Pressure on the loonie may lead to pressure on Canadian policy rates:

The outlook for the Canadian dollar just got worse.

The currency has slumped to a three-month low amid declining prices for oil, the nation’s largest export. That’s adding to pressure on the Bank of Canada to cut interest rates after a report Tuesday showed the country posted its second-largest trade deficit ever, led by tumbling exports.

…

Twenty-eight percent of economists surveyed by Bloomberg June 30 to July 2 see the Bank of Canada lowering its benchmark rate from 0.75 percent when it meets next week. That up from 6 percent of participants in a survey conducted June 5-10.

Matt Levine complains that front-running is a phrase that is losing all meaning and points out that it is really … selling liquidity:

The people who bought the stock on Tuesday and sold it to the index funds on Friday performed a market-making function: They knew that there would be a lot of concentrated demand for stock on one day, they knew there wouldn’t be enough “natural” supply to meet that demand, and so they spread that demand backwards in time by buying ahead of the big demand event. They — it’s become a dirty phrase by now, but here it is — supplied liquidity. And they got paid for doing it.4 But trading ahead of anticipated demand looks a lot like front-running, for some definition of front-running,5 so they look a little like villains. Even if they actually helped their supposed victims.

…

One of my little stock-market obsessions is that index funds free-ride on the work done by active investors. Someone needs to make decisions that allocate capital to businesses. A world in which everyone indexes, and in which no one thinks that active managers should be able to charge for their services, is a world that will spend too little time and effort on allocating capital to the right businesses.

…

The index funds have the advantage of free-riding, but the disadvantage of being predictable. Stocks should go up when they join an index. That’s the price that the index funds pay to active traders for picking stocks. Stock picking is valuable; active investors pay for it in fees, while passive investors pay for it in, you know, front-running or whatever.

I have often written about a so-called ‘meta-index’ which would include issues on their announcement date, rather than their effective date. Stocks added to indices tend to rise during the interim period, while deletions fall. The purpose of having the intervening time is to smooth the trading through the change, in order to give index funds a better chance of equalling their benchmark; a side effect is that the index itself underperforms its meta-index through this period. And, it would seem, this has finally attracted some notice:

The traders are simply buying stocks before they’re added to the indexes that, by definition, index funds must track.

As the popularity of index investing soars to new heights, the emergence of index front-running is raising fundamental questions about so-called passive investment strategies, as well as how indexes are compiled and the role the funds themselves play in elevating costs. By one estimate, it gouges owners of funds tracking the Standard & Poor’s 500 Index to the tune of $4.3 billion a year, a sum that can double or even triple the cost of such investments.

“Portfolio managers are aware of it, but some of them will say ‘My clients demand an index fund, and I’m going to give it to them come hell or high water,’” Michael Rawson, an analyst at Morningstar Inc., said from Chicago. “Yes, you matched the index return, but the investor is now worse off. You don’t hear about that as much.”

…

Over a course of a year, front-running — of stocks going into and coming out of indexes — costs investors in S&P 500 tracker funds at least 0.2 percentage points, according to research published last year by Winton Capital Management Ltd., a quantitative hedge fund that analyzed data from 1990 to 2011. That’s equal to $4.3 billion in lost income in 2014.A study in 2008 by Antti Petajisto, now a money manager at BlackRock Inc., estimated the impact could boost the expense of owning an index fund by as much as 0.28 percentage points.

…

Petajisto and Morningstar’s Rawson also suggest passive funds that buy the entire market can minimize the damage of front-running. By owning almost every stock, there’s barely anything for arbitragers to buy first.Vanguard’s $411 billion Total Stock Market Index Fund is the most prominent example. In the past decade, it has returned 8.2 percent a year, beating the firm’s own S&P 500 tracker fund by 0.4 percentage points, data compiled by Morningstar show.

The Greek situation looks like it’s passed the table-thumping stage and has reached the ‘take it or leave it’ stage:

After five months of drama, false dawns and unpleasant surprises, Europe’s leaders are finally ready to show Alexis Tsipras the exit.

Behind the doors of the Justus Lipsius building in the heart of the political district in Brussels, the euro-region’s leaders rounded on the Greek prime minister for destabilizing the currency union before Germany’s Angela Merkel emerged to deliver an official ultimatum.

In a tense and at times emotional meeting, Tsipras’s European peers told him he’d failed to appreciate the efforts the continent’s voters and taxpayers had made to help the Greek people and blamed him for escalating tensions across the region.

The Chinese have developed a novel method of preventing stock market declines:

A wave of Chinese companies halted trading in their shares and regulators unveiled new measures to prop up the value of small-cap stocks in the latest attempts to stem a rout that’s wiped more than $3.5 trillion of value.

At least 1,249 companies have halted trading on mainland Chinese exchanges, locking up $2.2 trillion of shares, or about 33 percent of China’s market capitalization.

It didn’t help much:

China’s Shanghai Composite Index plunged amid concern a raft of measures to stabilize equities is failing to stop the bear-market rout as traders unwind margin bets at a record pace.

The Shanghai Composite tumbled as much as 8.2 percent, the most since 2007, before paring losses to 4.8 percent to trade at 3,549.92 at 9:56 a.m. local time. There were four gainers among the 1,106 stocks that trade on the benchmark gauge, which has slumped 28 percent since the June peak. PetroChina Co., the biggest stock, tumbled 4.9 percent as nine out of 10 industry gauges dropped at least 4 percent in the CSI 300 Index.

In the latest attempts to stem losses, the government raised margin requirements for CSI 500 Index futures, while the China Securities Finance Corp. will buy more shares of smaller companies. About 43 percent of the stock market is frozen after more than a thousand companies suspended their shares.

It was a violently mixed day for the Canadian preferred share market, with PerpetualDiscounts up 25bp, FixedResets off 53bp and DeemedRetractibles gaining 23bp. Floaters got hammered. The lengthy Performance Highlights table is dominated by losing FixedResets, with a few winning Straights mixed in. Volume was above average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

