Split Yield Corp has announced:

Split Yield Corporation (“Split Yield”) reports financial results for the six months ending July 31, 2009.

The six month period ending July 31, 2009 was one of the most tumultuous periods in financial market history. Against this backdrop, the market prices of the stocks in the portfolio mirrored this activity reaching lows in early March but recovering significantly by the end of July. The net asset value per unit (a unit consists of one Class I Preferred share, one Class II Preferred share and one Capital share) increased by $3.43 to $18.66 per unit as at July 31, 2009.

In a word, yech. As the audited financials state:

The Company has 1,213,202 Class I Preferred shares and 1,213,202 Class II Preferred shares outstanding as at July 31, 2009 with a principal repayment of $24,264,040 and $18,198,030 respective due on termination date, February 1, 2012. As at July 31, 2009 the Company had net assets equivalent to $18.66 per Class I Preferred share and nil per Class II Preferred share. This represents a deficiency as at July 31, 2009 of $1.34 per Class I Preferred share and $15.00 per Class II Preferred share for a total deficiency of $19,823,720. If this condition prevails, the Company will have insufficient assets to meet its full liability of the Preferred shares at the termination date.

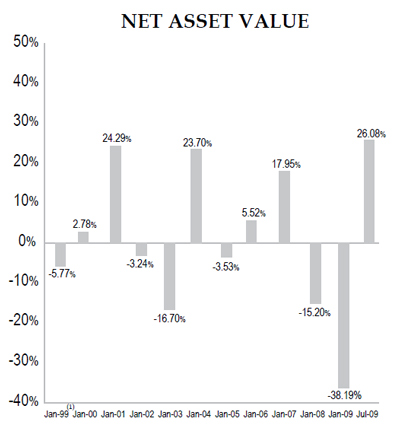

How did things come to such a pass? Well … I don’t know. The chart of NAV:

… shows some numbers for cumulative performance that, when a product is taken, come to a cumulative return since inception of -4.77%, and NAV has declined a lot more than that. I can only assume that this figure reports total return on the portfolio gross of distributions, in which case the decline in NAV is due to the cumulative distributions since inception of $7.25, $10.54 and $12.52 on the capital units, YLD.PR.B and YLD.PR.A, respectively. The MER (1.95% annualized in 1H09) will also have played a role.

The company notes:

The Company’s investment manager, Quadravest Capital Management Inc., actively manages the Company’s portfolio consisting primarily of common equities in the S&P/TSX 60 and the S&P 100 Indices. In order to generate additional income above the dividend and interest income earned in the Portfolio, the Company writes covered call options. This conservative strategy is designed to enhance the income in the portfolio by enabling the Company to earn strong income in times of volatile markets while reducing the effects of market corrections. In addition, this source of income is treated as capital gains and as such receives a more favorable tax treatment relative to other sources of income.

Quick! Does anybody have total return figures handy for those indices, from April 16, 1998 to July 31, 2009?