The Fed is uncertain on inflation:

Federal Reserve officials signaled concern about stubbornly low inflation even as they indicated that an improving job market is bringing them closer to the first interest-rate increase in almost a decade.

Participants in the July 28-29 Federal Open Market Committee meeting said economic conditions “were approaching that point” where the economy could sustain a slight increase in borrowing costs, according to minutes of the meeting released in Washington on Wednesday.

Preserving their flexibility on the timing of rate liftoff, they also showed more concern about how soon they would hit their 2 percent inflation target, a goal they have missed for more than three years.

… so the cowboys are getting cold feet about the Fed liftoff:

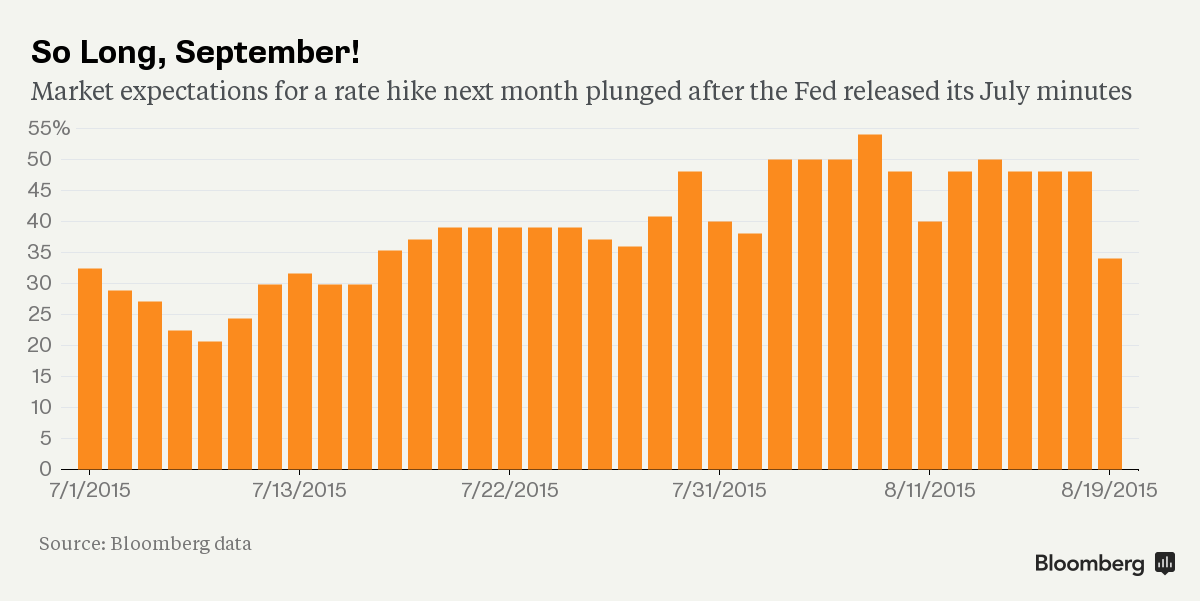

Traders gearing up for the Federal Reserve to raise interest-rates next month reversed course Wednesday after minutes from the central bank’s July meeting showed policy makers were still waffling on whether the economy is strong enough to warrant higher borrowing costs.

That’s far short of the confidence they expected to see from a central bank supposedly just weeks away from what would be the first increase in almost a decade.

The probability that futures traders assign to a rate boost next month slid to 36 percent, the lowest since July, from about 50 percent earlier in the day. The levels assume that the Fed’s target will average 0.375 percent after the first move. The chance of an increase at or before the Fed’s December meeting dropped as well, to 65 percent from 73 percent Tuesday.

Click for Big

GWO, proud issuer of more preferred shares than you can shake a stick at, was confirmed at Pfd-1(high) by DBRS:

Combining somewhat higher leverage with stable profits, GWO has been able to produce an above-peer return on equity in the mid-teens for several years running. As the Company is the largest insurer in Canada, its top-line growth will be limited largely to total market growth. Growth by acquisition within Canada is also constrained, given the dominance of the big three insurers. Achieving a full turnaround with the Putnam investment subsidiary has proven elusive, but recently its funds have achieved high-ranking performance statistics, which should allow a shift toward better results.

Financial leverage at June 30, 2015, is 27.5%, which has shown considerable improvement over recent quarters.

The Canadian operations have a Minimum Continuing Capital and Surplus Requirements ratio of 229%, which is satisfactory. The Company’s U.S. subsidiaries follow and meet U.S. regulatory requirements.

The Company’s credit rating may be negatively affected by an extended decline in interest rates or equity market returns (though it is less sensitive to these declines than its peers), which would affect long-term product profitability; a sustained reduction in earnings; or by large debt-financed acquisitions. Conversely, GWO’s rating may benefit from further improvements in its leverage and coverage ratios.

