Click for Big

Brace yourself for staggering unemployment numbers:

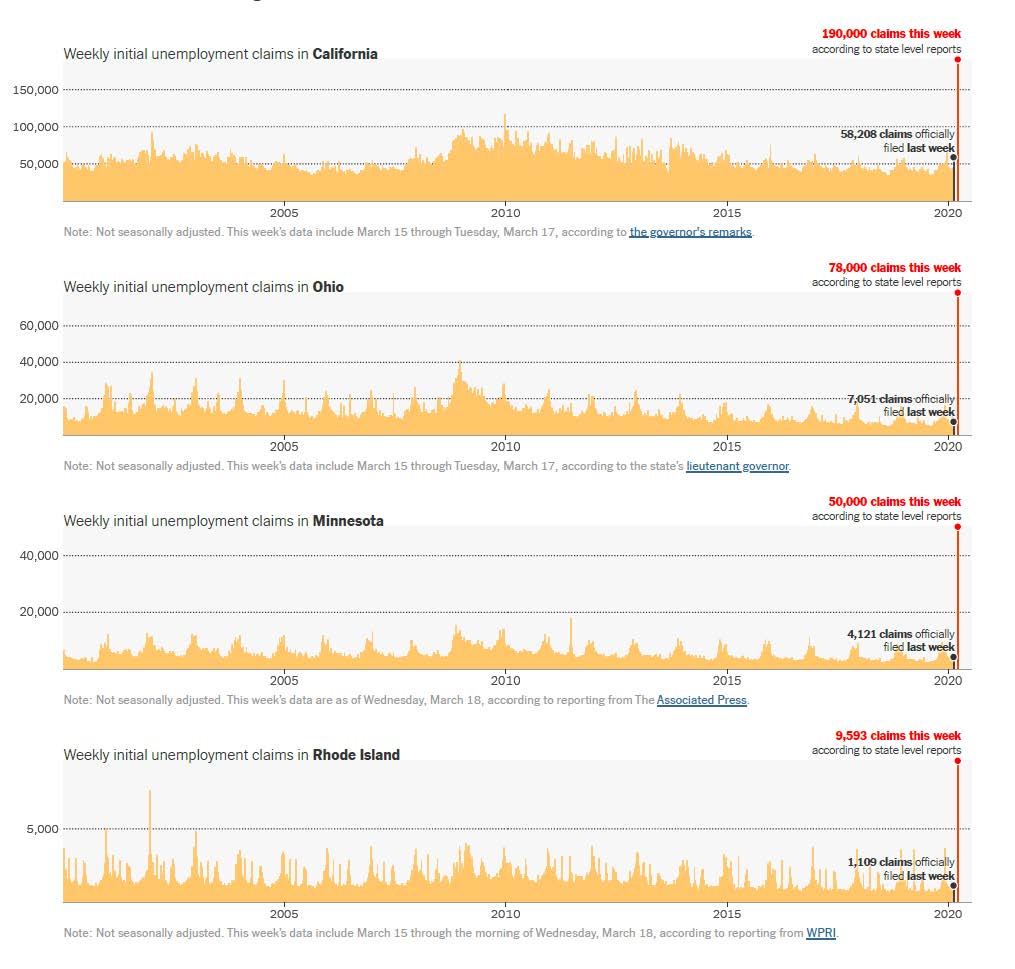

Numbers released on Thursday by the Labor Department — as well as a preliminary analysis of even more recent data — provide the first hard confirmation that the new coronavirus is bringing the United States economy to a shuddering halt. The government reported that the number of initial unemployment claims rose to 281,000 last week, a sharp rise from 211,000 the previous week. This rise in initial claims of 70,000 is larger than any week-to-week movement that occurred during (or since) the 2008 financial crisis.

But even these numbers understate the economy’s free fall, as they reflect the state of the economy last week. Based on preliminary news reports this week from 15 states, it’s already clear that initial claims will skyrocket next week, most likely to levels never seen before.

…

Although Washington has not revealed the most recent official figures, state officials said that claims increased 150 percent last week and that the state was seeing an “even more dramatic increase this week.” They also mentioned that call volume surged more than eightfold on Tuesday.As the accompanying charts show, jobless claims rose sharply in the vast majority of states. These figures come from state unemployment insurance offices tallying up the number of people newly applying for unemployment benefits.

Click for Big

DBRS downgraded Alberta:

DBRS Morningstar downgraded the Province of Alberta’s Issuer Rating and Long-Term Debt rating to AA (low) from AA and its Short-Term Debt rating to R-1 (middle) from R-1 (high). In addition, DBRS Morningstar changed the trend on the Province of Alberta’s Short-Term Debt to Stable from Negative. DBRS Morningstar also downgraded the Alberta Capital Finance Authority’s Long-Term Obligations rating to AA (low). The trends on all Issuer Rating and Long-Term Debt ratings are Negative.

