John Heinzl was kind enough to quote me in his piece This borrowing-to-invest strategy is no slam dunk, which discusses a couple’s proposal to take out a home-equity loan and invest the proceeds in ZPR, the BMO Laddered Preferred Share Index ETF:

If you look up ZPR’s distribution history, however, you’ll see that the monthly payout has been dropping. At the start of 2014 it was 5.3 cents, a year later it was 4.8 cents and currently it’s 4.5 cents. The reason: ZPR holds a basket of rate-reset preferred shares, many of which have cut their dividends because of a steep drop in the five-year Government of Canada bond yield that is used to set the dividends on these shares.

Barring a rebound in bond yields, ZPR’s distribution could fall even further as more rate-reset preferred shares cut their dividends, says James Hymas, president of Hymas Investment Management. Assuming the five-year Canada yield remains at its current level of about 0.8 per cent, the “implied current yield” of ZPR’s underlying portfolio is just 4.74 per cent, according to a BMO document dated April 29. After deducting the ETF’s management expense ratio of 0.5 per cent, ZPR’s net implied yield to investors is about 4.24 per cent, Mr. Hymas says.

That’s not nearly as attractive as the 5.6-per-cent yield for ZPR advertised on BMO’s website.

The document mentioned in the article is available here … for now! Hat tip to MikeFreedom49? on the Financial Wisdom Forum for bringing this document to my attention.

This is probably a good place to make two other points.

First, the document states that the duration of ZPR is 3.11 years, with a footnote indicating that:

Duration is a measure of sensitivity to changes in interest rates. For example, a 5 year duration means the value will decrease by 5% if interest rates rise 1% and increase in value by 5% if interest rates fall 1%. Generally, the higher the duration the more volatile the price will be when interest rates change.

This assertion of a 3.11 year duration without any qualifiers is irresponsible, reckless and wrong. Such an answer in the current environment can only be derived by pegging the price on the next reset date at an arbitrary level – it could be the current price, it could be $25.00, it could be anything you like, as long as it’s presumed to be a value unaffected by market yields. These are perpetual instruments trading below par; their duration in the current environment is better in the 20 to 25 year range (with respect to spreads) … or it could even be negative (if we assume yield-to-perpetuity will be constant in the face of a changing 5-year Canada rate)! . Holders of ZPR – and other FixedResets – over the past two years will doubtless be happy to confirm that the price volatility they have experienced far exceeds what they might have expected from an investment with a 3.11 year duration.

Classical bond mathematics is a very useful tool for examining preferred shares, but must be accompanied by a very cautious and explicit statement of assumptions and these assumptions should be disclosed.

Secondly, I note that BMO touts the fund as being “Low to Medium Risk”, which I feel confident will be considered laughable by those who have suffered through the woes of the preferred share market for the past two years.

The whole concept of these risk assessments, with their mandatory reporting on the “Fund Facts” statements is under constant attack by those with even a smidgen of knowledge about risk (which leaves out the regulators), so I won’t go into this further except to say I’d love to see how they justify their claim!

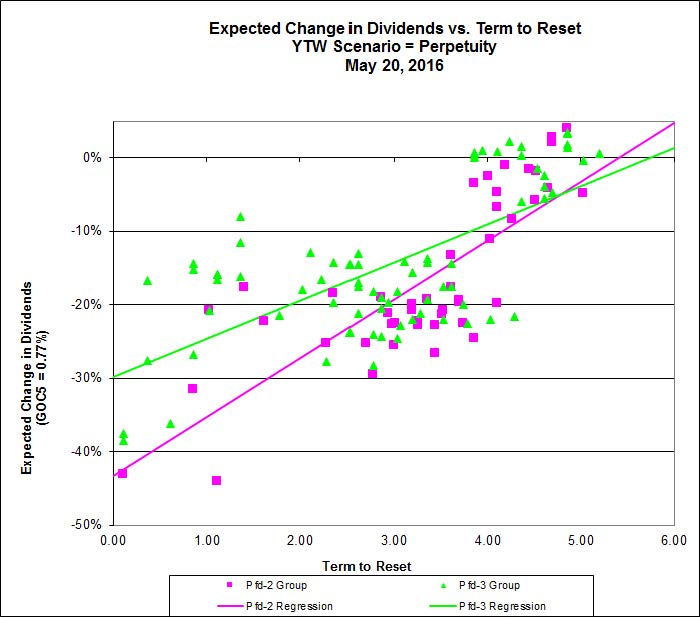

Finally, here’s a chart of expected changes in the dividends of Fixed Resets for which the YTW scenario is perpetuity, taken from the May, 2016, edition of PrefLetter:

Click for Big

I looked at the document and it is still up. It is negligence for a major firm like BMO/Nesbitt to willfully misrepresent an investment in ZPR like they have (re:duration which is clearly wrong by all measures). Good for you for showing it. You should get paid by the OSC/IDA for your work. Or maybe you should organize a class action suit? Really. I am sure their would be takers.

Banks can do whatever they like!

Click for Big

apparently, the only place you can invest risk free is at a Canadian bank GIC. what a fantastic system.

They don’t tell you, of course, that this depends on a definition of risk equivalent to ‘not losing capital’, nor that it depends on the bank not going bankrupt, or of the risk of the CDIC not being able to cover the losses if they do go bust.

These notes are just like the Lehman PPNs that were heavily sold in Hong Kong in the lead-up to the financial crisis and promptly defaulted; but this lesson is inconvenient and counter-narrative – therefore, ignored.