Today’s market moronization means that none of the following numbers should be taken very seriously, but we’ll do what we can …

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts up 18bp, FixedResets getting whacked for 74bp and DeemedRetractibles gaining 10bp. The Performance Highlights table is:

- Lengthy

- Dominated by FixedReset losers, and

- Virtually meaningless

. Volume was high

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

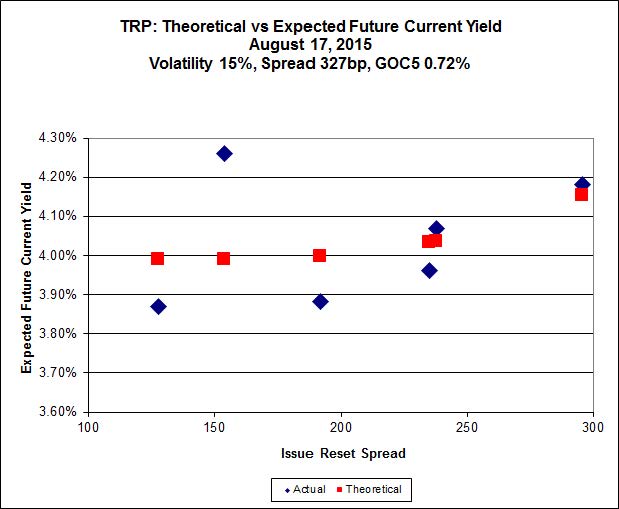

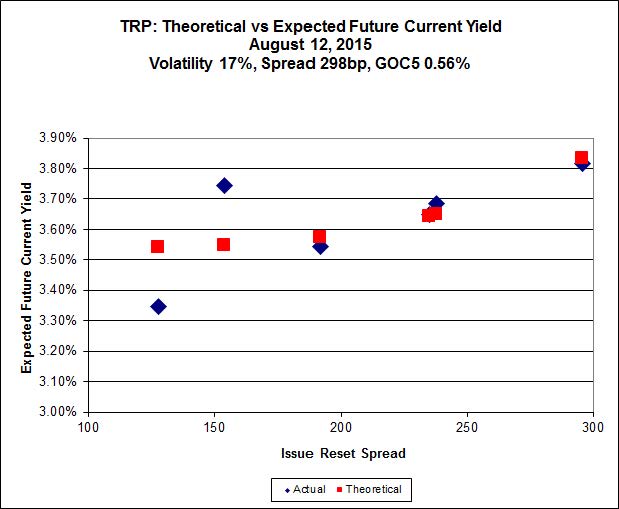

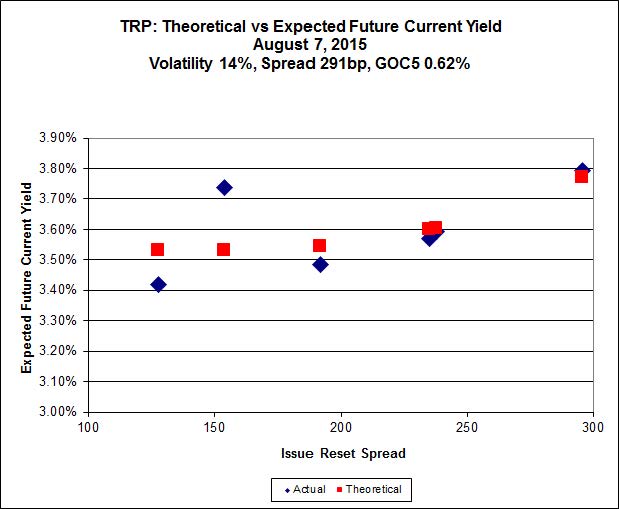

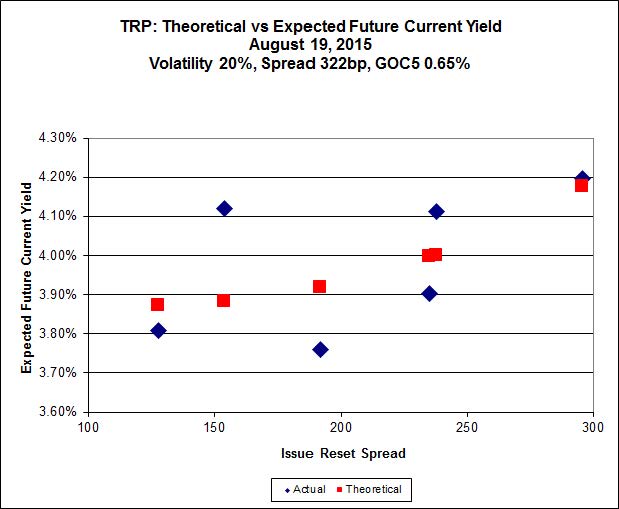

Here’s TRP:

Click for Big

TRP.PR.A, which resets 2019-12-31 at +192, is bid at 17.09 to be $0.69 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.82 cheap at its bid price of 13.29.

