There has been a 10% net conversion of TA.PR.E into TA.PR.D. I have updated the linked post regarding the reset rate with this information.

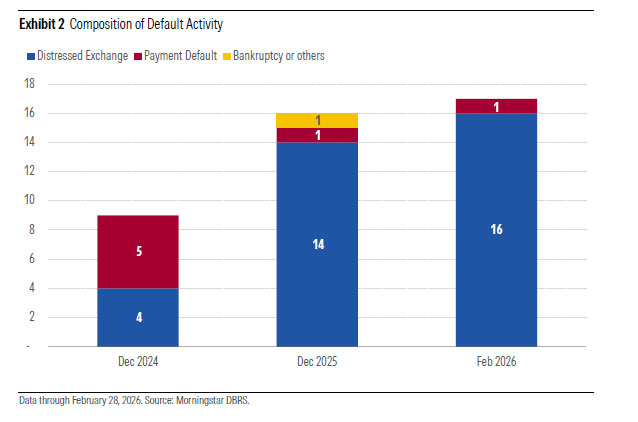

DBRS has released a commentary titled Private Credit Default Momentum Increasingly Tied to Distressed Debt Exchanges and I have tucked away a copy HERE:

Key highlights from this commentary include:

— Distressed exchange transactions now dominate default activity, primarily driven by increased use of interest deferrals as a late-stage tactic among borrowers after less severe capital support measures were attempted and were unsuccessful.

— We attribute the rise in distressed exchange situations to borrowers still struggling with declining revenue, weak operating margins, and a significant debt burden.

— We expect the recent accelerated pace of default to continue into 2026, following a 78% year-over-year increase of default events in 2025. We expect a high proportion of borrowers currently rated in the CCC through C categories to weaken further, particularly those that have relied on waivers or amendments that loosened covenant thresholds or required external capital support.

Real housing prices have been flat for about nine years:

In real, or inflation-adjusted terms, the benchmark national home price has fallen by close to 30 per cent from its peak, bringing home prices back to the inflation-adjusted level of nine years ago.

…

As is often said, there is no national housing market, and the differences that exist between some Canadian markets are even more extreme in real terms. Prices in Quebec in February, for instance, hit an all-time high.Meanwhile, in Alberta the inflation-adjusted benchmark price sat roughly where it was a decade earlier, having generally flatlined for most of that time. The typical home in Greater Vancouver has also endured a lost decade after accounting for the corrosive effect of inflation on prices.

Ontario home prices have suffered some of the steepest real declines from the 2022 peak, however, even if prices haven’t touched decade-ago lows, with the typical home in Greater Toronto shedding more than one-third of its value since the peak.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.6960 % | 2,463.4 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.6960 % | 4,671.0 |

| Floater | 5.85 % | 6.02 % | 53,122 | 13.93 | 3 | -0.6960 % | 2,691.9 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 3,680.9 |

| SplitShare | 4.74 % | 3.48 % | 80,010 | 0.92 | 5 | 0.0000 % | 4,395.7 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 3,429.7 |

| Perpetual-Premium | 5.71 % | 5.81 % | 72,495 | 14.06 | 7 | -0.1704 % | 3,065.5 |

| Perpetual-Discount | 5.66 % | 5.75 % | 45,047 | 14.23 | 28 | -0.7469 % | 3,341.6 |

| FixedReset Disc | 5.90 % | 6.05 % | 118,365 | 13.77 | 27 | -0.4237 % | 3,191.5 |

| Insurance Straight | 5.59 % | 5.63 % | 62,433 | 14.50 | 22 | -0.7467 % | 3,251.1 |

| FloatingReset | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.4237 % | 3,796.6 |

| FixedReset Prem | 5.98 % | 4.68 % | 87,439 | 2.42 | 21 | -0.0733 % | 2,652.6 |

| FixedReset Bank Non | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.4237 % | 3,262.3 |

| FixedReset Ins Non | 5.29 % | 5.47 % | 87,545 | 14.26 | 14 | -0.0614 % | 3,124.5 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| CU.PR.F | Perpetual-Discount | -3.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 19.70 Evaluated at bid price : 19.70 Bid-YTW : 5.77 % |

| MFC.PR.C | Insurance Straight | -2.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 21.06 Evaluated at bid price : 21.06 Bid-YTW : 5.38 % |

| PWF.PR.S | Perpetual-Discount | -2.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 21.25 Evaluated at bid price : 21.25 Bid-YTW : 5.74 % |

| POW.PR.D | Perpetual-Discount | -2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 22.28 Evaluated at bid price : 22.55 Bid-YTW : 5.63 % |

| GWO.PR.G | Insurance Straight | -1.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 22.77 Evaluated at bid price : 23.05 Bid-YTW : 5.65 % |

| SLF.PR.E | Insurance Straight | -1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 21.14 Evaluated at bid price : 21.14 Bid-YTW : 5.34 % |

| BN.PR.B | Floater | -1.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 12.81 Evaluated at bid price : 12.81 Bid-YTW : 6.11 % |