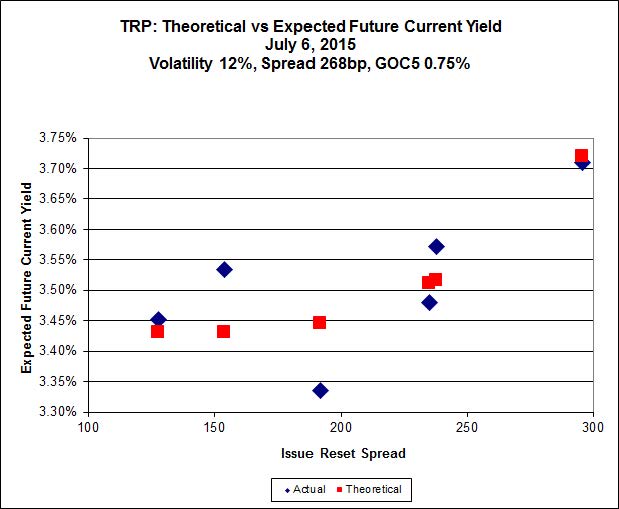

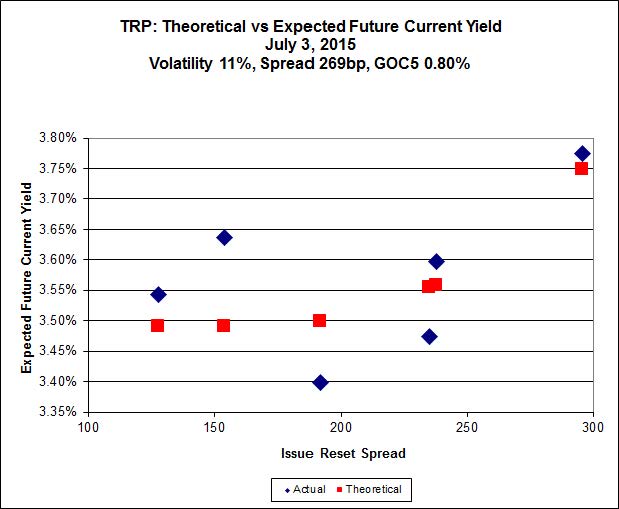

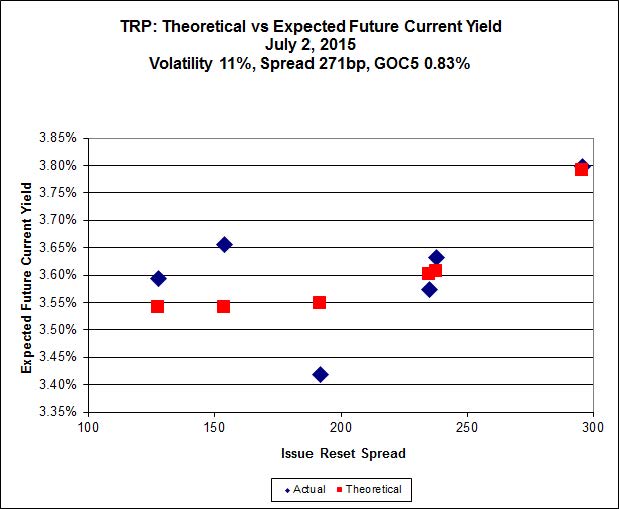

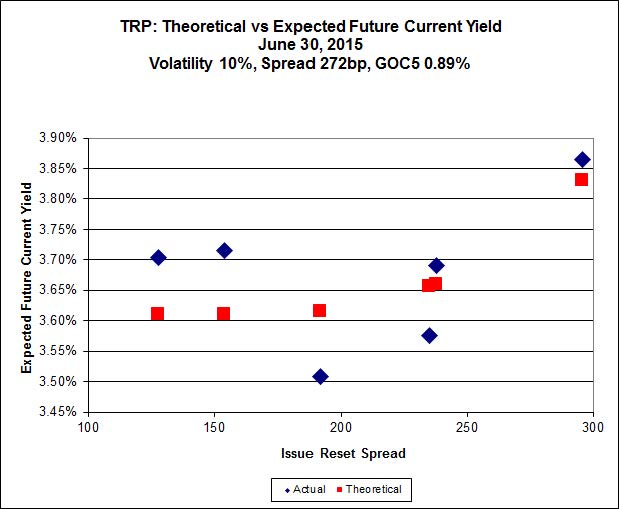

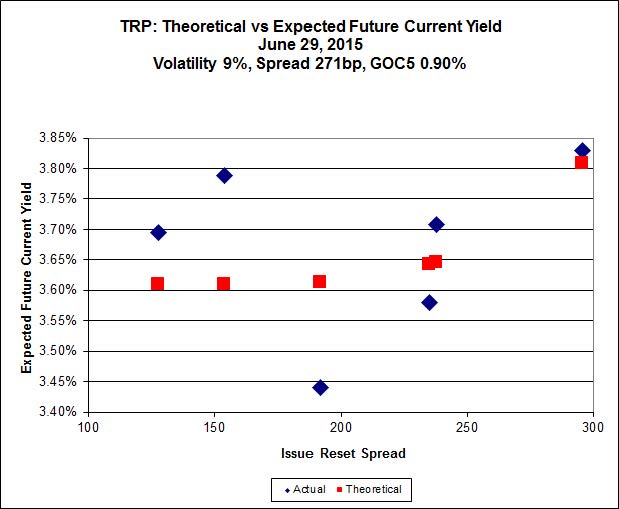

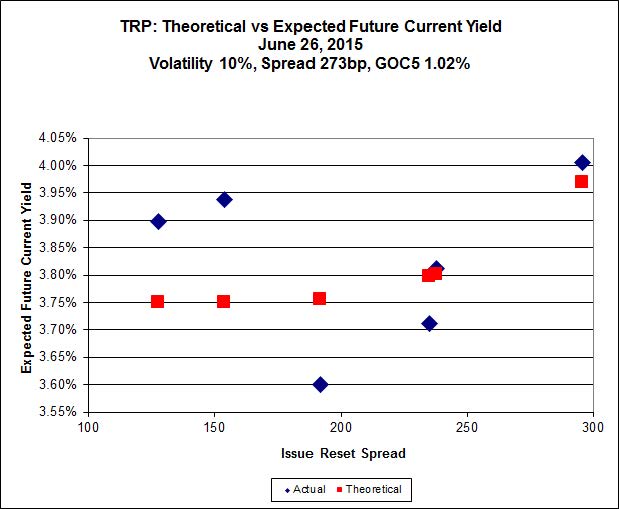

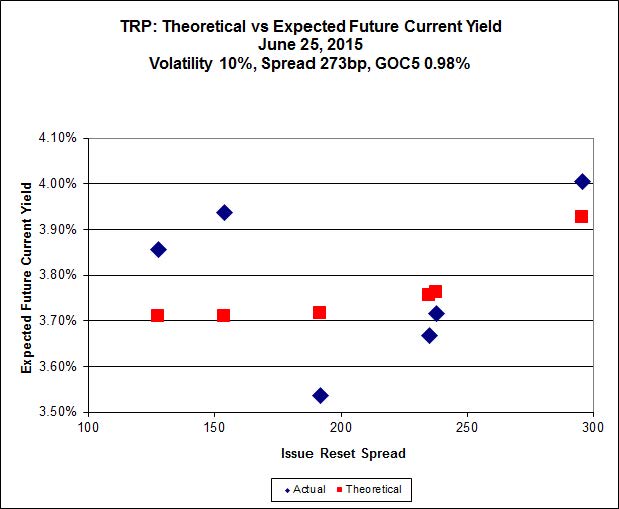

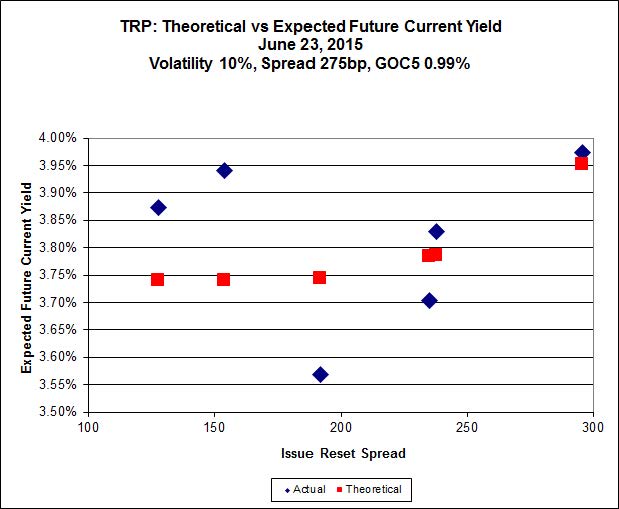

Here’s TRP:

Click for Big

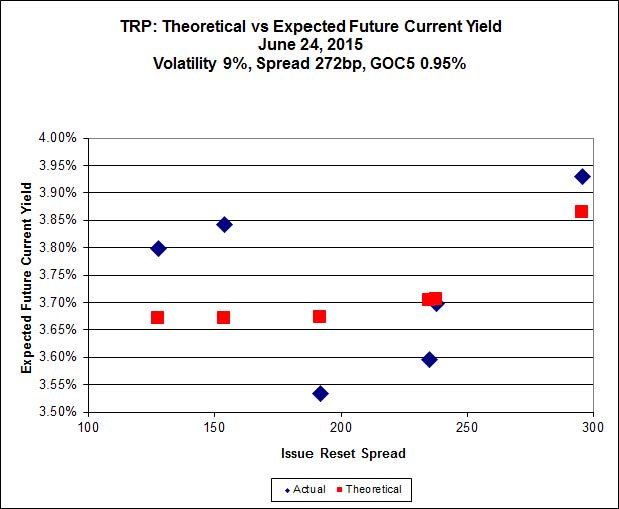

TRP.PR.A, which resets 2019-12-31 at +192, is bid at 19.99 to be $0.59 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.47 cheap at its bid price of 16.27.