…

DBRS Morningstar believes that Alberta’s credit profile is no longer consistent with a AA rating and that risks remain firmly tilted toward the downside; as a result, DBRS Morningstar has maintained the Negative trend on Alberta’s Issuer Rating and Long-Term debt rating. Current economic conditions and actions taken by Saudi Arabian and Russian governments suggest that oil prices will be under pressure for the foreseeable future, which will have a significant and adverse impact on Alberta’s economic activity and government revenue. This will likely drive debt ratios significantly higher in the near to medium term.DBRS Morningstar has estimated possible impacts using Alberta’s 2020 Budget, released in late February 2020. DBRS Morningstar estimates that the 2020–21 deficit (on an adjusted basis) may exceed 4.0% of GDP and that the adjusted debt-to-GDP ratio may rise above 30% in 2020–21 alone. Notwithstanding these estimates, there is uncertainty with respect to the current situation and Alberta has yet to outline a full fiscal policy response.

Yesterday I mentioned the problem of bond ETFs and inverted liquidity and, right on cue, I got a call from a client worried about his holdings in VCSH – Vanguard Short-Term Corporate Bond ETF. Holy smokes, look at that price chart!

Click for Big

When I looked into this, I found another Reuters article with a bit more colour:

For the iShares iBoxx Investment Grade Corporate Bond ETF , that has created the widest gap between the price at which it trades and the underlying value of the assets – known as net asset value. LQD on Thursday traded at a nearly 5% discount to its net asset value, the widest spread since 2008.

…

That has meant that corporate bonds are traded less, and when they are, the difference between bid and ask prices are wider. But the ETFs that track those bonds have had less trouble trading. The harder the asset is to trade, the greater the price dislocation.The problem seems to be in investment grade debt at the moment rather than in high yield. Two major high-yield bond ETFs saw spreads between their trade price and net asset value widen, but far less dramatically than in LQD. (Reporting by Kate Duguid Editing by Marguerita Choy)

Fortunately, I was able to refer my client to the VCSH website which contained the information that although VCSH closed 3/19 at 71.75, down 2.55 (!), its NAVPU as of 3/18 was 77.79, implying it was trading at a 4.5% discount to NAV. Incredible.

What’s more, I understand this fund is actually bringing in money:

Looking today at week-over-week shares outstanding changes among the universe of ETFs covered at ETF Channel, one standout is the Vanguard Short-Term Corporate Bond ETF (Symbol: VCSH) where we have detected an approximate $408.0 million dollar inflow — that’s a 1.8% increase week over week in outstanding units (from 303,016,326 to 308,330,856).

… but its growth is an exception:

BlackRock’s exchange-traded fund focused on investment-grade corporate bonds has seen big price declines. The net asset value of iShares iBoxx $ Investment Grade Corporate Bond ETF, which trades under the ticker LQD, dropped 5 percent on March 18. Its shares continued to fall Thursday.

The steep price declines of the ETF over the past few days resemble the massive drop seen in a similarly short period during the financial crisis, the Bank of America report shows. A downward spiraling effect is at play, with investors fearing corporate cash flows will dwindle as the escalating coronavirus crisis halts economic activity.

…

The billions of dollars in outflows from U.S. investment-grade corporate debt funds and ETFs in each of the past few days reached record levels, according to the Bank of America report. During the financial crisis, investment-grade bond funds and ETFs lost 3.7 percent of assets over two months, which the strategists estimated would be $133 billion based on today’s assets under management.

The VCSH fact sheet indicates that all the bonds are investment grade – although I bet that a few downgrades are pending!

Fortunately for shareholders, the fund’s prospectus indicates:

ETF Shares of the Fund cannot be directly purchased from or redeemed with the Fund, except by certain authorized broker-dealers. These broker-dealers may purchase and redeem ETF Shares only in large blocks (Creation Units), typically in exchange for baskets of securities.

… which offers some measure of protection for shareholders … the fund doesn’t have to sell securities at garbage prices to fund redemptions, all that risk is borne by the market-makers who, presumably, are currently having a hell of a time right now.

It’s a wild world; I fear that are a lot of people making some very bad decisions right now; although the nature of markets demands that other people are making some very good ones, as the rich get richer.

TXPR closed at 410.23, up 1.96% on the day. Volume today was 5.35-million, fourth-highest of the past 30 trading days.

Today’s rally means the total return version of this index is down only 13.33% from last Friday, so it looks like a pretty good week!

