Today’s big news was the BoC announcement:

The Bank of Canada today announced that it is maintaining its target for the overnight rate at 1/2 per cent. The Bank Rate is correspondingly 3/4 per cent and the deposit rate is 1/4 per cent.

The global economy is progressing largely as the Bank anticipated in its January Monetary Policy Report (MPR). Financial market volatility, reflecting heightened concerns about economic momentum, appears to be abating. Although downside risks remain, the Bank still expects global growth to strengthen this year and next. Recent data indicate that the U.S. expansion remains broadly on track. At the same time, the low level of oil prices will continue to dampen growth in Canada and other energy-producing countries.

Prices of oil and other commodities have rebounded in recent weeks. In this context, and in light of shifting expectations for monetary policy in Canada and the United States, the Canadian dollar has appreciated from its recent lows. With these movements, both the price of oil and the exchange rate have averaged close to levels assumed in the January MPR.

Canada’s GDP growth in the fourth quarter was not as weak as expected, but the near-term outlook for the economy remains broadly the same as in January. National employment has held up despite job losses in resource-intensive regions, and household spending continues to underpin domestic demand. Non-energy exports are gathering momentum, particularly in sectors that are sensitive to exchange rate movements. However, overall business investment remains very weak due to retrenchment in the resource sector.

Inflation in Canada is evolving broadly as anticipated. The factors that pushed total CPI inflation up to 2 per cent will likely unwind in the months ahead. Measures of core inflation are at or just below 2 per cent, boosted by the temporary effects of past exchange rate depreciation. Material excess capacity in the Canadian economy will continue to dampen inflation.

An assessment of the impact of the upcoming federal budget’s fiscal measures will be incorporated into the Bank’s April projection. All things considered, the risks to the profile for inflation are roughly balanced. Meanwhile, financial vulnerabilities continue to edge higher, in part due to regional shifts in activity associated with the structural adjustment underway in Canada’s economy. The Bank’s Governing Council judges that the overall balance of risks remains within the zone for which the current stance of monetary policy is appropriate, and the target for the overnight rate remains at 1/2 per cent.

Meanwhile, there is a larger than usual international influence on Fed policy:

Investors are betting that the Fed will hold interest rates steady at its March 15-16 meeting as it assess the impact of a shaky global economy and jittery financial markets. A rise in the dollar triggered by easier policy from the ECB and perhaps the BOJ would support a go-slow strategy to raising rates in the U.S.

Asked how the U.S. central bank would respond if the ECB pushed rates further into negative territory, Fed Governor Lael Brainard told CNBC television on March 7 that she was focused on developments in the U.S. She quickly added though that the economy was being buffeted by “powerful cross currents” from abroad and that a further rise in the dollar would hit manufacturing-industry exports.

…

Fed Vice Chairman Stanley Fischer alluded to the central bank’s dollar dilemma when he spoke to the American Economic Association’s annual meeting in San Francisco on Jan. 3.While policy makers in general recognize the benefits of floating currency rates in redistributing demand throughout the world economy, “they’re not so happy” when they’re the ones “giving up some growth, for instance, by having their exchange rate appreciate,” he said.

And New Zealand has cut its policy rate:

New Zealand’s central bank unexpectedly cut interest rates to a fresh record low and signaled further easing may be needed, saying it’s concerned by a slump in inflation expectations. The kiwi plunged by more than one U.S. cent.

Reserve Bank Governor Graeme Wheeler lowered the official cash rate by a quarter point to 2.25 percent, a move predicted by just two of 17 economists surveyed by Bloomberg. The remainder tipped no change. “Further policy easing may be required to ensure that future average inflation settles near the middle of the target range,” Wheeler said Thursday in Wellington.

Wheeler has resumed easing monetary policy as a stubbornly firm New Zealand dollar, weaker commodity prices and falling price expectations keep inflation beneath his 1-3 percent target. The central bank’s forecasts suggest one further reduction in borrowing costs this year to underpin economic growth and return inflation to its 2 percent target midpoint by early 2018.