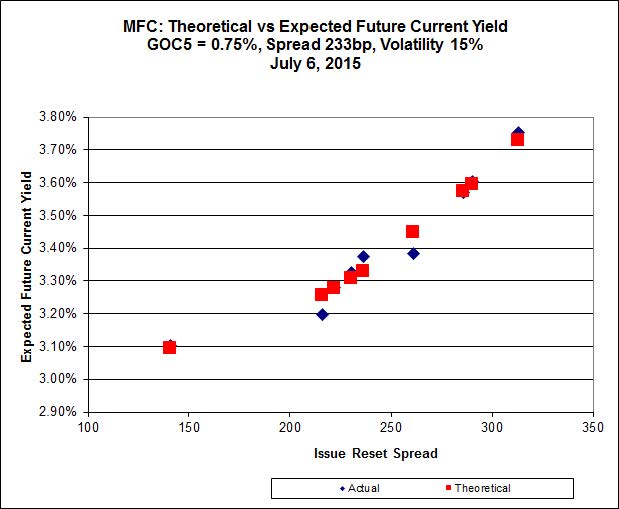

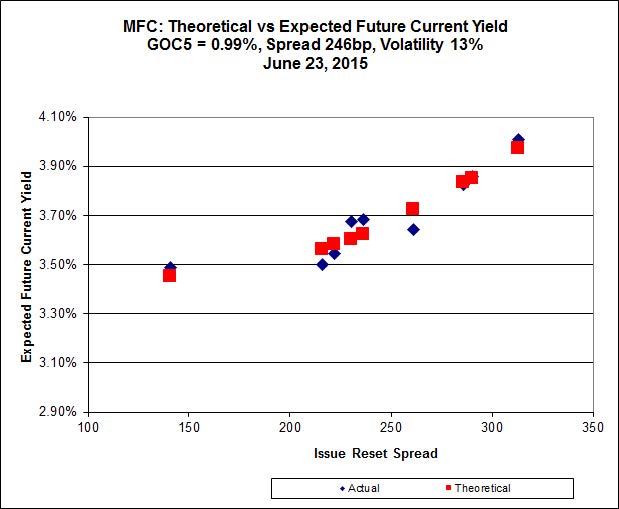

Click for Big

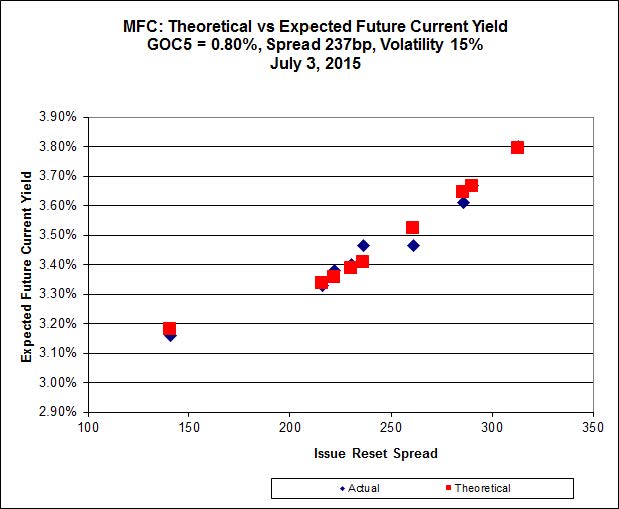

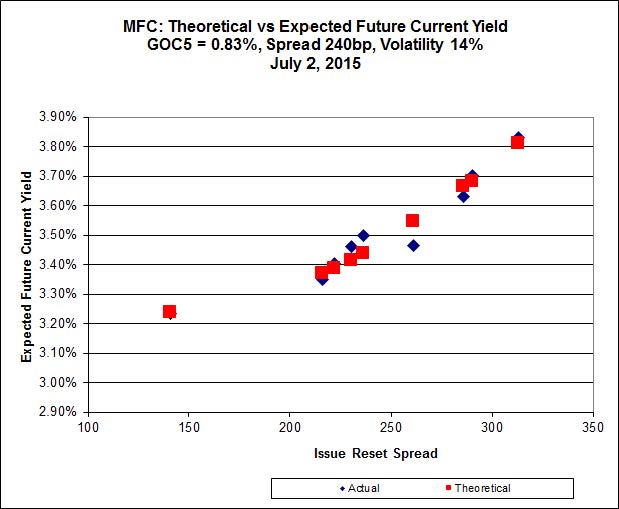

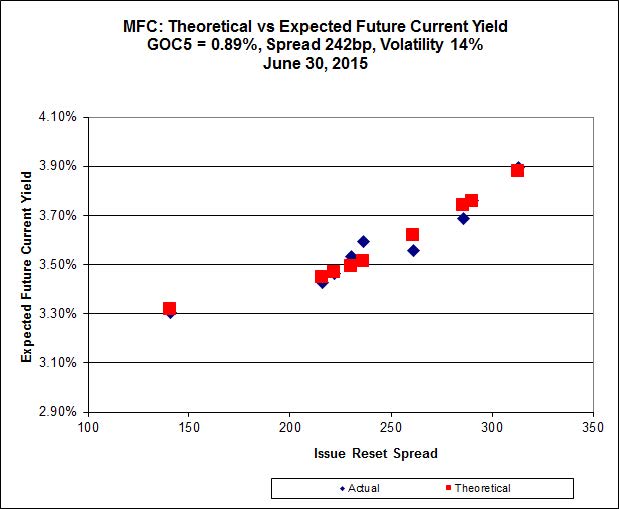

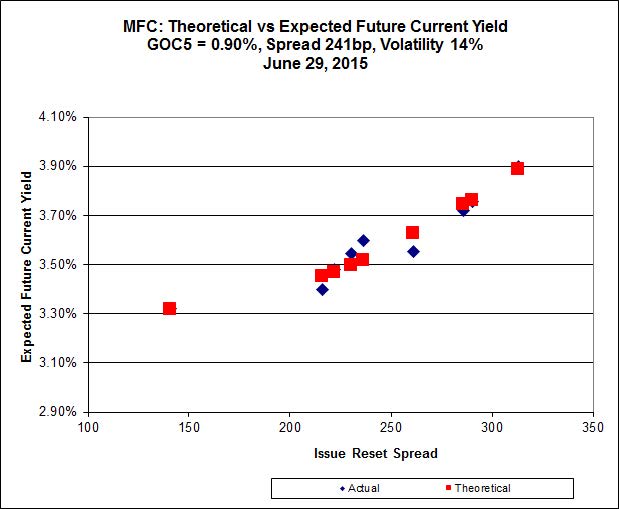

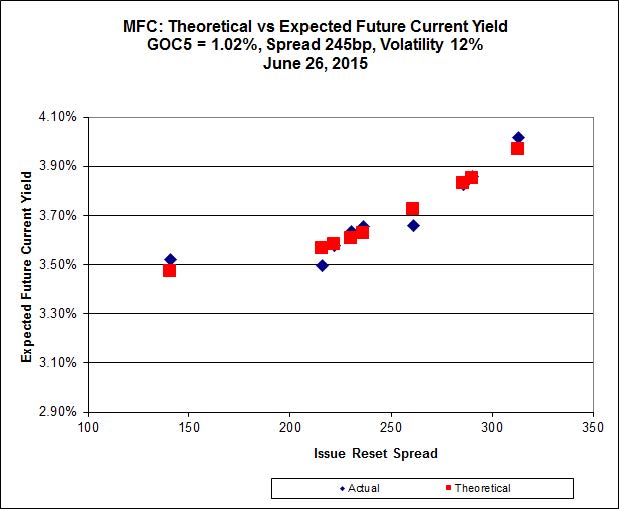

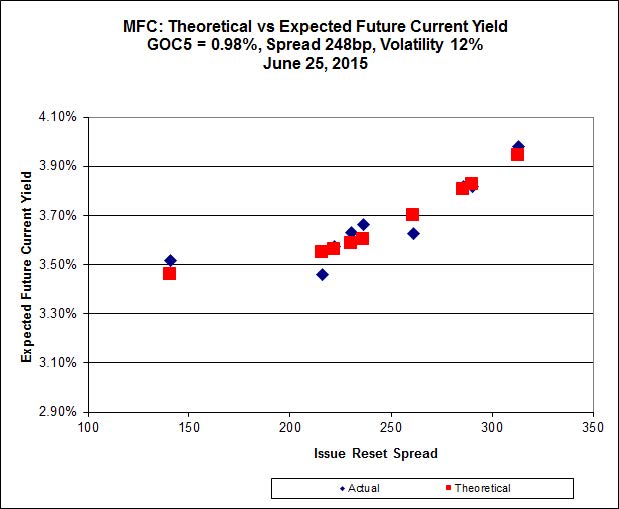

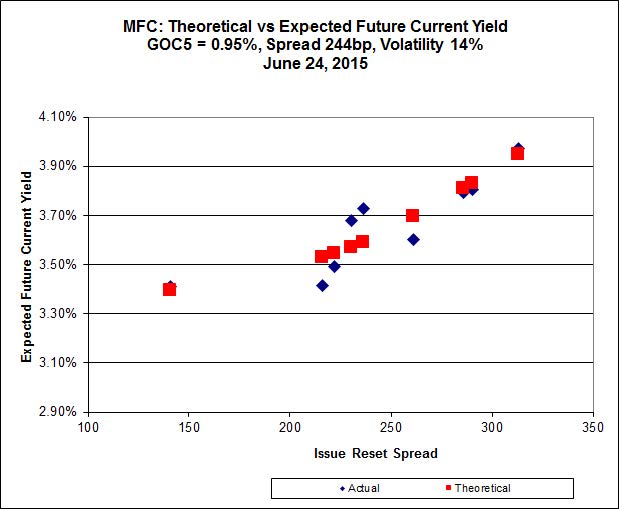

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.J, resetting at +261bp on 2018-3-19, bid at 24.60 to be $0.33 rich, while MFC.PR.K, resetting at +222bp on 2018-9-19, is bid at 22.23 to be $0.29 cheap.

