The U.S. economy looks to be in danger of losing its main pillar as employers throttled back hiring in May to the lowest level in almost six years.

The slowdown — payrolls rose by 38,000 after a downwardly revised 123,000 in April — raised questions about the ability of consumers to keep spending at a good clip. It also cast doubts on Federal Reserve policy makers’ intentions to raise interest rates soon.

…

The deceleration in the labor market was widespread, with industries from construction and manufacturing to temporary-help services cutting workers.

…

Unemployment did drop, to an almost nine-year low of 4.7 percent last month from 5 percent in April. But even that was bad news as the decline was mainly because more Americans dropped out of the labor force rather than from an increase in employment.In a sign that the jobs market may remain weak, the Institute for Supply Management reported that American service providers expanded in May at the slowest pace in more than two years. Its measure of services employment dropped to its lowest since February 2014.

…

About the only bright spot in the report was worker pay. Average hourly earnings, rose by 0.2 percent in May after a 0.4 percent gain in April that was a bit stronger than initially reported. Pay increased 2.5 percent over the 12 months ended in May.

This, naturally enough, dampens expectations for a Fed hike:

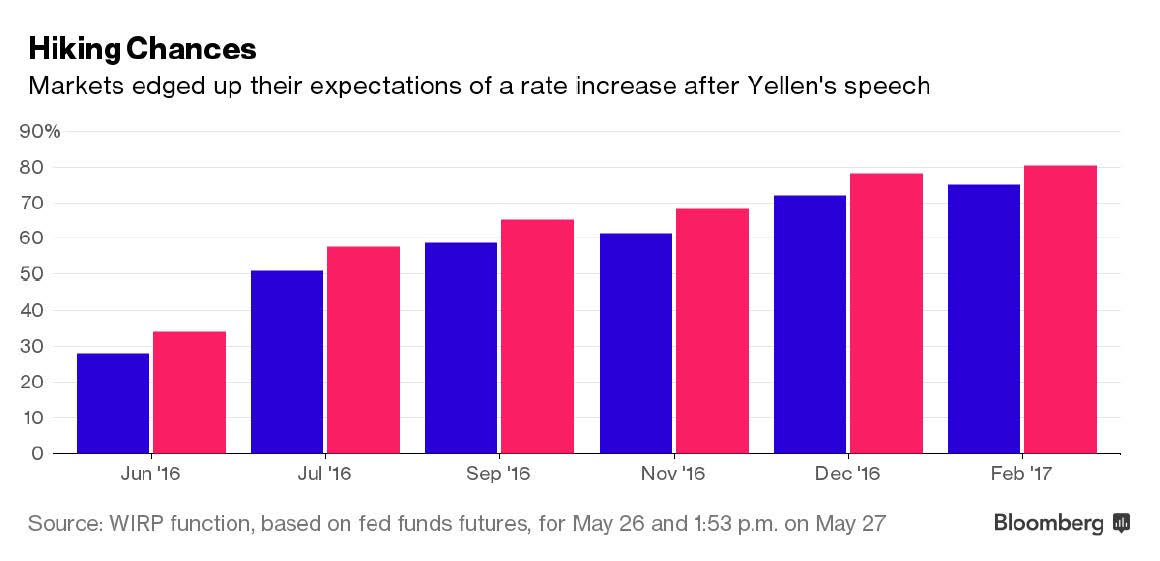

The argument for a June interest-rate hike from the Federal Reserve has evaporated.

Economists and investors largely agreed that a disappointing employment report for May — the U.S. economy added just 38,000 new jobs — all but eliminated the chance that Fed officials would tighten policy when they meet June 14-15 in Washington, and may make it difficult for them to raise in July.

…

Odds of a June hike implied by futures trading, which had risen as high as 34 percent in late May as Fed officials hinted at their eagerness to raise rates, tumbled to just 4 percent following the employment report. The odds are based on prices in federal funds futures contracts.

And, perhaps on a related note, the amount of negative yield debt is increasing:

Negative-yielding government debt has risen above $10tn for the first time, enveloping an increasingly large part of the financial markets after being fuelled by central bank stimulus and a voracious investor appetite for sovereign paper.