…

The New Zealand dollar plunged after the statement, buying 66.58 U.S. cents at 9:38 a.m. in Wellington from 67.80 before the decision. The currency has climbed since late January, muting price pressures, and “a decline would be appropriate given the weakness in export prices,” Wheeler said today.

CalPers, the $284.56-billion dollar pension fund that doesn’t do its own credit analysis, has managed to shake down Moody’s:

Moody’s Investors Service Inc. agreed to pay $130 million to settle claims by the California Public Employee Retirement System over allegedly inflated ratings on residential-mortgage bond deals.

The largest U.S. state pension fund’s accord with Moody’s follows the February 2015 announcement that McGraw Hill Financial Inc.’s Standard & Poor’s would pay $125 million to settle claims by Calpers over grades on subprime mortgages during the run-up to the 2008 financial crisis.

…

McGraw Hill’s pact with Calpers was part of a $1.5 billion settlement to resolve similar allegations from the U.S. Justice Department and more than a dozen states.Calpers sued the companies along with Fitch Ratings Ltd. in 2009 alleging it sustained losses of as much as $1 billion from “wildly inaccurate” risk assessments. Calpers said it put $1.3 billion into three investment vehicles backed by subprime mortgages in 2006 and 2007. The investments crumbled amid the housing crisis. The pension fund claimed the ratings companies helped fuel the investments and bent rules to give them the highest ratings to boost their profits from issuers, Calpers alleged.

They’d be better off checking their assumptions:

The economic assumptions include an assumed inflation assumption of 2.75 percent compounded annually. The inflation assumption is a component of assumed investment return, assumed wage growth, and assumed future post-retirement cost-of-living increases.

Based upon the asset allocation of the Public Employees’ Retirement Fund (PERF), the assumed investment return (net of administrative and investment expenses) is 7.5 percent per year, compounded annually.

On a positive note, the settlement will provide funds for senior management to give to their buddies, similarly to the scam discussed on April 23, 2012.

The Saudis are looking for a bank loan:

Saudi Arabia is seeking a bank loan of between $6-billion (U.S.) and $8-billion, sources familiar with the matter told Reuters, in what would be the first significant foreign borrowing by the kingdom’s government for over a decade.

Riyadh has asked lenders to submit proposals to extend it a five-year U.S. dollar loan of that size, with an option to increase it, the sources said, to help plug a record budget deficit caused by low oil prices.

…

The kingdom’s budget deficit reached nearly $100-billion last year. The government is currently bridging the gap by drawing down its massive store of foreign assets and issuing domestic bonds. But the assets will only last a few more years at their current rate of decline, while the bond issues have started to strain liquidity in the banking system.

Comic book fans and supporters of civil forfeiture will be pleased to learn that the Junior Justice League has another member:

The NHL ruled that an off-season rape allegation made against Patrick Kane was unfounded in determining that the Chicago Blackhawks star forward will not face any league disciplinary action.

The decision was issued on Wednesday, when the league issued a one-paragraph statement announcing it had completed its independent review of the allegations against Kane. The final step of the investigation occurred on Monday, when Kane met with NHL Commissioner Gary Bettman in New York.

Barry Critchley has enthusiastically endorsed the quixotic bid to get RON.PR.A taken out at par. I have updated the PrefBlog report on this week’s development.

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts gaining 2bp, FixedResets up 37bp and DeemedRetractibles off 26bp. The Performance Highlights table is lengthy, with numerous TRP and HSE issues at the top of the list. Volume was below average.