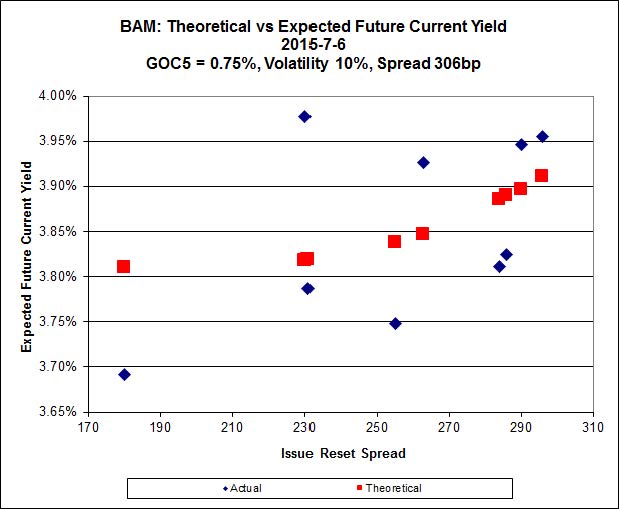

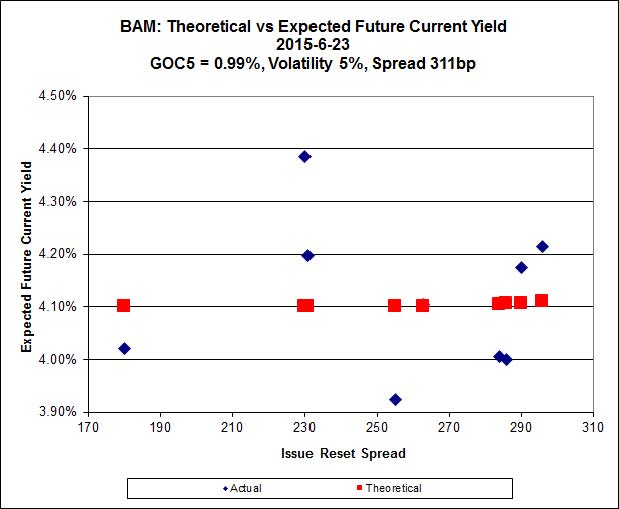

Click for Big

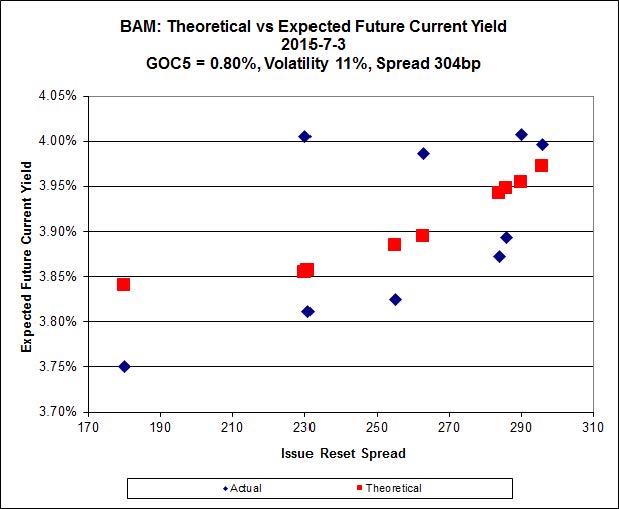

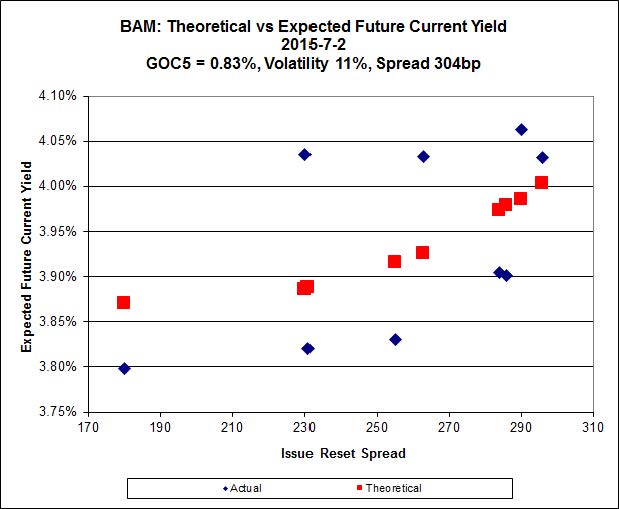

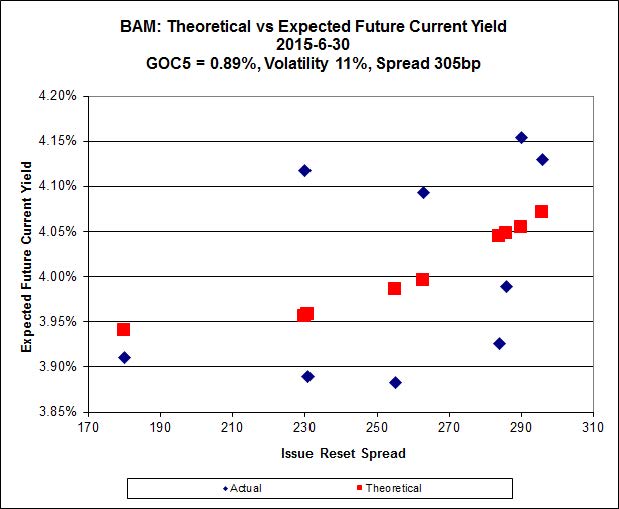

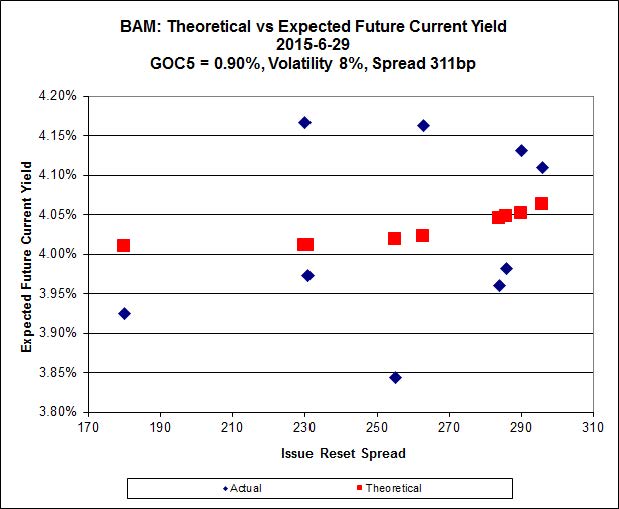

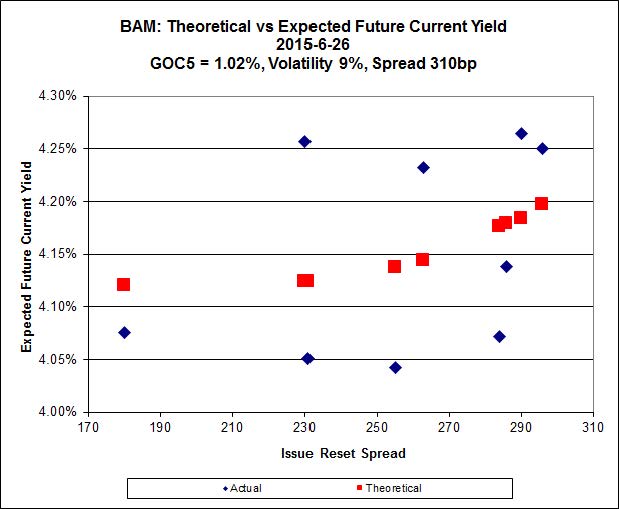

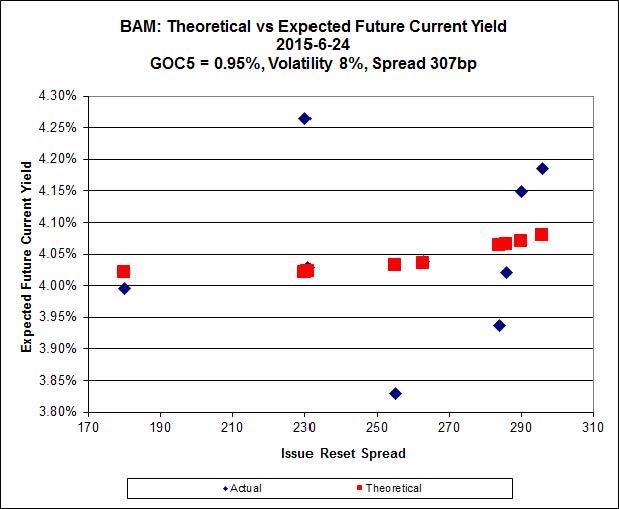

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 19.31 to be $0.81 cheap. BAM.PF.G, resetting at +284bp 2020-6-30 is bid at 23.45 and appears to be $0.70 rich.