CPD closed at 8.22, up 3.27% on the day. Volume of 183,495 was … oh, I don’t know, around the median of the past 30 trading days.

ZPR closed at 6.38, up 1.59% on the day. Volume of 764,911 was pretty low in the context of the past two weeks.

Five-year Canada yields were down 6bp to 0.86% today.

I’m not reviewing suspect quotes today, as has been the case for the past while. I’m saving my sarcasm for less turbulent times.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 4.1604 % | 1,234.9 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 4.1604 % | 2,265.9 |

| Floater | 8.77 % | 8.78 % | 75,758 | 10.64 | 4 | 4.1604 % | 1,305.9 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 3.2699 % | 2,818.1 |

| SplitShare | 5.89 % | 10.59 % | 76,481 | 3.87 | 7 | 3.2699 % | 3,365.4 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 3.2699 % | 2,625.8 |

| Perpetual-Premium | 7.47 % | 7.78 % | 100,623 | 11.53 | 12 | 8.3465 % | 2,281.1 |

| Perpetual-Discount | 6.95 % | 6.95 % | 84,397 | 12.61 | 24 | 2.8266 % | 2,521.5 |

| FixedReset Disc | 9.01 % | 7.91 % | 214,129 | 11.11 | 64 | 3.5069 % | 1,338.4 |

| Deemed-Retractible | 6.77 % | 7.49 % | 97,916 | 12.01 | 27 | 7.2355 % | 2,496.0 |

| FloatingReset | 6.49 % | 6.64 % | 65,721 | 12.93 | 3 | 1.9383 % | 1,449.7 |

| FixedReset Prem | 7.15 % | 7.20 % | 190,263 | 12.31 | 22 | 0.4592 % | 1,895.5 |

| FixedReset Bank Non | 2.29 % | 14.86 % | 114,627 | 1.76 | 3 | 4.9139 % | 2,320.3 |

| FixedReset Ins Non | 9.04 % | 8.33 % | 121,605 | 10.98 | 22 | 2.9140 % | 1,307.4 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| MFC.PR.M | FixedReset Ins Non | -10.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 8.97 Evaluated at bid price : 8.97 Bid-YTW : 9.65 % |

| HSE.PR.C | FixedReset Disc | -6.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 6.76 Evaluated at bid price : 6.76 Bid-YTW : 16.27 % |

| BAM.PF.H | FixedReset Prem | -5.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 17.40 Evaluated at bid price : 17.40 Bid-YTW : 7.24 % |

| TRP.PR.K | FixedReset Prem | -4.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 6.89 % |

| HSE.PR.E | FixedReset Disc | -4.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 6.70 Evaluated at bid price : 6.70 Bid-YTW : 16.70 % |

| SLF.PR.J | FloatingReset | -3.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 7.21 Evaluated at bid price : 7.21 Bid-YTW : 6.15 % |

| TD.PF.G | FixedReset Prem | -3.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 19.50 Evaluated at bid price : 19.50 Bid-YTW : 7.19 % |

| ELF.PR.G | Perpetual-Discount | -3.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 16.61 Evaluated at bid price : 16.61 Bid-YTW : 7.31 % |

| PWF.PR.A | Floater | -2.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 6.80 Evaluated at bid price : 6.80 Bid-YTW : 9.05 % |

| TRP.PR.J | FixedReset Prem | -2.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 20.33 Evaluated at bid price : 20.33 Bid-YTW : 6.89 % |

| BMO.PR.Z | Perpetual-Discount | -2.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 19.50 Evaluated at bid price : 19.50 Bid-YTW : 6.49 % |

| PVS.PR.D | SplitShare | -2.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2021-10-08 Maturity Price : 25.00 Evaluated at bid price : 22.01 Bid-YTW : 13.45 % |

| EMA.PR.H | FixedReset Prem | -2.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 21.42 Evaluated at bid price : 21.75 Bid-YTW : 5.69 % |

| NA.PR.C | FixedReset Disc | -1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 12.85 Evaluated at bid price : 12.85 Bid-YTW : 8.54 % |

| BIP.PR.A | FixedReset Disc | -1.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 10.46 Evaluated at bid price : 10.46 Bid-YTW : 10.61 % |

| TD.PF.I | FixedReset Disc | -1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 13.31 Evaluated at bid price : 13.31 Bid-YTW : 7.62 % |

| BAM.PF.I | FixedReset Prem | -1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 16.75 Evaluated at bid price : 16.75 Bid-YTW : 7.21 % |

| BIK.PR.A | FixedReset Prem | -1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 8.67 % |

| BMO.PR.C | FixedReset Disc | -1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 14.61 Evaluated at bid price : 14.61 Bid-YTW : 7.33 % |

