistent with the current rating. DBRS expects Pembina to maintain the debt-to-capital ratio at around 40% and the cash flow-to-debt ratio at 25% on a sustainable basis. DBRS recognizes that during this period of large capital projects, Pembina’s credit metrics are expected to decline modestly but should improve once the major projects are completed. However, should Pembina’s credit metrics deteriorate significantly from current levels, a negative rating action could occur.

It was another poor day for the Canadian preferred share market, with PerpetualDiscounts losing 49bp, FixedResets down 31bp and DeemedRetractibles off 21bp. The Performance Highlights table was produced. Volume was above average.

PerpetualDiscounts now yield 5.86%, equivalent to 7.62% interest at the standard equivalency factor of 1.3x. Long corporates continue to yield about 4.2%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 340bp, a slight (and perhaps spurious) widening from the 335bp reported February 18.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

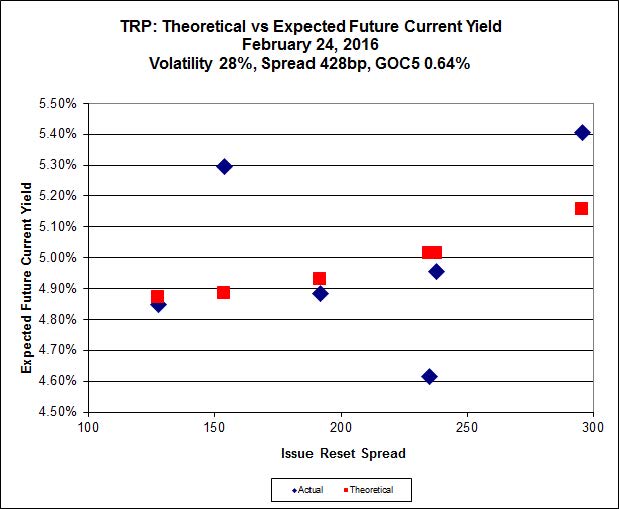

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 16.20 to be $1.29 rich, while TRP.PR.C, resetting 2021-1-30 at +296, is $0.87 cheap at its bid price of 10.29.

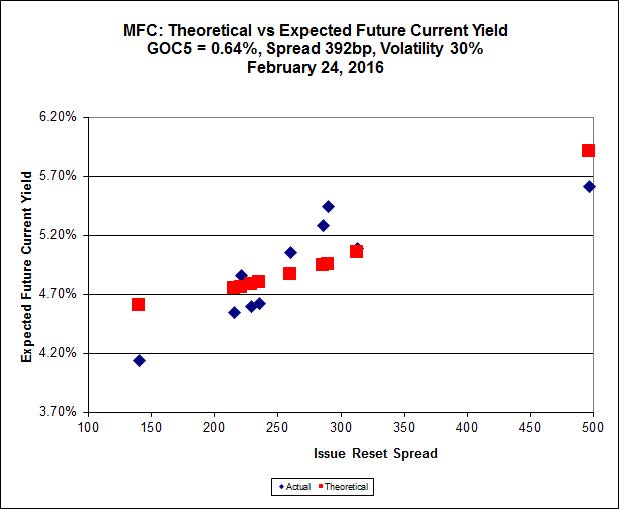

Click for Big

This analysis includes the new issue with a deemed price of 25.00.

Most expensive is the new issue, resetting at +497bp on 2021-6-19, deemed at 25.00 to be 1.27 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 16.25 to be 1.62 cheap.

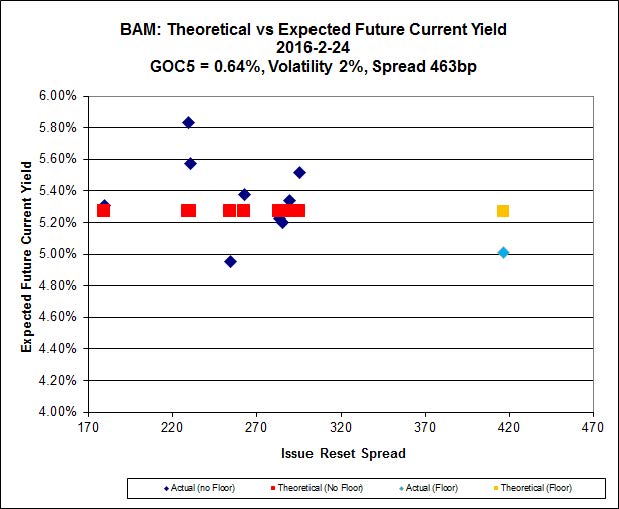

Click for Big

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 12.60 to be $1.35 cheap. BAM.PF.H, resetting at +417M500 on 2020-12-31 is bid at 24.96 and appears to be $1.24 rich.

