Manulife Financial Corporation has announced:

the applicable dividend rates for its Non-cumulative Rate Reset Class 1 Shares Series 5 (the “Series 5 Preferred Shares”) (TSX: MFC.PR.G) and Non-cumulative Floating Rate Class 1 Shares Series 6 (the “Series 6 Preferred Shares”).

With respect to any Series 5 Preferred Shares that remain outstanding after December 19, 2016, holders thereof will be entitled to receive fixed rate non-cumulative preferential cash dividends on a quarterly basis, as and when declared by the Board of Directors of Manulife and subject to the provisions of the Insurance Companies Act (Canada). The dividend rate for the five-year period commencing on December 20, 2016, and ending on December 19, 2021, will be 3.89100% per annum or $0.243188 per share per quarter, being equal to the sum of the five-year Government of Canada bond yield as at November 21, 2016, plus 2.90%, as determined in accordance with the terms of the Series 5 Preferred Shares.

With respect to any Series 6 Preferred Shares that may be issued on December 19, 2016 in connection with the conversion of the Series 5 Preferred Shares into the Series 6 Preferred Shares, holders thereof will be entitled to receive floating rate non-cumulative preferential cash dividends on a quarterly basis, calculated on the basis of actual number of days elapsed in each quarterly floating rate period divided by 365, as and when declared by the Board of Directors of Manulife and subject to the provisions of the Insurance Companies Act (Canada). The dividend rate for the three-month period commencing on December 20, 2016, and ending on March 19, 2017, will be 0.83885% (3.40200% on an annualized basis) or $0.209713 per share, being equal to the sum of the three-month Government of Canada Treasury bill yield as at November 21, 2016, plus 2.90%, as determined in accordance with the terms of the Series 6 Preferred Shares.

Beneficial owners of Series 5 Preferred Shares who wish to exercise their right of conversion should instruct their broker or other nominee to exercise such right before 5:00 p.m. (Toronto time) on December 5, 2016. The news release announcing such conversion right was issued on October 20, 2016 and can be viewed on SEDAR or Manulife’s website. Conversion inquiries should be directed to Manulife’s Registrar and Transfer Agent, CST Trust Company, at 1-800-387-0825.

The Toronto Stock Exchange (“TSX”) has conditionally approved the listing of the Series 6 Preferred Shares effective upon conversion. Listing of the Series 6 Preferred Shares is subject to Manulife fulfilling all the listing requirements of the TSX and, upon approval, the Series 6 Preferred Shares will be listed on the TSX under the trading symbol “MFC.PR.Q”.

The prior notice of extension was reported on PrefBlog.

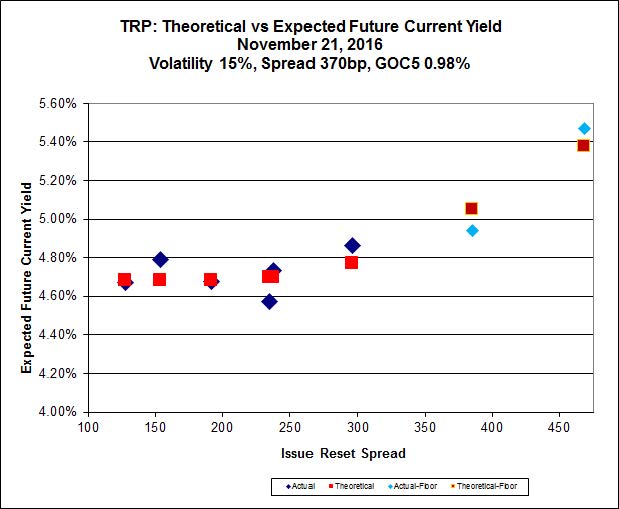

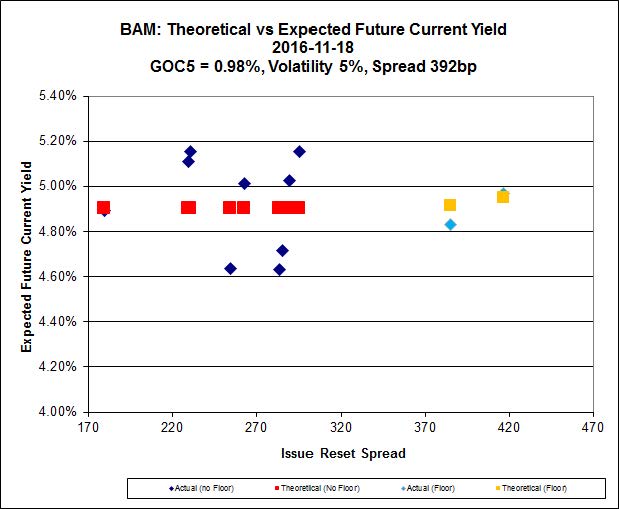

I will make a recommendation regarding whether to convert or hold MFC.PR.G at month-end.