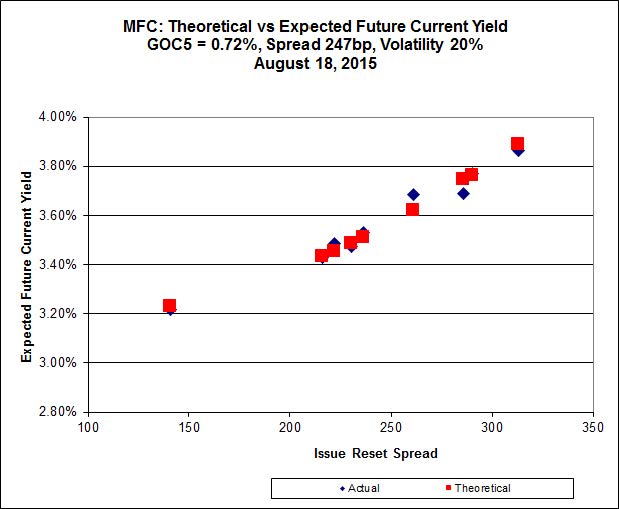

Click for Big

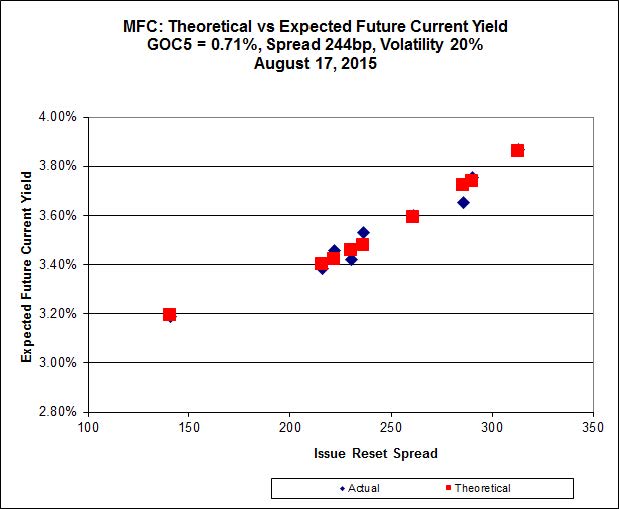

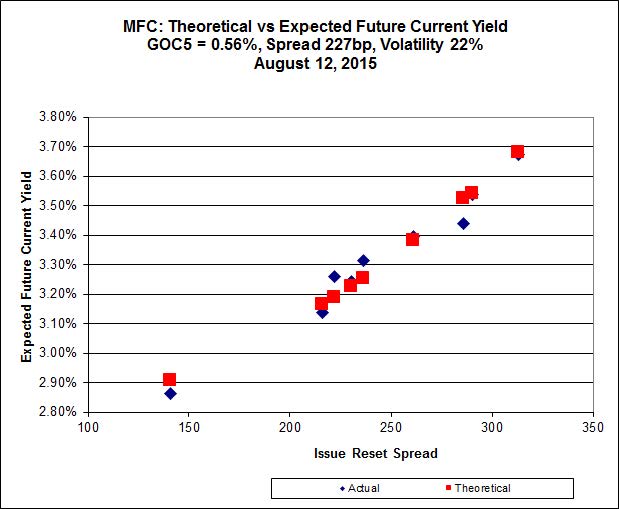

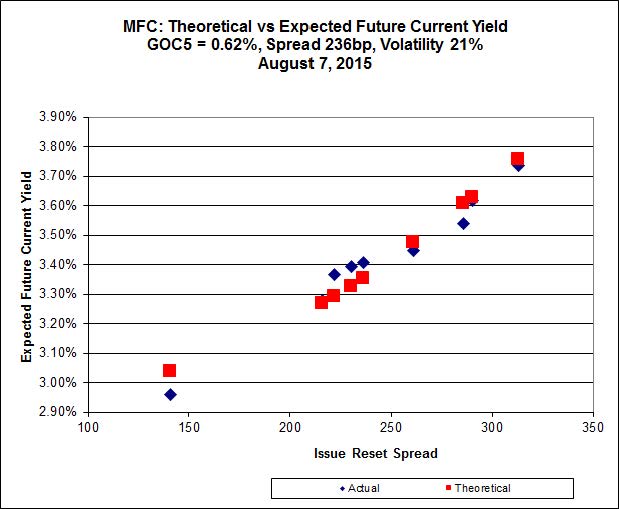

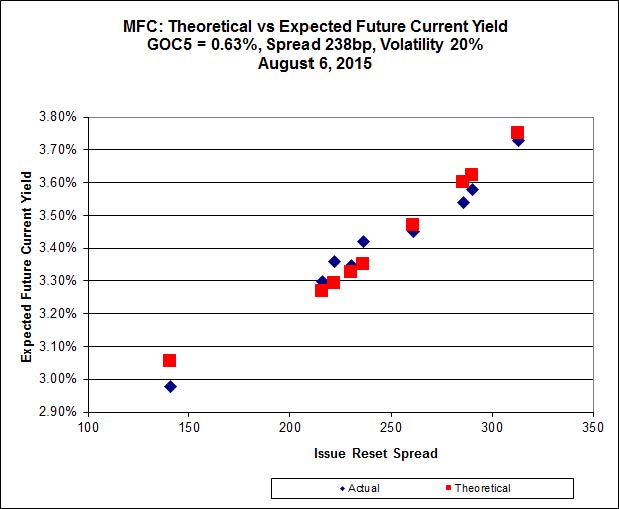

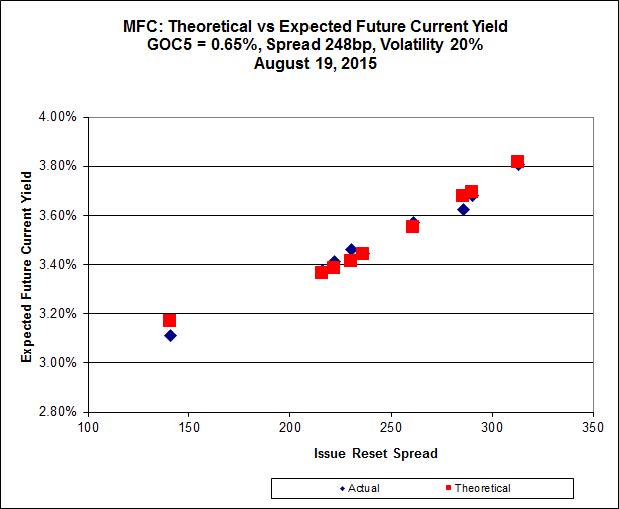

Another good fit today!