| SLF.PR.H | FixedReset Ins Non | -1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 9.53 Evaluated at bid price : 9.53 Bid-YTW : 7.90 % |

| RY.PR.Q | FixedReset Prem | -1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 19.50 Evaluated at bid price : 19.50 Bid-YTW : 6.99 % |

| BMO.PR.D | FixedReset Disc | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 14.04 Evaluated at bid price : 14.04 Bid-YTW : 7.36 % |

| CM.PR.R | FixedReset Disc | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 13.10 Evaluated at bid price : 13.10 Bid-YTW : 8.31 % |

| PVS.PR.F | SplitShare | -1.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2024-09-30 Maturity Price : 25.00 Evaluated at bid price : 18.31 Bid-YTW : 12.90 % |

| RY.PR.E | Deemed-Retractible | 1.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.85 Bid-YTW : 9.88 % |

| RY.PR.F | Deemed-Retractible | 1.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.70 Bid-YTW : 10.21 % |

| TD.PF.A | FixedReset Disc | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 10.73 Evaluated at bid price : 10.73 Bid-YTW : 7.78 % |

| EML.PR.A | FixedReset Ins Non | 1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 17.20 Evaluated at bid price : 17.20 Bid-YTW : 8.49 % |

| EIT.PR.A | SplitShare | 1.18 % | YTW SCENARIO Maturity Type : Soft Maturity Maturity Date : 2024-03-14 Maturity Price : 25.00 Evaluated at bid price : 22.31 Bid-YTW : 8.07 % |

| EMA.PR.E | Perpetual-Discount | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 17.72 Evaluated at bid price : 17.72 Bid-YTW : 6.43 % |

| RY.PR.J | FixedReset Disc | 1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 12.87 Evaluated at bid price : 12.87 Bid-YTW : 7.05 % |

| CU.PR.E | Perpetual-Discount | 1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 6.70 % |

| RY.PR.A | Deemed-Retractible | 1.37 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.88 Bid-YTW : 9.75 % |

| NA.PR.S | FixedReset Disc | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 10.30 Evaluated at bid price : 10.30 Bid-YTW : 8.62 % |

| IAF.PR.I | FixedReset Ins Non | 1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 11.71 Evaluated at bid price : 11.71 Bid-YTW : 8.29 % |

| IFC.PR.C | FixedReset Ins Non | 1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 10.75 Evaluated at bid price : 10.75 Bid-YTW : 8.15 % |

| IFC.PR.F | Deemed-Retractible | 1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 17.75 Evaluated at bid price : 17.75 Bid-YTW : 7.51 % |

| RY.PR.C | Deemed-Retractible | 1.46 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.93 Bid-YTW : 9.79 % |

| NA.PR.A | FixedReset Prem | 1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 17.25 Evaluated at bid price : 17.25 Bid-YTW : 8.10 % |

| MFC.PR.H | FixedReset Ins Non | 1.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 11.27 Evaluated at bid price : 11.27 Bid-YTW : 9.02 % |

| BMO.PR.Y | FixedReset Disc | 1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 12.37 Evaluated at bid price : 12.37 Bid-YTW : 7.29 % |

| MFC.PR.O | FixedReset Ins Non | 1.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 17.55 Evaluated at bid price : 17.55 Bid-YTW : 8.33 % |

| CM.PR.Q | FixedReset Disc | 1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 11.00 Evaluated at bid price : 11.00 Bid-YTW : 8.43 % |

| TD.PF.L | FixedReset Disc | 1.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 14.86 Evaluated at bid price : 14.86 Bid-YTW : 7.60 % |

| BNS.PR.G | FixedReset Prem | 1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 20.46 Evaluated at bid price : 20.46 Bid-YTW : 6.92 % |

| BAM.PR.R | FixedReset Disc | 1.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 9.06 Evaluated at bid price : 9.06 Bid-YTW : 8.70 % |

| PWF.PR.S | Perpetual-Discount | 1.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 15.79 Evaluated at bid price : 15.79 Bid-YTW : 7.76 % |

| BMO.PR.S | FixedReset Disc | 1.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 10.80 Evaluated at bid price : 10.80 Bid-YTW : 7.93 % |

| BMO.PR.W | FixedReset Disc | 1.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 10.80 Evaluated at bid price : 10.80 Bid-YTW : 7.79 % |

| BMO.PR.Q | FixedReset Bank Non | 1.89 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.38 Bid-YTW : 16.40 % |

| MFC.PR.L | FixedReset Ins Non | 2.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 9.55 Evaluated at bid price : 9.55 Bid-YTW : 8.58 % |

| CIU.PR.A | Perpetual-Discount | 2.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 16.76 Evaluated at bid price : 16.76 Bid-YTW : 6.95 % |