Click for Big

FTS.PR.K, with a spread of +205bp, and bid at 14.60, looks $0.58 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 14.00 and is $0.42 cheap.

Click for Big

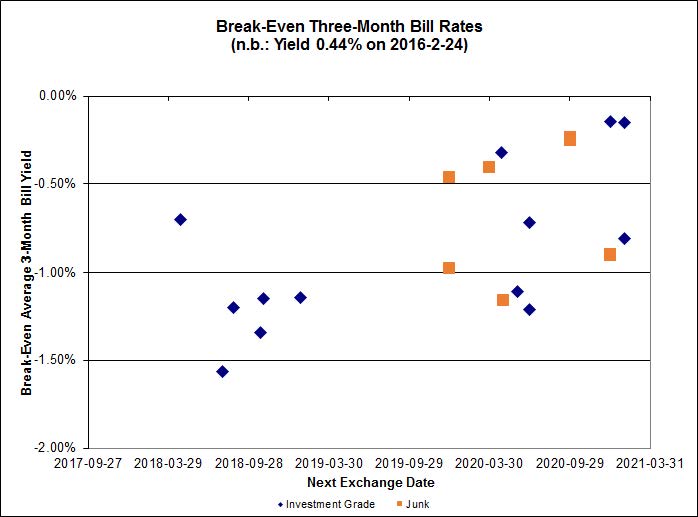

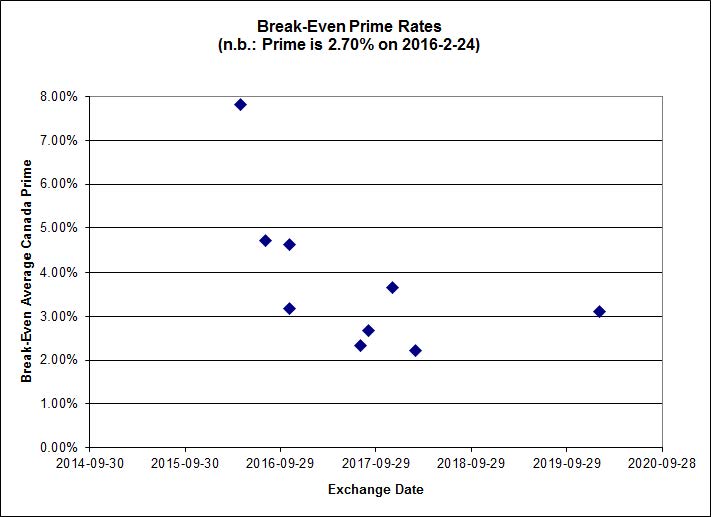

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.77%, with two outliers above 0.00% and one below -2.00%. Note that the range of the y-axis has changed today. There are three junk outlier above 0.00% and one below -2.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 5.64 % | 6.87 % | 14,091 | 15.60 | 1 | -0.9083 % | 1,382.5 |

| FixedFloater | 7.85 % | 6.87 % | 22,856 | 15.31 | 1 | -0.9009 % | 2,532.2 |

| Floater | 4.91 % | 5.10 % | 77,577 | 15.26 | 4 | 1.2625 % | 1,561.9 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2558 % | 2,736.0 |

| SplitShare | 4.88 % | 5.98 % | 74,648 | 2.68 | 6 | -0.2558 % | 3,201.6 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2558 % | 2,498.0 |

| Perpetual-Premium | 5.85 % | 5.84 % | 81,978 | 13.88 | 6 | -0.0864 % | 2,524.1 |