Most expensive is MFC.PR.I, resetting at +286bp on 2017-9-19, bid at 24.22 to be 0.34 rich, while MFC.PR.N, resetting at +230bp on 2020-3-19, is bid at 21.31 to be $0.29 cheap.

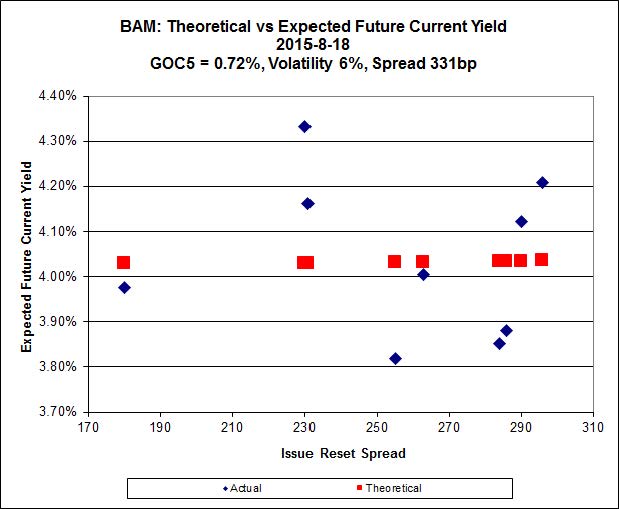

Click for Big

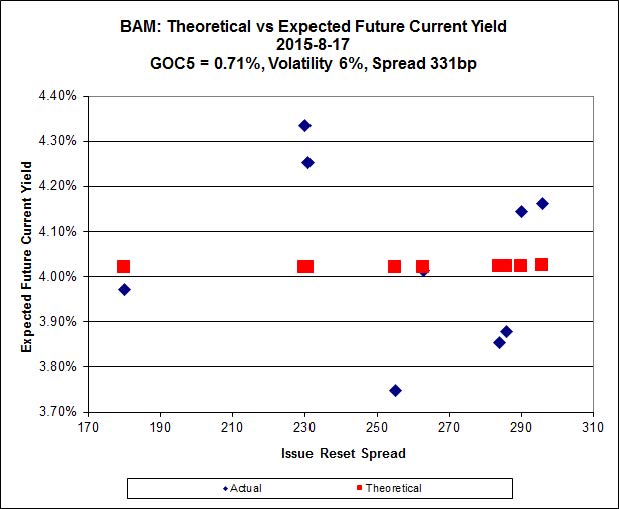

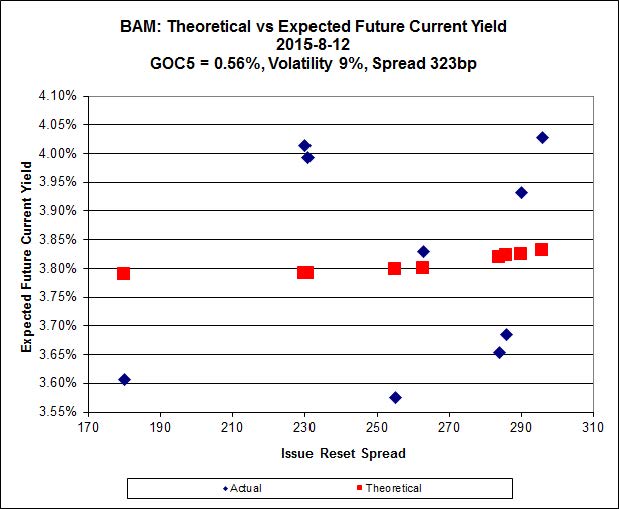

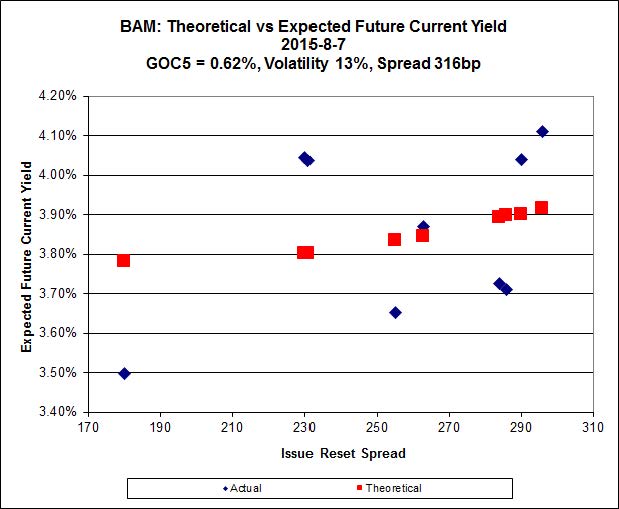

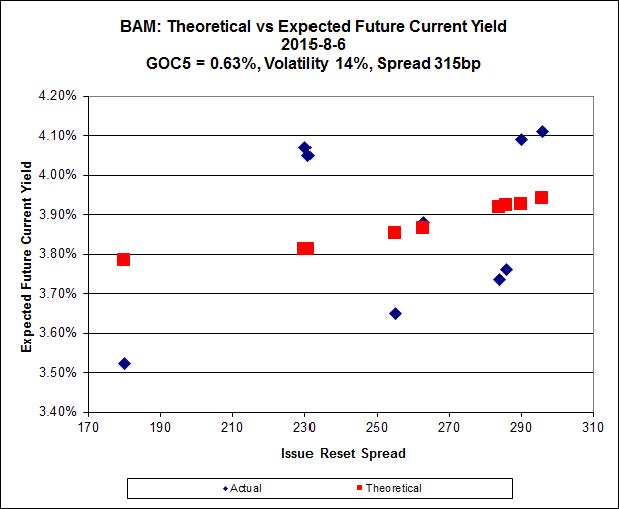

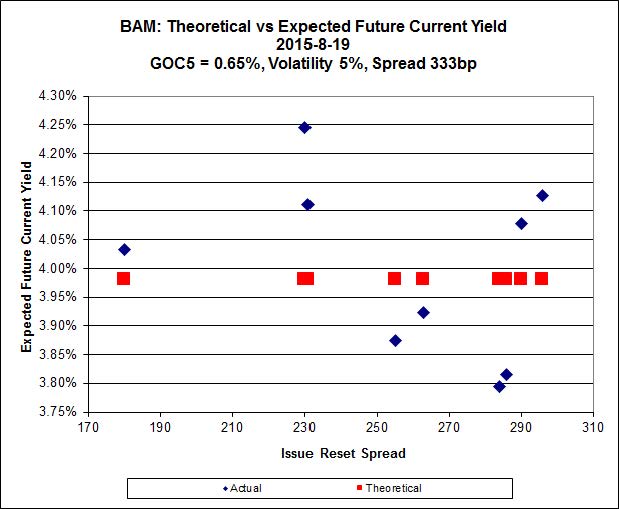

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 17.37 to be $1.16 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 22.99 and appears to be $1.07 rich.

