Pembina Pipelines and Veresen have announced:

they have entered into an arrangement agreement to create one of the largest energy infrastructure companies in Canada with a pro-forma enterprise value of approximately $33 billion (the “Transaction”).

…

Under the terms of the arrangement agreement, Pembina is offering to acquire all the issued and outstanding shares of Veresen by way of a plan of arrangement under the Business Corporations Act (Alberta). The Transaction is valued at approximately $9.7 billion including the assumption of Veresen’s debt (including subsidiary debt) and preferred shares.Pembina is offering to acquire all of the outstanding Veresen common shares in exchange for either (i) 0.4287 of a common share of Pembina or (ii) $18.65 in cash, subject to pro-ration based on maximum share consideration of approximately 99.5 million Pembina common shares and maximum cash consideration of approximately $1.523 billion. Assuming full pro-ration, each Veresen shareholder would receive $4.8494 in cash and 0.3172 of a common share of Pembina for each Veresen common share.

…

Furthermore, Veresen will be seeking approval of holders of outstanding Veresen preferred shares to effect the exchange of such shares for Pembina preferred shares with the same terms and conditions as the outstanding Veresen preferred shares. For such exchange to occur at closing of the Transaction, approval of at least 662/3 percent of holders of Veresen’s preferred shares is required, voting as one class, represented in person or by proxy at a special meeting of Veresen preferred shareholders to be called to consider the Transaction. Closing of the Transaction is not conditional on the approval of the holders of Veresen’s preferred shares.

…

The cash consideration associated with the Transaction will be initially funded through the company’s $2.5 billion unsecured credit facility. Subsequently, Pembina expects to refinance this with a combination of internally generated cash flows and the issuance of Medium Term Notes and preferred shares.In addition, a special meeting of the holders of preferred shares of Veresen will be called to approve the Transaction. If the holders of Veresen preferred shares, voting together as a single class, approve the Transaction, each preferred share of Veresen would be exchanged, on a one for one basis, for a new preferred share of Pembina having the same terms and conditions as the Veresen preferred shares. Completion of the Transaction is not conditional upon the approval of the Transaction by holders of Veresen’s preferred shares.

If the holders of Veresen’s preferred shares do not approve the Transaction, voting as a single class but separate from common shares, the Veresen preferred shares will remain outstanding following completion of the Transaction.

DBRS immediately gave its blessing to the transaction:

DBRS Limited (DBRS) has today confirmed the Issuer Rating and Senior Unsecured Notes rating of Pembina Pipeline Corporation (Pembina or the Company) at BBB and the Company’s Preferred Shares at Pfd-3. All trends remain Stable. The confirmations follow Pembina’s announcement that it has entered into an agreement to acquire Veresen Inc. (Veresen) for $9.7 billion, including the assumption of Veresen’s debt (the Acquisition or the Transaction). The confirmations reflect DBRS’s expectation that the Acquisition would not have a material impact on the Company’s current credit profile. On March 3, 2017, DBRS confirmed all of Pembina’s ratings with Stable trends reflecting its solid financial performance in 2016 and the continued improvement of its business risk profile. Veresen was rated BBB by DBRS. However, On August 4, 2016, DBRS placed the ratings of Veresen Under Review with Negative Implications pending the completion of the sales of its power generation assets.

…

With respect to the potential impact of the Acquisition on Pembina’s financial risk profile, DBRS has reviewed Pembina’s financing plan and performed a pro forma analysis and is of the view that the Acquisition would modestly weaken Pembina’s credit metrics in the near term but would not have a material impact over the medium term.

DBRS later added:

DBRS Limited (DBRS) today notes that Veresen Inc. (Veresen or the Company; BBB, Under Review with Negative Implications) and Pembina Pipeline Corporation (Pembina; rated BBB, Stable trend) have announced that they have agreed to combine to create one of the largest energy infrastructure companies in Canada (the Transaction). Under the Transaction, valued at approximately $9.7 billion, including the assumption of Veresen’s debt (including subsidiary debt) and preferred shares, Pembina has offered to acquire all the issued and outstanding shares of Veresen. The Transaction is subject to approval by Veresen’s common shareholders, as well as regulatory approvals, and is expected to close late in the third quarter or early Q4 2017.

DBRS placed Veresen’s ratings Under Review with Negative Implications following the Company’s announcement that it would sell its power generation business. Please refer to the DBRS press releases “DBRS Places Veresen Inc.’s Ratings Under Review with Negative Implications,” dated August 4, 2016, and “DBRS Comments on Veresen’s Sale of Power Business,” dated February 21, 2017. Today’s announcement does not have an immediate impact on the credit profile of Veresen as the Transaction is expected to close later this year. Consequently, DBRS is maintaining the Under Review with Negative Implications status on Veresen’s ratings. DBRS will review the Under Review with Negative Implications status after the sale of Veresen’s remaining power assets has closed in Q2 2017 and as more details become available with respect to the Transaction.

Veresen preferred shares immediately leapt upwards, although early gains did not hold, as illustrated by this chart of the day’s trading in VSN.PR.A:

Click for Big

VSN.PR.E saw very heavy trading (368,192 shares) but simply rose to a modest premium over par and stayed there.

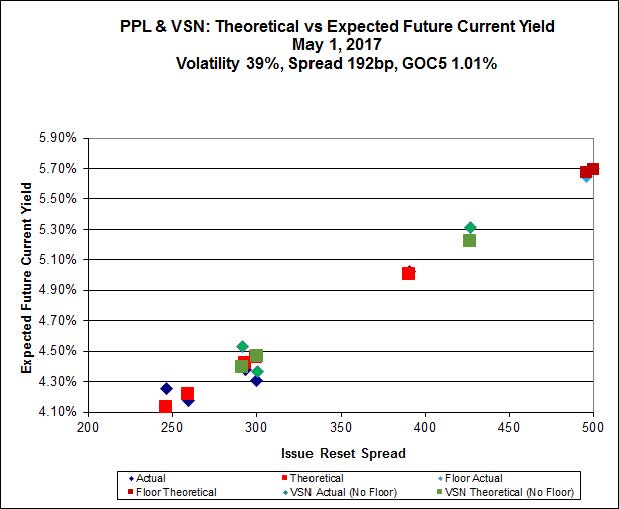

The price movement left the PPL and VSN preferreds trading as equivalents:

Click for Big

The results of this Implied Volatility analysis are a little puzzling. The near-par price for an issue with a spread of 427bp (VSN.PR.E) does not seem unreasonable in light of last week’s issuance of BPO FixedReset 4.85%+374M485 and EFN FixedReset 5.75%+464M575, but the Implied Volatility of 39% is ludicrously high; much higher than can be expected even assuming a huge market appetite for low-spread issues (in anticipation of GOC-5 yields). Thus, I would expect the higher-spread issues to outperform the lower spread issues over the next … period. (Predictions are one thing – predictions with a time frame are quite another!).

Affected issues are VSN.PR.A, VSN.PR.C and VSN.PR.E.

Outstanding PPL issues are PPL.PR.A, PPL.PR.C, PPL.PR.E, PPL.PR.G, PPL.PR.I, PPL.PR.K and PPL.PR.M.