The amount of sovereign debt trading with a sub-zero yield climbed 5 per cent in May from a month earlier to $10.4tn, buoyed by rising bond prices in Italy, Japan, Germany and France, according to rating agency Fitch. Yields fall as the price of the underlying bonds climbs.

The ascent of the negative yield, which first affected only the shortest maturing notes from highly rated sovereigns, has encompassed seven-year German Bunds and 10-year Japanese government bonds as both the European Central Bank and Bank of Japan have cut benchmark interest rates and launched bond-buying programmes.

On Wednesday the ECB left its main deposit rate for bank reserves unchanged at minus 0.4 per cent.

Unwinding this easy-money is going to be interesting:

Lurking in the bond market is a $1 trillion reason for the Federal Reserve to go slow on interest-rate increases.

That’s how much bondholders stand to lose if Treasury yields rise unexpectedly by 1 percentage point, according to a Goldman Sachs Group Inc. estimate. A hit of that magnitude would exceed the realized losses since the financial crisis on mortgage bonds without government backing, Goldman Sachs analysts Marty Young and Charles Himmelberg wrote in a note published today.

There’s been some loss of face for the US government’s regulatory extortion squad:

The U.S. government has been made several of these unusual repayments in the aftermath of its historic pursuit of insider trading, which led to 80 convictions, brought down at least five hedge funds and resulted in more than $2 billion in payments from defendants.

Fourteen of those convictions have now been overturned — including two that were struck down by an appeals court in 2014, opening the door for the victors and others to claw back penalties and fines from the Justice Department and the U.S. Securities and Exchange Commission. The government has now handed back more than $40 million in all, including to three individuals whose convictions were overturned and two of the hedge funds where they worked.

…

The refunds are among several setbacks for the government recently in its insider-trading crackdown. Earlier this year, an appeals court temporarily released convicted stock trader Douglas Whitman from a California halfway house after he argued that his conduct may not have been illegal, depending on how the U.S. Supreme Court rules in another pending insider-trading case.Five others convicted of insider trading, including former Goldman Sachs Group Inc. director Rajat Gupta, have sought reviews of their cases.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0320 % | 1,673.5 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0320 % | 3,057.1 |

| Floater | 4.54 % | 4.61 % | 64,181 | 16.14 | 3 | -0.0320 % | 1,761.8 |

| OpRet | 4.88 % | -0.61 % | 46,540 | 0.08 | 1 | -0.2779 % | 2,827.9 |

| SplitShare | 4.90 % | 5.14 % | 81,368 | 4.70 | 7 | -0.0231 % | 3,324.7 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0231 % | 2,594.1 |

| Perpetual-Premium | 5.62 % | 3.54 % | 79,812 | 0.09 | 9 | 0.2007 % | 2,616.7 |

| Perpetual-Discount | 5.39 % | 5.50 % | 110,101 | 14.62 | 28 | 0.2864 % | 2,719.4 |

| FixedReset | 5.10 % | 4.66 % | 163,460 | 14.32 | 87 | -0.0451 % | 2,003.0 |

| Deemed-Retractible | 5.12 % | 5.36 % | 128,646 | 4.97 | 33 | -0.0240 % | 2,699.5 |

| FloatingReset | 3.20 % | 5.25 % | 26,200 | 5.24 | 17 | -1.9133 % | 2,080.5 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| PWF.PR.Q | FloatingReset | -28.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 9.32 Evaluated at bid price : 9.32 Bid-YTW : 5.81 % |

| TRP.PR.H | FloatingReset | -10.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 9.35 Evaluated at bid price : 9.35 Bid-YTW : 4.86 % |

| TRP.PR.I | FloatingReset | -3.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 11.20 Evaluated at bid price : 11.20 Bid-YTW : 4.69 % |

| IAG.PR.G | FixedReset | -2.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.99 Bid-YTW : 6.81 % |

| TRP.PR.G | FixedReset | -1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 19.15 Evaluated at bid price : 19.15 Bid-YTW : 4.94 % |

| BNS.PR.Y | FixedReset | -1.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.11 Bid-YTW : 5.98 % |