PerpetualDiscounts now yield 5.76%, equivalent to 7.49% interest at the standard equivalency factor of 1.3x. Long corporates now yield about 4.25%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 325bp, equal to the spread reported on March 2.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

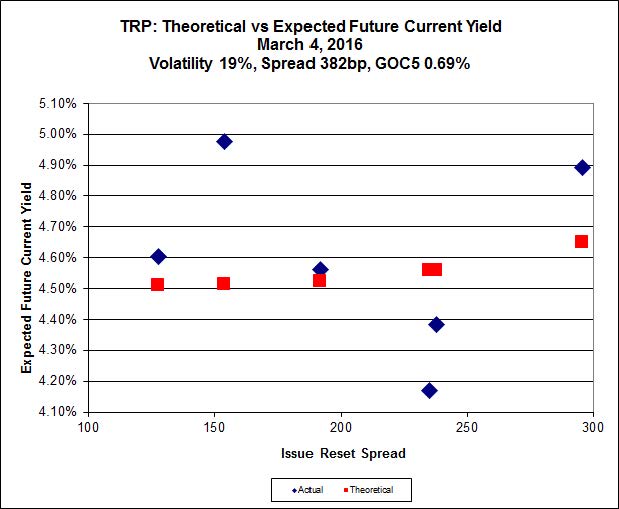

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 17.30 to be $0.99 rich, while TRP.PR.C, resetting 2021-1-30 at +296, is $0.69 cheap at its bid price of 11.40.

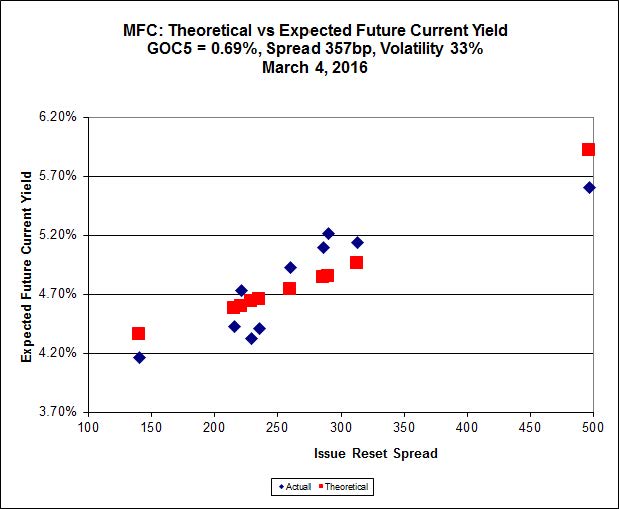

Click for Big

Most expensive is MFC.PR.N, resetting at +230bp on 2020-3-19, bid at 17.50 to be 1.08 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 17.55 to be 1.32 cheap.

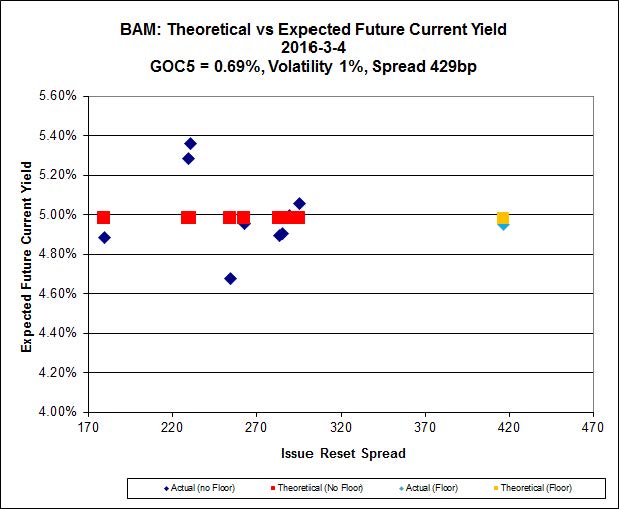

Click for Big

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 13.77 to be $1.29 cheap. BAM.PF.E, resetting at +255 on 2020-3-31 is bid at 17.55 and appears to be $1.15 rich.

Click for Big

FTS.PR.K, with a spread of +205bp, and bid at 15.40 looks $0.53 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 15.05 and is $0.24 cheap.