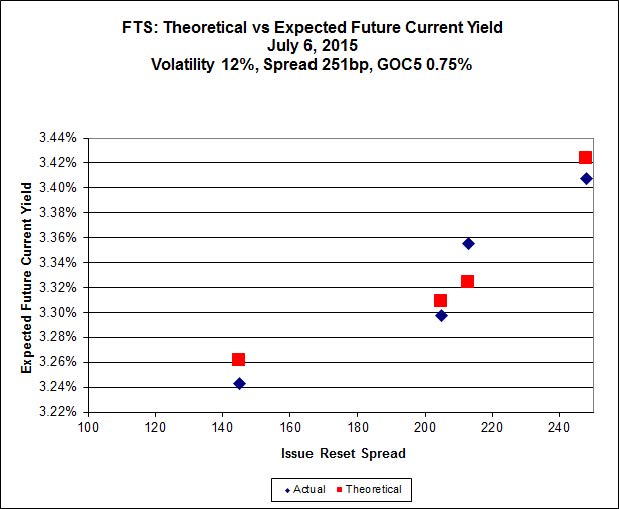

Click for Big

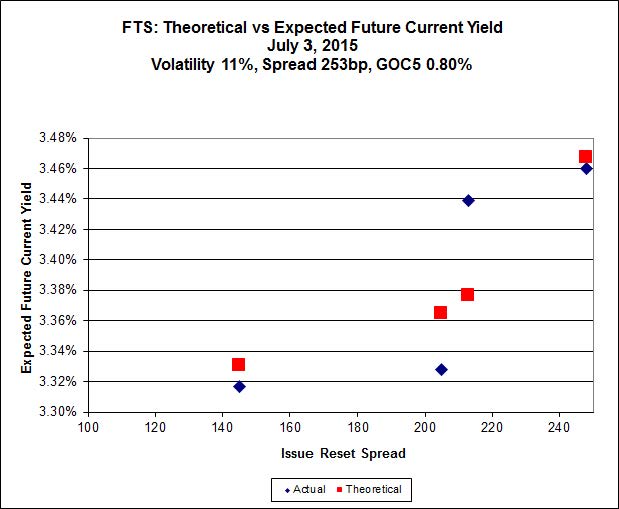

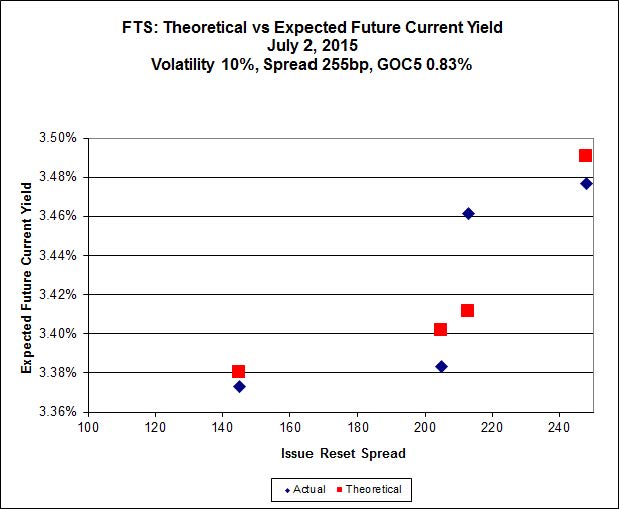

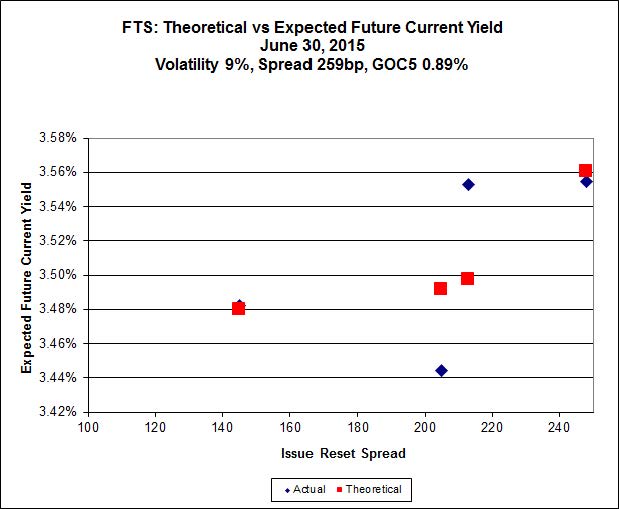

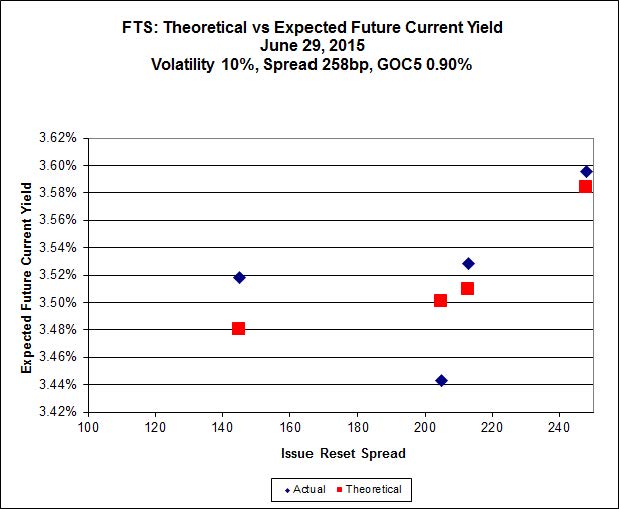

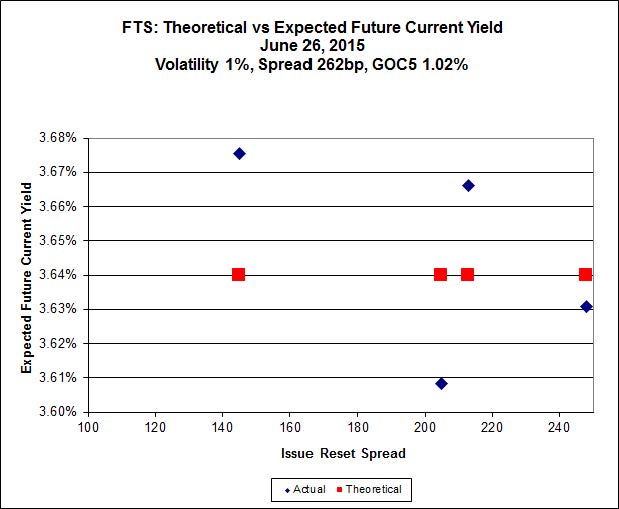

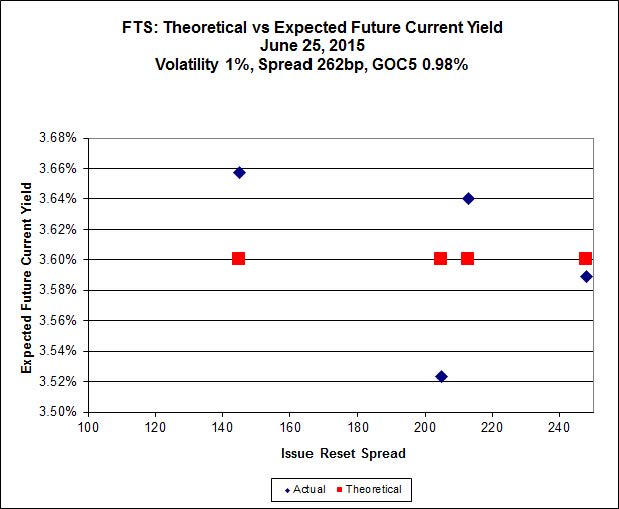

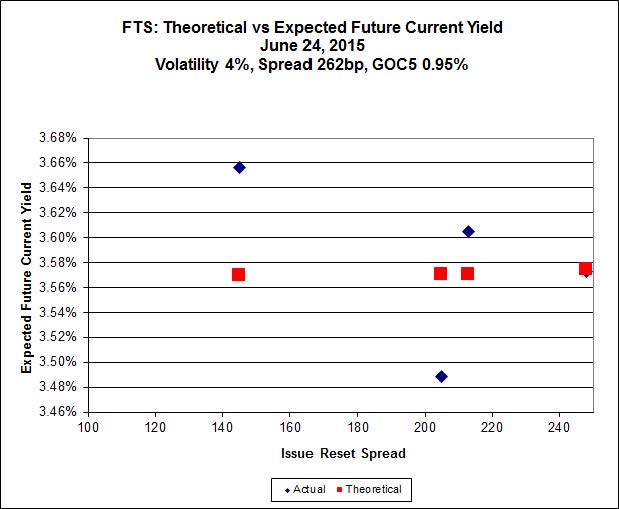

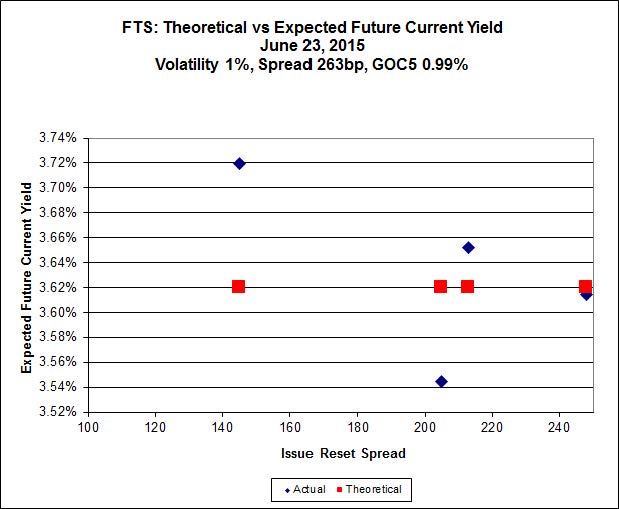

FTS.PR.G, with a spread of +213bp, and bid at 21.54, looks $0.19 cheap and resets 2018-9-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 21.34 and is $0.12 rich.