| Perpetual-Discount | 5.81 % | 5.86 % | 98,294 | 14.10 | 33 | -0.4942 % | 2,487.8 |

| FixedReset | 5.82 % | 5.22 % | 205,683 | 14.04 | 84 | -0.3073 % | 1,745.8 |

| Deemed-Retractible | 5.38 % | 6.03 % | 125,534 | 6.87 | 34 | -0.2148 % | 2,513.0 |

| FloatingReset | 3.18 % | 5.33 % | 49,452 | 5.48 | 16 | -0.3879 % | 1,921.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.F | FloatingReset | -7.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 9.96 Evaluated at bid price : 9.96 Bid-YTW : 6.02 % |

| BNS.PR.F | FloatingReset | -2.78 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.51 Bid-YTW : 8.33 % |

| TRP.PR.D | FixedReset | -2.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 15.24 Evaluated at bid price : 15.24 Bid-YTW : 5.27 % |

| FTS.PR.I | FloatingReset | -2.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 9.00 Evaluated at bid price : 9.00 Bid-YTW : 5.26 % |

| CIU.PR.C | FixedReset | -2.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 10.33 Evaluated at bid price : 10.33 Bid-YTW : 4.81 % |

| MFC.PR.M | FixedReset | -2.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.25 Bid-YTW : 9.29 % |

| TRP.PR.E | FixedReset | -2.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 16.20 Evaluated at bid price : 16.20 Bid-YTW : 5.03 % |

| TRP.PR.G | FixedReset | -2.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 16.65 Evaluated at bid price : 16.65 Bid-YTW : 5.49 % |

| BAM.PF.B | FixedReset | -2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 15.21 Evaluated at bid price : 15.21 Bid-YTW : 5.73 % |

| MFC.PR.K | FixedReset | -2.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.72 Bid-YTW : 10.33 % |

| RY.PR.J | FixedReset | -1.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 17.17 Evaluated at bid price : 17.17 Bid-YTW : 5.00 % |

| MFC.PR.N | FixedReset | -1.90 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.01 Bid-YTW : 9.43 % |

| TD.PF.C | FixedReset | -1.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 16.20 Evaluated at bid price : 16.20 Bid-YTW : 4.76 % |

| FTS.PR.H | FixedReset | -1.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 10.85 Evaluated at bid price : 10.85 Bid-YTW : 5.01 % |

| CU.PR.C | FixedReset | -1.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 15.28 Evaluated at bid price : 15.28 Bid-YTW : 5.06 % |

| TD.PF.D | FixedReset | -1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 17.71 Evaluated at bid price : 17.71 Bid-YTW : 4.92 % |

| TD.PR.S | FixedReset | -1.68 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.86 Bid-YTW : 4.43 % |

| RY.PR.M | FixedReset | -1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 4.92 % |

| IAG.PR.A | Deemed-Retractible | -1.53 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.62 Bid-YTW : 7.47 % |

| HSE.PR.C | FixedReset | -1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 13.11 Evaluated at bid price : 13.11 Bid-YTW : 7.70 % |

| PWF.PR.F | Perpetual-Discount | -1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 22.07 Evaluated at bid price : 22.30 Bid-YTW : 5.94 % |

| RY.PR.P | Perpetual-Discount | -1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 23.76 Evaluated at bid price : 24.10 Bid-YTW : 5.46 % |

| PWF.PR.K | Perpetual-Discount | -1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 21.34 Evaluated at bid price : 21.34 Bid-YTW : 5.87 % |

| CU.PR.I | FixedReset | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 23.05 Evaluated at bid price : 24.64 Bid-YTW : 4.48 % |

| BNS.PR.D | FloatingReset | -1.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.45 Bid-YTW : 7.90 % |

| BMO.PR.S | FixedReset | -1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 16.76 Evaluated at bid price : 16.76 Bid-YTW : 4.69 % |

| BAM.PF.E | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 16.10 Evaluated at bid price : 16.10 Bid-YTW : 5.47 % |

| BAM.PR.Z | FixedReset | -1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 16.32 Evaluated at bid price : 16.32 Bid-YTW : 5.79 % |