Click for Big

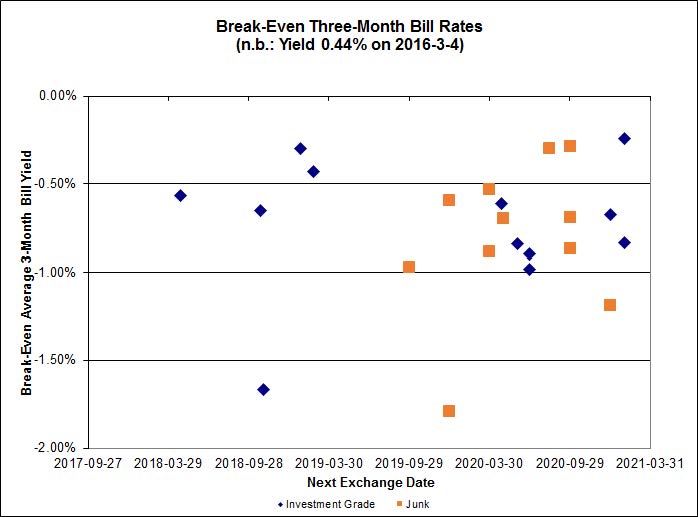

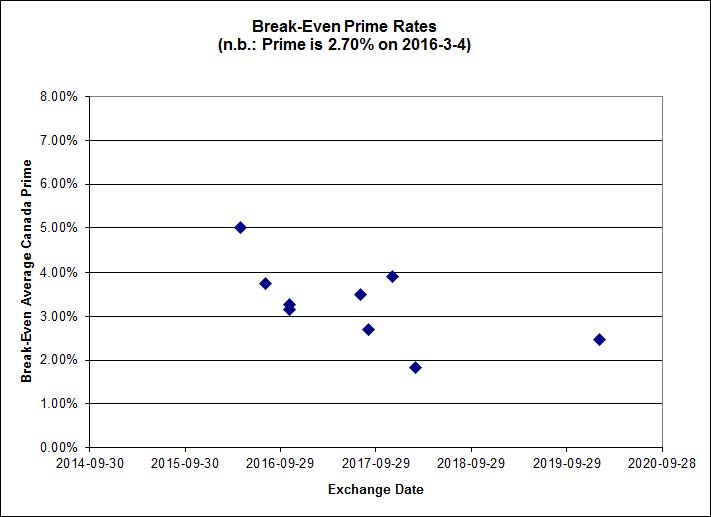

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.95%, with one outlier below -2.00%. There is one junk outlier above 0.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 5.11 % | 6.21 % | 12,116 | 16.42 | 1 | 0.0000 % | 1,534.4 |

| FixedFloater | 7.20 % | 6.32 % | 24,080 | 15.95 | 1 | 0.9946 % | 2,762.4 |

| Floater | 4.52 % | 4.71 % | 73,033 | 15.94 | 4 | 0.8191 % | 1,697.8 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0730 % | 2,750.8 |

| SplitShare | 4.83 % | 5.82 % | 71,615 | 2.64 | 7 | 0.0730 % | 3,219.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0730 % | 2,511.6 |

| Perpetual-Premium | 5.81 % | -0.80 % | 77,419 | 0.08 | 6 | 0.1259 % | 2,539.1 |

| Perpetual-Discount | 5.71 % | 5.76 % | 98,605 | 14.20 | 33 | 0.0219 % | 2,533.3 |

| FixedReset | 5.54 % | 5.19 % | 205,975 | 14.53 | 86 | 0.3709 % | 1,834.8 |

| Deemed-Retractible | 5.32 % | 5.54 % | 115,745 | 5.12 | 34 | -0.2631 % | 2,558.4 |