Click for Big

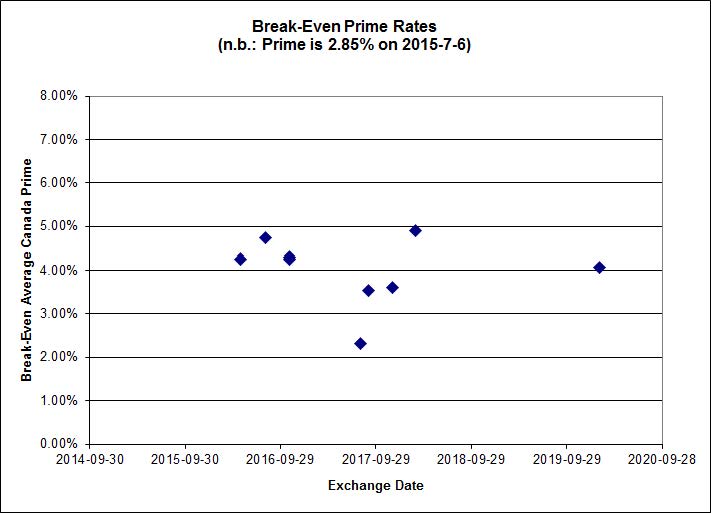

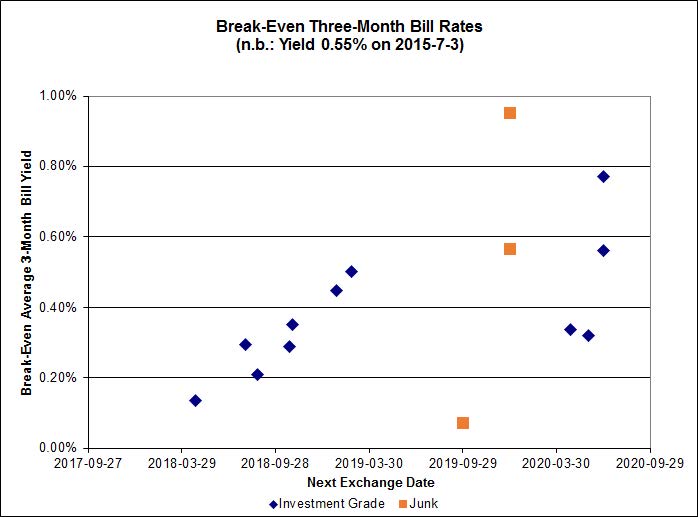

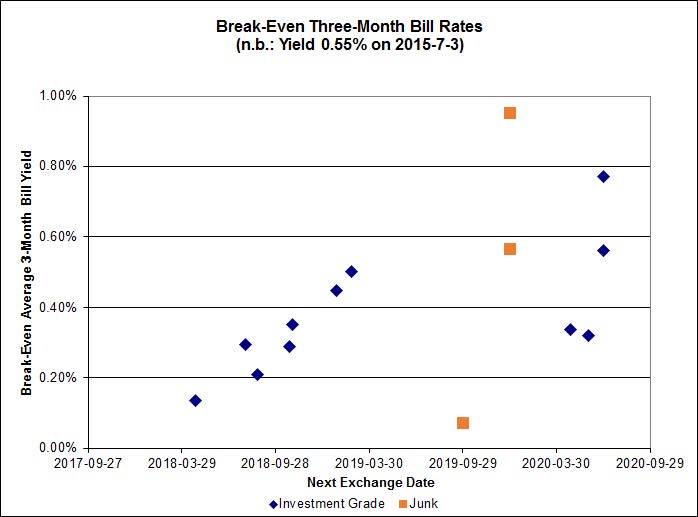

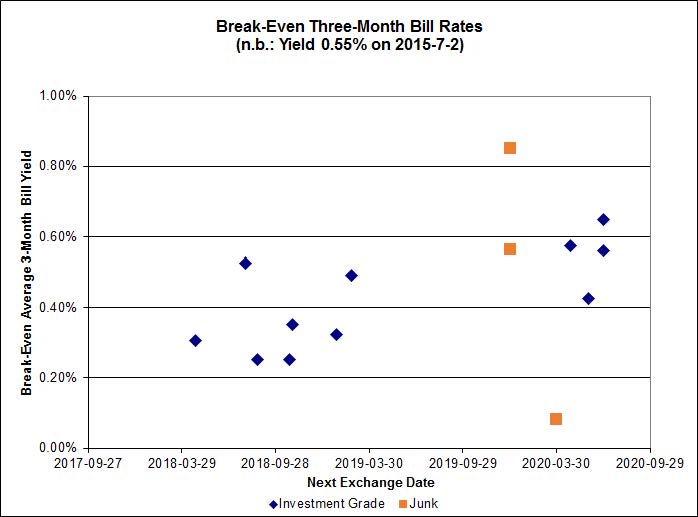

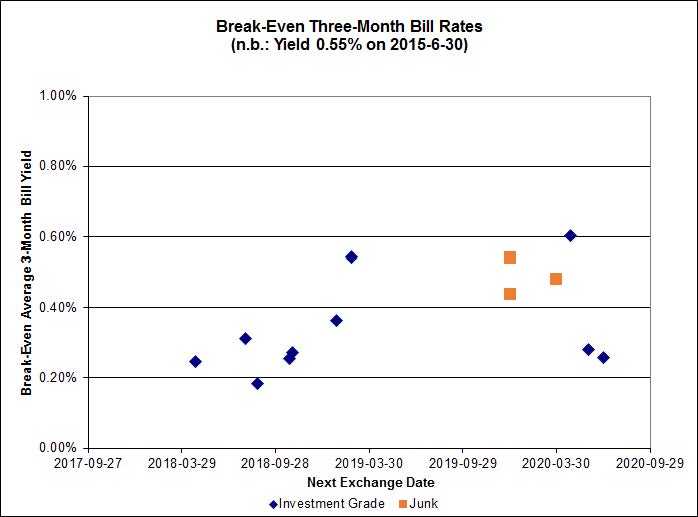

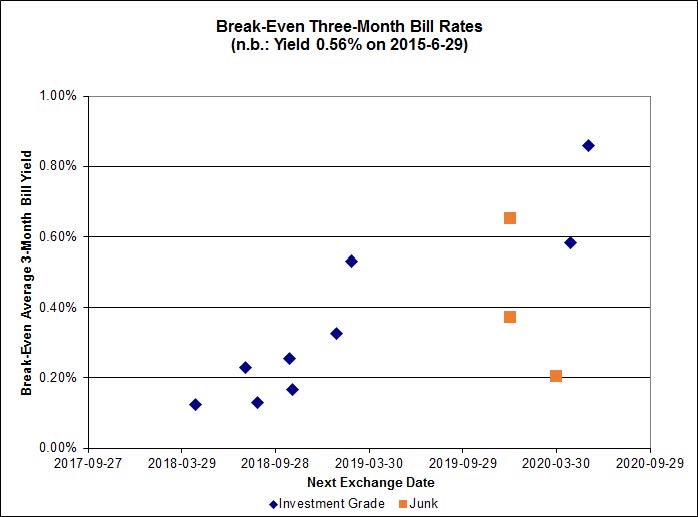

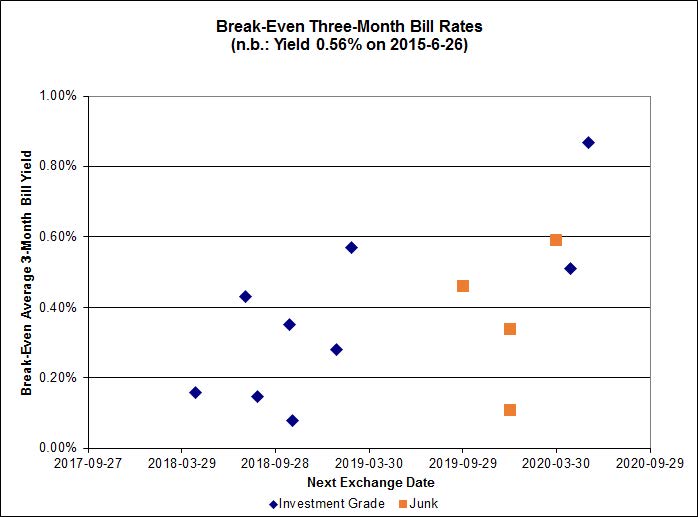

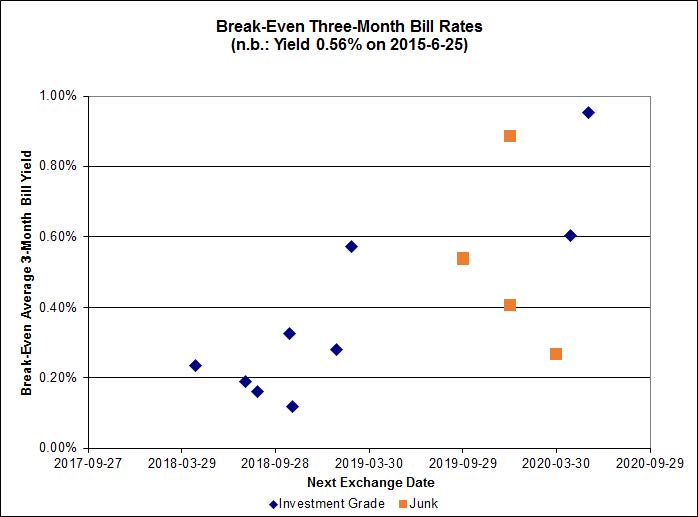

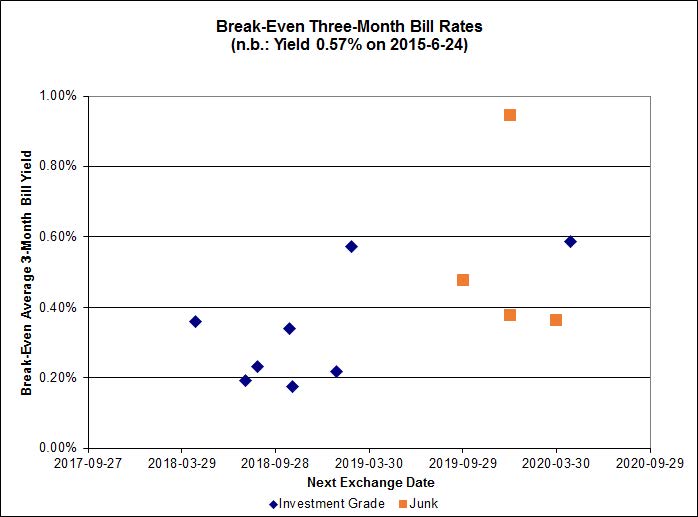

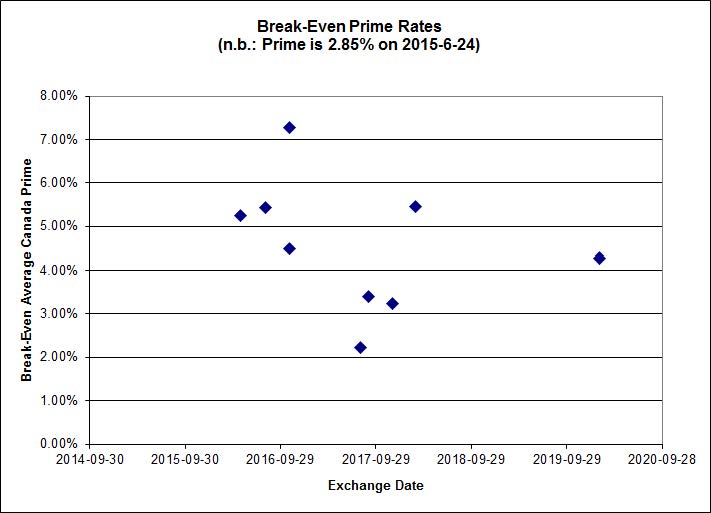

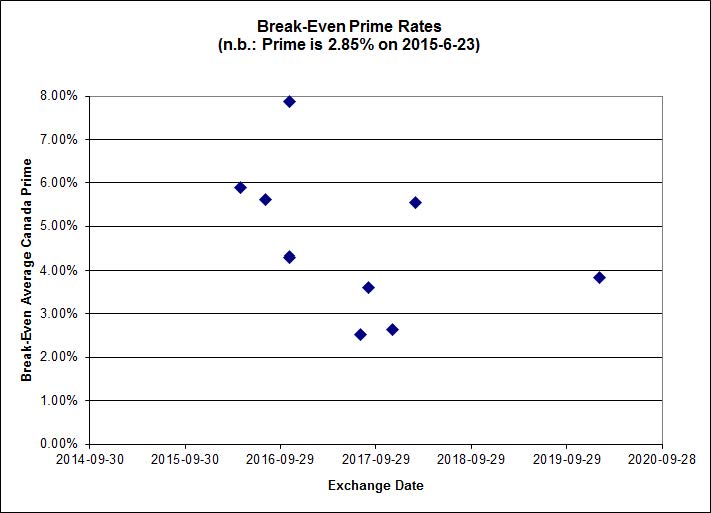

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of about 0.15%, including the outliers TRP.PR.A / TRP.PR.F at -0.07%, BMO.PR.M / BMO.PR.R at -0.01%, BNS.PR.Q / BNS.PR.B at -0.21% and TRP.PR.B / TRP.PR.H at -0.67% (note that the bid price for TRP.PR.H is silly). On the junk side, three of the six pairs are outliers, two pairs with negative break-even yields, and one above 1.00%.

Click for Big

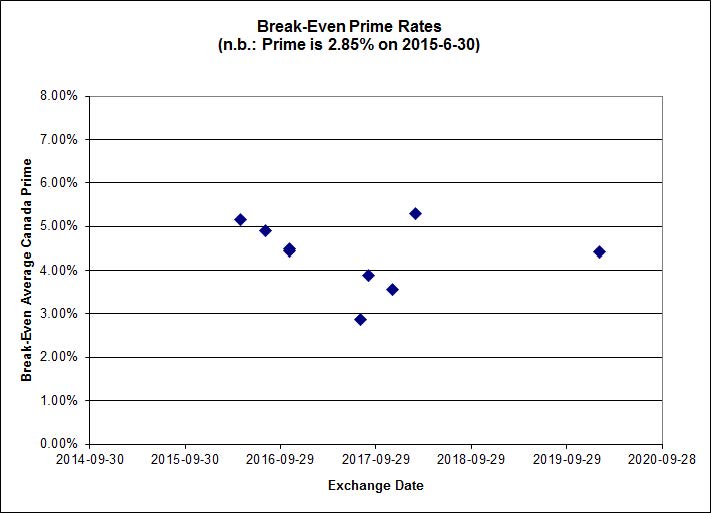

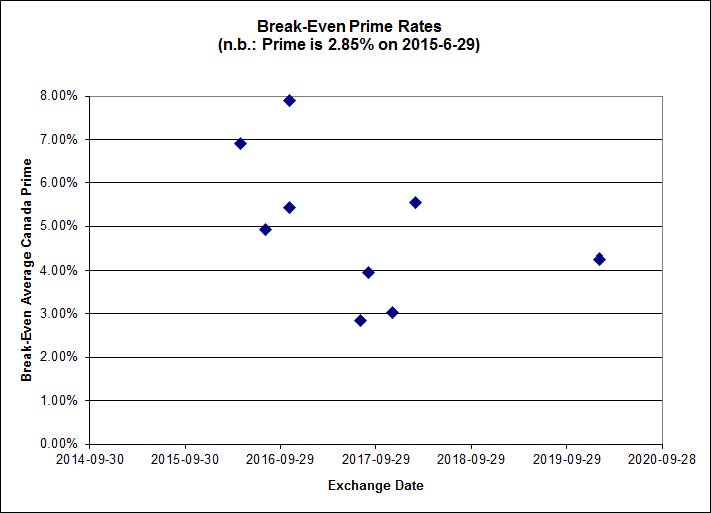

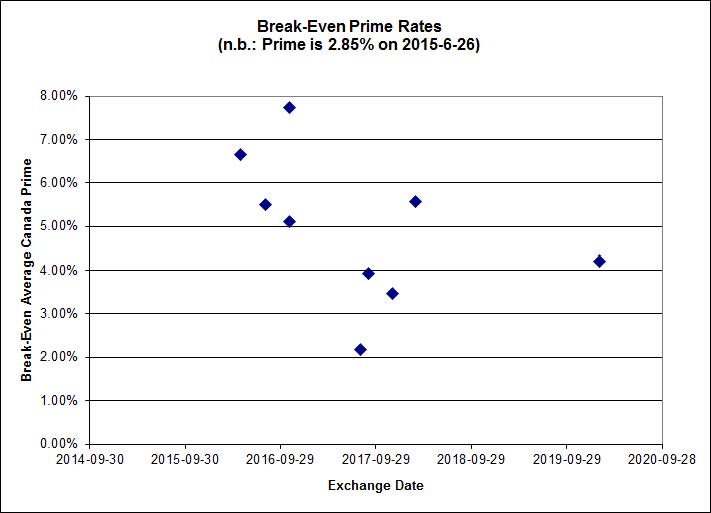

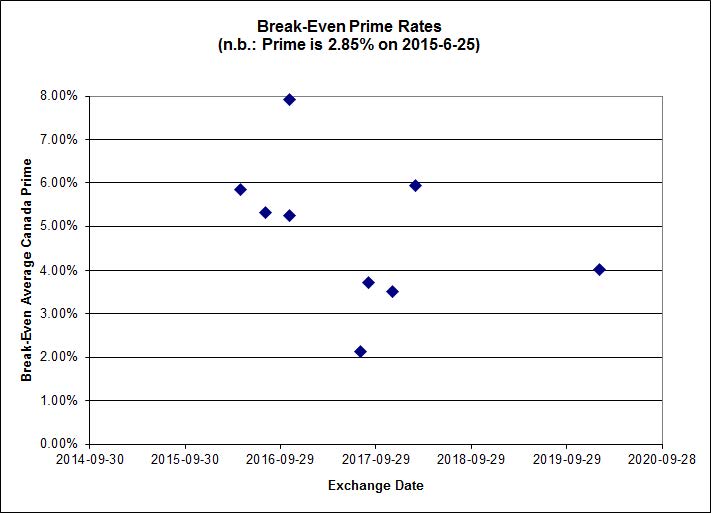

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.8700 % | 2,172.9 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.8700 % | 3,799.2 |

