Capital Power Corporation has announced:

that it will issue 6,000,000 Cumulative Minimum Rate Reset Preference Shares, Series 7 (the “Series 7 Shares”) at a price of $25.00 per Series 7 Share (the “Offering”) for aggregate gross proceeds of $150 million on a bought deal basis with a syndicate of underwriters, co-led by TD Securities Inc. and CIBC Capital Markets. In addition, Capital Power has granted the underwriters an option, exercisable in whole or in part anytime up to two business days prior to closing, to purchase up to an additional 2,000,000 Series 7 Shares on the same terms, for additional gross proceeds of up to $50 million.

The Series 7 Shares will pay fixed cumulative dividends of $1.50 per share per annum, yielding 6.00% per annum, payable on the last business day of March, June, September and December of each year, as and when declared by the board of directors of Capital Power, for the initial period ending December 31, 2021. Based on an October 4, 2016 closing, the first quarterly dividend of $0.3616 per share is expected to be paid on December 30, 2016. The dividend rate will be reset on December 31, 2021 and every five years thereafter at a rate equal to the sum of the then five-year Government of Canada bond yield and 5.26%, provided that, in any event, such rate shall not be less than 6.00%. The Series 7 Shares are redeemable by Capital Power, at its option, on December 31, 2021 and every five years thereafter.

Holders of Series 7 Shares will have the right to convert all or any part of their shares into Cumulative Floating Rate Preference Shares, Series 8 (the “Series 8 Shares”), subject to certain conditions, on December 31, 2021 and every five years thereafter. Holders of Series 8 Shares will be entitled to receive a cumulative quarterly floating dividend at a rate equal to the sum of the then 90-day Government of Canada Treasury Bill yield plus 5.26%, as and when declared by the board of directors of Capital Power.

Net proceeds of the offering will be used to reduce indebtedness under Capital Power’s credit facilities.

Standard & Poor’s, a division of the McGraw Hill Companies, Inc. has assigned a provisional rating of P-3 for the Series 7 Shares and DBRS Limited has assigned a preliminary rating of Pfd-3 (low) for the Series 7 Shares.

The Series 7 Shares will be issued pursuant to a prospectus supplement to Capital Power’s short form base shelf prospectus dated May 3, 2016. This prospectus supplement will be filed with securities regulatory authorities in Canada. The Offering is subject to receipt of all necessary regulatory and stock exchange approvals.

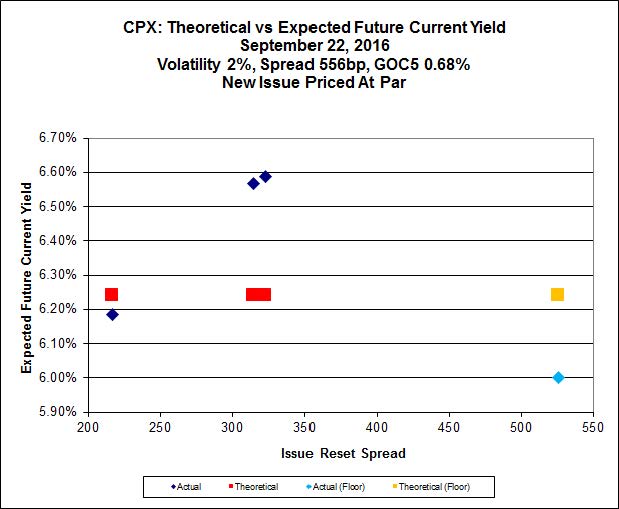

I don’t get it, frankly. This issue looks horrifically expensive. Look at the Implied Volatility analysis, for instance:

Click for Big

So look, there’s the new issue, way over on the right hand side with an Expected Future Current Yield of 6.00% – that’s the lowest of all the CPX outstanding FixedResets: CPX.PR.A, 6.18%; CPX.PR.C, 6.59%; CPX.PR.E, 6.57%.

So look, you can pick up over half a point in yield AND have lower call risk AND have increased leverage with respect to future increases in GOC-5 by buying CPX.PR.C or CPX.PR.E. These issues are even relatively liquid – relative to other junk issues – trading about $100,000-worth every day. Why wouldn’t you just buy on the secondary market?

All I can think of is:

- Liquidity: You can put a million dollars to work with one ‘phone call. Doing this on the secondary market would require you to do some work, like a peon.

- The Minimum Reset: I don’t understand how it could possibly be so valuable, but it takes two to make a market!

Hi, does it not make sense to buy a new issue preferred with a floor of 6%?. If interest rates fall, we will loose on the par the value, not in this case since we have a guaranteed floor for the yield.

Maybe you have already written about this.

Thanks.

It is quite true that if the five-year Canada yield (GOC-5) drops, we will expect a decline in future non-floored FixedReset dividends while dividends in this issue will remain constant.

From recent experience, we might infer that prices on the non-floored instruments will decline, but this is not automatic. I confess that I have been amazed at just how vigorously the income effect has been transmitted to prices over the past two years.

However, a decline in GOC-5 is not the only scenario.

If GOC-5 remains constant, the lower-coupon, higher-yielding issues should do better because they are higher yielding.

If GOC-5 increases, we can legitimately expect a rise in price in the lower-coupon issues, both due to mathematics (these issues have leverage to GOC-5, since the yield is calculated based on par value) and – less assuredly – due to a reversal of the effects of the last two years. We will not see any increase in the expected price of the new issue, because if it rises above par we have to expect a call. The call provision puts a cap on possible gains while putting no floor on possible losses.

So … do some scenario analysis with different expected values of GOC-5, assign probabilities to each GOC-5 level, calculate prices for each of the three issues in each scenario, and then combine all your numbers to find a probability distribution of prices for each issue. Have fun!

Thanks for your reply!