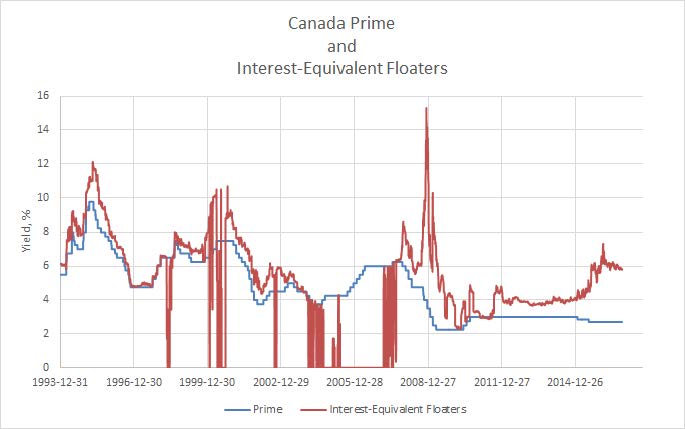

In response to overwhelming public demand (SafetyinNumbers asked me), I present a chart of Canada Prime and the interest-equivalent yield of Floaters.

Click for Big

There are problems with this chart:

- Often, Floaters have traded above their contemporary call price. When this has happened I have set the interest-equivalent yield to zero.

- In late years, the Floater index has been dominated by BAM issues, which often trade differently from the market as a whole due to credit worries and investor concentration concerns.

- In later years, PWF.PR.A has drifted in and out of the index, relegated intermittently to Scraps on volume concerns. As PWF.PR.A has a significantly lower yield than the BAM Floaters, this creates inconsistencies when comparing one period to another.

- At the beginning of February, 2011, I abruptly changed the interest-equivalency factor from 1.4x to 1.3x

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0680 % | 1,750.0 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0680 % | 3,196.8 |

| Floater | 4.28 % | 4.45 % | 47,922 | 16.44 | 4 | 0.0680 % | 1,842.4 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2847 % | 2,911.5 |

| SplitShare | 4.85 % | 4.30 % | 52,565 | 2.02 | 6 | -0.2847 % | 3,476.9 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2847 % | 2,712.8 |

| Perpetual-Premium | 5.45 % | 5.08 % | 78,671 | 14.41 | 23 | -0.2058 % | 2,653.8 |

| Perpetual-Discount | 5.41 % | 5.37 % | 91,538 | 14.82 | 15 | 0.0000 % | 2,772.0 |

| FixedReset | 4.90 % | 4.61 % | 207,126 | 6.81 | 96 | 0.1275 % | 2,083.1 |

| Deemed-Retractible | 5.14 % | 5.31 % | 136,327 | 4.51 | 32 | -0.1664 % | 2,748.1 |

| FloatingReset | 2.87 % | 3.65 % | 42,493 | 4.87 | 12 | 0.0678 % | 2,309.6 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| CCS.PR.C | Deemed-Retractible | -1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.21 Bid-YTW : 6.29 % |

| VNR.PR.A | FixedReset | -1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-24 Maturity Price : 18.90 Evaluated at bid price : 18.90 Bid-YTW : 5.12 % |

| PWF.PR.E | Perpetual-Premium | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-24 Maturity Price : 24.34 Evaluated at bid price : 24.65 Bid-YTW : 5.63 % |

| PWF.PR.P | FixedReset | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-24 Maturity Price : 13.62 Evaluated at bid price : 13.62 Bid-YTW : 4.67 % |

| TRP.PR.C | FixedReset | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-24 Maturity Price : 13.29 Evaluated at bid price : 13.29 Bid-YTW : 4.68 % |

| BAM.PR.Z | FixedReset | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-24 Maturity Price : 19.56 Evaluated at bid price : 19.56 Bid-YTW : 5.21 % |

| MFC.PR.F | FixedReset | 1.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.65 Bid-YTW : 10.73 % |

| TRP.PR.A | FixedReset | 1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-24 Maturity Price : 15.75 Evaluated at bid price : 15.75 Bid-YTW : 4.78 % |

| TRP.PR.F | FloatingReset | 1.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-24 Maturity Price : 14.95 Evaluated at bid price : 14.95 Bid-YTW : 4.11 % |

| TRP.PR.H | FloatingReset | 2.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-24 Maturity Price : 11.31 Evaluated at bid price : 11.31 Bid-YTW : 4.00 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TRP.PR.K | FixedReset | 377,038 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-24 Maturity Price : 23.10 Evaluated at bid price : 24.91 Bid-YTW : 4.84 % |

| TRP.PR.G | FixedReset | 237,996 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-24 Maturity Price : 20.21 Evaluated at bid price : 20.21 Bid-YTW : 4.86 % |

| MFC.PR.R | FixedReset | 203,300 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.99 Bid-YTW : 4.87 % |

| TD.PF.H | FixedReset | 198,328 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-10-31 Maturity Price : 25.00 Evaluated at bid price : 25.52 Bid-YTW : 4.51 % |

| TD.PF.B | FixedReset | 118,600 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-24 Maturity Price : 18.60 Evaluated at bid price : 18.60 Bid-YTW : 4.52 % |

| TRP.PR.E | FixedReset | 113,321 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-24 Maturity Price : 18.35 Evaluated at bid price : 18.35 Bid-YTW : 4.79 % |

| There were 45 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| IFC.PR.D | FloatingReset | Quote: 19.25 – 22.00 Spot Rate : 2.7500 Average : 2.1856 YTW SCENARIO |

| PWF.PR.E | Perpetual-Premium | Quote: 24.65 – 24.94 Spot Rate : 0.2900 Average : 0.1878 YTW SCENARIO |

| SLF.PR.C | Deemed-Retractible | Quote: 21.16 – 21.45 Spot Rate : 0.2900 Average : 0.1980 YTW SCENARIO |

| TD.PR.Z | FloatingReset | Quote: 23.23 – 23.55 Spot Rate : 0.3200 Average : 0.2281 YTW SCENARIO |

| TD.PR.S | FixedReset | Quote: 23.99 – 24.24 Spot Rate : 0.2500 Average : 0.1807 YTW SCENARIO |

| TD.PR.Y | FixedReset | Quote: 24.16 – 24.39 Spot Rate : 0.2300 Average : 0.1638 YTW SCENARIO |

Thanks! It will be interesting to see if there is some compression between the yield of the floaters and the prime rate if interest rates in Canada follow the US. Of course, higher dividends and a lower/same yield could make for some nice capital gains. But the opposite could always happen too!