| BMO.PR.Q | FixedReset | -1.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.50 Bid-YTW : 5.79 % |

| HSE.PR.A | FixedReset | -1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 11.46 Evaluated at bid price : 11.46 Bid-YTW : 5.43 % |

| TRP.PR.A | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 15.00 Evaluated at bid price : 15.00 Bid-YTW : 4.71 % |

| TRP.PR.F | FloatingReset | -1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 13.90 Evaluated at bid price : 13.90 Bid-YTW : 4.42 % |

| BNS.PR.Z | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.10 Bid-YTW : 6.30 % |

| CU.PR.C | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 17.75 Evaluated at bid price : 17.75 Bid-YTW : 4.57 % |

| BAM.PR.Z | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 19.50 Evaluated at bid price : 19.50 Bid-YTW : 5.02 % |

| TD.PF.E | FixedReset | -1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 20.71 Evaluated at bid price : 20.71 Bid-YTW : 4.48 % |

| W.PR.H | Perpetual-Discount | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 23.91 Evaluated at bid price : 24.15 Bid-YTW : 5.78 % |

| BAM.PR.X | FixedReset | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 14.30 Evaluated at bid price : 14.30 Bid-YTW : 4.83 % |

| HSE.PR.E | FixedReset | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 19.86 Evaluated at bid price : 19.86 Bid-YTW : 5.54 % |

| BAM.PF.G | FixedReset | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 20.50 Evaluated at bid price : 20.50 Bid-YTW : 4.75 % |

| FTS.PR.H | FixedReset | 1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 13.52 Evaluated at bid price : 13.52 Bid-YTW : 4.26 % |

| FTS.PR.J | Perpetual-Discount | 1.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 22.58 Evaluated at bid price : 22.90 Bid-YTW : 5.20 % |

| BAM.PR.T | FixedReset | 1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 15.60 Evaluated at bid price : 15.60 Bid-YTW : 5.17 % |

| GWO.PR.N | FixedReset | 1.63 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.34 Bid-YTW : 9.46 % |

| FTS.PR.F | Perpetual-Discount | 2.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 23.32 Evaluated at bid price : 23.60 Bid-YTW : 5.21 % |

| HSE.PR.G | FixedReset | 2.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 19.99 Evaluated at bid price : 19.99 Bid-YTW : 5.48 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| CU.PR.E | Perpetual-Discount | 142,332 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 22.48 Evaluated at bid price : 22.79 Bid-YTW : 5.39 % |

| BAM.PR.C | Floater | 100,891 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 10.36 Evaluated at bid price : 10.36 Bid-YTW : 4.62 % |

| CU.PR.D | Perpetual-Discount | 94,671 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 22.45 Evaluated at bid price : 22.76 Bid-YTW : 5.40 % |

| MFC.PR.F | FixedReset | 94,281 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.71 Bid-YTW : 10.20 % |

| RY.PR.H | FixedReset | 80,961 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-03 Maturity Price : 18.61 Evaluated at bid price : 18.61 Bid-YTW : 4.32 % |

| BNS.PR.A | FloatingReset | 72,063 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.85 Bid-YTW : 4.38 % |

| There were 33 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| PWF.PR.Q | FloatingReset | Quote: 9.32 – 13.00 Spot Rate : 3.6800 Average : 2.0883 YTW SCENARIO |

| TRP.PR.F | FloatingReset | Quote: 13.90 – 14.90 Spot Rate : 1.0000 Average : 0.6346 YTW SCENARIO |

| HSE.PR.G | FixedReset | Quote: 19.99 – 21.00 Spot Rate : 1.0100 Average : 0.7024 YTW SCENARIO |

| TRP.PR.H | FloatingReset | Quote: 9.35 – 10.47 Spot Rate : 1.1200 Average : 0.8416 YTW SCENARIO |

| TRP.PR.G | FixedReset | Quote: 19.15 – 19.71 Spot Rate : 0.5600 Average : 0.3927 YTW SCENARIO |

| CGI.PR.D | SplitShare | Quote: 24.71 – 25.23 Spot Rate : 0.5200 Average : 0.3727 YTW SCENARIO |