| TD.PF.F | Perpetual-Discount | 2.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 20.00 Evaluated at bid price : 20.00 Bid-YTW : 6.23 % |

| NA.PR.W | FixedReset Disc | 2.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 10.22 Evaluated at bid price : 10.22 Bid-YTW : 8.36 % |

| BNS.PR.Y | FixedReset Bank Non | 2.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.70 Bid-YTW : 7.36 % |

| TD.PF.C | FixedReset Disc | 2.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 11.15 Evaluated at bid price : 11.15 Bid-YTW : 7.71 % |

| MFC.PR.G | FixedReset Ins Non | 2.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 10.64 Evaluated at bid price : 10.64 Bid-YTW : 8.93 % |

| HSE.PR.A | FixedReset Disc | 2.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 4.31 Evaluated at bid price : 4.31 Bid-YTW : 15.00 % |

| BMO.PR.E | FixedReset Disc | 2.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 13.37 Evaluated at bid price : 13.37 Bid-YTW : 7.31 % |

| BAM.PF.J | FixedReset Prem | 2.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 16.65 Evaluated at bid price : 16.65 Bid-YTW : 7.18 % |

| RY.PR.W | Perpetual-Discount | 2.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 20.50 Evaluated at bid price : 20.50 Bid-YTW : 6.05 % |

| BNS.PR.I | FixedReset Disc | 2.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 13.54 Evaluated at bid price : 13.54 Bid-YTW : 6.93 % |

| CU.PR.I | FixedReset Prem | 2.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 19.51 Evaluated at bid price : 19.51 Bid-YTW : 5.87 % |

| PWF.PR.L | Perpetual-Discount | 2.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 16.28 Evaluated at bid price : 16.28 Bid-YTW : 8.00 % |

| TD.PF.B | FixedReset Disc | 2.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 10.95 Evaluated at bid price : 10.95 Bid-YTW : 7.65 % |

| EIT.PR.B | SplitShare | 2.77 % | YTW SCENARIO Maturity Type : Soft Maturity Maturity Date : 2025-03-14 Maturity Price : 25.00 Evaluated at bid price : 22.25 Bid-YTW : 7.54 % |

| RY.PR.S | FixedReset Disc | 2.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 13.67 Evaluated at bid price : 13.67 Bid-YTW : 6.72 % |

| CM.PR.O | FixedReset Disc | 2.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 10.30 Evaluated at bid price : 10.30 Bid-YTW : 8.30 % |

| RY.PR.M | FixedReset Disc | 2.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 11.98 Evaluated at bid price : 11.98 Bid-YTW : 7.34 % |

| PWF.PR.O | Perpetual-Premium | 2.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 18.10 Evaluated at bid price : 18.10 Bid-YTW : 8.19 % |

| PVS.PR.H | SplitShare | 2.86 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2027-02-28 Maturity Price : 25.00 Evaluated at bid price : 18.00 Bid-YTW : 10.59 % |

| NA.PR.E | FixedReset Disc | 2.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 11.50 Evaluated at bid price : 11.50 Bid-YTW : 8.19 % |

| RY.PR.Z | FixedReset Disc | 3.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 10.96 Evaluated at bid price : 10.96 Bid-YTW : 7.49 % |

| TD.PF.M | FixedReset Disc | 3.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 15.97 Evaluated at bid price : 15.97 Bid-YTW : 7.36 % |

| EMA.PR.F | FixedReset Disc | 3.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 11.85 Evaluated at bid price : 11.85 Bid-YTW : 7.98 % |

| BAM.PR.N | Perpetual-Discount | 3.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 15.84 Evaluated at bid price : 15.84 Bid-YTW : 7.54 % |

| RY.PR.P | Perpetual-Premium | 3.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 20.95 Evaluated at bid price : 20.95 Bid-YTW : 6.35 % |

| BAM.PF.C | Perpetual-Discount | 3.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 16.17 Evaluated at bid price : 16.17 Bid-YTW : 7.55 % |

| BIP.PR.D | FixedReset Disc | 3.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 15.91 Evaluated at bid price : 15.91 Bid-YTW : 7.91 % |

| MFC.PR.R | FixedReset Ins Non | 3.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 13.70 Evaluated at bid price : 13.70 Bid-YTW : 8.66 % |

| BAM.PR.M | Perpetual-Discount | 3.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 15.86 Evaluated at bid price : 15.86 Bid-YTW : 7.54 % |

| CM.PR.P | FixedReset Disc | 3.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 10.60 Evaluated at bid price : 10.60 Bid-YTW : 8.15 % |