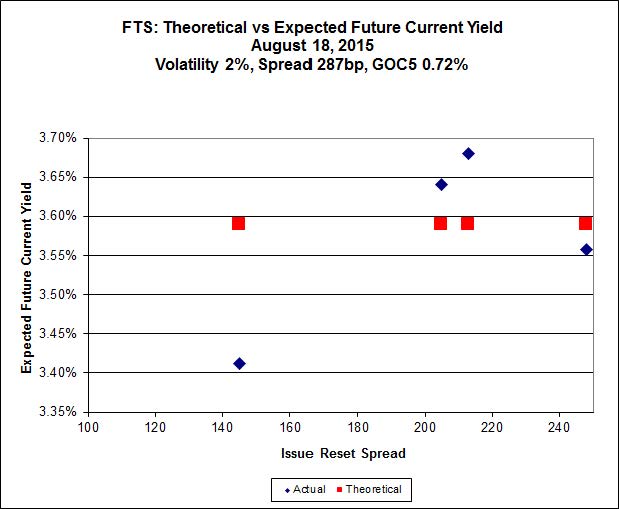

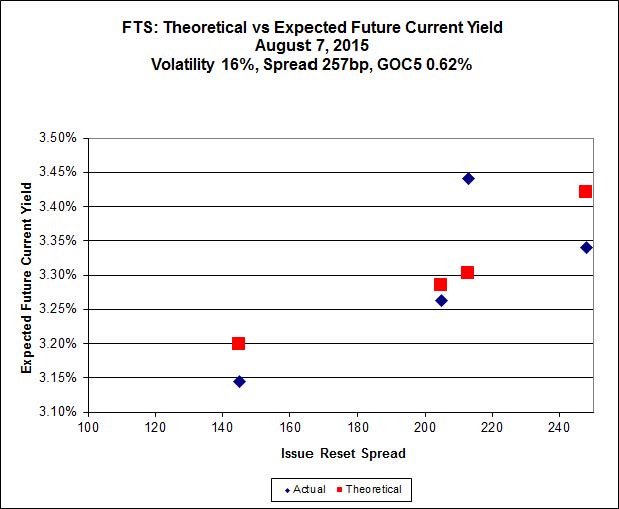

Click for Big

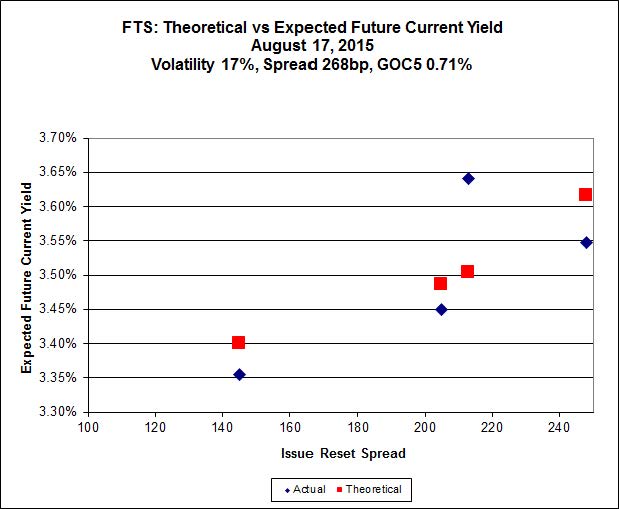

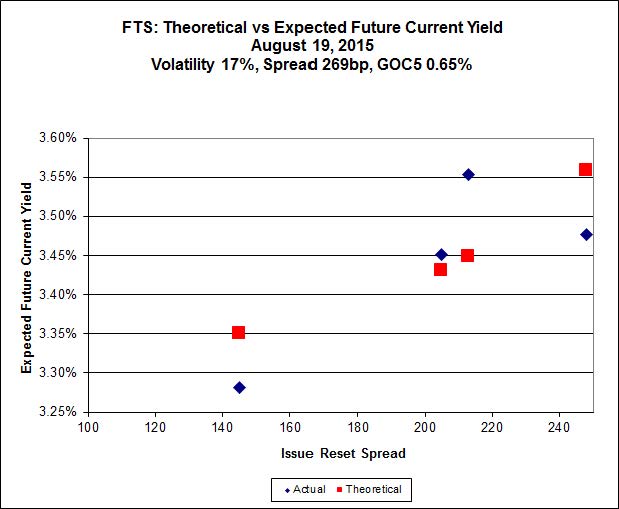

FTS.PR.M, with a spread of +248bp, and bid at 22.51, looks $0.52 expensive and resets 2019-12-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 19.56 and is $0.60 cheap.