| SLF.PR.C | Insurance Straight | -1.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 21.11 Evaluated at bid price : 21.11 Bid-YTW : 5.29 % |

| ENB.PF.G | FixedReset Disc | -1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 22.24 Evaluated at bid price : 22.89 Bid-YTW : 6.28 % |

| SLF.PR.D | Insurance Straight | -1.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 20.95 Evaluated at bid price : 20.95 Bid-YTW : 5.33 % |

| GWO.PR.L | Insurance Straight | -1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 24.23 Evaluated at bid price : 24.52 Bid-YTW : 5.77 % |

| BN.PF.E | FixedReset Disc | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 22.49 Evaluated at bid price : 23.26 Bid-YTW : 5.91 % |

| GWO.PR.R | Insurance Straight | -1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 21.36 Evaluated at bid price : 21.36 Bid-YTW : 5.64 % |

| ENB.PR.F | FixedReset Disc | -1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 22.16 Evaluated at bid price : 22.44 Bid-YTW : 6.26 % |

| BN.PR.N | Perpetual-Discount | -1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 20.06 Evaluated at bid price : 20.06 Bid-YTW : 5.95 % |

| GWO.PR.I | Insurance Straight | -1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 20.43 Evaluated at bid price : 20.43 Bid-YTW : 5.53 % |

| PWF.PR.F | Perpetual-Discount | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 22.66 Evaluated at bid price : 22.90 Bid-YTW : 5.81 % |

| ENB.PR.J | FixedReset Disc | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 22.56 Evaluated at bid price : 23.20 Bid-YTW : 6.19 % |

| GWO.PR.P | Insurance Straight | -1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 23.33 Evaluated at bid price : 23.62 Bid-YTW : 5.73 % |

| ENB.PR.Y | FixedReset Disc | -1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 21.34 Evaluated at bid price : 21.65 Bid-YTW : 6.30 % |

| MFC.PR.B | Insurance Straight | -1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 21.44 Evaluated at bid price : 21.70 Bid-YTW : 5.38 % |

| GWO.PR.H | Insurance Straight | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 21.47 Evaluated at bid price : 21.47 Bid-YTW : 5.67 % |

| BN.PF.B | FixedReset Disc | -1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 23.19 Evaluated at bid price : 24.50 Bid-YTW : 5.86 % |

| CU.PR.J | Perpetual-Discount | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 5.71 % |

| CIU.PR.A | Perpetual-Discount | 1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 20.55 Evaluated at bid price : 20.55 Bid-YTW : 5.65 % |

| GWO.PR.S | Insurance Straight | 2.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 21.81 Evaluated at bid price : 22.05 Bid-YTW : 5.97 % |

| ENB.PF.C | FixedReset Disc | 3.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 22.29 Evaluated at bid price : 22.90 Bid-YTW : 6.21 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| ENB.PR.P | FixedReset Disc | 293,462 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 22.56 Evaluated at bid price : 23.20 Bid-YTW : 6.11 % |

| GWO.PR.H | Insurance Straight | 142,582 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 21.47 Evaluated at bid price : 21.47 Bid-YTW : 5.67 % |

| POW.PR.D | Perpetual-Discount | 48,875 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 22.28 Evaluated at bid price : 22.55 Bid-YTW : 5.63 % |

| SLF.PR.C | Insurance Straight | 46,610 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-19 Maturity Price : 21.11 Evaluated at bid price : 21.11 Bid-YTW : 5.29 % |

| BN.PF.J | FixedReset Prem | 43,325 | YTW SCENARIO Maturity Type : Call Maturity Date : 2027-12-31 Maturity Price : 25.00 Evaluated at bid price : 25.50 Bid-YTW : 4.95 % |

| BN.PF.M | FixedReset Prem | 28,740 | YTW SCENARIO Maturity Type : Call Maturity Date : 2031-01-01 Maturity Price : 25.00 Evaluated at bid price : 26.25 Bid-YTW : 4.46 % |

| There were 9 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| See TMX DataLinx: ‘Last’ != ‘Close’ and the posts linked therein for an idea of why these quotes are so horrible. | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.F | FixedReset Ins Non | Quote: 19.35 – 23.80 Spot Rate : 4.4500 Average : 2.4140 YTW SCENARIO |

| GWO.PR.M | Insurance Straight | Quote: 23.90 – 25.50 Spot Rate : 1.6000 Average : 1.2809 YTW SCENARIO |

| MFC.PR.J | FixedReset Ins Non | Quote: 25.46 – 26.15 Spot Rate : 0.6900 Average : 0.4324 YTW SCENARIO |

| CU.PR.F | Perpetual-Discount | Quote: 19.70 – 20.70 Spot Rate : 1.0000 Average : 0.7771 YTW SCENARIO |

| GWO.PR.L | Insurance Straight | Quote: 24.52 – 25.05 Spot Rate : 0.5300 Average : 0.3265 YTW SCENARIO |

| PVS.PR.J | SplitShare | Quote: 25.25 – 26.00 Spot Rate : 0.7500 Average : 0.5499 YTW SCENARIO |