| TRP.PR.E | FixedReset Disc | 3.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 9.85 Evaluated at bid price : 9.85 Bid-YTW : 8.80 % |

| RY.PR.H | FixedReset Disc | 3.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 11.33 Evaluated at bid price : 11.33 Bid-YTW : 7.31 % |

| BAM.PR.Z | FixedReset Disc | 3.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 11.90 Evaluated at bid price : 11.90 Bid-YTW : 8.43 % |

| PWF.PR.R | Perpetual-Premium | 3.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 17.63 Evaluated at bid price : 17.63 Bid-YTW : 7.97 % |

| PVS.PR.E | SplitShare | 3.66 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-10-31 Maturity Price : 25.00 Evaluated at bid price : 21.25 Bid-YTW : 12.56 % |

| IFC.PR.I | Perpetual-Premium | 3.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 18.15 Evaluated at bid price : 18.15 Bid-YTW : 7.56 % |

| BIP.PR.E | FixedReset Disc | 3.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 15.30 Evaluated at bid price : 15.30 Bid-YTW : 8.23 % |

| CU.PR.D | Perpetual-Discount | 3.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 6.61 % |

| IFC.PR.G | FixedReset Ins Non | 3.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 12.20 Evaluated at bid price : 12.20 Bid-YTW : 7.70 % |

| PWF.PR.H | Perpetual-Premium | 3.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 18.49 Evaluated at bid price : 18.49 Bid-YTW : 7.94 % |

| TD.PF.E | FixedReset Disc | 3.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 12.90 Evaluated at bid price : 12.90 Bid-YTW : 7.33 % |

| CM.PR.S | FixedReset Disc | 3.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 11.50 Evaluated at bid price : 11.50 Bid-YTW : 7.93 % |

| POW.PR.G | Perpetual-Premium | 4.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 17.89 Evaluated at bid price : 17.89 Bid-YTW : 8.02 % |

| BMO.PR.F | FixedReset Disc | 4.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 15.75 Evaluated at bid price : 15.75 Bid-YTW : 7.35 % |

| NA.PR.G | FixedReset Disc | 4.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 12.25 Evaluated at bid price : 12.25 Bid-YTW : 8.26 % |

| TRP.PR.G | FixedReset Disc | 4.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 11.38 Evaluated at bid price : 11.38 Bid-YTW : 8.48 % |

| IFC.PR.A | FixedReset Ins Non | 4.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 8.98 Evaluated at bid price : 8.98 Bid-YTW : 7.62 % |

| RY.PR.O | Perpetual-Discount | 4.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 20.39 Evaluated at bid price : 20.39 Bid-YTW : 6.08 % |

| IAF.PR.G | FixedReset Ins Non | 4.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 11.25 Evaluated at bid price : 11.25 Bid-YTW : 8.29 % |

| W.PR.M | FixedReset Prem | 4.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 16.75 Evaluated at bid price : 16.75 Bid-YTW : 8.18 % |

| PWF.PR.F | Perpetual-Discount | 4.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 16.95 Evaluated at bid price : 16.95 Bid-YTW : 7.91 % |

| BNS.PR.E | FixedReset Prem | 5.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 19.39 Evaluated at bid price : 19.39 Bid-YTW : 7.05 % |

| RY.PR.N | Perpetual-Discount | 5.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 20.01 Evaluated at bid price : 20.01 Bid-YTW : 6.20 % |

| GWO.PR.H | Deemed-Retractible | 5.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 16.56 Evaluated at bid price : 16.56 Bid-YTW : 7.37 % |

| CM.PR.T | FixedReset Disc | 5.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 14.75 Evaluated at bid price : 14.75 Bid-YTW : 7.71 % |

| CU.PR.H | Perpetual-Discount | 5.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 19.50 Evaluated at bid price : 19.50 Bid-YTW : 6.81 % |

| BAM.PF.D | Perpetual-Discount | 5.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 16.50 Evaluated at bid price : 16.50 Bid-YTW : 7.47 % |

| GWO.PR.I | Deemed-Retractible | 5.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 15.27 Evaluated at bid price : 15.27 Bid-YTW : 7.41 % |

| PWF.PR.K | Perpetual-Discount | 5.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 16.09 Evaluated at bid price : 16.09 Bid-YTW : 7.85 % |

| CM.PR.Y | FixedReset Disc | 5.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 15.70 Evaluated at bid price : 15.70 Bid-YTW : 7.61 % |

| TD.PF.J | FixedReset Disc | 5.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 13.01 Evaluated at bid price : 13.01 Bid-YTW : 7.45 % |

| POW.PR.C | Perpetual-Premium | 6.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 19.10 Evaluated at bid price : 19.10 Bid-YTW : 7.78 % |