Click for Big

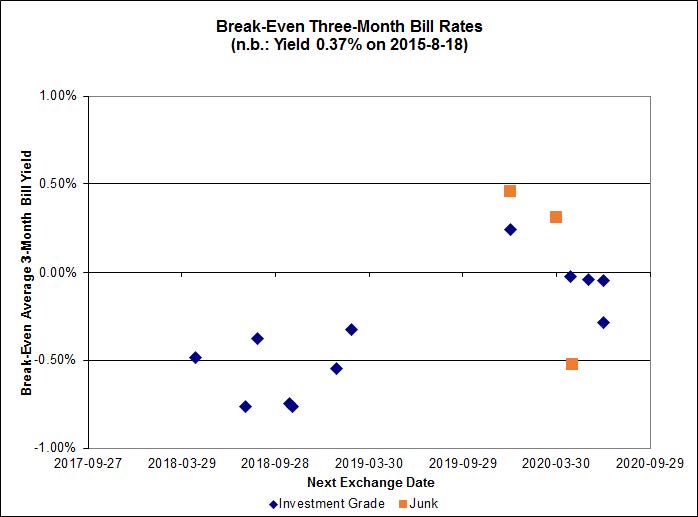

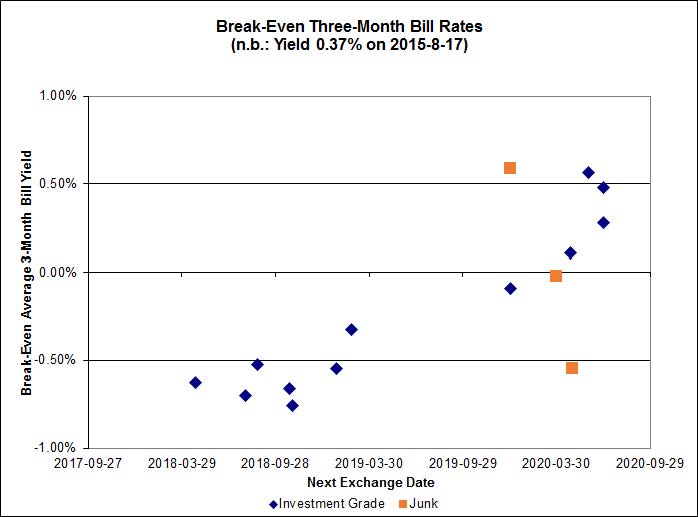

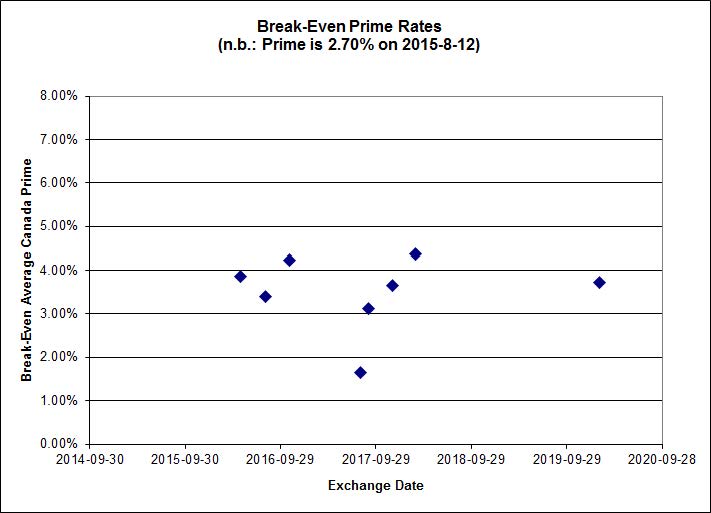

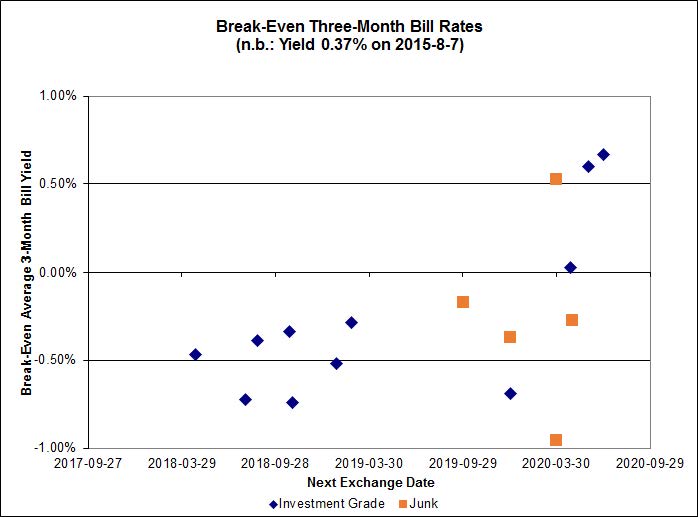

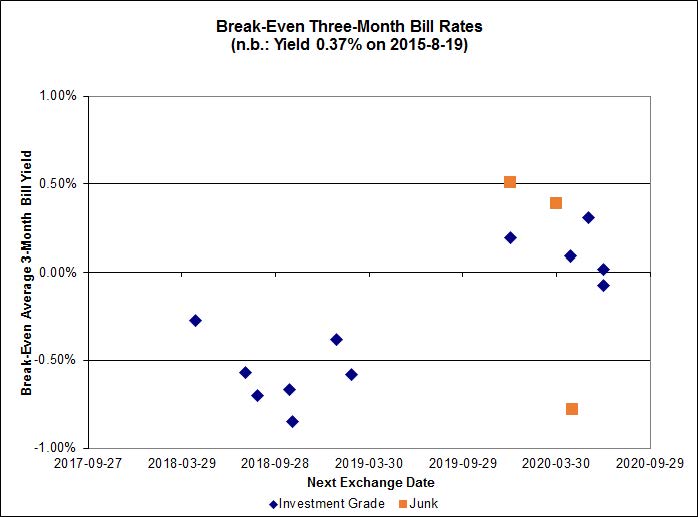

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.29%, with no outliers. Note that the distribution is bimodal, with NVCC non-compliant bank issues averaging -0.48% and the unregulated issues averaging +0.09%. There are three junk outliers below -1.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -3.5294 % | 1,867.5 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -3.5294 % | 3,265.2 |

| Floater | 3.93 % | 4.00 % | 55,061 | 17.37 | 3 | -3.5294 % | 1,985.3 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0217 % | 2,783.9 |

| SplitShare | 4.62 % | 5.04 % | 55,762 | 3.15 | 3 | 0.0217 % | 3,262.6 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0217 % | 2,545.6 |

| Perpetual-Premium | 5.71 % | 5.39 % | 60,202 | 2.05 | 9 | 0.1898 % | 2,488.9 |

| Perpetual-Discount | 5.42 % | 5.46 % | 78,136 | 14.70 | 29 | 0.1849 % | 2,607.2 |

| FixedReset | 4.82 % | 3.96 % | 190,573 | 15.83 | 87 | -0.7423 % | 2,187.9 |

| Deemed-Retractible | 5.11 % | 5.26 % | 96,347 | 5.43 | 34 | 0.1035 % | 2,586.3 |

| FloatingReset | 2.35 % | 3.37 % | 49,190 | 5.98 | 9 | -0.0548 % | 2,244.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BMO.PR.W | FixedReset | -5.50 % | See notes regarding Market Moronization. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 20.44 Evaluated at bid price : 20.44 Bid-YTW : 3.66 % |

| CM.PR.Q | FixedReset | -4.64 % | See notes regarding Market Moronization. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 22.18 Evaluated at bid price : 22.82 Bid-YTW : 3.71 % |

| BAM.PR.K | Floater | -4.39 % | See notes regarding Market Moronization. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 11.75 Evaluated at bid price : 11.75 Bid-YTW : 4.06 % |