| Floater | 3.56 % | 3.62 % | 59,926 | 18.28 | 3 | -1.8700 % | 2,309.9 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0537 % | 2,770.3 |

| SplitShare | 4.59 % | 4.96 % | 62,085 | 3.23 | 3 | 0.0537 % | 3,246.7 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0537 % | 2,533.2 |

| Perpetual-Premium | 5.46 % | 3.61 % | 64,464 | 0.31 | 13 | 0.1298 % | 2,519.7 |

| Perpetual-Discount | 5.31 % | 5.21 % | 93,109 | 14.85 | 21 | 0.2454 % | 2,691.9 |

| FixedReset | 4.54 % | 3.58 % | 213,378 | 16.30 | 88 | -0.5323 % | 2,317.6 |

| Deemed-Retractible | 4.99 % | 3.15 % | 106,291 | 0.79 | 34 | 0.2349 % | 2,634.8 |

| FloatingReset | 2.50 % | 2.95 % | 52,719 | 6.09 | 10 | -0.6437 % | 2,305.5 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.H | FloatingReset | -7.99 % | Very misleading, as the low for the day was 14.35 on volume of 3,140 shares, so this is just more Toronto Stock Exchange nonsense. I have not checked whether this is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 13.25 Evaluated at bid price : 13.25 Bid-YTW : 3.42 % |

| ENB.PF.G | FixedReset | -3.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 19.65 Evaluated at bid price : 19.65 Bid-YTW : 4.77 % |

| BAM.PR.Z | FixedReset | -2.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 22.41 Evaluated at bid price : 22.86 Bid-YTW : 4.23 % |

| TD.PF.A | FixedReset | -2.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 22.00 Evaluated at bid price : 22.49 Bid-YTW : 3.50 % |

| MFC.PR.L | FixedReset | -2.29 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.23 Bid-YTW : 4.87 % |

| BAM.PR.B | Floater | -2.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 14.28 Evaluated at bid price : 14.28 Bid-YTW : 3.51 % |

| HSE.PR.A | FixedReset | -2.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 15.92 Evaluated at bid price : 15.92 Bid-YTW : 4.07 % |

| ENB.PR.J | FixedReset | -2.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 19.10 Evaluated at bid price : 19.10 Bid-YTW : 4.69 % |

| NA.PR.S | FixedReset | -1.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 22.58 Evaluated at bid price : 23.40 Bid-YTW : 3.48 % |

| BAM.PR.C | Floater | -1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 13.85 Evaluated at bid price : 13.85 Bid-YTW : 3.62 % |

| MFC.PR.K | FixedReset | -1.77 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.23 Bid-YTW : 4.78 % |

| VNR.PR.A | FixedReset | -1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 22.85 Evaluated at bid price : 23.15 Bid-YTW : 3.94 % |

| PWF.PR.P | FixedReset | -1.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 17.91 Evaluated at bid price : 17.91 Bid-YTW : 3.43 % |

| ENB.PF.E | FixedReset | -1.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 19.51 Evaluated at bid price : 19.51 Bid-YTW : 4.77 % |

| GWO.PR.N | FixedReset | -1.54 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.58 Bid-YTW : 7.12 % |

| BAM.PF.A | FixedReset | -1.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 22.27 Evaluated at bid price : 22.77 Bid-YTW : 4.16 % |

| BAM.PR.K | Floater | -1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 13.85 Evaluated at bid price : 13.85 Bid-YTW : 3.62 % |

| ENB.PR.P | FixedReset | -1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 18.28 Evaluated at bid price : 18.28 Bid-YTW : 4.72 % |

| BMO.PR.W | FixedReset | -1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 21.92 Evaluated at bid price : 22.37 Bid-YTW : 3.53 % |

| ENB.PR.F | FixedReset | -1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 17.94 Evaluated at bid price : 17.94 Bid-YTW : 4.78 % |

| BAM.PF.B | FixedReset | -1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 21.22 Evaluated at bid price : 21.22 Bid-YTW : 4.21 % |

| IFC.PR.C | FixedReset | -1.34 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.75 Bid-YTW : 4.73 % |

| ENB.PF.C | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 19.42 Evaluated at bid price : 19.42 Bid-YTW : 4.76 % |

| TRP.PR.G | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 23.02 Evaluated at bid price : 24.67 Bid-YTW : 3.71 % |

| BAM.PF.F | FixedReset | -1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 22.49 Evaluated at bid price : 23.30 Bid-YTW : 4.05 % |

| ENB.PR.N | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 18.92 Evaluated at bid price : 18.92 Bid-YTW : 4.71 % |

| BMO.PR.T | FixedReset | -1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 22.10 Evaluated at bid price : 22.62 Bid-YTW : 3.51 % |

| SLF.PR.J | FloatingReset | -1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.01 Bid-YTW : 7.21 % |

| TD.PF.D | FixedReset | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 22.85 Evaluated at bid price : 24.18 Bid-YTW : 3.58 % |

| CU.PR.C | FixedReset | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 23.31 Evaluated at bid price : 24.27 Bid-YTW : 3.29 % |

| ENB.PR.Y | FixedReset | -1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 17.76 Evaluated at bid price : 17.76 Bid-YTW : 4.75 % |

| MFC.PR.N | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.68 Bid-YTW : 4.71 % |

| CM.PR.O | FixedReset | 1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 22.19 Evaluated at bid price : 22.75 Bid-YTW : 3.53 % |

| RY.PR.N | Perpetual-Premium | 1.04 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2024-11-24 Maturity Price : 25.00 Evaluated at bid price : 25.37 Bid-YTW : 4.79 % |

| HSE.PR.C | FixedReset | 1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 22.64 Evaluated at bid price : 23.62 Bid-YTW : 4.23 % |

| PWF.PR.S | Perpetual-Discount | 1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 23.99 Evaluated at bid price : 24.40 Bid-YTW : 4.98 % |

| TRP.PR.B | FixedReset | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 14.88 Evaluated at bid price : 14.88 Bid-YTW : 3.49 % |

| GWO.PR.I | Deemed-Retractible | 1.31 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.20 Bid-YTW : 5.52 % |

| CU.PR.E | Perpetual-Discount | 1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 23.63 Evaluated at bid price : 24.04 Bid-YTW : 5.14 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BNS.PR.A | FloatingReset | 123,950 | TD crossed 119,400 at 24.20. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.21 Bid-YTW : 2.99 % |

| ENB.PR.H | FixedReset | 78,000 | TD crossed two blocks of 35,000 each, both at 16.80. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 16.70 Evaluated at bid price : 16.70 Bid-YTW : 4.66 % |

| RY.PR.G | Deemed-Retractible | 46,951 | RBC crossed 41,400 at 25.50. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-08-06 Maturity Price : 25.25 Evaluated at bid price : 25.47 Bid-YTW : 0.38 % |

| TD.PF.E | FixedReset | 45,330 | Raymond James bought two blocks of 10,000 each from TD, both at 25.05. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 23.14 Evaluated at bid price : 25.00 Bid-YTW : 3.51 % |

| CM.PR.Q | FixedReset | 40,836 | Raymond James bought 13,500 from anonymous at 24.75. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 23.06 Evaluated at bid price : 24.71 Bid-YTW : 3.48 % |

| RY.PR.J | FixedReset | 38,473 | Raymond James bought 16,300 from TD at 24.65. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-07 Maturity Price : 23.03 Evaluated at bid price : 24.60 Bid-YTW : 3.50 % |

| There were 39 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| SLF.PR.G | FixedReset | Quote: 16.29 – 16.70 Spot Rate : 0.4100 Average : 0.2874 YTW SCENARIO |

| TRP.PR.E | FixedReset | Quote: 22.08 – 22.68 Spot Rate : 0.6000 Average : 0.4882 YTW SCENARIO |

| TD.PF.A | FixedReset | Quote: 22.49 – 22.85 Spot Rate : 0.3600 Average : 0.2482 YTW SCENARIO |

| BAM.PF.B | FixedReset | Quote: 21.22 – 21.64 Spot Rate : 0.4200 Average : 0.3126 YTW SCENARIO |

| PVS.PR.D | SplitShare | Quote: 24.52 – 24.85 Spot Rate : 0.3300 Average : 0.2292 YTW SCENARIO |

| TRP.PR.G | FixedReset | Quote: 24.67 – 25.00 Spot Rate : 0.3300 Average : 0.2312 YTW SCENARIO |