| BAM.PR.C | Floater | 6.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 6.92 Evaluated at bid price : 6.92 Bid-YTW : 8.78 % |

| GWO.PR.G | Deemed-Retractible | 6.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 17.28 Evaluated at bid price : 17.28 Bid-YTW : 7.57 % |

| GWO.PR.L | Deemed-Retractible | 6.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 18.20 Evaluated at bid price : 18.20 Bid-YTW : 7.81 % |

| BAM.PR.K | Floater | 6.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 6.88 Evaluated at bid price : 6.88 Bid-YTW : 8.83 % |

| SLF.PR.I | FixedReset Ins Non | 6.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 11.25 Evaluated at bid price : 11.25 Bid-YTW : 8.05 % |

| GWO.PR.F | Deemed-Retractible | 6.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 19.25 Evaluated at bid price : 19.25 Bid-YTW : 7.71 % |

| GWO.PR.M | Deemed-Retractible | 6.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 18.15 Evaluated at bid price : 18.15 Bid-YTW : 8.04 % |

| BAM.PF.A | FixedReset Disc | 6.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 12.09 Evaluated at bid price : 12.09 Bid-YTW : 8.51 % |

| PWF.PR.G | Perpetual-Premium | 7.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 20.00 Evaluated at bid price : 20.00 Bid-YTW : 7.53 % |

| POW.PR.D | Perpetual-Discount | 7.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 16.50 Evaluated at bid price : 16.50 Bid-YTW : 7.76 % |

| BAM.PR.B | Floater | 7.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 6.94 Evaluated at bid price : 6.94 Bid-YTW : 8.75 % |

| SLF.PR.E | Deemed-Retractible | 7.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 15.78 Evaluated at bid price : 15.78 Bid-YTW : 7.17 % |

| PWF.PR.E | Perpetual-Premium | 7.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 17.81 Evaluated at bid price : 17.81 Bid-YTW : 7.88 % |

| GWO.PR.R | Deemed-Retractible | 8.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 16.80 Evaluated at bid price : 16.80 Bid-YTW : 7.19 % |

| SLF.PR.A | Deemed-Retractible | 8.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 16.61 Evaluated at bid price : 16.61 Bid-YTW : 7.19 % |

| TRP.PR.D | FixedReset Disc | 8.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 10.00 Evaluated at bid price : 10.00 Bid-YTW : 8.79 % |

| POW.PR.B | Perpetual-Discount | 8.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 17.10 Evaluated at bid price : 17.10 Bid-YTW : 8.02 % |

| BAM.PF.B | FixedReset Disc | 8.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 11.18 Evaluated at bid price : 11.18 Bid-YTW : 8.45 % |

| MFC.PR.I | FixedReset Ins Non | 8.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 10.85 Evaluated at bid price : 10.85 Bid-YTW : 8.91 % |

| GWO.PR.Q | Deemed-Retractible | 9.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 16.73 Evaluated at bid price : 16.73 Bid-YTW : 7.75 % |

| TRP.PR.F | FloatingReset | 9.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 8.43 Evaluated at bid price : 8.43 Bid-YTW : 6.78 % |

| GWO.PR.P | Deemed-Retractible | 9.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 17.59 Evaluated at bid price : 17.59 Bid-YTW : 7.73 % |

| BAM.PF.F | FixedReset Disc | 9.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 11.01 Evaluated at bid price : 11.01 Bid-YTW : 8.71 % |

| PWF.PR.I | Perpetual-Premium | 10.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 7.28 % |

| TRP.PR.B | FixedReset Disc | 10.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 7.07 Evaluated at bid price : 7.07 Bid-YTW : 7.54 % |

| BAM.PR.T | FixedReset Disc | 10.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 9.20 Evaluated at bid price : 9.20 Bid-YTW : 8.76 % |

| SLF.PR.B | Deemed-Retractible | 10.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 17.01 Evaluated at bid price : 17.01 Bid-YTW : 7.10 % |

| SLF.PR.C | Deemed-Retractible | 11.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 15.90 Evaluated at bid price : 15.90 Bid-YTW : 7.04 % |

| SLF.PR.D | Deemed-Retractible | 11.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 15.70 Evaluated at bid price : 15.70 Bid-YTW : 7.13 % |

| CU.PR.C | FixedReset Disc | 11.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 11.40 Evaluated at bid price : 11.40 Bid-YTW : 7.25 % |

| BNS.PR.Z | FixedReset Bank Non | 11.39 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.05 Bid-YTW : 14.86 % |

| TD.PF.D | FixedReset Disc | 11.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 12.60 Evaluated at bid price : 12.60 Bid-YTW : 7.35 % |