| ENB.PR.H | FixedReset | -4.32 % | See notes regarding Market Moronization. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 14.18 Evaluated at bid price : 14.18 Bid-YTW : 5.13 % |

| BAM.PR.X | FixedReset | -4.16 % | See notes regarding Market Moronization. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 15.19 Evaluated at bid price : 15.19 Bid-YTW : 4.30 % |

| TD.PF.A | FixedReset | -3.89 % | See notes regarding Market Moronization. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 3.62 % |

| TD.PF.B | FixedReset | -3.71 % | See notes regarding Market Moronization. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 3.61 % |

| BAM.PF.E | FixedReset | -3.55 % | See notes regarding Market Moronization. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 20.65 Evaluated at bid price : 20.65 Bid-YTW : 4.21 % |

| TRP.PR.D | FixedReset | -3.31 % | See notes regarding Market Moronization. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 18.42 Evaluated at bid price : 18.42 Bid-YTW : 4.29 % |

| BAM.PR.B | Floater | -3.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 12.40 Evaluated at bid price : 12.40 Bid-YTW : 3.85 % |

| BAM.PR.C | Floater | -3.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 11.93 Evaluated at bid price : 11.93 Bid-YTW : 4.00 % |

| ENB.PR.D | FixedReset | -2.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 15.05 Evaluated at bid price : 15.05 Bid-YTW : 5.12 % |

| ENB.PR.Y | FixedReset | -2.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 16.06 Evaluated at bid price : 16.06 Bid-YTW : 4.95 % |

| RY.PR.Z | FixedReset | -2.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 21.32 Evaluated at bid price : 21.62 Bid-YTW : 3.44 % |

| TRP.PR.G | FixedReset | -2.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 4.18 % |