| FloatingReset | 3.09 % | 4.98 % | 40,623 | 5.45 | 16 | 0.5651 % | 1,981.0 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TD.PF.D | FixedReset | -8.12 % | Completely nonsensical, as the issue traded 6,646 shares today in a range of 18.50-17 before closing at 17.32-19.30. VWAP was 18.87. Way to go with the $1.98 spreads there, guys! I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 17.32 Evaluated at bid price : 17.32 Bid-YTW : 5.16 % |

| TRP.PR.E | FixedReset | -3.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 17.30 Evaluated at bid price : 17.30 Bid-YTW : 4.83 % |

| CIU.PR.C | FixedReset | -2.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 10.52 Evaluated at bid price : 10.52 Bid-YTW : 4.96 % |

| TRP.PR.B | FixedReset | -2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 10.31 Evaluated at bid price : 10.31 Bid-YTW : 4.93 % |

| BAM.PF.F | FixedReset | -1.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 18.36 Evaluated at bid price : 18.36 Bid-YTW : 5.23 % |

| TRP.PR.D | FixedReset | -1.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 16.80 Evaluated at bid price : 16.80 Bid-YTW : 4.90 % |

| BNS.PR.L | Deemed-Retractible | -1.68 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.04 Bid-YTW : 5.39 % |

| BAM.PR.N | Perpetual-Discount | -1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 19.75 Evaluated at bid price : 19.75 Bid-YTW : 6.14 % |

| BNS.PR.R | FixedReset | -1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.55 Bid-YTW : 5.30 % |

| MFC.PR.F | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.26 Bid-YTW : 11.43 % |

| BAM.PF.E | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 17.55 Evaluated at bid price : 17.55 Bid-YTW : 5.12 % |

| GWO.PR.I | Deemed-Retractible | -1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.40 Bid-YTW : 7.35 % |

| VNR.PR.A | FixedReset | 1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 16.84 Evaluated at bid price : 16.84 Bid-YTW : 5.44 % |

| MFC.PR.K | FixedReset | 1.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.68 Bid-YTW : 9.57 % |

| RY.PR.Z | FixedReset | 1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 17.38 Evaluated at bid price : 17.38 Bid-YTW : 4.50 % |

| SLF.PR.I | FixedReset | 1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.30 Bid-YTW : 8.52 % |

| RY.PR.M | FixedReset | 1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 17.91 Evaluated at bid price : 17.91 Bid-YTW : 4.78 % |

| IFC.PR.C | FixedReset | 1.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.40 Bid-YTW : 9.37 % |

| GWO.PR.O | FloatingReset | 1.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 11.20 Bid-YTW : 12.00 % |

| TD.PF.A | FixedReset | 1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 17.02 Evaluated at bid price : 17.02 Bid-YTW : 4.67 % |

| FTS.PR.M | FixedReset | 1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 16.98 Evaluated at bid price : 16.98 Bid-YTW : 5.01 % |

| MFC.PR.J | FixedReset | 1.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.25 Bid-YTW : 8.57 % |

| GWO.PR.N | FixedReset | 1.48 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.07 Bid-YTW : 10.50 % |

| BNS.PR.Z | FixedReset | 1.54 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.09 Bid-YTW : 7.10 % |

| BMO.PR.Q | FixedReset | 1.56 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.28 Bid-YTW : 7.83 % |

| CM.PR.P | FixedReset | 1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 16.86 Evaluated at bid price : 16.86 Bid-YTW : 4.70 % |

| CM.PR.O | FixedReset | 1.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 17.25 Evaluated at bid price : 17.25 Bid-YTW : 4.70 % |

| BAM.PR.X | FixedReset | 1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 13.16 Evaluated at bid price : 13.16 Bid-YTW : 5.19 % |

| BAM.PR.Z | FixedReset | 1.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 17.70 Evaluated at bid price : 17.70 Bid-YTW : 5.47 % |

| TRP.PR.F | FloatingReset | 1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 11.85 Evaluated at bid price : 11.85 Bid-YTW : 4.98 % |