| SLF.PR.A | Deemed-Retractible | -1.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.01 Bid-YTW : 7.37 % |

| NA.PR.W | FixedReset | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 14.71 Evaluated at bid price : 14.71 Bid-YTW : 5.30 % |

| POW.PR.D | Perpetual-Discount | -1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 21.44 Evaluated at bid price : 21.44 Bid-YTW : 5.92 % |

| TD.PR.Z | FloatingReset | 1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.97 Bid-YTW : 5.28 % |

| PWF.PR.P | FixedReset | 1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 11.50 Evaluated at bid price : 11.50 Bid-YTW : 4.91 % |

| IFC.PR.C | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.70 Bid-YTW : 9.83 % |

| TD.PF.E | FixedReset | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 18.40 Evaluated at bid price : 18.40 Bid-YTW : 4.85 % |

| TRP.PR.B | FixedReset | 1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 9.90 Evaluated at bid price : 9.90 Bid-YTW : 5.01 % |

| FTS.PR.K | FixedReset | 1.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 14.60 Evaluated at bid price : 14.60 Bid-YTW : 4.96 % |

| BMO.PR.Q | FixedReset | 1.80 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.51 Bid-YTW : 8.47 % |

| GWO.PR.O | FloatingReset | 2.73 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 11.30 Bid-YTW : 11.95 % |

| SLF.PR.H | FixedReset | 2.76 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.90 Bid-YTW : 9.90 % |

| BAM.PR.B | Floater | 3.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 9.40 Evaluated at bid price : 9.40 Bid-YTW : 5.10 % |

| HSE.PR.G | FixedReset | 3.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 15.00 Evaluated at bid price : 15.00 Bid-YTW : 7.27 % |

| HSE.PR.E | FixedReset | 4.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 15.15 Evaluated at bid price : 15.15 Bid-YTW : 7.04 % |

| TD.PR.T | FloatingReset | 4.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.00 Bid-YTW : 5.17 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PF.G | FixedReset | 190,574 | Nesbitt crossed blocks of 120,000 and 36,500, both at 25.33. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 23.26 Evaluated at bid price : 25.33 Bid-YTW : 5.22 % |

| PWF.PR.P | FixedReset | 163,503 | TD crossed blocks of 10,600 and 100,000 at 11.40, then another 50,000 at 11.45. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 11.50 Evaluated at bid price : 11.50 Bid-YTW : 4.91 % |

| BAM.PR.K | Floater | 79,400 | Scotia crossed 74,300 at 9.40. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 9.16 Evaluated at bid price : 9.16 Bid-YTW : 5.23 % |

| MFC.PR.C | Deemed-Retractible | 73,005 | RBC crossed 50,000 at 19.75. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.76 Bid-YTW : 7.80 % |

| NA.PR.X | FixedReset | 69,984 | TD crossed 25,000 at 25.11. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 23.20 Evaluated at bid price : 25.15 Bid-YTW : 5.47 % |

| PWF.PR.L | Perpetual-Discount | 59,850 | Desjardins crossed 50,000 at 22.11. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-24 Maturity Price : 21.81 Evaluated at bid price : 22.05 Bid-YTW : 5.84 % |

| There were 43 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| PWF.PR.Q | FloatingReset | Quote: 10.00 – 13.14 Spot Rate : 3.1400 Average : 2.1228 YTW SCENARIO |

| TRP.PR.F | FloatingReset | Quote: 9.96 – 10.75 Spot Rate : 0.7900 Average : 0.4949 YTW SCENARIO |

| RY.PR.C | Deemed-Retractible | Quote: 24.05 – 24.64 Spot Rate : 0.5900 Average : 0.3761 YTW SCENARIO |

| GWO.PR.I | Deemed-Retractible | Quote: 20.25 – 20.88 Spot Rate : 0.6300 Average : 0.4308 YTW SCENARIO |

| POW.PR.B | Perpetual-Discount | Quote: 23.06 – 23.60 Spot Rate : 0.5400 Average : 0.3493 YTW SCENARIO |

| HSE.PR.C | FixedReset | Quote: 13.11 – 13.69 Spot Rate : 0.5800 Average : 0.3992 YTW SCENARIO |