| CU.PR.C | FixedReset | -2.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 21.70 Evaluated at bid price : 22.15 Bid-YTW : 3.39 % |

| NA.PR.S | FixedReset | -2.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 21.88 Evaluated at bid price : 22.25 Bid-YTW : 3.53 % |

| NA.PR.W | FixedReset | -1.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 21.22 Evaluated at bid price : 21.22 Bid-YTW : 3.59 % |

| TD.PF.C | FixedReset | -1.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 21.28 Evaluated at bid price : 21.28 Bid-YTW : 3.55 % |

| MFC.PR.N | FixedReset | -1.98 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.31 Bid-YTW : 5.34 % |

| TRP.PR.B | FixedReset | -1.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 12.67 Evaluated at bid price : 12.67 Bid-YTW : 3.81 % |

| HSE.PR.E | FixedReset | -1.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 22.19 Evaluated at bid price : 22.81 Bid-YTW : 4.65 % |

| CM.PR.P | FixedReset | -1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 21.13 Evaluated at bid price : 21.13 Bid-YTW : 3.59 % |

| PWF.PR.K | Perpetual-Discount | -1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 22.56 Evaluated at bid price : 22.82 Bid-YTW : 5.46 % |

| PWF.PR.T | FixedReset | -1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 22.64 Evaluated at bid price : 23.44 Bid-YTW : 3.29 % |

| ENB.PR.B | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 14.55 Evaluated at bid price : 14.55 Bid-YTW : 5.27 % |

| PWF.PR.P | FixedReset | -1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 16.74 Evaluated at bid price : 16.74 Bid-YTW : 3.28 % |

| HSE.PR.C | FixedReset | -1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 21.77 Evaluated at bid price : 22.15 Bid-YTW : 4.41 % |

| BAM.PR.T | FixedReset | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 4.26 % |

| POW.PR.D | Perpetual-Discount | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 22.60 Evaluated at bid price : 22.85 Bid-YTW : 5.53 % |

| MFC.PR.J | FixedReset | 1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.83 Bid-YTW : 4.52 % |

| FTS.PR.G | FixedReset | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 19.56 Evaluated at bid price : 19.56 Bid-YTW : 3.66 % |

| ENB.PR.F | FixedReset | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 15.70 Evaluated at bid price : 15.70 Bid-YTW : 5.13 % |

| CU.PR.D | Perpetual-Discount | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 22.18 Evaluated at bid price : 22.53 Bid-YTW : 5.44 % |

| CU.PR.E | Perpetual-Discount | 1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 22.12 Evaluated at bid price : 22.44 Bid-YTW : 5.46 % |

| RY.PR.W | Perpetual-Discount | 1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 24.30 Evaluated at bid price : 24.61 Bid-YTW : 4.99 % |

| FTS.PR.J | Perpetual-Discount | 1.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 22.31 Evaluated at bid price : 22.70 Bid-YTW : 5.23 % |

| ELF.PR.H | Perpetual-Discount | 2.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 23.75 Evaluated at bid price : 24.21 Bid-YTW : 5.73 % |

| FTS.PR.K | FixedReset | 2.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 19.56 Evaluated at bid price : 19.56 Bid-YTW : 3.64 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| CM.PR.O | FixedReset | 194,658 | RBC bought blocks of 12,000 and 10,300 from anonymous, both at 22.70. TD crossed 100,000 at 22.72 and another 25,000 at 22.70. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 22.13 Evaluated at bid price : 22.65 Bid-YTW : 3.37 % |

| MFC.PR.G | FixedReset | 54,307 | Desjardins crossed 50,000 at 24.02. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.10 Bid-YTW : 4.02 % |

| BMO.PR.T | FixedReset | 48,858 | RBC bought 10,000 from CIBC at 22.21. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 21.83 Evaluated at bid price : 22.20 Bid-YTW : 3.36 % |

| TD.PF.F | Perpetual-Discount | 47,876 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 23.98 Evaluated at bid price : 24.33 Bid-YTW : 5.07 % |

| CM.PR.P | FixedReset | 37,770 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 21.13 Evaluated at bid price : 21.13 Bid-YTW : 3.59 % |

| TRP.PR.C | FixedReset | 37,149 | RBC crossed 28,900 at 13.45. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-19 Maturity Price : 13.29 Evaluated at bid price : 13.29 Bid-YTW : 4.03 % |

| There were 45 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| CM.PR.Q | FixedReset | Quote: 22.82 – 24.05 Spot Rate : 1.2300 Average : 0.7592 YTW SCENARIO |

| BAM.PF.E | FixedReset | Quote: 20.65 – 21.75 Spot Rate : 1.1000 Average : 0.6580 YTW SCENARIO |

| MFC.PR.L | FixedReset | Quote: 20.80 – 21.84 Spot Rate : 1.0400 Average : 0.6711 YTW SCENARIO |

| FTS.PR.F | Perpetual-Discount | Quote: 22.75 – 23.60 Spot Rate : 0.8500 Average : 0.5699 YTW SCENARIO |

| MFC.PR.N | FixedReset | Quote: 21.31 – 22.10 Spot Rate : 0.7900 Average : 0.5173 YTW SCENARIO |

| CU.PR.C | FixedReset | Quote: 22.15 – 22.99 Spot Rate : 0.8400 Average : 0.5855 YTW SCENARIO |