| FTS.PR.H | FixedReset | 2.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 11.43 Evaluated at bid price : 11.43 Bid-YTW : 4.93 % |

| SLF.PR.J | FloatingReset | 2.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 11.75 Bid-YTW : 11.52 % |

| PWF.PR.A | Floater | 2.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 11.65 Evaluated at bid price : 11.65 Bid-YTW : 4.09 % |

| IAG.PR.G | FixedReset | 2.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.20 Bid-YTW : 8.01 % |

| HSE.PR.C | FixedReset | 2.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 15.70 Evaluated at bid price : 15.70 Bid-YTW : 6.52 % |

| RY.PR.J | FixedReset | 2.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 18.44 Evaluated at bid price : 18.44 Bid-YTW : 4.76 % |

| BIP.PR.A | FixedReset | 2.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 18.70 Evaluated at bid price : 18.70 Bid-YTW : 5.80 % |

| BAM.PR.R | FixedReset | 2.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 14.15 Evaluated at bid price : 14.15 Bid-YTW : 5.51 % |

| TRP.PR.H | FloatingReset | 2.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 9.25 Evaluated at bid price : 9.25 Bid-YTW : 4.64 % |

| TRP.PR.C | FixedReset | 2.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 11.40 Evaluated at bid price : 11.40 Bid-YTW : 5.01 % |

| HSE.PR.G | FixedReset | 3.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 17.69 Evaluated at bid price : 17.69 Bid-YTW : 6.25 % |

| TRP.PR.I | FloatingReset | 3.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 10.90 Evaluated at bid price : 10.90 Bid-YTW : 4.59 % |

| HSE.PR.E | FixedReset | 3.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 17.69 Evaluated at bid price : 17.69 Bid-YTW : 6.26 % |

| HSE.PR.A | FixedReset | 4.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 9.40 Evaluated at bid price : 9.40 Bid-YTW : 6.65 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.R | FixedReset | 255,385 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2021-08-24 Maturity Price : 25.00 Evaluated at bid price : 25.31 Bid-YTW : 5.28 % |

| RY.PR.H | FixedReset | 60,655 | RBC crossed 40,000 at 17.35. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 17.25 Evaluated at bid price : 17.25 Bid-YTW : 4.59 % |

| RY.PR.Q | FixedReset | 60,473 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 23.31 Evaluated at bid price : 25.53 Bid-YTW : 5.20 % |

| SLF.PR.E | Deemed-Retractible | 60,419 | Desjardins crossed 50,000 at 20.01. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.00 Bid-YTW : 7.64 % |

| TD.PF.G | FixedReset | 51,152 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 23.31 Evaluated at bid price : 25.49 Bid-YTW : 5.27 % |

| FTS.PR.J | Perpetual-Discount | 46,730 | Scotia crossed 20,600 at 21.22. CIBC bought 20,000 from TD at 21.45. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-09 Maturity Price : 21.22 Evaluated at bid price : 21.22 Bid-YTW : 5.64 % |

| There were 26 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TD.PF.D | FixedReset | Quote: 17.32 – 19.30 Spot Rate : 1.9800 Average : 1.1657 YTW SCENARIO |

| BAM.PR.G | FixedFloater | Quote: 13.20 – 14.50 Spot Rate : 1.3000 Average : 0.8361 YTW SCENARIO |

| TRP.PR.E | FixedReset | Quote: 17.30 – 18.40 Spot Rate : 1.1000 Average : 0.6668 YTW SCENARIO |

| MFC.PR.L | FixedReset | Quote: 16.32 – 17.27 Spot Rate : 0.9500 Average : 0.6609 YTW SCENARIO |

| TRP.PR.B | FixedReset | Quote: 10.31 – 10.95 Spot Rate : 0.6400 Average : 0.4377 YTW SCENARIO |

| PVS.PR.D | SplitShare | Quote: 22.71 – 23.24 Spot Rate : 0.5300 Average : 0.3465 YTW SCENARIO |