| TRP.PR.A | FixedReset Disc | 13.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 9.23 Evaluated at bid price : 9.23 Bid-YTW : 8.18 % |

| PWF.PR.P | FixedReset Disc | 13.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 8.01 Evaluated at bid price : 8.01 Bid-YTW : 7.75 % |

| GWO.PR.N | FixedReset Ins Non | 13.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 8.75 Evaluated at bid price : 8.75 Bid-YTW : 6.15 % |

| GWO.PR.T | Deemed-Retractible | 15.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 17.30 Evaluated at bid price : 17.30 Bid-YTW : 7.49 % |

| TRP.PR.C | FixedReset Disc | 15.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 7.50 Evaluated at bid price : 7.50 Bid-YTW : 8.08 % |

| MFC.PR.C | Deemed-Retractible | 15.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 16.07 Evaluated at bid price : 16.07 Bid-YTW : 7.06 % |

| GWO.PR.S | Deemed-Retractible | 16.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 18.01 Evaluated at bid price : 18.01 Bid-YTW : 7.33 % |

| BAM.PR.X | FixedReset Disc | 17.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 8.26 Evaluated at bid price : 8.26 Bid-YTW : 8.09 % |

| BNS.PR.H | FixedReset Prem | 18.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 17.75 Evaluated at bid price : 17.75 Bid-YTW : 7.20 % |

| PVS.PR.G | SplitShare | 18.82 % | YTW SCENARIO Maturity Type : Option Certainty Maturity Date : 2026-02-28 Maturity Price : 25.00 Evaluated at bid price : 20.20 Bid-YTW : 9.26 % |

| MFC.PR.B | Deemed-Retractible | 19.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 6.51 % |

| BAM.PF.G | FixedReset Disc | 25.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 10.67 Evaluated at bid price : 10.67 Bid-YTW : 8.69 % |

| POW.PR.A | Perpetual-Premium | 26.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 17.89 Evaluated at bid price : 17.89 Bid-YTW : 8.02 % |

| MFC.PR.N | FixedReset Ins Non | 27.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 9.72 Evaluated at bid price : 9.72 Bid-YTW : 8.16 % |

| ELF.PR.H | Perpetual-Premium | 28.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 19.25 Evaluated at bid price : 19.25 Bid-YTW : 7.31 % |

| IAF.PR.B | Deemed-Retractible | 32.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 15.95 Evaluated at bid price : 15.95 Bid-YTW : 7.25 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TRP.PR.K | FixedReset Prem | 192,480 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 6.89 % |

| RY.PR.R | FixedReset Prem | 153,091 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 20.90 Evaluated at bid price : 20.90 Bid-YTW : 6.82 % |

| BNS.PR.H | FixedReset Prem | 134,198 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 17.75 Evaluated at bid price : 17.75 Bid-YTW : 7.20 % |

| HSE.PR.A | FixedReset Disc | 80,490 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 4.31 Evaluated at bid price : 4.31 Bid-YTW : 15.00 % |

| TD.PF.H | FixedReset Prem | 69,142 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 17.40 Evaluated at bid price : 17.40 Bid-YTW : 7.25 % |

| TD.PF.C | FixedReset Disc | 65,118 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-19 Maturity Price : 11.15 Evaluated at bid price : 11.15 Bid-YTW : 7.71 % |

| There were 109 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.G | FixedReset Ins Non | Quote: 10.64 – 19.17 Spot Rate : 8.5300 Average : 4.7372 YTW SCENARIO |

| HSE.PR.E | FixedReset Disc | Quote: 6.70 – 13.00 Spot Rate : 6.3000 Average : 4.1768 YTW SCENARIO |

| NA.PR.G | FixedReset Disc | Quote: 12.25 – 15.95 Spot Rate : 3.7000 Average : 2.1292 YTW SCENARIO |

| TRP.PR.D | FixedReset Disc | Quote: 10.00 – 13.20 Spot Rate : 3.2000 Average : 1.8157 YTW SCENARIO |

| TD.PF.E | FixedReset Disc | Quote: 12.90 – 15.95 Spot Rate : 3.0500 Average : 1.8493 YTW SCENARIO |

| IFC.PR.I | Perpetual-Premium | Quote: 18.15 – 22.00 Spot Rate : 3.8500 Average : 2.7672 YTW SCENARIO |

It’s a wild world; I fear that are a lot of people making some very bad decisions right now; although the nature of markets demands that other people are making some very good ones, as the rich get richer.

My thoughts exactly. When this wild ride ends (and it will), the scale of the global wealth transfer may be one of the greatest in history. Every share sold is bought by someone. It will fascinating to see who rises strongest out of this carnage. Some new household names for sure.